The Credit Guarantee Fund Scheme for Education Loans (CGFSEL) is the reason a bank cannot ask you for collateral or a third-party guarantor on an education loan up to ₹7.5 lakh: a government trust, NCGTC, guarantees 75 percent of the loan to the bank, so the bank carries less risk and lends without security. Most students never hear its name. They just see no collateral needed up to 7.5 lakh on a bank page and assume the bank is being generous. It is not. This scheme is quietly doing the work, and understanding it tells you exactly where the collateral-free door opens, where it closes, and what the bank can and cannot demand.

A father in Coimbatore once argued with an SBI branch for a week because they asked for property papers on his son’s ₹6 lakh loan. He was right to push back, and he did not know why. The answer is this scheme. For a loan of ₹7.5 lakh or below, under the standard scheme, the branch is not supposed to insist on collateral, because a central guarantee already covers most of their downside. Once he mentioned the credit guarantee scheme by name, the conversation changed. Knowing the mechanism is leverage, and this guide gives it to you.

Below is what CGFSEL actually is, what it does and does not do for you as a borrower, the ₹7.5 lakh line that matters, and how it sits alongside the other schemes. If you want the wider funding picture first, start with the complete India education loan guide and the breakdown of the maximum education loan amount in India.

The credit guarantee is often the real lever when no interest subsidy applies. See where it sits among the schemes in which subsidy is actually yours.

What CGFSEL actually is

The Credit Guarantee Fund Scheme for Education Loans is a government-backed guarantee, not a loan and not a subsidy. It was set up by the Department of Financial Services under the Ministry of Finance, and it is run by the National Credit Guarantee Trustee Company, NCGTC. It sits behind the Indian Banks’ Association Model Education Loan Scheme, which is the common rulebook most banks follow.

The mechanic is simple. When a bank gives you an education loan up to ₹7.5 lakh under the scheme, NCGTC promises to reimburse the bank for 75 percent of the amount if you default. That guarantee is what lets the bank drop the demand for collateral or a third-party guarantor on loans in that bracket. You are not the customer of this scheme. The bank is. But you are the beneficiary, because the guarantee is the thing standing between you and a request to mortgage a house for a modest loan.

Faz's rule

No collateral up to 7.5 lakh is not a favour the bank is doing you. It is a government guarantee working in the background. Name it when a branch forgets.

Branches still ask for security on small loans out of habit or caution. Knowing that a central credit guarantee covers 75 percent of a loan up to 7.5 lakh is your strongest, calmest argument to have that demand withdrawn.

What the scheme does and does not do for you

It is easy to over-read a guarantee scheme and assume it makes borrowing free or automatic. It does neither. Here is the honest split between what it changes for you and what it leaves exactly as it was.

| What CGFSEL does for you | What it does not do |

|---|---|

| Removes the collateral requirement on loans up to ₹7.5 lakh under the scheme | It does not remove the need for a co-applicant, usually a parent, as joint borrower |

| Removes the third-party guarantor requirement in that bracket | It does not guarantee approval. Your file still has to clear the bank’s credit checks |

| Caps the interest a member bank can charge at 2 percent over its benchmark rate | It does not pay or subsidise your interest. That is a different scheme, CSIS |

| Sets a nil margin up to ₹4 lakh, easing the upfront contribution on small loans | It does not cover you above ₹7.5 lakh, where collateral rules return |

| Works for recognised courses in India and, for eligible cases, abroad | It does not pay your loan for you. The 75 percent cover protects the bank, not you |

The single most misread point is the last one. The guarantee protects the lender, not the borrower. If you default, NCGTC pays the bank most of the loss, but you still owe the debt, your CIBIL is still damaged, and the co-applicant is still on the hook. The scheme lowers the bank’s risk so it will lend without security. It does not lower yours. Read the difference between secured and unsecured borrowing in full in our note on secured versus unsecured education loans.

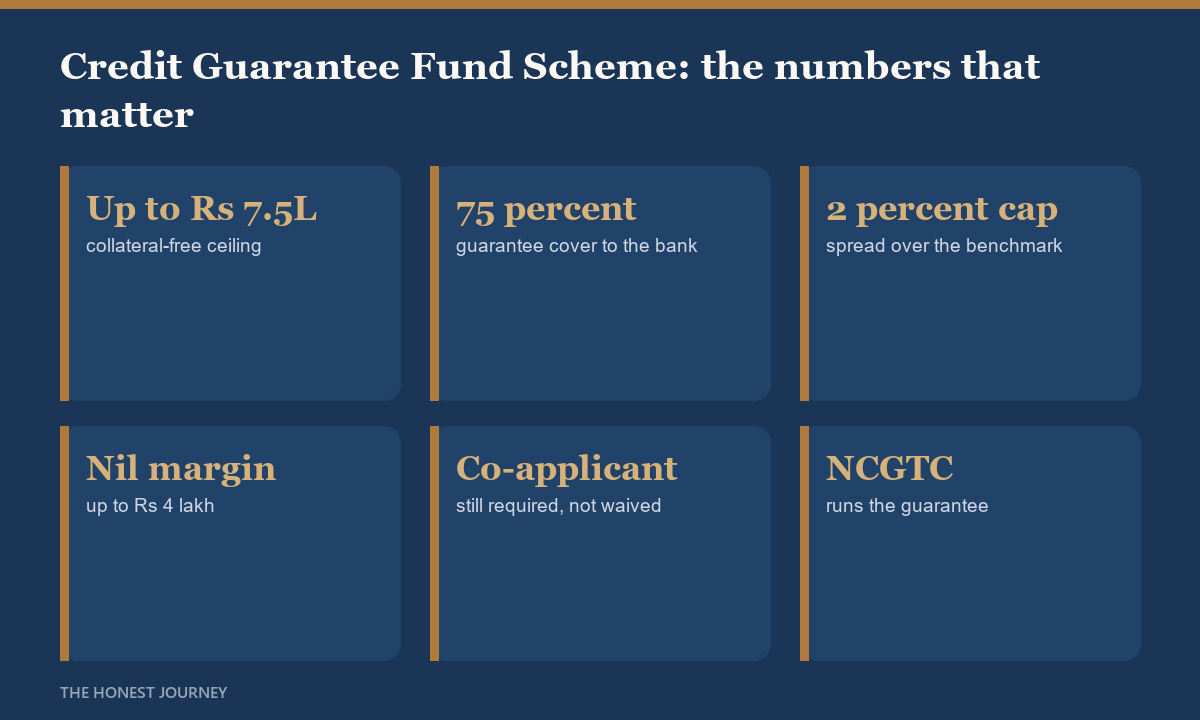

The numbers that define the scheme

A few figures do all the work here. Confirm each against your own sanction letter and your bank’s current circular, because banks apply the scheme through their own product rules and the details move.

| Line item | The figure | The honest reading |

|---|---|---|

| Collateral-free ceiling | Up to ₹7.5 lakh | This is the whole point. At or below this, no collateral or third-party guarantee under the scheme. |

| Guarantee cover to the bank | 75 percent of the amount in default | Protects the lender, not you. Your liability is unchanged. |

| Interest cap | Up to 2 percent over the bank’s benchmark rate | A ceiling on the spread, not a low rate by itself. Compare actual rates across lenders. |

| Margin money | Nil up to ₹4 lakh; 5 percent for India and 15 percent for abroad above ₹4 lakh | The abroad margin is the number that surprises families funding a foreign course. |

| Governing framework | IBA Model Education Loan Scheme | The common rulebook. Individual banks layer their own conditions on top. |

On income eligibility, be careful, because sources disagree. Some describe a household income ceiling of around ₹4.5 lakh for the economically weaker section framing, while the core collateral-free bracket under the Model Education Loan Scheme is often applied more broadly. The safest move is to ask your bank directly whether it applies an income test to the collateral-free ₹7.5 lakh loan, and not to assume you are ruled in or out. The ₹4.5 lakh figure is a hard ceiling for the separate interest-subsidy scheme, CSIS, which is a different benefit and worth claiming if you qualify.

Faz's rule

The 15 percent abroad margin above 4 lakh is the line families forget. On a 7.5 lakh loan for a foreign course, that is real money you fund yourself.

Margin money is your own contribution the bank will not finance. Nil up to 4 lakh sounds clean, but push the loan toward 7.5 lakh for an abroad course and a 15 percent margin on the slice above 4 lakh appears. Plan it as cash you must have ready. The mechanics are unpacked in our margin money guide.

Where CGFSEL sits among the schemes

People mix up three different things that all sound like government help. They are separate, they stack, and knowing which is which stops you chasing the wrong one.

| Scheme | What it is | Who it helps |

|---|---|---|

| CGFSEL, the credit guarantee | A guarantee that removes collateral up to ₹7.5 lakh | You, indirectly, by making a small loan collateral-free |

| CSIS, the interest subsidy | The government pays your moratorium-period interest, income ceiling around ₹4.5 lakh | Lower-income families, on the interest bill itself |

| PM Vidyalakshmi | A portal plus a newer interest subvention for eligible top institutions | Students at listed quality institutions |

The clean way to think about it: CGFSEL decides whether you need collateral, CSIS decides whether the government helps pay your interest, and PM Vidyalakshmi is the portal and the newer subvention for students at listed institutions. A single borrower can benefit from more than one. A ₹7.5 lakh collateral-free loan under the guarantee, with CSIS covering the moratorium interest, is a genuinely strong starting structure for a family within the income limits. For anything above ₹7.5 lakh you move into the secured or NBFC world, covered in the no-collateral loan guide.

How to actually use it when you borrow

You do not apply to CGFSEL. You apply for an ordinary education loan and make sure the bank extends it under the scheme. The steps are about knowing what to ask for.

- Keep the loan at or under ₹7.5 lakh if you want the collateral-free bracket. If your total need is higher, consider splitting the funding rather than pushing one loan past the line into collateral territory.

- Ask the branch to confirm in writing that the loan is under the credit guarantee scheme. This is your basis for declining a collateral or guarantor demand on a sub-7.5 lakh loan.

- Line up your co-applicant regardless. The guarantee does not replace the joint borrower. A parent with a clean record and documented income is still required, as explained in our co-applicant guide.

- Budget the margin. Nil up to ₹4 lakh, then 5 percent in India or 15 percent abroad on the slice above. Have that cash ready, per the margin money explainer.

- Claim CSIS separately if your family income is within its ceiling. It is a different form and a different benefit, and it stacks on top of a guaranteed loan.

A public-sector bank is usually the right place to start for a scheme-backed loan of this size, because they apply the Model Education Loan Scheme most directly. See how the largest lender handles it in the SBI education loan guide, and compare the real rates across lenders in our interest rate comparison.

The honest closing take

CGFSEL is not a scheme you chase. It is a scheme you invoke. Its entire value to you is that it makes a loan up to ₹7.5 lakh collateral-free and guarantor-free, and that it caps how much spread a bank can charge over its benchmark rate. For a modest loan, that is exactly the protection you want, and most borrowers benefit from it without ever learning its name.

The two things to keep straight are that the guarantee protects the bank and not you, so a default still lands on your CIBIL and your co-applicant, and that the collateral-free door closes at ₹7.5 lakh, above which security returns. Borrow within that bracket where you can, stack CSIS on top if you qualify, keep your co-applicant ready, and use the scheme’s name as leverage the moment a branch asks for collateral it is not entitled to demand.

FAQ

What is the Credit Guarantee Fund Scheme for Education Loans?

It is a government-backed guarantee, run by the National Credit Guarantee Trustee Company (NCGTC) under the Ministry of Finance, that covers 75 percent of an education loan up to ₹7.5 lakh if the borrower defaults. Because the bank’s risk is reduced, it can lend that amount without collateral or a third-party guarantor. It sits behind the IBA Model Education Loan Scheme. It is not a loan or a subsidy in itself, it is the mechanism that makes small education loans collateral-free.

Does CGFSEL mean I get an education loan without collateral?

Yes, up to ₹7.5 lakh. That is the practical effect of the scheme. For a loan at or below ₹7.5 lakh extended under the scheme, the bank should not insist on collateral or a third-party guarantor. Above ₹7.5 lakh, the guarantee no longer applies and banks typically ask for security. You still need a co-applicant, usually a parent, as joint borrower even within the collateral-free bracket, because the guarantee does not remove that requirement.

Does the credit guarantee pay my loan if I cannot?

No. This is the most important thing to understand. The 75 percent guarantee protects the bank, not you. If you default, NCGTC reimburses the bank for most of its loss, but you still owe the full debt, your CIBIL score is still damaged, and your co-applicant remains liable. The scheme lowers the lender’s risk so it will lend without security. It does not lower your obligation to repay.

What is the interest rate under CGFSEL?

The scheme caps the interest a member bank can charge at up to 2 percent over its benchmark or base rate. That is a ceiling on the spread, not a guaranteed low rate, and the actual rate still varies by bank. It does not subsidise your interest. If you want the government to help pay your interest, that is a separate scheme called CSIS, which covers moratorium-period interest for families within its income ceiling. The two can apply to the same loan.

Is there an income limit for CGFSEL?

Sources differ. Some describe a household income ceiling of around ₹4.5 lakh under an economically weaker section framing, while the collateral-free ₹7.5 lakh bracket under the Model Education Loan Scheme is often applied more broadly. The safest approach is to ask your bank directly whether it applies an income test to the guaranteed loan. Note that ₹4.5 lakh is a firm ceiling for the separate CSIS interest subsidy, which is worth claiming if your family qualifies.

What margin money do I need under the scheme?

There is no margin on loans up to ₹4 lakh. Above ₹4 lakh, the margin is 5 percent for studies in India and 15 percent for studies abroad, applied to the amount over that threshold. Margin money is your own contribution that the bank will not finance, so it is cash you must have ready. For a foreign course funded near the ₹7.5 lakh ceiling, that 15 percent abroad margin is a real out-of-pocket figure families often overlook.

Can I use CGFSEL for studying abroad?

Yes, for eligible recognised courses, the collateral-free guarantee can apply to abroad education loans up to ₹7.5 lakh, subject to the higher 15 percent margin above ₹4 lakh. The catch is that ₹7.5 lakh rarely covers a full foreign degree, so it usually forms only one part of the funding. Most students combine a guaranteed collateral-free base with additional secured or NBFC borrowing for the balance, which is covered in our guide to education loans for abroad studies without collateral.

Faz · The Honest Journey · 2026