The Dr Ambedkar Central Sector Scheme is a Government of India subsidy that pays your full education loan interest during the moratorium for OBC and EBC students studying abroad for a Master’s, MPhil, or PhD. The OBC family income ceiling is 8 lakh a year and the EBC ceiling is 5 lakh. In my experience it saves 5 to 7 lakh on a typical 20 lakh abroad loan.

The Dr Ambedkar Central Sector Scheme is one of those schemes that sits quietly on a government portal, helps a real number of OBC and EBC students every year, and almost never gets named in the loan brochures your bank hands over. If you are an OBC or EBC student headed abroad for a Master’s, MPhil, or PhD, this scheme can wipe out the entire moratorium interest bill on your education loan. The catch is that the income ceiling is low, the paperwork is specific, and the application has to be timed before disbursement, not after.

I wrote this post because three different readers asked me the same week whether the dr ambedkar central sector scheme education loan subsidy still exists and whether it actually pays out. It does, and it does. Here is the honest version of how it works in 2026.

The Dr Ambedkar Central Sector Scheme provides full interest subsidy during the moratorium period on education loans taken by OBC and Economically Backward Class (EBC) students for approved Master’s, MPhil and PhD programs abroad. The OBC family income ceiling is ₹8 lakh per annum and the EBC ceiling is ₹5 lakh. The Ministry of Social Justice and Empowerment funds the subsidy and the bank credits it directly against your accruing interest, so you start repayment on the original principal only.

Other state and central schemes: the state education loan schemes india post, the education loan kerala post, and the education loan maharashtra bengal UP post.

The Dr Ambedkar scheme is one of several subsidies, and the ceilings decide who gets what. Line them up in the subsidy schemes compared.

What the scheme actually pays for

The scheme pays the entire interest that accrues on your education loan during the moratorium period (course duration plus the standard grace period of 6 to 12 months, capped at one year post-course). The Ministry of Social Justice and Empowerment routes the subsidy through the Canara Bank, which is the nodal bank, and the amount is credited to your loan account so that none of the moratorium interest gets capitalised into your principal.

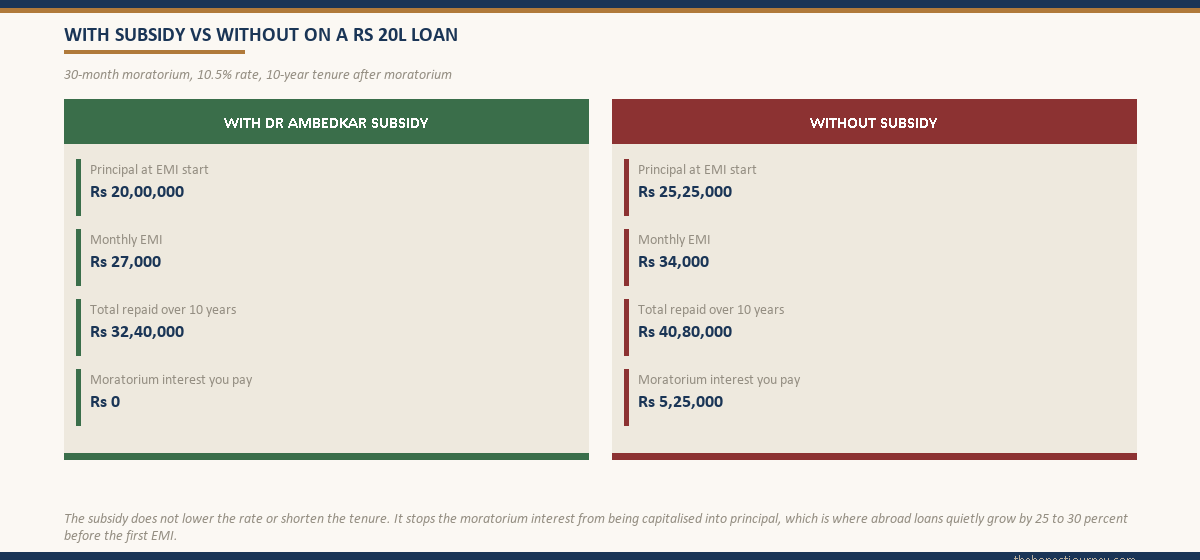

For a real sense of the value: on a ₹20 lakh loan at 10.5% with a 30-month moratorium (2 year Master’s plus 6 month grace), the interest that would normally get added to your balance is around ₹5.25 lakh. Under the Dr Ambedkar scheme, that ₹5.25 lakh is paid by the government. You begin EMIs on ₹20 lakh, not ₹25.25 lakh. The EMI on a 10-year tenure drops from roughly ₹34,000 a month to ₹27,000 a month. Across the full tenure that is close to ₹8.5 lakh less out of your pocket.

Who is eligible

Three filters apply and you have to clear all three.

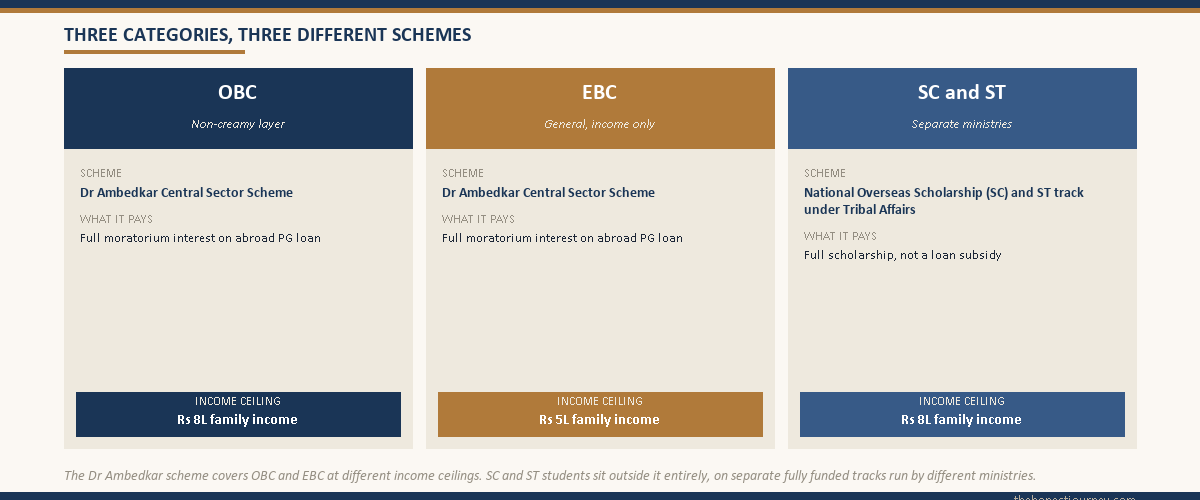

1. Category. The scheme covers two distinct groups under one umbrella: Other Backward Classes (OBC, non-creamy layer) and Economically Backward Classes (EBC) which is a general-category bracket defined by income alone. SC and ST students are not covered by this scheme. There is a separate National Overseas Scholarship for SC students that is a full scholarship, not a loan subsidy, and a different subsidy track for ST students.

2. Income ceiling. Total annual family income from all sources must be at or below ₹8,00,000 for OBC applicants and at or below ₹5,00,000 for EBC applicants. The income is the combined gross of both parents (or guardians) for the financial year preceding the year of application. Form 16, ITRs, salary certificates, or a tehsildar income certificate are the accepted proofs.

3. Course and level. Only postgraduate study qualifies. Master’s, MPhil, and PhD programs at recognised foreign institutions. Undergraduate study, diploma programs, and certificate courses are excluded. The course list is broad and includes Management, Engineering, Pure Sciences, Medicine, Agricultural Sciences, Applied Sciences, Law, Humanities, Social Sciences, and a few others. The institution does not have to be on a fixed list but it has to be a recognised university or institute in the country where you are studying.

Faz's ruleIncome certificate is the single most rejected document. Get it issued for the correct financial year and with the right authority before you submit anything else.

Most rejections I have seen come from an income certificate that is more than 12 months old, issued by the wrong authority, or quoting net income instead of gross. Use the same income proofs you would use for an OBC non-creamy layer certificate. Tehsildar or revenue officer, current FY, all family sources included.

Where this scheme differs from CSIS and from National Overseas Scholarship

Confusion between these three schemes costs students months and sometimes whole windows. Here is the clean separation.

| Scheme | Who it covers | What it pays | Income ceiling | Where you study |

|---|---|---|---|---|

| Dr Ambedkar Central Sector Scheme | OBC and EBC | Full moratorium interest on education loan | ₹8L (OBC), ₹5L (EBC) | Abroad only, PG only |

| CSIS (Padho Pardesh successor for general) | All categories meeting income test | Full moratorium interest on education loan | ₹4.5L | India, undergrad and PG |

| National Overseas Scholarship | SC, Denotified Tribes, Landless Labourers | Full scholarship (tuition, living, travel) | ₹8L family income | Abroad only, PG and PhD |

If you are OBC or EBC and going abroad for a Master’s, the Dr Ambedkar scheme is your track. CSIS covers domestic study and has a lower income ceiling. National Overseas Scholarship is a different beast entirely (a full scholarship) and is only for the categories listed. For a closer look at how CSIS works for families inside the ₹4.5L ceiling, see the CSIS interest subsidy guide.

Which loans qualify

The scheme applies to education loans taken under the Indian Banks’ Association (IBA) Model Education Loan Scheme. In practice that means all public sector banks, most private banks, and a few NBFCs that have signed on to the IBA model. Pure private NBFC loans that do not follow the IBA scheme structure (some specialist abroad-loan NBFCs operate outside it) are not eligible.

The loan must be for an approved professional or technical course at a foreign institution. There is no formal maximum loan amount cap for the loan itself under the scheme. The subsidy covers the full moratorium interest regardless of loan size, provided you meet the income and category criteria. The interest rate the bank charges is set by your loan agreement, not the scheme.

One important detail: the scheme is available only once in the lifetime of a student. If you used the subsidy for a Master’s, you cannot reapply for a PhD subsidy a few years later. Choose your moment carefully if you are planning a multi-stage abroad education.

The application process, step by step

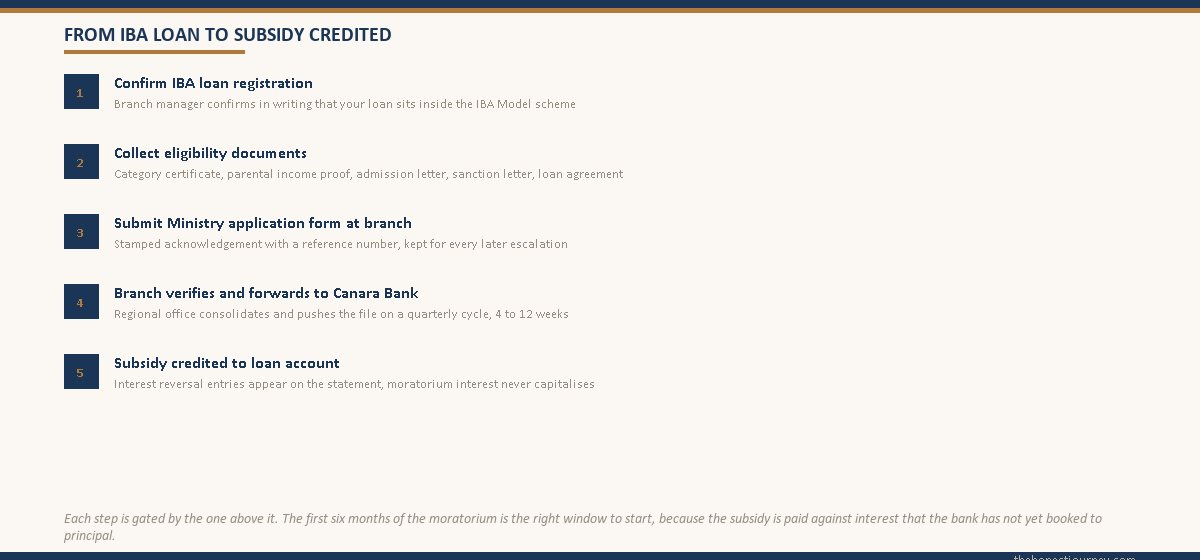

The application happens through the bank that sanctioned your loan, not directly through the Ministry. The bank forwards your file to Canara Bank (the nodal agency), which validates and releases the subsidy. Timeline matters here because the subsidy is intended to cover interest that has not yet been capitalised. Apply late and you may lose months of subsidy.

Step 1. Confirm with your bank that they participate in the scheme. Every public sector bank does. Most private banks do. Ask the branch manager (not the relationship manager who sold you the loan) to confirm in writing that your loan is registered under the IBA Model Education Loan Scheme. If the bank pushes back or seems unsure, that is a sign to escalate to a different branch or a different lender entirely.

Step 2. Collect the eligibility documents. The standard list: OBC non-creamy layer certificate or EBC income certificate (issued for the current financial year, by Tehsildar / SDM / authorised revenue officer), parental income proof for the preceding FY (ITRs, Form 16, salary slips), your admission letter from the foreign institution, the sanction letter from the bank, and the loan agreement.

Step 3. Submit the prescribed application form at your branch. The form is a standard Ministry of Social Justice and Empowerment template. The branch will give it to you. Fill it, attach all documents, and submit. Get a stamped acknowledgement with a reference number.

Step 4. Wait for branch verification and forwarding. The branch verifies your category certificate, income proof, and admission letter, then forwards the full file to its regional office, which consolidates and sends to Canara Bank quarterly. This stage typically takes 4 to 12 weeks. Slower at quarter-end.

Step 5. Track subsidy credit. Once Canara Bank releases the subsidy, your loan account will show interest reversal entries for the moratorium months covered. Check your loan statement. If you do not see entries within six months of submission, escalate first to your branch, then to the Ministry of Social Justice and Empowerment’s grievance channel on the MyScheme portal.

Faz's ruleApply within the first six months of your moratorium. The subsidy is meant to cover interest as it accrues, not interest that has already been capitalised.

Banks have refused or delayed subsidy claims for students who applied in the final year of the moratorium because the interest for the early years had already been booked to principal. Submit your application as soon as your first disbursement clears. Do not wait for the second year.

Common reasons applications get rejected

From the rejections I have seen documented in branch correspondence and on government grievance portals, four issues account for most denials.

Wrong income certificate. The certificate must be for the financial year preceding your application year, must include income from all family sources, and must be issued by an authority empowered to issue OBC NCL or EBC income certificates in your state (usually Tehsildar, SDM, or Revenue Officer). A certificate from a Notary or a Gram Panchayat Pradhan is rejected.

Course or institution does not match the approved list. Diploma courses, short certificate programs, undergraduate degrees, and language courses are excluded. The institution must be a recognised university or equivalent in its country. Online degrees and distance programs do not qualify.

Loan is not under the IBA scheme. Some specialist abroad-loan NBFCs operate on their own product structure, not the IBA model. If your loan was sanctioned by such a lender, the Dr Ambedkar subsidy is not available. This is one of the underrated reasons to prefer a public sector bank or an IBA-aligned lender if you qualify. The education loan for abroad without collateral guide covers which lenders sit inside the IBA framework.

Late application. Applying in your second year of a 2-year course when most of the moratorium interest has already been capitalised leads to partial or full rejection. The scheme is forward-looking and is paid against interest that the bank has not yet booked.

Using Vidyalakshmi alongside the scheme

The PM Vidyalakshmi portal at vidyalakshmi.co.in is the single window for education loan applications and for the central interest subsidy schemes. You can submit a Common Education Loan Application Form (CELAF) to multiple banks at once and the same login lets you initiate your interest subsidy claim through the Jan Samarth track. For Dr Ambedkar specifically, the portal links you to the relevant scheme page and to the Ministry of Social Justice and Empowerment workflow.

The portal does not replace the bank-level application. You still submit the physical form at your branch. But it does give you a unified record of your loan, your application status, and your scheme registration, which is useful if you need to escalate a delay later. For more on using the portal end to end, see the PM Vidyalakshmi portal education loan walkthrough.

What this means for the math on your loan

If you qualify and get the subsidy approved, the entire moratorium-interest trap on your education loan is neutralised. The mechanism is the same as a true zero-interest education loan for the duration of your studies: interest accrues, but you do not pay it and it does not capitalise, because the government has stepped in. You begin EMIs on the original principal. The total cost of your loan drops by the full subsidised amount, which on a typical ₹20L abroad loan is between ₹5L and ₹7L depending on rate and moratorium length.

One caveat. The principal is still yours to repay. The scheme does not forgive the loan. It only kills the interest accumulation during the study years. EMIs after the moratorium are calculated on the original ₹20L at the rate your bank charges, for the tenure you agreed to. If you also want a sense of how the post-moratorium math works without any subsidy (as a reference point), the moratorium period interest post runs the full numbers.

Faz's ruleThe subsidy is real money and it is yours to claim, but the paperwork discipline has to come from you. Banks process, Ministries fund. Neither will chase you to apply.

I have seen perfectly eligible students miss the subsidy entirely because they assumed the bank would file the paperwork automatically. Banks file what you submit. If you do not submit a complete application with the right certificates inside the first six months of moratorium, the money is not coming.

The honest closing take

The Dr Ambedkar Central Sector Scheme is a genuinely useful piece of policy. If you are OBC or EBC, your family income is below the ceiling, and you are headed abroad for a Master’s, this is a subsidy that can save you several lakh rupees over the life of your loan. It will not change the principal you have to repay. It will not lower your interest rate. But it will stop the moratorium-period compounding that quietly inflates abroad-education loans by 25 to 30 percent before repayment even begins.

The friction is real. The paperwork is specific, the timing window is narrow, and a careless income certificate or a late application can lose you the entire benefit. But the work pays back at a rate that few other things in personal finance match. A weekend of certificate gathering and form filling, in exchange for ₹5 to 7 lakh off your total loan cost, is a trade most students would take if they knew the trade was on offer.

The Ministry of Social Justice and Empowerment publishes scheme updates and any revisions to income ceilings or coverage on its official site. The consolidated scheme page is also listed on the MyScheme government portal. Verify the current parameters at the time you apply, because the central schemes do see periodic revisions and the version applicable to you is the one in force on the date of your sanction.

FAQ

What is the Dr Ambedkar Central Sector Scheme interest subsidy?

It is a Government of India scheme administered by the Ministry of Social Justice and Empowerment that pays the full interest accruing on an education loan during the moratorium period for OBC and Economically Backward Class students pursuing approved Master’s, MPhil, or PhD programs abroad. The subsidy is credited directly to your loan account by the nodal bank (Canara Bank), so the moratorium interest does not get capitalised into your principal and your post-moratorium EMI is calculated on the original sanctioned amount.

Is the scheme available for SC and ST students?

No. The Dr Ambedkar scheme is specifically for OBC (non-creamy layer) and EBC (general category, income-based) students. SC students have access to the separate National Overseas Scholarship, which is a full scholarship covering tuition, living, and travel, not a loan interest subsidy. ST students have their own dedicated scheme under the Ministry of Tribal Affairs. These are funded and administered separately and have different application processes and ceilings. Check the relevant ministry portal for the scheme that applies to your category.

What is the income ceiling for the Dr Ambedkar interest subsidy?

The annual family income ceiling is ₹8,00,000 for OBC applicants and ₹5,00,000 for EBC applicants. Family income is the combined gross income of both parents (or guardians) from all sources, calculated for the financial year preceding the year of application. Acceptable proof is the OBC non-creamy layer certificate or the EBC income certificate, issued by a Tehsildar, SDM, or other authorised revenue officer in your state. Certificates issued by a Notary or a Gram Panchayat are not accepted.

Which courses and countries qualify under the scheme?

Only postgraduate study qualifies: Master’s, MPhil, and PhD programs. Approved fields include Management, Engineering, Pure Sciences, Applied Sciences, Medicine, Agricultural Sciences, Law, Humanities, and Social Sciences. The course must be at a recognised university or institute in any foreign country. Undergraduate degrees, diploma programs, short certificate courses, language courses, and online or distance-mode programs are not eligible. The institution does not have to be on a fixed list but it must be a recognised degree-granting body in the country where it operates.

How do I apply for the Dr Ambedkar subsidy?

You apply through the bank that sanctioned your education loan, not directly to the Ministry. Confirm with the branch that your loan is registered under the IBA Model Education Loan Scheme, then submit the prescribed Ministry of Social Justice and Empowerment application form along with your category certificate, parental income proof, foreign institution admission letter, bank sanction letter, and loan agreement. The branch forwards your file through its regional office to Canara Bank, the nodal agency. Apply within the first six months of your moratorium for best results.

How long does it take for the subsidy to be credited?

Processing typically takes 4 to 12 weeks from branch submission to forwarding, and Canara Bank releases subsidy disbursements on a quarterly cycle. In practice, you should see the first interest reversal entries on your loan account within 4 to 6 months of submitting a complete application. If you do not see entries within six months, escalate first to the branch manager, then to the regional office, then to the Ministry through the grievance channel on the MyScheme portal. Keep your stamped acknowledgement and reference number for all escalations.

Can I claim both the Dr Ambedkar scheme and CSIS?

No. The schemes are mutually exclusive. CSIS (the Central Sector Interest Subsidy for general category students with family income below ₹4.5 lakh, applicable to domestic higher education) and the Dr Ambedkar scheme (for OBC and EBC students pursuing abroad PG study) cover different sets of borrowers and you can be on only one at a time. If you are OBC and meet both income ceilings, the Dr Ambedkar scheme is the correct track because CSIS is for India-based study. Confirm the applicable scheme at your branch before filing.

Does the subsidy cover the principal or only the interest?

Only the interest, and only the interest that accrues during the moratorium period (course duration plus the standard 6 to 12 month grace, capped at one year post-course). The principal is fully your responsibility to repay. After the moratorium ends, EMIs are calculated on the original sanctioned principal at the interest rate set in your loan agreement, over the tenure you agreed to. The scheme is a meaningful reduction in total loan cost, often ₹5 to 7 lakh on a ₹20 lakh abroad loan, but it is not a loan waiver and the post-moratorium repayment math still applies.

Faz · The Honest Journey · 2026