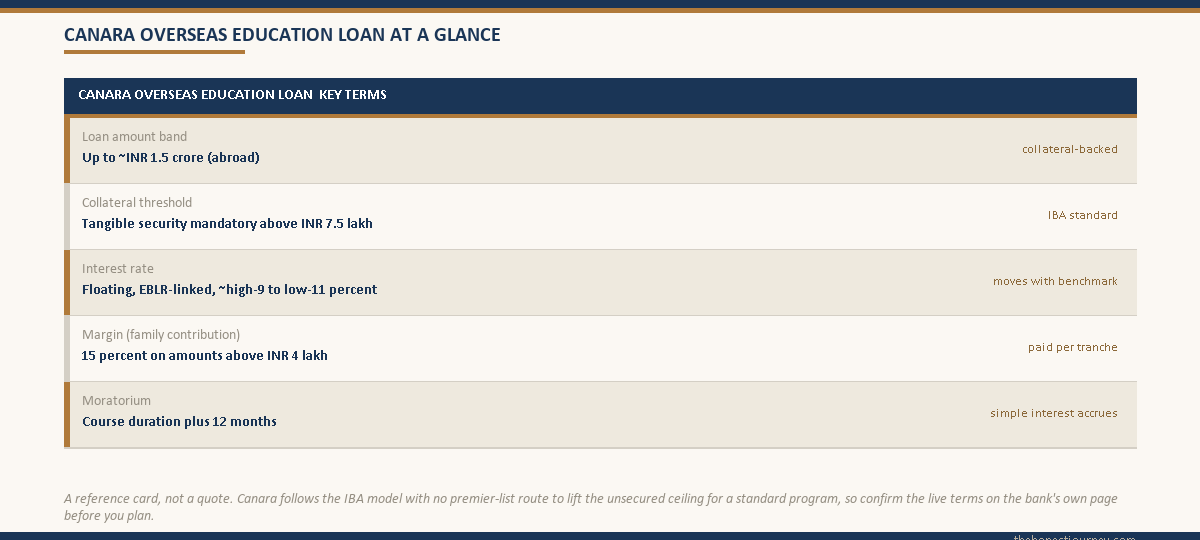

Canara Bank’s overseas education loan follows the IBA model scheme, sanctioning up to around ₹1.5 crore for studies abroad with tangible collateral and capping the unsecured amount at ₹7.5 lakh for most students. It is one of the most heavily used PSU banks for education loans in India, priced on a floating rate in the high-9 to low-11 percent range for 2026, with a 15 percent margin on abroad amounts and a moratorium of course duration plus twelve months. Above ₹7.5 lakh, collateral is mandatory, the same as every PSU bank.

One of the quiet truths about education loans in India is that a huge share of them, far more than the marketing of any single bank would suggest, are written by Canara Bank. It is one of the workhorse PSU lenders for students, and plenty of families end up with a Canara loan simply because the branch processed it cleanly and the relationship manager actually returned calls. That is not a small thing when you are racing a visa deadline.

This post is the honest product picture for the Canara Bank overseas education loan. It is the loan terms, the collateral threshold, the rate, the worked math and the plain question of who the scheme fits and who it does not. No sales tone, no implied endorsement, just the mechanics you need before you sit across from a loan officer.

To weigh this lender against the others: the secured vs unsecured education loan post, the bank of baroda education loan post, and the axis bank education loan post.

What the Canara overseas education loan actually is

Canara Bank is a public sector bank, so its overseas education loan runs under the Indian Banks’ Association model educational loan scheme, the same template SBI, Bank of Baroda and the other PSU banks use. The scheme covers tuition and examination fees, the cost of books, equipment and instruments, travel for studies abroad, and reasonable living expenses, all assessed against the offer letter and the published cost of the program.

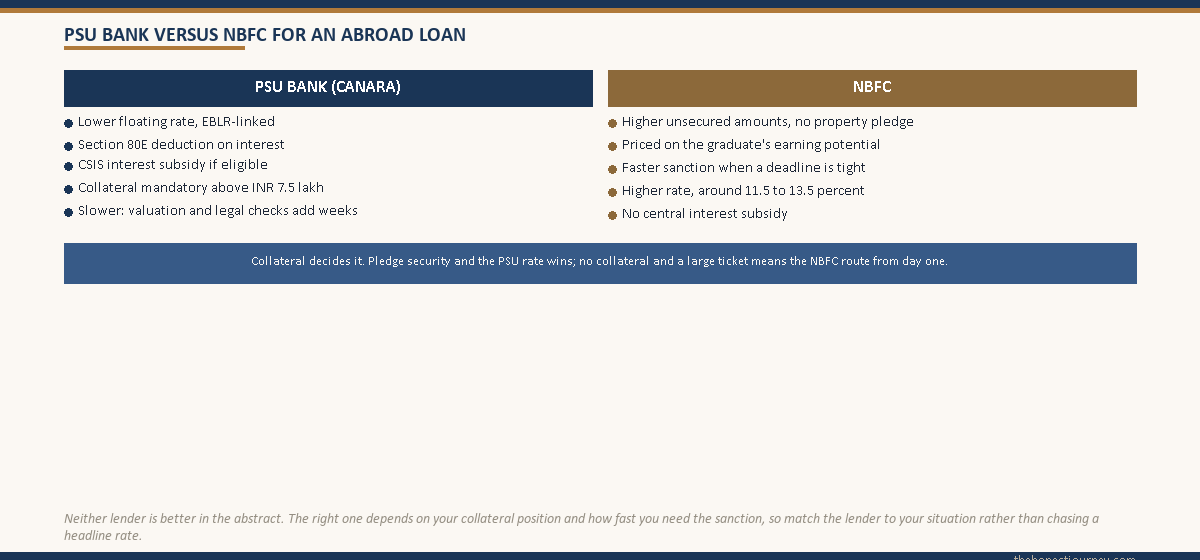

Two consequences follow from it being a PSU loan. The interest qualifies for the Section 80E tax deduction, and eligible families can claim the central interest subsidy during the moratorium under the government scheme. These are benefits an NBFC loan does not carry, and they are part of why families weigh a PSU sanction against a quicker NBFC one. The wider context of how Indian education loans work sits in the complete guide to education loans in India.

The bank’s own product details live on the Canara Bank website. Always cross-check the live page, because product terms shift and the bank’s published version is the one that actually governs your loan.

The amount band and the ₹7.5 lakh threshold

Because it follows the IBA model, the Canara structure splits exactly the way every PSU education loan does. The tier you fall into decides your collateral, your rate and your repayment runway.

- Up to ₹4 lakh: no margin and no collateral, parent as co-applicant. Almost no abroad program is this small.

- Above ₹4 lakh to ₹7.5 lakh: co-applicant and usually a third-party guarantee, no tangible collateral. Still below most abroad tickets.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory, which is where almost every abroad Master’s lands.

That ₹7.5 lakh line is the whole story for an abroad student. A one-year UK Master’s is ₹30 to 45 lakh, a two-year Australian or US program more, so you are almost always above the unsecured ceiling and into collateral territory. Canara does not have a special premier-list mechanism that lifts the unsecured ceiling the way some banks advertise, so for the standard abroad ticket, plan on pledging security. The general ceiling picture across all lenders is in the maximum education loan amount in India post.

Rate, margin and moratorium

The interest is floating, linked to the bank’s external benchmark lending rate, which is how all PSU education loans are priced now. For 2026 an abroad education loan from Canara sits broadly in the high-9 to low-11 percent range, varying with the loan amount, the collateral cover and any applicable concession the bank offers on its premier categories. Because the rate floats, it moves with the benchmark over the life of the loan, so build your repayment plan with a buffer rather than locking onto today’s exact figure.

Margin money is the family’s own contribution. For studies abroad it is 15 percent of the loan amount above ₹4 lakh, paid alongside each disbursement rather than handed over at the start. On a ₹40 lakh loan that is roughly ₹6 lakh of family money spread across the disbursement schedule. Scholarships can sometimes be folded into the margin calculation, so confirm at the branch how yours is worked out.

The moratorium, the gap before full repayment begins, runs for the course duration plus twelve months under the current IBA framework, or six months after getting a job, whichever comes first. Simple interest accrues during this period. Servicing that interest while you study, even partly, keeps it from capitalising and shrinks the principal you repay later. How this PSU rate compares with the NBFC alternatives is broken down in the education loan interest rate comparison.

Faz's rulePick the PSU bank whose branch actually answers the phone, because every PSU education loan is priced and structured almost identically under the same IBA model. The difference between banks is service, not terms.

Canara, SBI and Bank of Baroda all run the same model scheme, so the headline rate and collateral rules barely differ. What differs is how fast the branch moves your file. When a visa deadline is weeks away, a responsive relationship manager is worth more than a token rate difference.

A worked INR example for an Australian Master’s

Take a real-shaped case. Student admitted to a two-year Master’s at an Australian university for the 2026 intake. The university total comes to AUD 90,000, made up of AUD 66,000 tuition across two years and roughly AUD 24,000 of living and other costs the bank will count. At ₹55 per Australian dollar that is ₹49.5 lakh.

| Item | AUD | INR (at 55) |

|---|---|---|

| Tuition and fees (two years) | 66,000 | 36,30,000 |

| Living, travel, other eligible costs | 24,000 | 13,20,000 |

| Total program cost | 90,000 | 49,50,000 |

This is far above ₹7.5 lakh, so tangible collateral is mandatory. The family pledges a residential property valued at ₹80 lakh. Canara applies a valuation haircut, counts a security value comfortably above the loan, and sanctions the ₹49.5 lakh at the standard floating rate. Now the margin and the disbursement split.

| Funding layer | INR | Notes |

|---|---|---|

| Total program cost | 49,50,000 | The sanction basis |

| Family margin (15 percent above ₹4 lakh) | ~6,82,500 | Paid alongside disbursements |

| Bank-funded loan | ~42,67,500 | Disbursed per the fee schedule |

| Collateral pledged | Property ~80,00,000 | After valuation haircut |

If this family had no property to pledge, Canara could not bridge the gap, because the unsecured ceiling is ₹7.5 lakh and there is no PSU mechanism to exceed it for a standard program. The same case would then go to an NBFC for an unsecured sanction priced on the program’s earning potential, at a higher rate of 11.5 to 13.5 percent versus Canara’s floating rate near 10 percent. Over a long repayment that spread is several lakh of extra interest, and the honest economics of that route are in the education loan for abroad studies without collateral post.

Who the Canara education loan fits, and who it does not

The honest fit test for the Canara overseas loan is the same collateral question that governs every PSU loan, with a service overlay on top.

Canara fits well if the family has tangible collateral to pledge and wants the lower PSU floating rate plus the 80E deduction and the CSIS subsidy, and is not in a last-minute rush. It fits especially if you have a clean banking relationship with Canara or a responsive local branch, because given that all PSU banks offer near-identical terms, the deciding factor genuinely is which branch moves your file fastest. Canara’s scale in the education loan market means many branches handle these routinely.

It does not fit if your need is a large unsecured loan and the family has no collateral. The ₹7.5 lakh unsecured ceiling is a hard structural limit, the same at every PSU bank, and Canara has no premier-list route to lift it for a standard program. A large unsecured requirement belongs at an NBFC, which prices on the graduate’s earning potential rather than on collateral. It also fits poorly if you need a sanction in days rather than weeks, because PSU processing, with property valuation and legal checks, is slower than a streamlined NBFC sanction.

None of this is a criticism of Canara. The limits are structural to the PSU model, not specific to this bank. The point is to match your situation to the right lender before you invest weeks in a process the scheme cannot complete for you.

Faz's ruleIf your need is large and unsecured with no collateral, do not waste weeks in a PSU queue. No PSU bank, Canara included, can exceed the ₹7.5 lakh unsecured ceiling for a standard program, so that is an NBFC conversation from day one.

Families lose precious weeks applying to PSU banks for unsecured amounts those banks structurally cannot give. Know your collateral position first. If you can pledge security, the PSU route and its lower rate is the better deal. If you cannot, go straight to an NBFC and accept the higher rate as the price of an unsecured loan.

The tax and subsidy benefits, and what they are worth

Because Canara is a PSU bank, the interest you pay qualifies for the Section 80E income tax deduction. The full interest paid in a financial year is deductible from taxable income for up to eight years from the year repayment begins, with no upper cap. For a family in a higher bracket repaying a large loan, that deduction is a real cut in the effective cost of borrowing. The mechanics are laid out in the Section 80E tax benefit post.

Eligible families can also claim the central interest subsidy during the moratorium, which covers the interest accruing while you study for borrowers within the income criteria. This is a PSU-only benefit that NBFC loans do not offer, and for families who qualify it is one of the honest reasons a slightly slower Canara sanction can beat a faster NBFC one. How to actually claim it is covered in the CSIS interest subsidy claim post. The regulatory framework these schemes sit under is on the RBI site, and the model loan template is published by the Indian Banks’ Association.

The honest take on the Canara education loan

Canara Bank’s overseas education loan is a dependable, standard PSU product. It does not have a headline gimmick, no special unsecured-lifting list to chase, and that is fine, because for a collateral-backed abroad loan it gives you the lower PSU floating rate, the 80E deduction and the CSIS subsidy, which is the full set of advantages a PSU loan offers. Its real edge is reach and routine: many branches process abroad loans all the time, so a responsive one can move your file cleanly.

Because the terms are near-identical across PSU banks, there is no strong reason to fixate on Canara over SBI or Bank of Baroda on the numbers alone. Choose on branch responsiveness and your existing relationship. And if your need is a large unsecured loan with no collateral, Canara, like every PSU bank, cannot help, so save yourself the weeks and start the NBFC conversation instead.

The single thing that decides whether Canara is right for you is your collateral position. If you can pledge security, it is a strong, low-cost choice. If you cannot, and the ticket is large, no PSU bank is your answer. Know which side of that line you are on before you walk into the branch.

FAQ

What is the maximum Canara Bank education loan for studies abroad?

Canara Bank sanctions up to around ₹1.5 crore for studies abroad under the IBA model scheme, provided tangible collateral and co-applicant income support the amount. The unsecured ceiling stays at ₹7.5 lakh for most students, with property, fixed deposit or LIC required as security above that figure. Canara does not have a premier-list mechanism to exceed the unsecured ceiling for a standard program, so a large abroad ticket almost always needs collateral.

What interest rate does Canara Bank charge on an education loan?

The rate is floating, linked to the bank’s external benchmark lending rate. For 2026 a Canara abroad education loan sits broadly in the high-9 to low-11 percent range, depending on the loan amount, collateral cover and any concession the bank applies to its premier categories. Because the rate floats with the benchmark, it changes over the life of the loan, so plan your repayment with a buffer rather than assuming today’s exact rate will hold for the whole tenure.

Is collateral mandatory for a Canara overseas education loan?

For most students, yes. Any amount above ₹7.5 lakh requires tangible collateral such as property, fixed deposit or LIC, and almost every abroad program runs well above that figure. Canara has no special route to exceed the unsecured ceiling for a standard program, so if the family has no collateral and the ticket is large, the loan cannot be completed at Canara. That situation belongs at an NBFC, which lends unsecured against the graduate’s earning potential.

How much margin money does Canara Bank require for an abroad loan?

For studies abroad, the margin is 15 percent of the loan amount above ₹4 lakh, contributed by the family alongside each disbursement rather than upfront. On a ₹40 lakh loan that is roughly ₹6 lakh of family contribution spread across the disbursement schedule. Scholarships can sometimes be folded into the margin calculation, so confirm at the branch exactly how your margin is computed before you sign the sanction terms.

What is the moratorium period on a Canara education loan?

The moratorium, the period before full repayment begins, runs for the course duration plus twelve months under the current IBA framework, or six months after getting a job, whichever is earlier. Simple interest accrues during this time, so servicing even part of it while you study keeps it from capitalising and reduces the principal you eventually repay. Paying down moratorium interest where the family can afford it lowers the total cost of the loan over its tenure.

Does a Canara Bank education loan qualify for tax benefits?

Yes. Because Canara is a public sector bank, the interest qualifies for the Section 80E income tax deduction, which allows the full interest paid in a financial year to be deducted from taxable income for up to eight years from when repayment begins, with no upper limit. Eligible families may also claim the central interest subsidy during the moratorium, a benefit that NBFC loans do not carry, which can make a slower PSU sanction worthwhile for those who qualify.

Is Canara Bank good for education loans?

Canara is one of the most heavily used PSU banks for education loans, so many branches handle abroad loans routinely and can process a file cleanly. Its terms are near-identical to other PSU banks because all follow the same IBA model, so the deciding factor is usually branch responsiveness and your existing relationship rather than the headline numbers. It is a strong choice for a collateral-backed loan and a poor fit for a large unsecured need.

Should I choose Canara Bank or an NBFC for my abroad loan?

It comes down to collateral. If your family can pledge property, a fixed deposit or LIC, Canara gives a lower floating rate plus the Section 80E deduction and the CSIS subsidy, which an NBFC cannot match. If you have no collateral and need a large unsecured loan, Canara cannot exceed the ₹7.5 lakh ceiling, so an NBFC, which prices on the graduate’s earning potential at a higher rate, is the realistic route. NBFCs also sanction faster when a deadline is tight.

Faz · The Honest Journey · 2026