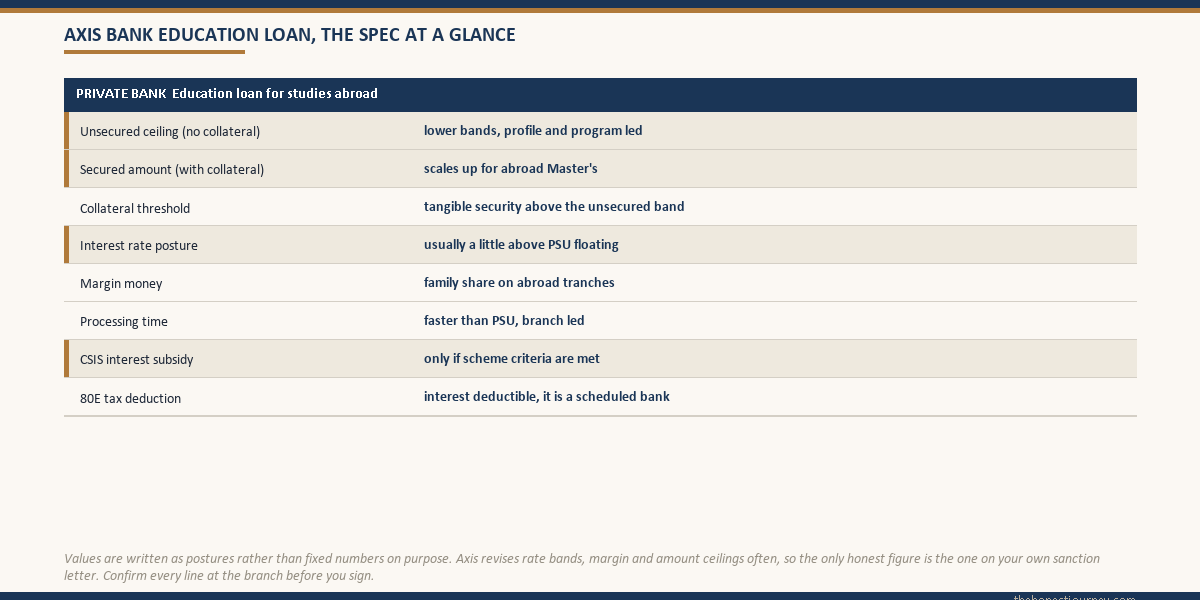

An Axis Bank education loan is a private bank loan for studies in India and abroad, with both unsecured and secured options. The unsecured band is profile led and modest, while larger abroad amounts need tangible collateral, much like a PSU. Axis usually prices a little above PSU floating rates but sanctions faster, and because it is a scheduled bank, the 80E interest deduction applies and CSIS is possible only if the scheme criteria are met.

A neighbour’s daughter had her SBI file sitting at a branch for six weeks last summer while her UK term start crept closer. She switched to Axis, got the sanction in under two weeks, and paid for it with a slightly higher rate. That trade, speed for a bit more interest, is the whole reason a private bank like Axis exists in this market. It is neither the cheapest money nor the most flexible, and the honest job of this post is to tell you exactly where it fits and where it does not.

I am not going to sell you on Axis. This is the same calm, who-does-it-actually-fit read I would give a cousin. The numbers below are illustrative postures, not quotes, because Axis revises its bands and rates often. The only figure that binds you is the one printed on your own sanction letter, so confirm everything at the branch.

To weigh this lender against the others: the canara bank education loan post, the bank of baroda education loan post, and the PNB education loan post.

What an Axis Bank education loan actually is

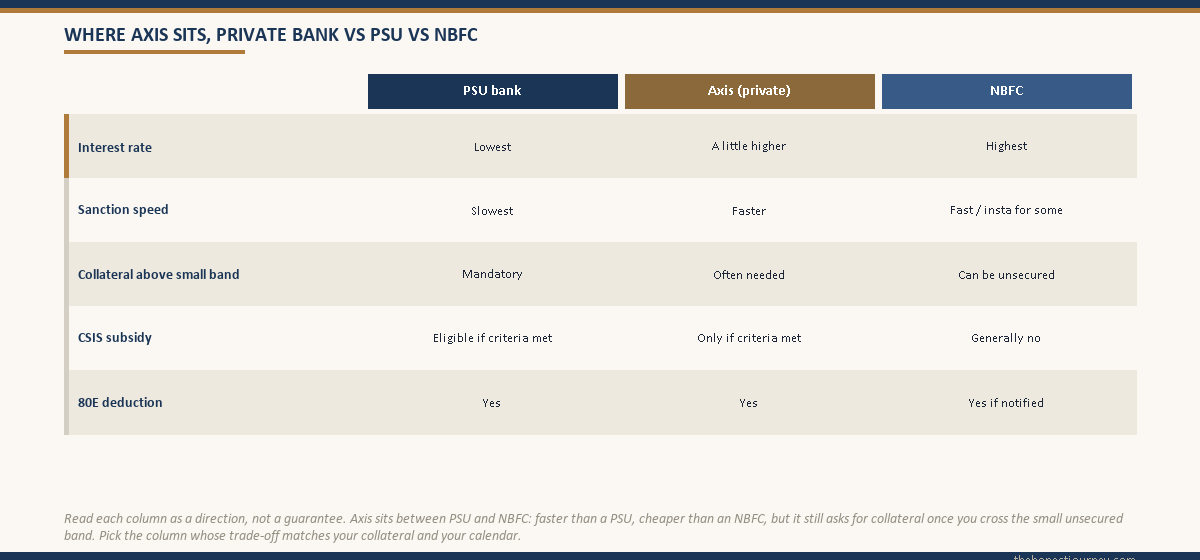

Axis is a private scheduled commercial bank, not a PSU and not an NBFC. That middle position shapes the whole product. Like a PSU, it follows the broad Indian Banks’ Association template and asks for collateral once the amount crosses a small unsecured band. Like an NBFC, it moves faster than a PSU branch and leans on the borrower profile and program quality. You get some of the speed of the NBFC world at a rate closer to, though usually above, the PSU world.

The product covers both domestic study and studies abroad. For abroad, Axis treats top destinations such as the US, UK, Canada and Australia as its main book, and the sanction is built on the admission letter and the certified cost of attendance from the institution, the same way every lender works. For the broader picture of how Indian education loans are structured across lenders, the education loan India complete guide sets the baseline this post sits inside.

How the amount bands and collateral work

The structure follows the familiar three-layer logic that every Indian education loan uses, and the layer you fall into decides your collateral and, to a large extent, your rate.

- A small unsecured band, where Axis lends against the co-applicant’s income and the borrower’s profile with no tangible security. This band is modest and profile led, nowhere near the size of an abroad Master’s ticket.

- A larger secured band, where tangible collateral becomes mandatory. This is where almost every abroad Master’s lands, because an abroad program runs well above the unsecured threshold.

- Above that, the amount scales with the value of the collateral and the co-applicant’s repayment capacity, up to the bank’s own product ceiling.

So the practical truth for an abroad student is the same as it is at SBI or Bank of Baroda: above the small unsecured band, you are pledging property, a fixed deposit or an LIC policy. Axis applies a valuation haircut on the security and wants the security value comfortably above the loan. The exact ceilings and thresholds shift, so cross-check against the maximum education loan amount in India post rather than trusting a single quoted figure.

One honest caveat. Some borrowers assume a private bank will hand them a large unsecured loan because the branch is friendlier and faster. It will not. Axis is still a bank, and above its unsecured band the collateral demand is real. If you have no collateral and need a large unsecured abroad loan, an NBFC is the structural answer, not a private bank, as the education loan for abroad studies without collateral post explains.

Faz's ruleA private bank is not a shortcut around collateral. Above the small unsecured band, Axis wants tangible security exactly like a PSU, it just processes it faster.

People hear private bank and assume easier money. Axis is friendlier on speed and paperwork, not on the collateral rule. If your abroad amount is large and you have nothing to pledge, you are looking at an NBFC, not Axis. Decide on the structure first, the brand second.

The rate posture, and why it sits above PSU

Axis usually prices its education loan a little above PSU floating rates and below the typical NBFC band. That is the structural position of a private bank. A PSU funds itself cheaply and runs on volume, so it offers the lowest rate but the slowest service. An NBFC takes more credit risk on unsecured lending, so it charges the most. Axis sits in between on both speed and price. If you are weighing private banks against each other, it is worth putting Axis next to the ICICI Bank education loan, since the two occupy the same middle slot and a small rate or speed difference between them can decide the case.

The gap to a PSU sounds small as a percentage, but on a large abroad loan over a long repayment it compounds into real money. That is the central trade you are weighing: is the faster sanction and smoother process worth paying a slightly higher rate over the whole loan life? For a small, time-critical case the answer is often yes. For a large loan with plenty of runway, the PSU rate usually wins. The full rate landscape across lenders is laid out in the education loan interest rate comparison post.

A worked INR example, Axis versus a PSU on the same case

Take a real-shaped case. A student admitted to a one-year Master’s in the UK with an all-in certified cost of around ₹30 lakh. The family can pledge a residential property, so collateral is not the constraint. The question is purely Axis versus a PSU on rate and speed. Assume an illustrative Axis rate of 11 percent against an illustrative PSU rate of 9.75 percent, both on a ₹30 lakh loan repaid over 10 years after the course and moratorium.

| Item | Axis (illustrative 11%) | PSU (illustrative 9.75%) |

|---|---|---|

| Loan amount | ₹30,00,000 | ₹30,00,000 |

| Indicative repayment tenure | 10 years | 10 years |

| Approx monthly EMI | ~₹41,300 | ~₹39,200 |

| Approx total interest over tenure | ~₹19.6 lakh | ~₹17.0 lakh |

| Extra interest cost of the Axis route | ~₹2.5 lakh over the loan life | |

| Sanction speed | Faster, often weeks | Slower, can be months |

The EMI and interest figures are rounded and indicative, meant to show the shape of the gap rather than to quote a rate. The lesson holds whatever the exact numbers: on a ₹30 lakh loan, a rate gap of just over a percentage point costs roughly ₹2.5 lakh of extra interest across the loan life. That is the price of the speed. If a PSU can fund you in time, that ₹2.5 lakh is money saved. If a PSU branch stalls and you would lose a whole year of earning by deferring, the speed is cheap at the price.

CSIS and the 80E deduction, hedged honestly

Two benefits get muddled constantly, so let me separate them cleanly.

The 80E income tax deduction lets you deduct the full interest paid on an education loan for up to eight years. It applies to loans from banks and notified financial institutions. Axis is a scheduled commercial bank, so the interest you pay on an Axis education loan qualifies for 80E. This is a genuine, reliable benefit and it slightly narrows the real cost gap to a PSU, because both qualify. The mechanics are in the secured versus unsecured education loan post where the cost comparison logic lives.

The Central Sector Interest Subsidy, CSIS, is different and far more conditional. It is an interest subsidy during the moratorium for economically weaker students within an income ceiling, on loans up to a capped amount, for study in India, claimed through scheme-eligible scheduled banks. Whether an Axis loan can route a CSIS claim depends on the scheme’s current rules and your eligibility, and for most abroad students the scheme does not apply at all because of the study-in-India and amount-cap conditions. Do not bank on CSIS through Axis for an abroad loan. Treat it as a maybe that you confirm in writing, never as a given.

Faz's rule80E is real and reliable on an Axis loan. CSIS is conditional and usually irrelevant for abroad study. Do not let a sales pitch blur the two.

Every scheduled bank loan, Axis included, earns you the 80E interest deduction, so factor that into both the Axis and the PSU column equally. CSIS is a narrow, income-capped, study-in-India subsidy that rarely touches an abroad Master’s. If a banker waves CSIS at you for a UK loan, ask them to show you the eligibility in writing.

Who an Axis Bank education loan actually fits

The honest fit is narrower than the marketing suggests, and that is fine. Axis is the right call when speed and process matter more than squeezing the last bit off the rate.

- You have collateral to pledge and a tight calendar, where a PSU branch is too slow to meet your term start.

- Your profile and program are strong, so the private bank prices you competitively and processes you quickly.

- You value a smoother, faster, more responsive process and are willing to pay a small rate premium for it.

- You want a scheduled bank loan, so the 80E benefit and a clean lender relationship are assured.

Who it does NOT fit

This is the section an agent will never give you, and it is the point of this whole site. Axis is the wrong choice in several common situations.

- You have no collateral and need a large unsecured abroad loan. Above its small unsecured band Axis wants security, so an NBFC is the structural fit, not a private bank.

- You are highly rate sensitive on a large, long loan with plenty of runway. A PSU’s lower rate will save you lakhs over the loan life, and the extra weeks of processing do not cost you a year.

- You are counting on CSIS to lower your cost. CSIS rarely applies to an abroad loan and should not drive your lender choice toward any private bank.

- You qualify comfortably for a PSU secured loan and your deadline is months away. The cheaper rate wins, plainly.

If your case is large, collateral backed and not time critical, compare Axis directly against the PSU benchmark in the SBI education loan for abroad studies post before you commit. The cheaper money is usually worth the wait when the calendar allows it.

The honest take on Axis Bank for an education loan

Axis is a competent, faster, slightly pricier middle option. It earns its place when your collateral is ready, your profile is strong and your calendar is tight, because then the speed it buys is worth the small rate premium. It loses its case when the loan is large and you have time, because then the PSU rate quietly saves you lakhs, or when you have no collateral, because then an NBFC, not a private bank, is the real answer.

Decide on the structure first. Work out whether you are a collateral case or a no-collateral case, and how tight your calendar really is. Only then does the brand on the sanction letter matter. Run the rate gap against your own loan size and tenure, the way the table above does, and let that number, not a friendly banker, make the call.

FAQ

Is Axis Bank good for an education loan for abroad?

Axis is a solid middle option for abroad study when you have collateral and a tight calendar. It processes faster than a PSU and usually costs less than an NBFC, while remaining a scheduled bank so the 80E deduction applies. It is not the cheapest money, and it still requires collateral above a small unsecured band. The honest fit is a borrower who values speed and a smooth process enough to pay a modest rate premium over a PSU.

Does Axis Bank give education loans without collateral?

Axis lends a modest unsecured amount against the co-applicant’s income and the borrower’s profile, but that band is far below the size of a typical abroad Master’s. Above it, tangible collateral such as property, a fixed deposit or an LIC policy becomes mandatory, much like a PSU. If you need a large unsecured abroad loan and have nothing to pledge, an NBFC is the structural answer rather than a private bank. Decide whether you are a collateral case before choosing the lender.

What is the interest rate on an Axis education loan?

Axis typically prices its education loan a little above PSU floating rates and below the usual NBFC band, which is the natural position of a private bank. The exact rate depends on your profile, the program, the collateral and the prevailing benchmark, and Axis revises its bands often. Treat any quoted figure as indicative until it appears on your sanction letter. On a large, long loan, even a small rate gap to a PSU compounds into lakhs of extra interest over the loan life.

Does the 80E tax deduction apply to an Axis education loan?

Yes. Section 80E lets you deduct the full interest paid on an education loan for up to eight years, and it applies to loans from banks and notified financial institutions. Axis is a scheduled commercial bank, so interest on an Axis education loan qualifies. This benefit applies equally to a PSU loan, so factor it into both columns when you compare. It does narrow the real cost slightly, but it does not change which lender is cheaper overall.

Can I claim CSIS on an Axis education loan?

CSIS is a narrow, income-capped interest subsidy during the moratorium, on capped loan amounts, generally for study in India, claimed through scheme-eligible scheduled banks. Whether an Axis loan can route a CSIS claim depends on the scheme’s current rules and your eligibility, and for most abroad students the scheme does not apply at all because of its study-in-India and amount-cap conditions. Do not let CSIS drive your choice toward a private bank. Confirm any subsidy eligibility in writing before you rely on it.

Is Axis faster than a PSU bank for an education loan?

Generally yes. A private bank like Axis processes education loans faster than a typical PSU branch, often in weeks rather than months, with a smoother and more responsive process. That speed is the main reason to choose Axis when your term start is close. The trade is a slightly higher rate. Whether the speed is worth the premium depends on your calendar: if missing the term costs you a whole year of earning, the faster sanction is cheap at the price.

How much collateral does Axis need for an abroad loan?

Above its small unsecured band, Axis requires tangible collateral whose value, after a valuation haircut, sits comfortably above the loan amount. Acceptable security usually includes residential property, a fixed deposit or an LIC policy, alongside a co-applicant with demonstrable repayment capacity. The exact threshold and acceptable security types shift with policy, so confirm at the branch. For almost every abroad Master’s, the amount lands in this secured band rather than the unsecured one.

Should I choose Axis or a PSU for my education loan?

Choose Axis when you have collateral ready, a strong profile and a tight calendar, because the faster sanction is worth a modest rate premium. Choose a PSU when the loan is large, you have plenty of runway and you want the lowest lifetime cost, because the cheaper rate saves lakhs over the loan life and the extra processing weeks do not cost you a year. Run the rate gap against your own loan size and tenure before deciding, and let that number make the call.

For the official product terms, see the Axis Bank education loan page, the regulatory framework on the RBI site, and the model education loan scheme published by the Indian Banks’ Association.

Faz · The Honest Journey · 2026