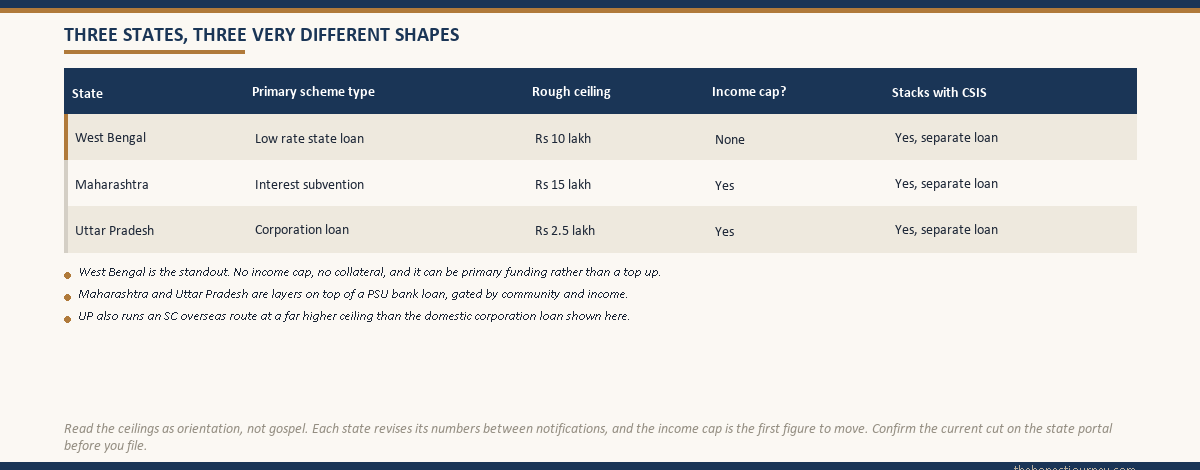

Maharashtra, West Bengal and Uttar Pradesh each run their own education loan and subsidy schemes that layer on top of a regular PSU bank loan, not instead of it. Maharashtra works mainly through interest subvention via the Annasaheb Patil corporation and overseas scholarships for backward classes. West Bengal runs the standout: the Student Credit Card scheme, up to ₹10 lakh at low single-digit interest through state cooperative and nationalised banks. Uttar Pradesh routes most support through its backward-class and SC welfare corporations plus an overseas scheme for SC students. None of these block you from also claiming the central CSIS subsidy on a separate PSU bank loan.

A father in Kolkata wrote to me last month saying his daughter had been told by a relative that the West Bengal Student Credit Card was “basically free money” and by a bank manager that it was “just a normal loan with paperwork.” Both were wrong, and the gap between those two answers is exactly why families either over-rely on a state scheme or ignore it entirely.

This post walks through how Maharashtra, West Bengal and Uttar Pradesh actually structure their state-level education finance in 2026, who qualifies, what the ceilings really are, how the West Bengal scheme stacks with central CSIS, and how the paperwork moves so you can decide what to file and when.

Other state and central schemes: the Dr ambedkar central sector scheme education loan post.

Why state schemes sit alongside central CSIS and PSU bank loans

The central government runs the National Scholarship Portal and the Central Sector Interest Subsidy Scheme (CSIS), which covers moratorium interest on education loans up to ₹10 lakh from scheduled banks for economically weaker section students. State governments run a parallel layer because the central ceiling does not stretch to cover most overseas costs, and because each state has its own welfare corporations with their own budgets and community mandates.

Across Maharashtra, West Bengal and Uttar Pradesh you will meet three kinds of state-level support. First, interest subvention, where the state pays the bank-charged interest on your loan either fully or partly. Second, direct loans from state welfare corporations, usually small ticket and meant for what the bank loan does not cover, except in West Bengal where the direct route is the whole story. Third, outright scholarships or grants for overseas study, which are not loans and simply reduce what you need to borrow.

The rule that governs all of it: the central CSIS and most state interest subsidies apply per loan account, and one loan account can carry only one moratorium interest subsidy. If your PSU bank account is already flagged for CSIS, a state interest subsidy on that same account gets rejected at verification. But a separate state corporation loan, or a West Bengal Student Credit Card account, is a different loan account and runs on its own terms in parallel.

West Bengal: the Student Credit Card scheme

This is the one worth reading slowly, because it is genuinely the most generous mainstream state education loan in the country right now, and it is structured differently from everything else on this page. The West Bengal Student Credit Card scheme is administered through the state and routed via the portal at wbscc.wb.gov.in, with disbursement handled by the West Bengal State Cooperative Bank and participating nationalised and private banks.

The headline numbers. The scheme lends up to ₹10 lakh per student. The interest rate is currently around 4 percent simple interest, with the state government bearing a 1 percent rebate for borrowers who service interest on time, which pulls the effective rate into low single digits. There is no collateral and no margin money requirement up to the ₹10 lakh ceiling. The repayment tenure runs up to 15 years after the moratorium, and the moratorium itself covers the course period plus a grace period.

Eligibility is unusually broad. The student must be a West Bengal resident for at least 10 years, must be enrolled in a recognised institution, and there is no family income ceiling, which is the part that surprises people. Unlike the community-gated schemes in other states, the Student Credit Card is open across categories and income brackets. The age ceiling is currently around 40, which makes it usable for working professionals returning to study, not just school leavers.

What it covers is also wide: school, undergraduate, postgraduate, professional, technical, doctoral, and study abroad. It covers tuition, hostel, books, equipment, and reasonable living expenses, and it can be used for coaching and competitive exam preparation in defined cases. The guardian acts as co-borrower, which is how the scheme keeps the no-collateral promise workable for the state cooperative bank.

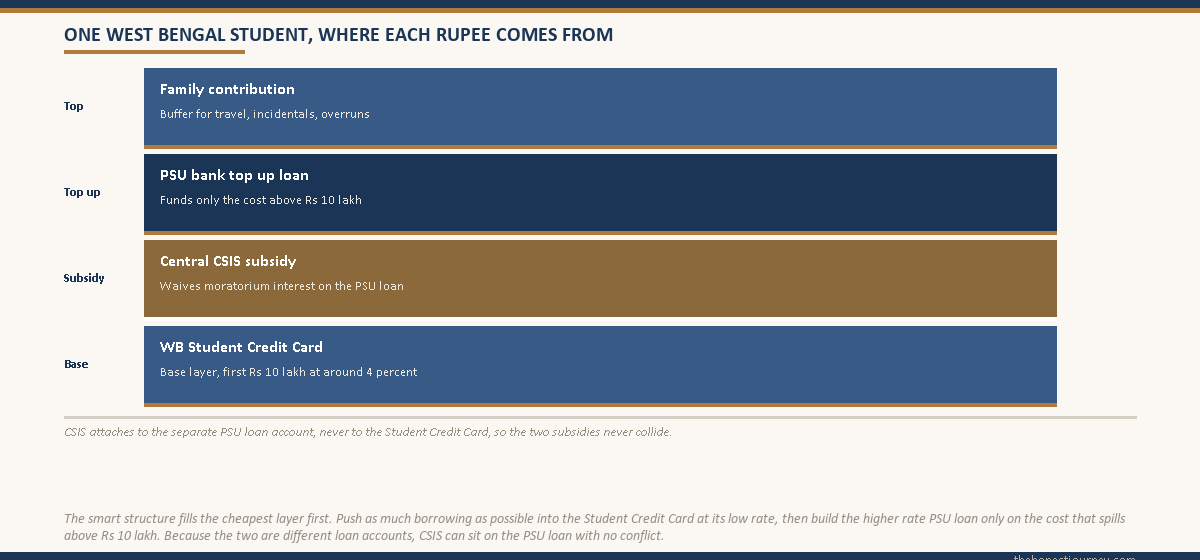

The honest framing point. Because there is no income ceiling and no collateral, families compare it directly to a PSU bank loan and ask why anyone would take the bank route at all. The answer is the ₹10 lakh cap. A one-year UK master’s costing ₹35 lakh cannot be funded by the Student Credit Card alone. The smart structure is to take the Student Credit Card for the first ₹10 lakh at its low rate and arrange a separate PSU bank loan for the balance, which is where the stacking question with CSIS becomes important.

Faz's ruleUse the West Bengal Student Credit Card for the first ₹10 lakh, then layer a PSU bank loan only for the excess.

The mistake I see is families treating the Student Credit Card as either the whole answer or an irrelevance. For a domestic professional course under ₹10 lakh it can genuinely be the whole answer at a rate no bank will match. For an expensive overseas course it covers the cheapest first slice, and you build the bank loan on top for the rest. The rate on the first ₹10 lakh is so low that you want as much of your borrowing as possible sitting inside the Student Credit Card before the higher-rate bank money begins.

How the West Bengal scheme stacks with central CSIS

This is where the per-account rule earns its keep, and the West Bengal case is the cleanest illustration on this page. The Student Credit Card is its own loan account at the state cooperative bank. The central CSIS subsidy attaches to a separate scheduled bank loan account. Because they are two different accounts, they do not collide.

So the structure that produces the lowest effective cost looks like this. Take the West Bengal Student Credit Card for ₹10 lakh at its roughly 4 percent rate with the 1 percent good-conduct rebate. Take a separate PSU bank education loan for the balance, say ₹15 lakh on a ₹25 lakh total. If you qualify under the central scheme (family income up to ₹4.5 lakh, professional or technical course at an accredited institution in India), claim CSIS on the first ₹10 lakh of that separate PSU loan. You now have three layers running at once: a low-rate state loan, a market-rate bank loan, and a central subsidy covering the moratorium interest on part of the bank loan.

What you cannot do is claim CSIS on the Student Credit Card account itself, because the Student Credit Card already carries its own state concessional rate, and that account is not a CSIS-flagged scheduled bank loan in the CSIS sense. You also cannot double up two moratorium interest subsidies on the single PSU bank account. One account, one moratorium subsidy. The mechanics of getting the bank to flag the account correctly are covered in the CSIS interest subsidy how to claim guide, and it is worth getting that flag right before the first disbursement because retrofitting it later is painful.

| Layer | Account | Rough rate | CSIS applies? |

|---|---|---|---|

| WB Student Credit Card (first ₹10 lakh) | State cooperative bank | Around 4 percent | No (already concessional) |

| PSU bank top-up loan (balance) | Scheduled bank | Market rate | Yes, on first ₹10 lakh of this account if eligible |

| Family contribution | None | Zero | Not applicable |

Maharashtra: Annasaheb Patil subvention and the overseas scholarship route

Maharashtra’s state education finance works mostly through interest subvention and overseas scholarships rather than a single flagship low-rate loan like West Bengal’s. The portal for most of the scholarship and subsidy schemes is mahadbt.maharashtra.gov.in, the state’s Direct Benefit Transfer platform, which is also where you track application status.

The Annasaheb Patil Arthik Magas Vikas Mahamandal runs an interest subvention scheme aimed primarily at economically weaker students from the Maratha and certain other communities. Under its individual loan interest refund component, the corporation refunds the interest on a bank loan up to a defined ceiling, currently around ₹15 lakh of loan principal, with the interest borne by the corporation for the eligible period. This is a subvention on a bank loan, which means the per-account stacking rule applies: you choose between the Annasaheb Patil interest refund and central CSIS on a given loan account, you do not get both on the same account.

For overseas study, Maharashtra runs scholarships through several social justice and backward-class welfare departments. The Rajarshi Shahu Maharaj overseas scholarship supports students from designated communities pursuing postgraduate and doctoral study abroad, covering tuition and maintenance up to a published ceiling that varies by country and is revised each notification cycle. Parallel overseas schemes exist for SC students through the Social Justice department and for OBC, VJNT and SBC students through the relevant welfare corporations. These are scholarships, not loans, so they do not interact with CSIS and stack freely with a bank loan.

The honest framing for Maharashtra is that the subvention schemes are real but procedurally heavy, and the ceilings and eligible communities shift between government orders more than in most states. The MahaDBT portal is the single source of truth for the current cut, because secondary guides routinely quote ceilings from notifications that have since been superseded. Verify on mahadbt.maharashtra.gov.in before you assume any number.

Faz's ruleFor Maharashtra subvention, decide upfront whether the state refund beats central CSIS on the same loan, then commit to one.

Because the Annasaheb Patil refund and central CSIS both attach to the bank loan account and you can only claim one, families lose money by assuming they will get both and only discovering the conflict at verification. Compare the two on your actual loan size. CSIS covers full moratorium interest up to ₹10 lakh of loan. The state refund covers interest up to its own ceiling. Pick whichever covers more of your interest bill and flag the account for that one from the start.

Uttar Pradesh: backward-class corporation loans and the SC overseas route

Uttar Pradesh channels most of its education finance through community welfare corporations rather than a single broad scheme, and the social-welfare scholarship and fee-reimbursement layer runs through the state scholarship portal linked from scholarships.gov.in and the UP social welfare department’s own pages.

For backward-class students, the UP Backward Classes Finance and Development Corporation offers education loans at concessional interest for professional and technical courses, with ticket sizes that are modest, currently around ₹1 lakh to ₹2.5 lakh per year depending on course category, and a family income ceiling that the corporation revises periodically. Like the small-ticket schemes in other states, this is meant to ease the family contribution while a bank loan does the heavy lifting, not to fund a full professional course on its own.

For SC students, the relevant SC Finance and Development Corporation runs both a domestic concessional loan and, importantly, an overseas education route for postgraduate and doctoral study abroad. The overseas component carries a materially higher ceiling than the domestic loans, with interest subsidy or direct support depending on the category, confirmed admission to a recognised foreign university, an age ceiling typically around 35, and a family income ceiling published with each year’s notification. The structure mirrors the SC overseas schemes other states run.

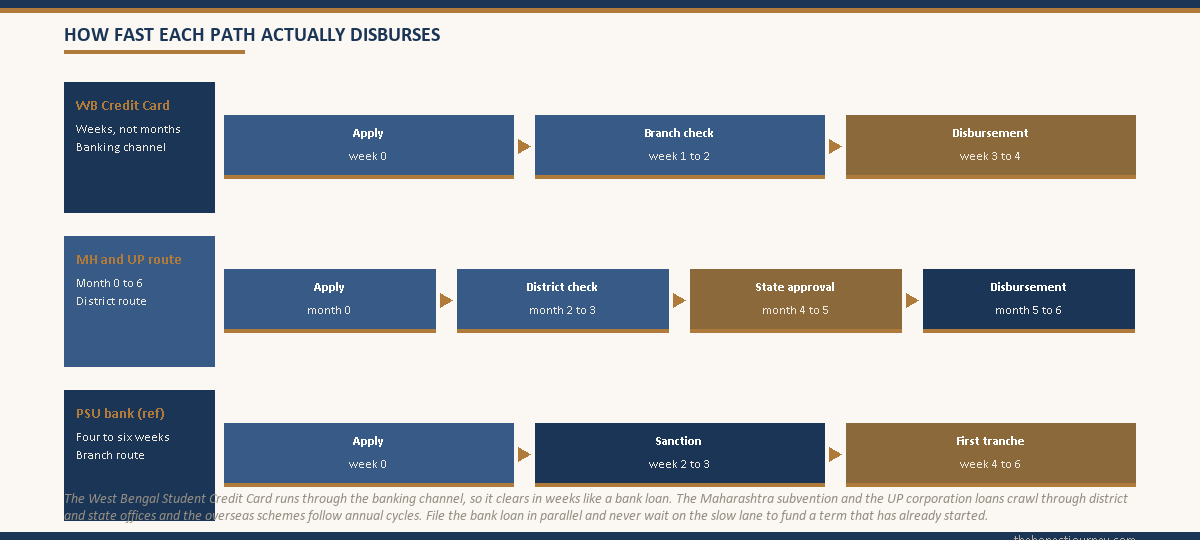

The honest framing for Uttar Pradesh is on processing reality. The corporation loans move through district-level offices and then up for sanction, and the timelines I have seen run longer and less predictably than the bank route. For a domestic professional course, the corporation loan is best treated as a top-up filed in parallel with a PSU bank loan, never as the primary funding you wait on. For the SC overseas scheme, because it runs on a notification cycle, you have to track the window precisely, since missing it means a twelve-month wait.

How state support stacks (or does not) with central CSIS

The single rule that decides everything: one loan account can claim only one moratorium interest subsidy. Once you internalise that, the three states sort themselves cleanly.

West Bengal Student Credit Card. Separate account at the state cooperative bank with its own low rate. A PSU bank loan you take for the excess above ₹10 lakh is a different account and can claim CSIS if you qualify. The two stack with no conflict. This is the cleanest stack on this page.

Maharashtra Annasaheb Patil interest subvention. This attaches to a bank loan account, so it competes with central CSIS on that same account. You choose one. The Maharashtra overseas scholarships, by contrast, are not subsidies on a loan account, so they stack freely with both a bank loan and CSIS.

Uttar Pradesh corporation loans. A corporation loan is a separate account from your PSU bank loan, so a PSU loan with CSIS and a corporation loan with its own concessional terms run in parallel without colliding. The SC overseas scheme, where it is structured as a scholarship or direct support, stacks freely; where it is structured as an interest subsidy on a bank loan, the per-account rule applies.

| State scheme | Type | Stacks with CSIS on a separate PSU loan? | Stacks with CSIS on the same loan? |

|---|---|---|---|

| WB Student Credit Card | Low-rate state loan (separate account) | Yes | Not applicable (different lender) |

| Maharashtra Annasaheb Patil | Interest subvention on bank loan | Yes | No |

| Maharashtra overseas scholarships | Scholarship (non-repayable) | Yes | Not applicable |

| UP BC / SC corporation loans | Direct loan (low interest) | Yes | Not applicable |

| UP SC overseas scheme | Scholarship or subsidy (varies) | Yes | Depends on structure |

For the full picture of how the central scheme verifies family income and flags the loan account, the CSIS interest subsidy guide covers the claim mechanics. For how these three states fit the broader national picture alongside Kerala, Karnataka, Tamil Nadu and Telangana, the state education loan schemes in India overview maps the whole landscape.

The paperwork delay, and when it stops being worth it

Every scheme here except the West Bengal Student Credit Card carries the same structural lag. Applications get processed by district welfare or corporation offices, sent up for state approval, then routed back for disbursement, while a PSU bank clears a clean file in four to six weeks inside its own credit machinery.

The West Bengal Student Credit Card is the exception worth noting. Because it is delivered through the banking channel rather than a welfare corporation, disbursement is faster and more predictable than the typical state portal route, though it still involves more documentation than a plain bank loan. The Maharashtra subvention and overseas schemes and the Uttar Pradesh corporation loans run slower, and the overseas schemes in both states run on annual notification cycles where missing the window costs a year.

The decision matrix that actually works:

- If you are a West Bengal resident under the ₹10 lakh ceiling for a domestic course, the Student Credit Card is likely your primary funding, not a top-up. Build everything else around it.

- If the state scheme is a scholarship (Maharashtra overseas, UP SC overseas where structured as a grant), it is worth waiting for the notification result before locking the bank loan amount, because the scholarship materially shrinks the loan needed.

- If the state scheme is interest subvention on the same loan account as your PSU loan (Maharashtra Annasaheb Patil), decide upfront which subsidy covers more interest, central CSIS or the state refund, and flag the account for that one before disbursement.

- If the state scheme is a small-ticket corporation loan (UP BC or SC domestic loans), file the PSU bank loan first, lock the sanction, and let the corporation loan top up afterwards. Do not let a ₹2 lakh corporation loan delay a ₹15 lakh bank sanction.

- If family income exceeds the scheme ceiling and no income-blind option exists, the question collapses to PSU bank loan plus, where eligible, CSIS. The West Bengal Student Credit Card is the notable income-blind exception.

For families sizing the total loan before any subsidy, the maximum education loan amount in India guide walks through the PSU bank ceilings under SBI Global Ed-Vantage, BOB Vidya, Canara and the rest, which is the number you build the state layer around.

What to confirm before you file

The portals publish notifications and forms, but the people who move the file are at the district level. For West Bengal that is the participating bank branch handling the Student Credit Card. For Maharashtra it is the MahaDBT helpdesk and the relevant welfare department. For Uttar Pradesh it is the BC or SC corporation district office.

The questions worth asking before you upload a single document. What is the current sanctioned ceiling for my course category this year, not last year. What is the current family income ceiling for my scheme, if any. Whether disbursement goes to the institution or to the student. Whether the institution is on the scheme’s approved list, since state schemes maintain lists separate from UGC and AICTE. And for the interest-subvention schemes specifically, whether claiming the state benefit will block central CSIS on the same loan, so you choose deliberately rather than discover the conflict at verification.

One West Bengal specific. Because the Student Credit Card has no income ceiling, families sometimes assume eligibility is automatic and skip confirming the 10-year residency proof and the co-borrower guardian documentation, which are the two things branches most often send back. Get those right before you submit and the file tends to move quickly.

Faz's ruleConfirm whether a state interest subvention will block central CSIS before you choose, not after the bank flags the account.

The most expensive avoidable mistake on this page is in Maharashtra: assuming you can stack the Annasaheb Patil interest refund and central CSIS on the same bank loan, building your budget on both, and then learning at verification that you only get one. Run the comparison on your actual loan size first. Whichever covers more of your moratorium interest is the one to claim, and you tell the bank which subsidy to flag the account for from the very first disbursement.

The honest closing take

West Bengal stands apart on this page. The Student Credit Card is the rare state scheme that can genuinely be primary funding rather than a top-up, because it is income-blind, collateral-free, and priced at a rate no bank will match on the first ₹10 lakh. For a West Bengal resident on a domestic course under that ceiling, it should be the first thing you reach for, with a PSU bank loan and CSIS layered on only if the total exceeds ₹10 lakh.

Maharashtra and Uttar Pradesh follow the more common pattern. Their support is real money but it is a layer on top of the bank route, gated by community certificates and income ceilings, and slowed by district-level processing. The families who win are the ones who file the bank loan in parallel, who decide deliberately between a state subvention and central CSIS where the two compete, and who treat overseas scholarships as something to wait for only because the grant is large enough to reshape the whole loan.

One final piece of honest framing. Ceilings, interest rebates and approved lists in all three states change between notifications, which is why the numbers here are written as “currently around X.” Before filing anything, open the relevant portal, the West Bengal Student Credit Card portal at wbscc.wb.gov.in, MahaDBT at mahadbt.maharashtra.gov.in, or the central National Scholarship Portal, and read the current notification end to end. The RBI framework and the Indian Banks’ Association model education loan scheme remain the two reference points for what the bank loan structure looks like in any given year.

FAQ

What is the West Bengal Student Credit Card scheme?

It is a state-backed education loan of up to ₹10 lakh, delivered through the West Bengal State Cooperative Bank and participating banks via the portal at wbscc.wb.gov.in. The interest rate is currently around 4 percent simple, with a 1 percent state rebate for borrowers who service interest on time, pulling the effective rate into low single digits. There is no collateral, no margin money up to the ceiling, and crucially no family income ceiling. Repayment runs up to 15 years after the moratorium, and it covers school, college, professional, doctoral and overseas study.

Can I stack the West Bengal Student Credit Card with central CSIS?

Yes, because they sit on different loan accounts. The Student Credit Card is its own account at the state cooperative bank with its own concessional rate, and you do not claim CSIS on it. If your total cost exceeds the ₹10 lakh ceiling, you take a separate PSU bank loan for the balance and can claim central CSIS on the first ₹10 lakh of that separate account if you qualify. The result is a low-rate state loan, a market-rate bank top-up, and a central subsidy on part of the bank loan, all running at once.

What education loan support does Maharashtra offer?

Maharashtra works mainly through interest subvention and overseas scholarships rather than a single low-rate loan. The Annasaheb Patil corporation refunds interest on a bank loan up to a ceiling currently around ₹15 lakh of principal for eligible students. Several departments run overseas postgraduate and doctoral scholarships, including the Rajarshi Shahu Maharaj scheme for designated communities and parallel SC and OBC schemes. Most schemes are tracked on the MahaDBT portal at mahadbt.maharashtra.gov.in, which is the reliable source for current ceilings since secondary guides often quote superseded numbers.

What education loan schemes does Uttar Pradesh run?

Uttar Pradesh channels support through community welfare corporations. The Backward Classes Finance and Development Corporation offers concessional education loans, currently around ₹1 lakh to ₹2.5 lakh per year for professional courses, with a periodically revised income ceiling. The SC Finance and Development Corporation runs both domestic concessional loans and an overseas route for postgraduate and doctoral study abroad with a higher ceiling, age limit typically around 35, and confirmed admission required. These corporation loans are best treated as top-ups filed in parallel with a PSU bank loan.

Is there a family income ceiling for the West Bengal Student Credit Card?

No, and this is what sets it apart from most state schemes. The Student Credit Card has no family income ceiling, which means middle-class and even higher-income West Bengal families qualify, unlike the community-gated and income-capped schemes in Maharashtra and Uttar Pradesh. The main eligibility conditions are West Bengal residency for at least 10 years, enrolment in a recognised institution, an age ceiling currently around 40, and a guardian acting as co-borrower. The two items branches most often return are the residency proof and the co-borrower documentation, so confirm those before submitting.

Can I claim Maharashtra interest subvention and central CSIS together?

Not on the same loan account. The Annasaheb Patil interest refund attaches to a bank loan account, and central CSIS also attaches to a bank loan account, and one account can carry only one moratorium interest subsidy. You choose whichever covers more of your interest bill, then flag the account for that one from the first disbursement. Maharashtra overseas scholarships are different: a scholarship is not a subsidy on a loan account, so it stacks freely with both a bank loan and central CSIS with no conflict at verification.

How fast does each state scheme disburse?

The West Bengal Student Credit Card is the fastest because it runs through the banking channel rather than a welfare corporation, though it still needs more documentation than a plain bank loan. Maharashtra subvention and overseas schemes and Uttar Pradesh corporation loans run slower, through district verification and state approval, and the overseas schemes follow annual notification cycles where missing the window costs a year. A PSU bank loan, by comparison, sanctions in four to six weeks for a clean file, which is why families file the bank application in parallel.

Should I wait for the state scheme or take a bank loan now?

It depends on the scheme type. If you are a West Bengal resident under the ₹10 lakh ceiling, the Student Credit Card is likely your primary funding, so build around it. If the state benefit is a large overseas scholarship, it is worth waiting for the notification result because the grant materially shrinks the loan. If it is a small-ticket corporation loan or a subvention worth less than the bank route, file the PSU bank loan first, lock the sanction, and let the state layer top up afterwards rather than missing the academic year start.

Faz · The Honest Journey · 2026