An education loan in Kerala usually means stacking a national PSU bank loan with one of three state-level layers: KSFE schemes (which are chitty-secured advances, not pure education loans), KSBCDC loans for OBC and minority students, and the state interest subsidy for SC and ST students. KSBCDC offers up to around ₹20 lakh for overseas study at concessional rates for eligible communities. KSFE provides chitty-backed financing that works as a top-up. The state SC/ST interest subsidy can sit on top of an SBI or Canara Bank loan, and most students in Kerala combine two of these rather than relying on one.

When my neighbour’s daughter got into a master’s program at Trinity College Dublin, the family assumed an SBI Global Ed-Vantage loan was the whole answer. It covered tuition. It did not cover the gap between sanction and the EUR 10K initial deposit Ireland’s immigration office wanted in her account before visa filing. That gap closed with a KSFE chitty her father had been running for seven years, and a KSBCDC top-up loan that came through in six weeks.

That is the Kerala reality. The national bank is the backbone, but the state-level layer is what fills the gaps national guides ignore.

Other state and central schemes: the education loan maharashtra bengal UP post.

What “education loan in Kerala” actually means in 2026

Kerala has three distinct funding tracks that operate alongside the national PSU bank route:

- KSFE (Kerala State Financial Enterprises) education loan and chitty schemes, run by the state-owned NBFC.

- KSBCDC (Kerala State Backward Classes Development Corporation) education loans for OBC, minority and converted Christian communities.

- The Kerala state interest subsidy scheme for SC and ST students, run through the SC Development Department and the Scheduled Tribes Development Department.

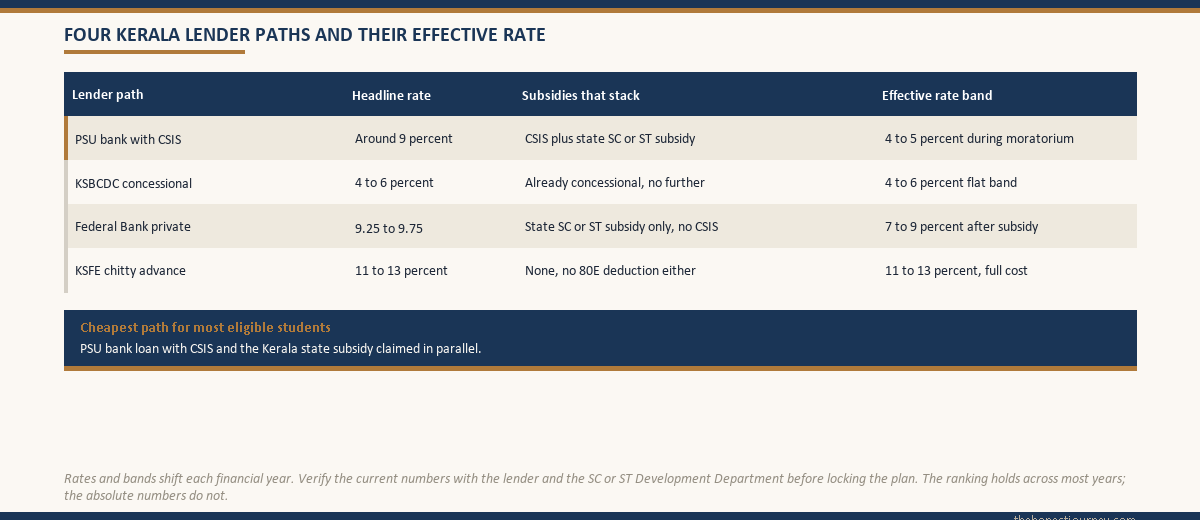

None of these replace the national PSU bank loan. They sit alongside it. A student in Kerala usually has an SBI, Canara, Federal Bank or Bank of Baroda education loan as the core, and one of the state options layered on top to bring the effective interest rate down, cover the proof-of-funds requirement, or fill a gap the national lender will not touch.

The model education loan scheme that PSU banks follow comes from the Indian Banks Association, and the regulator for all of this is the Reserve Bank of India. State schemes are governed by their own corporation rules, which is why eligibility, ceilings and paperwork differ from a normal bank loan.

KSFE education loan and chitty advances, and why the difference matters

This is the part most blogs get wrong, so let me be careful. KSFE runs two distinct things that get called “education loans” loosely:

The first is a structured education loan product offered through select KSFE branches, with tenure and EMI structure similar to a bank loan. The ceiling here is modest, currently around ₹10 lakh for domestic study and slightly higher for overseas at select branches. Interest is in the 11 to 13 percent band, higher than what a PSU bank charges on a subsidised loan but accessible to families that struggle with PSU bank documentation.

The second, which is far more common, is a chitty-secured advance against an existing chitty subscription. This is not an education loan in the regulatory sense. It is a personal loan or advance backed by the chitty you already pay into. KSFE markets this as education financing when families ask, because culturally a chitty is how Kerala households save for big-ticket items, including a child’s higher studies.

The practical difference matters for three reasons. A chitty advance does not qualify for the central CSIS interest subsidy or the state SC/ST subsidy because those subsidies require a recognised education loan from a scheduled bank. A chitty advance also does not get the Section 80E tax deduction on interest paid, because 80E is restricted to loans from approved financial institutions for education. And the repayment moratorium that real education loans give you (course period plus 6 to 12 months grace) does not apply to a chitty advance, which typically starts repayment immediately.

If a KSFE counter tells you they can give you an “education loan” against a running chitty, ask specifically whether it is the structured education loan product or a chitty advance. The paperwork makes it clear. The structured loan has a sanction letter naming the institution and course. The advance is a withdrawal against your chitty subscription with no course-specific terms. Both are useful, but only one gives you the tax and subsidy treatment of a real education loan. KSFE’s own scheme details are at the official KSFE site.

Faz's ruleAsk the KSFE branch whether the product is a structured education loan or a chitty advance, and get it in writing on the sanction document.

I have seen three families in my circle assume their chitty advance would qualify for 80E. It does not. The income tax officer in Kochi has been declining these claims for years, because the loan was not from a scheduled bank or a notified financial institution under the Income Tax Act. If you want the 80E deduction, the loan has to be the right kind of loan.

KSBCDC loans: who qualifies and what the ceiling actually looks like

The Kerala State Backward Classes Development Corporation is the state-level arm that channels concessional-rate education loans to students from OBC communities, minority communities and converted Christian groups listed under the Kerala backward classes order. Eligibility is community-based and income-based.

The broad eligibility outline (verify current numbers at the official KSBCDC site before applying, because the corporation revises these annually):

| Parameter | Typical position (verify on KSBCDC site) |

|---|---|

| Eligible communities | OBC, minority, converted Christian listed in Kerala backward classes order |

| Family annual income ceiling | Currently around ₹6 lakh for most schemes, higher under select sub-schemes |

| Domestic course loan ceiling | Currently around ₹10 lakh |

| Overseas course loan ceiling | Currently around ₹20 lakh for select sub-schemes |

| Interest rate | Concessional, typically in the 4 to 6 percent band depending on the sub-scheme |

| Repayment tenure | Up to 10 years after moratorium |

| Moratorium | Course period plus 6 months grace |

The application route is through the KSBCDC district office or the online portal. Paperwork is heavier than a PSU bank in some respects (community certificate, income certificate, parent’s affidavit) and lighter in others (the corporation does not run a separate CIBIL check the way a bank does).

The honest catch is timeline. A KSBCDC sanction can take 6 to 12 weeks from application to disbursement, sometimes longer if the district office is between batches. If your university semester starts in 8 weeks, KSBCDC alone will not get you there. Most students in this situation file an SBI or Canara application in parallel and treat KSBCDC as the second leg that brings the effective interest rate down once both are running.

State interest subsidy for SC and ST students in Kerala

This is the layer that surprises people most. The Kerala government runs an interest subsidy scheme for SC and ST students that pays the interest portion of an education loan during the moratorium and sometimes the early repayment period, provided the loan is from a scheduled commercial bank and the family income is within the prescribed ceiling.

The key features:

- The loan must be from a scheduled commercial bank (PSU, private or eligible cooperative). KSFE chitty advances do not qualify.

- The family income ceiling is set annually by the SC Development Department or the ST Development Department. Verify the current number with the respective department, because it is revised more often than the corporation websites get updated.

- The subsidy is paid as a direct transfer to the bank loan account, not to the student. The student continues to receive the interest certificate from the bank, and the subsidy shows as a credit on the loan statement.

- The scheme can stack with the central CSIS scheme (Central Sector Interest Subsidy for students with family income up to ₹4.5 lakh studying in approved Indian institutions) where both are claimable, but the rules on double-stacking are tight. Some districts process both, some allow only one. Get this confirmed in writing.

The combination of a PSU bank education loan plus the Kerala state SC/ST subsidy plus CSIS where eligible is the most cost-effective structure available in the state. The effective interest paid by the student during moratorium can drop to near zero in some cases. The detailed mechanics of claiming the central scheme are in my CSIS interest subsidy how to claim post, and the Ambedkar central sector scheme that runs alongside it is covered in Dr Ambedkar central sector scheme education loan.

The official subsidy notifications for all SC and ST scholarship and loan schemes are published on the National Scholarship Portal at scholarships.gov.in, which is the canonical source.

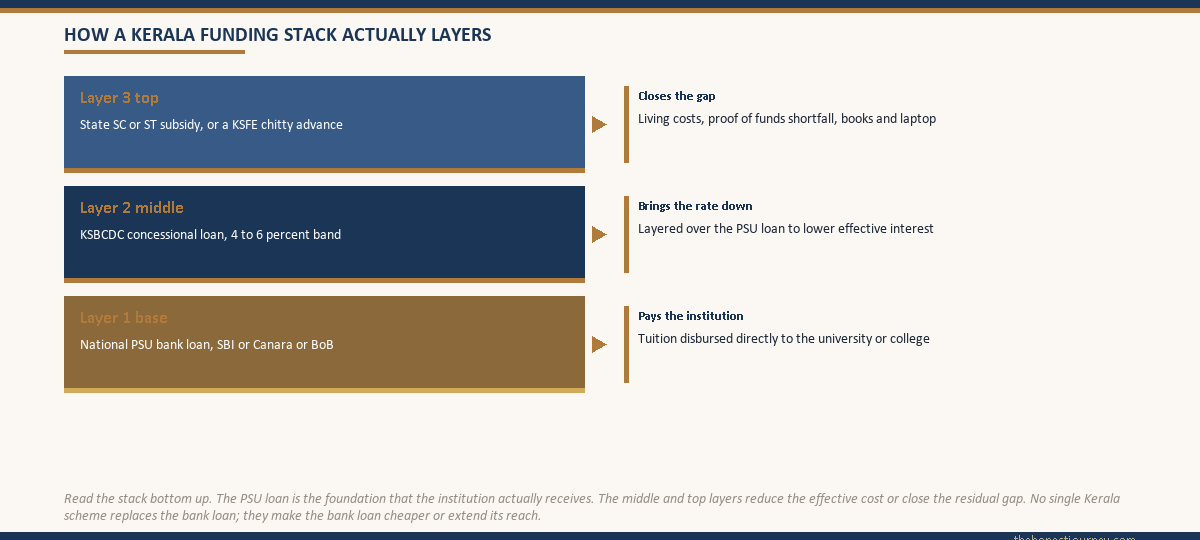

How to stack a national bank loan with a Kerala state scheme

The stacking pattern that works for most Kerala students looks like this:

Tuition portion goes on the national PSU bank loan (SBI, Canara, Bank of Baroda, Federal Bank, Indian Overseas Bank). This is the largest component and the bank pays the institution directly. The mechanics of how the bank releases this in tranches is covered in my education loan disbursement process post.

Living expenses, books, laptop, exam fees and proof-of-funds shortfall go on a second source. For OBC and minority students this is typically KSBCDC at concessional rates. For SC and ST students the state subsidy on the PSU loan plus a small KSFE chitty advance usually covers it. For students outside these categories, a KSFE structured education loan or a parent’s KSFE chitty advance is the common second leg.

Interest subsidy claims go in parallel. CSIS for eligible income brackets in approved Indian institutions, and the Kerala state SC/ST subsidy for the relevant communities. Both run as direct credits to the loan account, so the student does not see them as cash.

Faz's ruleFile the national bank application and the state corporation application in parallel from day one, not sequentially.

The biggest mistake I see in Kerala is treating these as a queue. Family applies to SBI first, waits for sanction, then thinks about KSBCDC. By the time they get to the corporation, the semester is two months away and KSBCDC’s 8-week processing window blows the deadline. Parallel filing means you have both options on the table when you actually need to commit.

When KSFE is the right answer and when it is not

KSFE is genuinely useful in three situations. First, when a family already runs a long-tenure chitty and the chitty maturity aligns with the course start, a structured chitty drawal is cleaner than any loan paperwork. Second, when the national bank has declined the loan (common reasons in Kerala are weak co-applicant CIBIL, a non-tier-1 destination college, or a course the bank does not rate) and the family needs a fallback. Third, when the gap to cover is small (under ₹5 lakh) and the family wants a chitty advance rather than a multi-year loan.

KSFE is the wrong answer when the student needs the 80E tax deduction on interest paid, when the student is eligible for CSIS or state subsidy on a regular education loan, or when the total funding need is large enough that the KSFE ceiling makes it only a partial solution while costing chitty-fee on the whole pot. If the maths shows the family will pay 11 to 13 percent on a KSFE drawal versus 9 percent on a PSU loan with a CSIS or state subsidy bringing the effective cost to 4 to 5 percent, KSFE is the expensive choice.

The honest line is that KSFE is a backup or a top-up, not a substitute for the national bank loan in most cases. The families I have seen use KSFE as the primary funding source were either declined elsewhere or had a chitty culture so deep that the chitty was the trusted path and a bank loan felt foreign. Neither is wrong, but the cost difference compounds across a 10-year repayment.

Federal Bank, South Indian Bank and the Kerala private sector option

Kerala has a strong private sector banking presence, and Federal Bank in particular runs an education loan product that competes directly with PSU banks. The interest rates are typically 25 to 75 basis points higher than SBI, but the processing is faster and the branches are more responsive, especially for students heading to Gulf-region universities and to UK, Ireland and Australia.

South Indian Bank and CSB Bank also offer education loans, with similar positioning. None of these private banks participate in the CSIS scheme the way PSU banks do, so the student loses the central interest subsidy by choosing a private lender. The Kerala state SC/ST subsidy can still be claimed on a private bank loan because the scheme requires only a scheduled commercial bank, not specifically a PSU one. Verify with the SC or ST Development Department before assuming.

The trade-off is speed versus subsidy. If the student is in a hurry and not eligible for CSIS anyway (family income above ₹4.5 lakh, or a non-approved institution), the private Kerala banks are often the cleaner option. If the student qualifies for CSIS, the PSU route saves more than the private bank’s faster processing is worth.

What students underestimate about Kerala state schemes

Three things consistently catch families out.

The community certificate validity. The OBC, SC, ST and minority certificates issued by the village office have a validity period, and KSBCDC and the SC/ST departments will not accept an expired one. Renewal is straightforward but takes 2 to 4 weeks through the village office or the Akshaya centre. Get this done early.

The income certificate threshold. The income certificate that backs the application has to show family income below the scheme’s ceiling. Kerala village offices issue these based on the documents the family submits. If the family has agricultural income, rental income or a small business, the income shown on the certificate has to be defensible if the corporation queries it. Most rejections at the verification stage are about income certificate mismatch with bank statement or ITR.

The disbursement-to-institution rule. State corporation loans, like PSU bank loans, are disbursed directly to the educational institution for the tuition portion. The student does not receive tuition money in their savings account. Families sometimes assume the corporation will hand over a lump sum and the student can pay the university themselves. That is not how any of these schemes work, including KSFE’s structured education loan product.

Faz's ruleGet the community certificate and income certificate renewed at the village office before you start any application, not after the bank asks for them.

The Akshaya centre near my home has a board listing how many days these certificates take. It is on average two weeks. When the corporation or the bank tells you they need a fresh one and you have not started the renewal, you are two weeks behind on a process that is already running tight. Renew first, apply second.

The honest closing take

If I had to write the playbook for a Kerala family planning a child’s higher education funding, it would be this. Open a long-tenure KSFE chitty in the year the child enters Plus Two, so a chitty drawal is available if needed three to four years later. File the national PSU bank application the day the admission offer arrives, and file the KSBCDC application the same week if the family qualifies, treating both as parallel tracks. If the family is SC or ST, register the subsidy claim with the relevant department the day the PSU loan is sanctioned, because the subsidy backfills only from registration date.

Do not treat KSFE as the primary education loan unless the bank has declined and the maths still works after the higher interest. Do not assume the state subsidy will track itself. Do not let the community or income certificate expire mid-process.

The Kerala layer is genuinely an advantage. Most states do not have this much state-level optionality, though it is worth seeing how your state compares in the state education loan schemes across India post before you assume. But the advantage only shows up if the family treats it as a stack to build deliberately, not a backup to fall into when the main plan slips. The national bank loan is the foundation. Everything else makes the foundation cheaper, faster or easier to access, but the foundation still has to be solid first. The base limit on how much a national bank will sanction is covered in my maximum education loan amount India guide, and the common reasons a Kerala application gets declined are walked through in education loan rejection reasons India.

FAQ

What is KSFE education loan?

KSFE runs two distinct products that get called education loans. The first is a structured education loan from select KSFE branches, with a domestic ceiling currently around ₹10 lakh and overseas ceilings slightly higher, at interest rates in the 11 to 13 percent band. The second, far more common, is a chitty-secured advance against an existing KSFE chitty subscription. The chitty advance is technically a personal loan and does not qualify for CSIS, state subsidy or the 80E tax deduction. Always check which product you are being offered.

Who qualifies for a KSBCDC education loan?

KSBCDC loans are for students from OBC, minority and converted Christian communities listed in the Kerala backward classes order, with family annual income typically within around ₹6 lakh for the main schemes. The student must have a confirmed admission to a recognised institution in India or abroad. The community certificate and income certificate from the village office have to be current. Domestic ceilings are currently around ₹10 lakh and overseas around ₹20 lakh for select sub-schemes, with concessional interest in the 4 to 6 percent band.

Can I stack the state subsidy on a national bank loan?

Yes. The Kerala state interest subsidy for SC and ST students applies to a scheduled commercial bank education loan, which includes SBI, Canara, Bank of Baroda, Federal Bank, South Indian Bank and other recognised lenders. The subsidy is paid directly to the loan account as a credit during the moratorium and sometimes the early repayment period. Eligibility requires a current community certificate and the family income within the SC or ST Development Department’s prescribed ceiling for the year. CSIS may also stack where the rules allow, but get the double-stacking confirmed by the district office in writing.

What is the Kerala state interest subsidy ceiling?

The state interest subsidy ceiling is revised annually by the SC Development Department and the ST Development Department, so verify the current number with the relevant department before assuming. The scheme typically covers the interest portion of the loan during the moratorium period and may extend into the early repayment phase under specific sub-schemes. The loan must be from a scheduled commercial bank, the student must be from an eligible community with a valid certificate, and the family income must be within the year’s prescribed ceiling.

Is KSFE chitty the same as a loan?

No. A KSFE chitty is a structured savings instrument where subscribers contribute monthly and rotate withdrawal rights. A chitty advance, which KSFE offers against an existing chitty subscription, is technically a personal loan backed by the chitty. It is not an education loan in the regulatory sense, does not qualify for the central CSIS subsidy or the state SC/ST subsidy, and does not earn the Section 80E tax deduction on interest paid. KSFE also offers a structured education loan product separately, which is a regular education loan and does qualify for those benefits.

How long does KSBCDC take to disburse?

A KSBCDC sanction typically takes 6 to 12 weeks from application to first disbursement, sometimes longer if the district office is between batches. This is materially slower than a PSU bank, which usually moves in 3 to 6 weeks once documents are complete. Most Kerala students file the national bank application and the KSBCDC application in parallel from day one, so the PSU loan covers the immediate semester start while the KSBCDC sanction catches up. Treating them sequentially is the most common reason families miss a deadline.

Can I claim 80E on a KSFE chitty advance?

No. Section 80E of the Income Tax Act restricts the deduction on education loan interest to loans from approved financial institutions or notified charitable institutions for the specific purpose of higher education. A KSFE chitty advance is treated as a personal loan against a chitty subscription, not an education loan. The income tax department has consistently declined 80E claims on chitty advances. If the family wants the 80E deduction, the funding has to come through a recognised education loan from a scheduled bank or KSFE’s structured education loan product, not a chitty drawal.

Which Kerala bank is best for an education loan?

For students who qualify for CSIS or the state SC/ST subsidy, a PSU bank like SBI, Canara or Bank of Baroda gives the lowest effective cost because the subsidies offset interest. For students who do not qualify for any subsidy and need faster processing, Federal Bank or South Indian Bank often clear in less time at interest rates 25 to 75 basis points higher. For OBC and minority students within income limits, KSBCDC alongside a small PSU loan is the cheapest stack. The best lender is the one whose terms match the student’s eligibility profile, not a single bank for everyone.

Faz · The Honest Journey · 2026