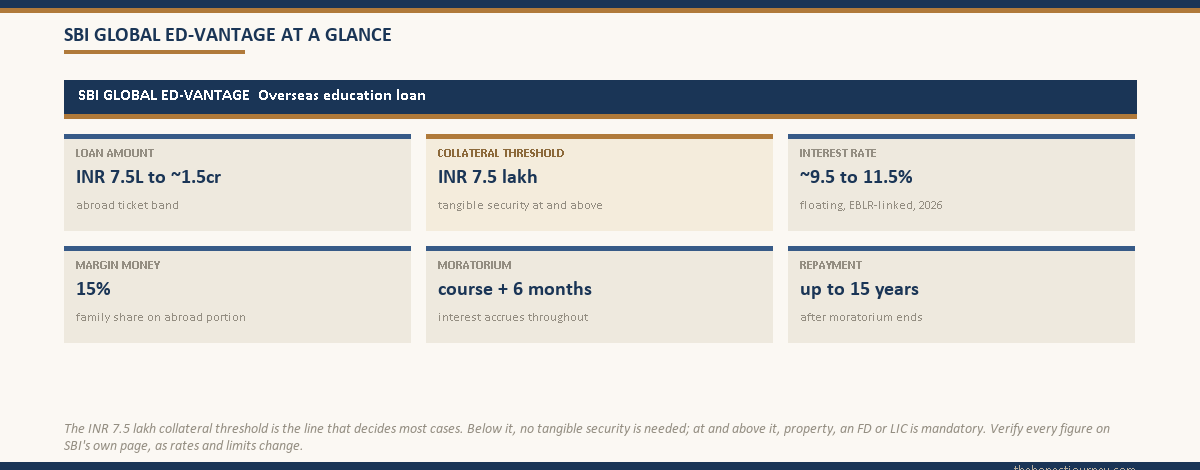

SBI’s overseas education loan, SBI Global Ed-Vantage, sanctions from ₹7.5 lakh up to around ₹1.5 crore for studies abroad. Below ₹7.5 lakh no tangible collateral is needed, but at ₹7.5 lakh and above SBI requires tangible security such as property, a fixed deposit or LIC. The rate is floating, linked to SBI’s external benchmark and usually landing in the rough range of 9.5 to 11.5 percent in 2026, with a 15 percent family margin on the abroad portion and a moratorium of the course period plus six months.

I have watched a few families go to SBI for an abroad loan, and the pattern is consistent. For families who own property or a chunky fixed deposit and have a child going to a solid program, SBI Global Ed-Vantage is often the cheapest serious option on the table. For families with no collateral chasing a large ticket, the same product becomes a wall, because the ₹7.5 lakh unsecured ceiling is firm. This post lays out the product honestly, what it is, what it costs, and plainly who it does not fit.

To be clear about what this is: I am not affiliated with SBI, I do not earn anything from this, and nothing here is an endorsement. It is a factual guide to one widely used PSU product so you can decide for yourself. Verify every current figure on SBI’s own page before you sign, because rates and limits change. The official product page is on sbi.co.in.

To weigh this lender against the others: the secured vs unsecured education loan post, the canara bank education loan post, and the bank of baroda education loan post.

What SBI Global Ed-Vantage actually is

Global Ed-Vantage is SBI’s dedicated loan for full-time courses abroad at the undergraduate, postgraduate and doctoral level. It is the product you use for a Master’s in the US, UK, Canada, Germany, the Netherlands, Australia and the other common destinations. It sits inside the Indian Banks’ Association model education loan framework, which is the template every PSU bank follows, so its structure rhymes with Bank of Baroda’s and Canara’s overseas products. SBI is a public sector bank, which matters for two benefits I will come to: the central interest subsidy and the Section 80E tax deduction.

The loan can cover the standard list of eligible expenses: tuition and college fees, exam, library and laboratory fees, the cost of books, equipment and a laptop where required, travel to and from the country of study, and reasonable living expenses. It can also fold in caution deposits and the cost of a study tour or thesis where the course requires it. The broad principle is that the loan funds the genuine cost of completing the course, not lifestyle spending on top.

The numbers that define the product

A few figures decide whether this loan fits you. I will take them one at a time, and these are the ones to verify on SBI’s page because they move.

- Loan amount: from ₹7.5 lakh up to around ₹1.5 crore for studies abroad. Some categories and premier-institute cases can go higher, but ₹1.5 crore is the practical headline ceiling for most.

- Collateral threshold: below ₹7.5 lakh, no tangible collateral is required, only a co-applicant. At ₹7.5 lakh and above, tangible collateral is mandatory. This single line is the whole story for most abroad tickets, because almost every Master’s abroad costs more than ₹7.5 lakh.

- Interest rate: floating, linked to SBI’s external benchmark lending rate (EBLR) plus a spread, so it moves when the RBI changes the repo rate. In 2026 it has typically sat in the rough range of 9.5 to 11.5 percent depending on the spread and any concessions. A small concession often applies for women students.

- Margin money: 15 percent for studies abroad. This is the family’s own contribution, paid alongside disbursements rather than upfront. How margin works in general is in the education loan for abroad studies without collateral post, and the broader product picture in the complete guide to education loans in India.

- Moratorium: the course period plus six months. You do not have to start full EMIs until then, though interest accrues during the moratorium and you can choose to service it as it accrues to keep the loan from ballooning.

- Processing fee: a fixed fee applies for studies abroad, a modest amount in the low thousands of rupees, refundable or adjustable in some cases. Confirm the current figure at the branch.

- Repayment: typically up to 15 years after the moratorium ends, which keeps EMIs manageable on a large ticket.

The two figures that decide most cases are the ₹7.5 lakh collateral threshold and the floating rate. The threshold decides whether you even qualify for the amount you need; the rate decides what it costs over the life of the loan.

A worked INR example for a typical abroad Master’s

Take a real-shaped case. Student admitted to a one-year Master’s abroad with a total cost, tuition plus living, of ₹30 lakh. The family approaches SBI for Global Ed-Vantage.

Because the amount is well above ₹7.5 lakh, tangible collateral is mandatory. The family pledges a residential flat. SBI applies a valuation haircut and counts a security value comfortably above the loan. The margin is 15 percent on the abroad portion, paid alongside disbursements.

| Funding layer | INR | Notes |

|---|---|---|

| Total program cost | 30,00,000 | Tuition plus living |

| Family margin (15 percent) | ~4,50,000 | Paid alongside disbursements |

| SBI-funded loan | ~25,50,000 | Disbursed per the fee schedule |

| Collateral pledged | Residential flat | After valuation haircut |

Now the cost of the loan. Assume the floating rate sits at 10.5 percent and the family services the interest during the one-year course plus the six-month moratorium, so the principal does not capitalise. After the moratorium, the roughly ₹25.5 lakh principal is repaid over, say, 10 years. At 10.5 percent over 120 months, the EMI is roughly ₹34,400 a month, and the total interest over the 10 years is roughly ₹15.8 lakh. If instead the family lets the interest accrue and capitalise during the moratorium, the principal at the start of repayment is higher and the total cost rises by more than a lakh, which is why servicing interest during study matters.

| Scenario | Principal at repayment | Approx EMI (10 yr, 10.5%) |

|---|---|---|

| Interest serviced during moratorium | ~25,50,000 | ~₹34,400 |

| Interest capitalised during moratorium | ~28,00,000 | ~₹37,800 |

These are indicative numbers at one assumed rate. Your actual rate, tenure and EMI come from your sanction letter. The point of the table is the gap between servicing interest during the moratorium and letting it capitalise, which is real money and within your control.

Faz's ruleService the interest during the course and moratorium if you possibly can. On a large abroad loan, letting interest capitalise before repayment quietly adds a lakh or more to what you owe, before your first EMI even starts.

The moratorium is a relief, not a free pass. Interest accrues the whole time. Even paying part of it during study keeps the principal from snowballing. Ask the branch for the simple interest option during the moratorium and budget a small monthly amount towards it.

Who SBI Global Ed-Vantage genuinely fits

This product is a strong fit for a specific kind of family, and I will say plainly which.

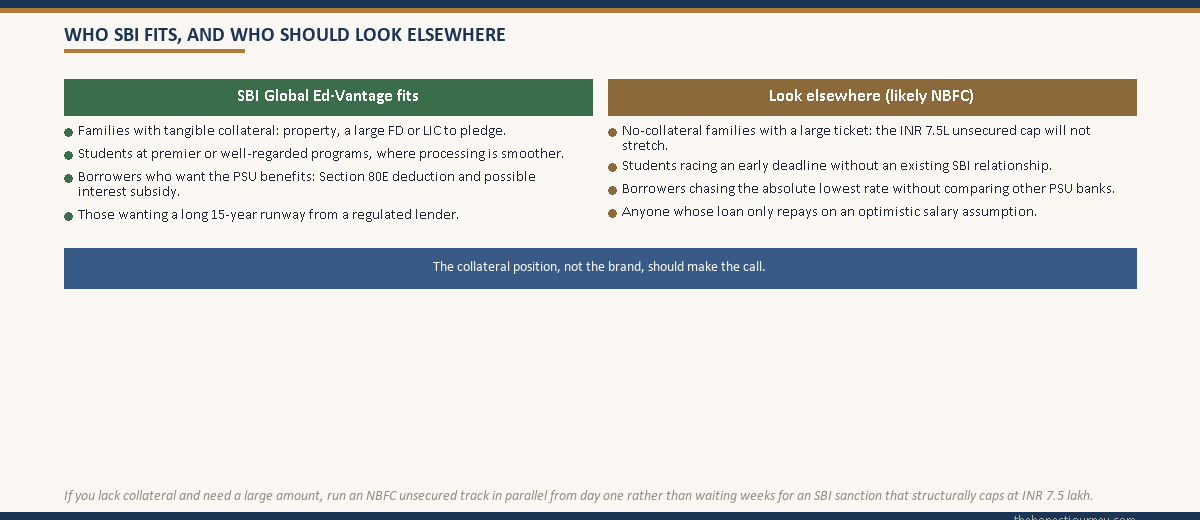

- Families with tangible collateral. If you own property, a sizable fixed deposit or LIC policies you can pledge, the ₹7.5 lakh threshold is a non-issue, and you get a PSU floating rate that is usually cheaper than any NBFC unsecured rate. The collateral route at SBI is, for most, the lowest lifetime cost of borrowing for an abroad ticket.

- Students at premier or well-regarded programs, where the bank is comfortable and processing is smoother.

- Families who value the PSU benefits: the loan qualifies for the Section 80E interest deduction, and for eligible income brackets the central interest subsidy can apply. The 80E mechanics are in the Section 80E tax benefit post, and the subsidy claim process in the CSIS interest subsidy post.

- Borrowers who want a long 15-year repayment runway and a transparent, regulated lender. The framework SBI operates under is set by the RBI and the model scheme published by the Indian Banks’ Association.

Who SBI Global Ed-Vantage does not fit

It would be dishonest to pretend this product suits everyone. It does not, and forcing it can waste weeks you do not have.

- Families with no tangible collateral and a large ticket. If your program costs ₹30 lakh and you cannot pledge property, an FD or LIC, SBI will not sanction the amount you need, because the unsecured ceiling is ₹7.5 lakh. This is the most common mismatch I see. An NBFC unsecured loan, at a higher rate, is the realistic route, covered in the no-collateral post.

- Students who need money fast for an early deadline and do not already bank with SBI. PSU processing, valuation and legal checks on collateral take time. If your university funding deadline is weeks away, an NBFC or a bank you already have a relationship with may move quicker.

- Borrowers chasing the absolute lowest rate at any cost. SBI is usually competitive, but rates shift, and other PSU banks like Bank of Baroda, Canara or PNB with its Udaan and Pratibha schemes may price a particular profile slightly differently. Compare, do not assume. The interest-rate landscape is in the interest rate comparison post, and if you are still weighing the two routes, the PSU bank vs NBFC education loan breakdown walks through which type fits which borrower.

- Anyone for whom the loan only repays on an optimistic earning assumption. The largest sanctions, near ₹1.5 crore, are serviceable only on a strong post-study salary. The general ceiling and what amounts make sense are in the maximum education loan amount post.

Faz's ruleIf you have no collateral and a large abroad ticket, do not waste weeks waiting on an SBI sanction it cannot give. The ₹7.5 lakh unsecured ceiling is firm, so look at an NBFC unsecured loan in parallel from day one.

The hardest version of this is the family that applies to SBI, waits a month, gets told the unsecured amount caps at ₹7.5 lakh, and only then turns to an NBFC with the deadline closing in. If you lack collateral, run both tracks at once and pick the one that clears in time.

The honest take on SBI Global Ed-Vantage

SBI Global Ed-Vantage is a solid, regulated, often cheapest-on-the-table loan for the family that has collateral and a child going to a real program. The PSU benefits, the 80E deduction and the possible interest subsidy, plus a floating rate that usually undercuts NBFC unsecured rates, make it the default worth checking first if you can pledge security.

But it is not a universal answer, and the people it lets down are predictable: no-collateral families with large tickets, and students racing an early deadline without an existing SBI relationship. For them the honest advice is to look at an NBFC unsecured loan with eyes open about the higher rate, rather than forcing a product that structurally cannot stretch. Check SBI’s current figures on its own page, model the cost with interest serviced during the moratorium, and decide against your actual collateral position, not against the brand. The math, not the name, should make the call.

Ready to fund it? Most Indian students route the loan through the PM Vidyalakshmi portal. That guide covers the step by step application and the 13 banks linked to it.

FAQ

What is SBI Global Ed-Vantage?

SBI Global Ed-Vantage is SBI’s dedicated education loan for full-time courses abroad at undergraduate, postgraduate and doctoral level. It sanctions from ₹7.5 lakh up to around ₹1.5 crore, funds tuition, living and the standard eligible expenses, and follows the Indian Banks’ Association model scheme. Because SBI is a public sector bank, the loan qualifies for the Section 80E tax deduction and, for eligible income brackets, the central interest subsidy. Verify current figures on SBI’s official page before applying.

How much can I borrow under SBI Global Ed-Vantage?

The product sanctions from ₹7.5 lakh up to around ₹1.5 crore for studies abroad, with some premier-institute and special categories able to go higher. Below ₹7.5 lakh no tangible collateral is needed, but at ₹7.5 lakh and above SBI requires tangible security such as property, a fixed deposit or LIC. The exact amount sanctioned depends on the program cost, your collateral value after a valuation haircut, and the co-applicant’s repayment capacity.

Does SBI Global Ed-Vantage need collateral?

Below ₹7.5 lakh, no tangible collateral is required, only a co-applicant. At ₹7.5 lakh and above, tangible collateral is mandatory: property, a fixed deposit, LIC policies or similar acceptable security. Since almost every abroad Master’s costs more than ₹7.5 lakh, most SBI abroad loans need collateral. Families without collateral chasing a large ticket usually cannot get the full amount from SBI and should look at an NBFC unsecured loan instead.

What is the interest rate on SBI Global Ed-Vantage?

The rate is floating, linked to SBI’s external benchmark lending rate plus a spread, so it moves with the RBI repo rate. In 2026 it has typically sat in the rough range of 9.5 to 11.5 percent depending on the spread and concessions, with a small concession often available for women students. Because it is floating, your EMI can change over the life of the loan. Always confirm the current applicable rate on your sanction letter, not from a general figure.

What is the moratorium period for SBI Global Ed-Vantage?

The moratorium is the course period plus six months. During it you are not required to pay full EMIs, but interest accrues throughout. You can choose to service the interest as it accrues, which keeps the principal from capitalising and quietly growing before repayment starts. Servicing even part of the interest during study can save a lakh or more on a large abroad loan, so ask the branch for the simple-interest option during the moratorium.

What expenses does SBI Global Ed-Vantage cover?

It covers tuition and college fees, exam, library and laboratory fees, the cost of books, equipment and a laptop where required, travel to and from the country of study, and reasonable living expenses. It can also include caution deposits and the cost of a study tour or thesis where the course requires it. The principle is funding the genuine cost of completing the course. It does not fund lifestyle spending beyond the reasonable living-cost estimate.

Who should not use SBI Global Ed-Vantage?

Families with no tangible collateral and a large ticket, because the unsecured ceiling of ₹7.5 lakh will not stretch to a typical abroad Master’s. Students facing an early funding deadline who do not already bank with SBI, since PSU collateral processing takes time and an NBFC may move faster. And anyone whose repayment only works on an optimistic salary assumption. For these cases an NBFC unsecured loan, despite its higher rate, is often the realistic route.

Does SBI Global Ed-Vantage qualify for tax benefits?

Yes. As a loan from a recognised lender, the interest you pay qualifies for the Section 80E deduction, which lets you deduct the full education-loan interest from taxable income for up to eight years. Because SBI is a public sector bank, eligible borrowers within the income criteria can also benefit from the central interest subsidy on the moratorium-period interest. Confirm your eligibility for the subsidy and keep the annual interest certificate for your 80E claim.

Faz · The Honest Journey · 2026