Karnataka, Tamil Nadu and Telangana each run their own state education loan and subsidy schemes that sit on top of, not instead of, a regular PSU bank education loan. Karnataka’s Arivu scheme through KMDC offers interest-free loans currently around ₹1 lakh for minority community students in professional courses. Tamil Nadu’s Adi Dravidar Welfare Department gives interest subsidy and direct loans for SC students with ceilings currently around ₹1.5 lakh domestic and higher for overseas. Telangana’s Mahatma Jyotiba Phule BC Welfare overseas scholarship pays up to ₹20 lakh for BC students going abroad. None of these block you from also claiming the central CSIS subsidy on a separate PSU bank loan, but you cannot claim two subsidies on the same loan account.

A student in Hyderabad asked me last month whether she should wait six months for her state scheme approval or take an SBI loan now and lose the subsidy. The honest answer is that this is the wrong framing. The state scheme and the PSU loan are not competing options. They are layers, and most families who get the math right run both in parallel.

This post walks through how Karnataka, Tamil Nadu and Telangana actually structure their state-level education finance, who qualifies, what the ceilings really are in 2026, and how the paperwork moves so you can decide whether the wait is worth it.

Other state and central schemes: the education loan maharashtra bengal UP post.

Why state schemes exist alongside central CSIS and PSU bank loans

The central government runs the National Scholarship Portal and the Central Sector Interest Subsidy Scheme (CSIS) for economically weaker section students taking education loans up to ₹10 lakh from scheduled banks. State governments run a parallel layer, partly because the CSIS ceiling does not cover most overseas costs and partly because each state has its own community welfare corporations with their own budgets.

The result is three categories of state-level support you will encounter when researching education loan state schemes Karnataka Tamil Nadu Telangana. First, direct loans from state welfare corporations, usually small ticket and meant for fees the bank loan does not cover. Second, interest subsidy on bank loans, where the state government pays the bank-charged interest on your behalf either fully or partially. Third, outright scholarships or grants which are not loans at all, but reduce the amount you need to borrow.

The thing to understand before reading state-by-state is that the central CSIS and most state interest subsidies apply per loan account. If you have one PSU bank loan for ₹7 lakh and CSIS covers your moratorium interest on the first ₹10 lakh, a state subsidy on the same loan account is usually disallowed by the state portal because the bank account is already flagged as CSIS-claimed. But if you have a state corporation loan of ₹1.5 lakh from a different lender and a PSU bank loan of ₹7 lakh, both can run with their respective subsidies.

Karnataka: KMDC Arivu scheme and the state minority loan layer

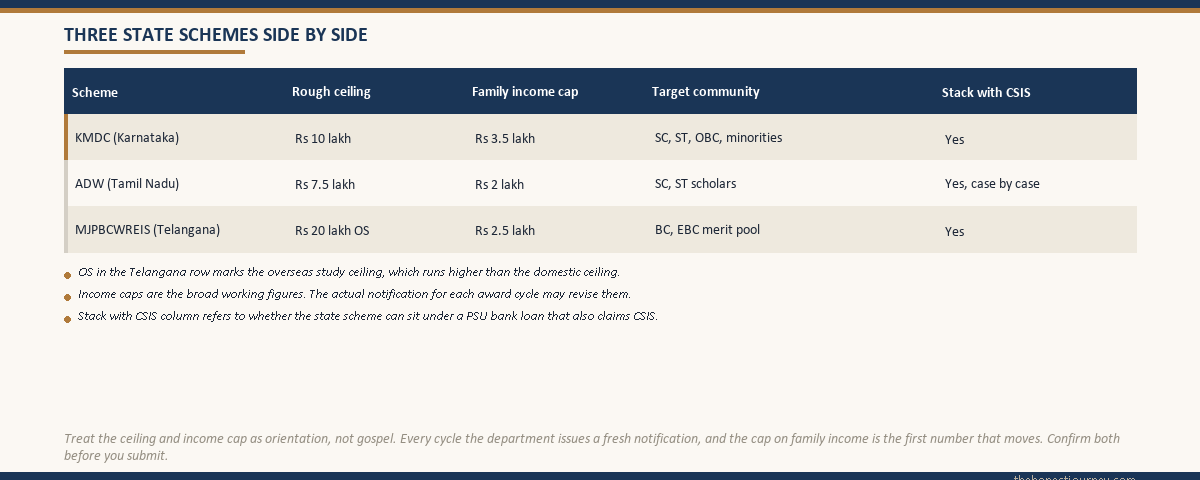

Karnataka’s flagship education finance scheme for minority community students is the Arivu Educational Loan Scheme, administered by the Karnataka Minorities Development Corporation. The scheme is open to students from Muslim, Christian, Jain, Sikh, Buddhist and Parsi communities domiciled in Karnataka, with a family income ceiling currently around ₹6 lakh per year for general courses and slightly higher for professional courses.

The Arivu loan is interest-free for the moratorium and carries a token interest rate (currently around 2 percent) during repayment. The ticket size is small. For diploma and undergraduate professional courses, the loan is currently around ₹50,000 to ₹1 lakh per year. For postgraduate medical and engineering, the ceiling rises but remains far below what a private MBBS seat actually costs. This is the first honest framing point: Arivu is not designed to fund your entire course. It is designed to take pressure off the family contribution while you also take a bank loan.

Applications open on the KMDC portal at kmdc.karnataka.gov.in usually in the July to September window each academic year, though dates shift. The paperwork is heavier than a bank loan: caste certificate, income certificate, domicile, admission letter, fee structure, two guarantors who are government employees or income tax payers, and bank account details. The disbursement happens directly to the institution.

Beyond Arivu, Karnataka also runs the Dr Babu Jagjivan Ram Loan-cum-Grant scheme through the Karnataka SC/ST Development Corporation for SC and ST students, and a parallel BC welfare corporation scheme. The framework is similar: small ticket, low or zero interest, requires community certificate, runs alongside (not instead of) a bank loan.

Faz's ruleTreat the Karnataka state scheme as the second loan in your stack, not the first.

The mistake families make is applying to KMDC, waiting for the result, and only then approaching SBI or Canara Bank. By the time the state approval lands, the academic year has started and the bank file gets rushed. The cleaner sequence is to file the PSU bank application first, lock in the sanction, and apply to KMDC in parallel so the state loan tops up whatever the bank loan does not cover.

Tamil Nadu: Adi Dravidar Welfare loans and the SC overseas scheme

Tamil Nadu’s state education finance for Scheduled Caste students runs through the Adi Dravidar and Tribal Welfare Department, with applications routed via the official state portal at tn.gov.in and the department’s own scheme pages. The department runs two distinct products that often get conflated in online guides.

The first is the domestic education loan and stipend scheme for SC students pursuing professional courses inside Tamil Nadu. The ceiling has historically sat around ₹1 lakh to ₹1.5 lakh per year for engineering, medicine and similar courses, with the state covering either the full interest during the course period or paying the institution directly. Family income ceilings apply, currently around ₹2.5 lakh for the full grant tier and higher tiers for partial support. The course must be at a recognised Tamil Nadu institution, and the application requires community certificate, income certificate, admission letter and parent’s nativity proof.

The second product is the overseas education loan scheme for SC students pursuing postgraduate or doctoral studies abroad. The ceiling here is materially higher, currently around ₹15 lakh to ₹20 lakh depending on country, with interest subsidy and in some categories full state coverage of fees. The eligibility is stricter: confirmed admission to a ranked overseas university (most state portals reference QS rankings or similar), age ceiling typically 35, family income ceiling typically ₹6 lakh.

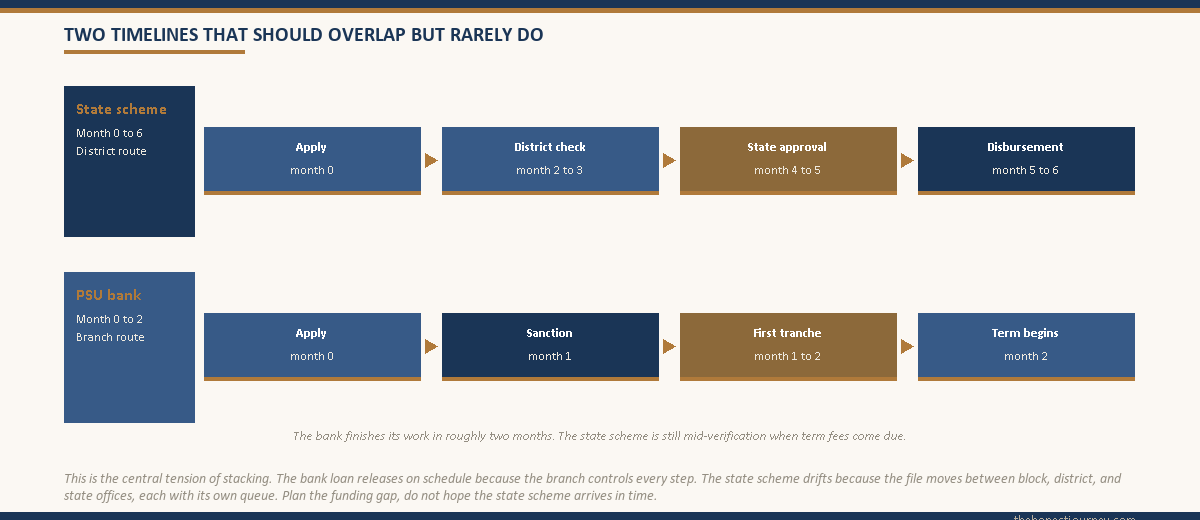

The honest framing here is on the timeline. The Tamil Nadu state portal applications are processed by district welfare officers and then reviewed at the state level. End-to-end timelines I have seen range from three to nine months, with overseas cases on the slower end because additional verification is needed. If your course starts in September and you only apply to the state scheme in May, you are running against the clock. PSU banks can sanction in four to six weeks; the state portal cannot.

Tamil Nadu also runs the Backward Classes, Most Backward Classes and Minorities Welfare Department schemes through parallel corporations. Each has its own income ceiling, course list and ticket size, and each requires the relevant community certificate. The pattern across all of them is the same: state scheme is meant to layer onto a bank loan, not replace it.

Telangana: Mahatma Jyotiba Phule BC Welfare overseas scholarship

Telangana runs one of the more generous state-level overseas finance schemes in the country through the Mahatma Jyotiba Phule Telangana Backward Classes Welfare Residential Educational Institutions Society, commonly shortened to MJPBCWREIS and reachable at mjpbcwreis.cgg.gov.in. The headline product is the overseas scholarship for BC students pursuing postgraduate studies abroad.

The scheme currently covers up to ₹20 lakh of expenses for BC, EBC and similar communities under Telangana’s state list. Eligibility broadly requires Telangana domicile, BC community certificate, family income ceiling currently around ₹5 lakh per year, confirmed admission to a recognised foreign university, and age ceiling typically 35. The list of approved countries and university tiers is published with each year’s notification, so the official portal is the only reliable source for the current cut.

The Telangana scheme is, in practice, a scholarship rather than a loan. It does not need to be repaid as long as the student completes the course and submits the required progress reports. This is important because it changes the math. A Telangana BC student going to a UK university for a one-year master’s costing ₹35 lakh in total could realistically run a ₹20 lakh scholarship from MJPBCWREIS alongside a ₹15 lakh PSU bank loan, leaving zero family contribution if the documentation lines up.

For SC students, Telangana runs a parallel Ambedkar Overseas Vidya Nidhi scheme through the Scheduled Castes Development Department, with similar ceilings and similar paperwork. For ST students, the Tribal Welfare Department runs an equivalent scheme. The eligibility differs by community certificate but the structural design (state scholarship plus bank loan plus family) is consistent.

Faz's ruleIf you qualify for a Telangana overseas scholarship, file it first and shape the bank loan around what is left.

The Telangana overseas schemes are large enough to materially shrink the loan you need, which means the loan terms (rate, tenure, collateral) become a much smaller part of the overall cost. This is the one situation where I tell families to slow down the bank application until the state notification result is in, because a ₹20 lakh non-repayable grant is worth waiting two months for. It flips the entire financial picture.

How state subsidy stacks (or does not stack) with central CSIS

This is the question I get more than any other on state schemes, and the answer is more specific than the online guides admit. The Central Sector Interest Subsidy Scheme (CSIS) covers moratorium interest on education loans up to ₹10 lakh from scheduled banks, for students from economically weaker sections (annual family income up to ₹4.5 lakh) pursuing professional or technical courses at NAAC accredited or NBA approved institutions in India. The subsidy is paid directly by the central government to the bank against your loan account.

The rule is straightforward: one loan account can claim only one moratorium interest subsidy. So if your PSU bank loan account is already flagged for CSIS, a state government interest subsidy cannot be claimed on the same account. The state portal will reject it at the verification stage because the bank account is already tagged.

But if you have two separate loan accounts (one PSU bank loan and one state corporation loan), they are treated independently. The PSU loan can claim CSIS if you qualify under the central scheme. The state corporation loan can carry its own state-level concessional terms. Most state corporation loans are already concessional (zero interest during moratorium, 2 to 4 percent post-moratorium), so the question of stacking a separate subsidy on them rarely comes up.

The scholarship route (Telangana MJPBCWREIS, Tamil Nadu overseas scheme) is even cleaner. A scholarship is not a subsidy on a loan account. It is a direct payment to you or to the institution, and it does not interact with CSIS at all. So a student can run a Telangana overseas scholarship plus a PSU bank loan plus CSIS on the bank loan portion, with all three layers active simultaneously. This is the structure that gets the lowest effective cost, and it is the structure most families either do not know about or do not have time to assemble.

| State scheme | Type | Stacks with CSIS on a separate PSU loan? | Stacks with CSIS on the same loan? |

|---|---|---|---|

| Karnataka KMDC Arivu | Direct loan (low interest) | Yes | Not applicable (different lender) |

| Karnataka SC/ST Corp loans | Direct loan (low interest) | Yes | Not applicable |

| TN Adi Dravidar domestic | Loan with state interest cover | Yes | No |

| TN SC overseas scheme | Loan with state interest cover | Yes | No |

| Telangana MJPBCWREIS | Scholarship (non-repayable) | Yes | Not applicable |

| Telangana Ambedkar Overseas | Scholarship (non-repayable) | Yes | Not applicable |

For deeper detail on how the central scheme works and the documentation banks need to flag a loan account as CSIS, the CSIS interest subsidy how to claim guide covers the claim mechanics end to end. The Dr Ambedkar central sector scheme guide covers the parallel OBC central scheme.

The paperwork delay, and when it stops being worth it

Every state scheme on this page has the same structural issue. State portal applications get processed by district-level welfare officers, sent up for state-level approval, and then routed back for disbursement. The PSU bank route, by contrast, sits inside one bank’s credit machinery and clears in four to six weeks for a clean file.

What this means in practice. Karnataka KMDC Arivu approvals I have seen take three to six months from filing to first disbursement. Tamil Nadu Adi Dravidar domestic schemes have run faster, currently around two to four months for clean files at the district level. The Tamil Nadu and Telangana overseas schemes run on a notification cycle, meaning applications are accepted in defined windows (usually once a year) and decisions are announced together. If you miss the window, you wait twelve months.

The decision matrix that actually works:

- If the state scheme is a scholarship (Telangana MJPBCWREIS, Telangana Ambedkar Overseas, TN SC overseas), it is worth waiting for the notification result before locking the bank loan amount, because the scholarship materially shrinks the loan needed.

- If the state scheme is a small-ticket loan (Karnataka Arivu currently around ₹1 lakh, similar state corporation schemes), file the PSU bank loan first, lock the bank sanction, and let the state loan top up afterwards. Do not let a ₹1 lakh state loan delay a ₹15 lakh bank sanction.

- If the state scheme is interest subsidy on the same loan account as your PSU loan, decide upfront which subsidy is better. Central CSIS covers full moratorium interest up to ₹10 lakh of loan. Some state subsidies cover the same interest but cap at a lower loan amount or higher income ceiling. Read the latest notification before deciding.

- If the family income exceeds the state scheme ceilings, the state scheme is closed regardless of community certificate, and the entire question collapses to PSU bank loan plus (where eligible) CSIS.

For families weighing the question of total loan size before any subsidy, the maximum education loan amount in India guide walks through the PSU bank ceilings under SBI Global Ed-Vantage, BOB Vidya, Canara and the rest. For state-level guidance on Kerala specifically (KSFE, K-FED, the Kerala state subsidy structure), the Kerala education loan guide covers that separate ecosystem.

What to ask the district welfare office before you file

The state portals publish notifications and forms, but the people who actually move the file are at the district welfare office (Karnataka district minorities officer, Tamil Nadu district Adi Dravidar welfare officer, Telangana district BC welfare officer). A short visit before filing saves weeks of back and forth.

The questions worth asking in that visit. What is the current sanctioned ticket size for my course category this year, not last year. What is the current family income ceiling for my community. How many applications has the office cleared so far this cycle and how many are pending. Whether the disbursement is going directly to the institution or to the student’s account. Whether the institution is on the approved list for this scheme (state schemes maintain their own approval lists separate from UGC or AICTE).

The other thing worth confirming. Some state schemes require the student to have first attempted a PSU bank loan and been refused, or to have a PSU loan sanction letter on file. Karnataka and Tamil Nadu schemes have, in some recent notifications, asked for a bank rejection letter or sanction letter as supporting paperwork. This is meant to demonstrate that the state loan is genuinely needed, but it changes the sequence: you cannot file the state application without first having a bank file. The district office will know the current rule for the current notification.

Faz's ruleVisit the district welfare office in person before filing the state portal application.

The district staff have institutional knowledge of which documents the state reviewer rejects, which institutions are currently approved, and which application windows are about to close. The portal page does not tell you any of this. A thirty minute visit before you upload a single document tends to save a couple of months of clarification cycles. Take printed copies of everything.

The honest closing take

State education loan and scholarship schemes in Karnataka, Tamil Nadu and Telangana are real money, but they are not a shortcut around the PSU bank route. They are a layer on top. The families who get the most out of them are the ones who treat the state scheme and the bank loan as parallel processes, not sequential, and who understand which subsidy belongs on which loan account.

The ones who lose are the ones who wait six months for a state approval that ends up being ₹1 lakh, miss the academic year start, and then take a rushed bank loan with worse terms than they would have got if they had filed in March. State schemes reward early filers and people who have visited the district office. They punish the people who treat the state portal as a self-service shop.

One final piece of honest framing. The schemes described here change wording, ceilings and approved-list composition between notifications. The numbers in this post are written as “currently around X” precisely because they shift. Before filing anything, open the relevant state portal, find the current academic year notification, and read it end to end. The RBI framework and the central National Scholarship Portal remain the two non-negotiable references for what the bank loan and the central subsidy structures look like in any given year.

FAQ

What is the Arivu scheme in Karnataka?

The Arivu Educational Loan Scheme is run by the Karnataka Minorities Development Corporation for students from Muslim, Christian, Jain, Sikh, Buddhist and Parsi communities domiciled in Karnataka. It offers low-interest loans currently around ₹50,000 to ₹1 lakh per year for diploma, undergraduate and postgraduate professional courses, with higher ceilings for some categories. The family income ceiling is currently around ₹6 lakh per year, and applications are filed on the KMDC portal during the annual notification window. The loan is meant to layer onto a PSU bank loan, not replace it.

Is there a Tamil Nadu education loan for SC students?

Yes. Tamil Nadu’s Adi Dravidar and Tribal Welfare Department runs two main products for SC students. The first is a domestic education loan with state interest cover, currently around ₹1 lakh to ₹1.5 lakh per year for professional courses at recognised Tamil Nadu institutions, with family income ceilings around ₹2.5 lakh for full grant and higher for partial support. The second is an overseas scheme for postgraduate and doctoral studies, with ceilings currently around ₹15 lakh to ₹20 lakh depending on country tier and confirmed admission to a ranked university.

Who is eligible for the Telangana overseas scholarship?

The Mahatma Jyotiba Phule BC Welfare overseas scholarship is open to BC, EBC and similar community students with Telangana domicile, confirmed admission to a recognised foreign university for postgraduate study, family income currently around ₹5 lakh or less per year, age typically under 35, and a valid BC community certificate. The scheme currently covers up to ₹20 lakh and is a scholarship rather than a loan, meaning it does not need to be repaid if the student completes the course and submits progress reports. Parallel schemes exist for SC students (Ambedkar Overseas Vidya Nidhi) and ST students.

Can I claim state and central CSIS subsidy together?

You cannot claim both on the same loan account, because one loan account is allowed only one moratorium interest subsidy and the state portal verification will reject a duplicate claim. You can run them in parallel if they sit on different loan accounts: a PSU bank loan with central CSIS claimed on it, and a separate state corporation loan running under its own concessional terms. Scholarships like Telangana MJPBCWREIS are not subsidies on a loan account at all, so they sit alongside a PSU bank loan plus CSIS with no conflict.

How long does state portal application take?

Timelines vary by state and scheme. Karnataka KMDC Arivu has historically taken three to six months from filing to first disbursement. Tamil Nadu Adi Dravidar domestic schemes run faster, currently around two to four months for clean files at the district level. The Tamil Nadu SC overseas scheme and Telangana overseas scholarships run on annual notification cycles, meaning applications are accepted in defined windows and decisions announced together. PSU bank loans, by comparison, sanction in four to six weeks for clean files, which is why most families file the bank application in parallel.

Does state subsidy stack with a PSU bank loan?

Yes, but with one rule. A state direct loan from a welfare corporation (Karnataka KMDC, Tamil Nadu ADW corporation, Telangana welfare corporations) is a separate loan account and runs alongside a PSU bank loan with no conflict. A state interest subsidy applied to a PSU bank loan account cannot coexist with central CSIS on the same account, because one account can carry only one moratorium interest subsidy. A scholarship from a state scheme is not a subsidy at all and stacks freely with both a PSU bank loan and CSIS.

What family income ceiling applies to these state schemes?

The ceilings differ by state and by scheme tier. Karnataka KMDC Arivu currently uses around ₹6 lakh per year for general courses and slightly higher for professional courses. Tamil Nadu Adi Dravidar full grant uses around ₹2.5 lakh, with partial support tiers at higher incomes. Telangana MJPBCWREIS uses around ₹5 lakh. Each notification publishes the current ceiling, and these numbers do shift. The district welfare office is the most reliable source for the live cut, since portal pages sometimes lag the latest government order by weeks.

Do I need to apply through the state portal or the district office?

Both. The state portal is the official filing channel and is non-negotiable for record keeping. The district welfare office is where the file gets verified, scrutinised and forwarded for state-level approval. Filing only on the portal without visiting the district office tends to slow the process because clarifications come back as portal messages that students sometimes miss for weeks. The cleaner sequence is to visit the district office first, confirm the current paperwork list and approved institution list, file the portal application, and follow up at the district level once a week until the file moves.

Faz · The Honest Journey · 2026