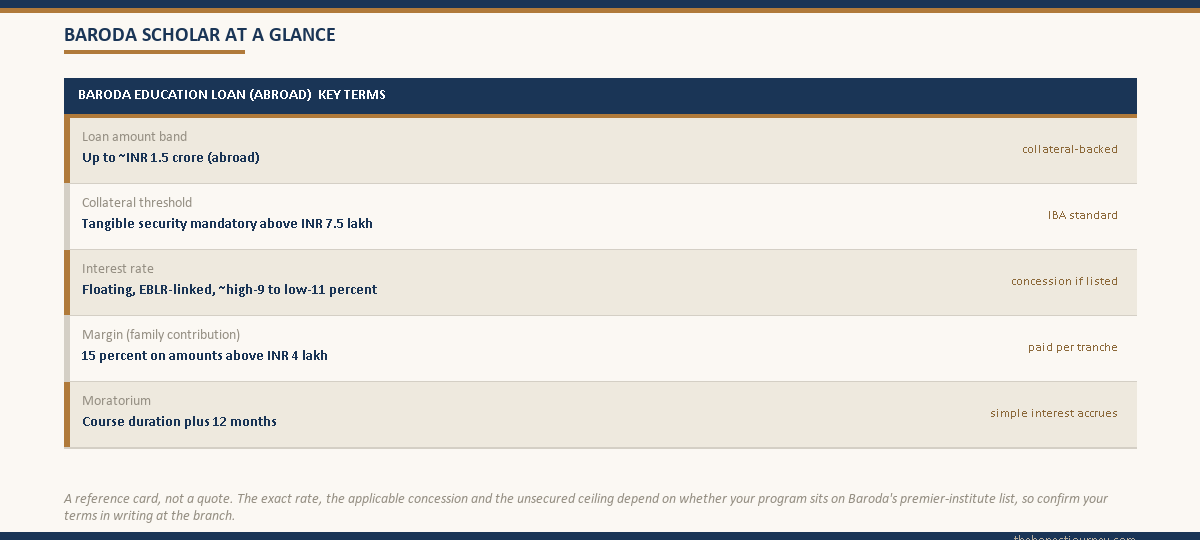

Bank of Baroda’s education loan for abroad studies runs under its Baroda Scholar scheme, sanctioning up to around ₹1.5 crore with collateral and capping the unsecured amount at ₹7.5 lakh for most students. The distinctive feature is a published list of premier institutes where Baroda offers a lower interest rate and, for some of those programs, a higher unsecured ceiling. For everyone outside that list the scheme is a standard IBA-model PSU loan with mandatory collateral above ₹7.5 lakh.

A neighbour’s daughter took a Baroda Scholar loan for a Master’s in the UK last year. What made her family pick Baroda over the bank they already used was one line on a PDF: her university sat on Baroda’s premier-institute list, which knocked close to a full percentage point off her rate and let her borrow more without pledging the family flat. A friend of hers, admitted to a perfectly good but unlisted university, got none of that and ended up at a different bank. Same scheme, two very different deals, and the only thing separating them was a list.

This post is the honest product picture for the Baroda education loan for abroad studies. It is the loan angle, the rate, the collateral, the premier-list concession and who the scheme actually fits, not a sales page. I will say plainly where Baroda is the right call and where it is not.

To weigh this lender against the others: the secured vs unsecured education loan post, the canara bank education loan post, and the axis bank education loan post.

What the Baroda education loan for abroad studies actually is

Bank of Baroda is a public sector bank, so its overseas education loan follows the Indian Banks’ Association model educational loan scheme like every other PSU lender. The abroad-studies version is marketed as Baroda Scholar. It covers tuition, examination and lab fees, the cost of books and equipment, travel for studies abroad, and reasonable living expenses, all built on the offer letter and the published cost of the program.

Because it is a PSU loan, two things follow that an NBFC loan does not give you. The interest qualifies for the Section 80E tax deduction, and eligible families can claim the central interest subsidy under CSIS during the moratorium. Those benefits are part of why families weigh a PSU loan against a faster NBFC sanction. The full picture of the Indian education loan landscape sits in the complete guide to education loans in India.

The official product terms live on the Bank of Baroda education loan page. Read that alongside this, because product specifics change and the bank’s own page is the version that binds you.

The amount band and the collateral threshold

The structure mirrors the IBA model that every PSU bank uses, and it splits the same way regardless of which bank’s logo is on the sanction letter.

- Up to ₹4 lakh: no margin and no collateral, parent as co-applicant. Almost no abroad program fits inside this.

- Above ₹4 lakh to ₹7.5 lakh: co-applicant and usually a third-party guarantee, no tangible collateral. Still below most abroad tickets.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory, which is where almost every abroad Master’s lands.

That ₹7.5 lakh line is the one that decides your life. A one-year UK Master’s runs ₹30 to 45 lakh all in, a two-year US program more, so the standard student is firmly in collateral territory. The exception, and the reason Baroda is worth a separate look, is the premier-institute list, where a higher unsecured ceiling can apply for some listed programs. The general ceiling picture across all banks is in the maximum education loan amount in India post.

The premier-institute concession, explained honestly

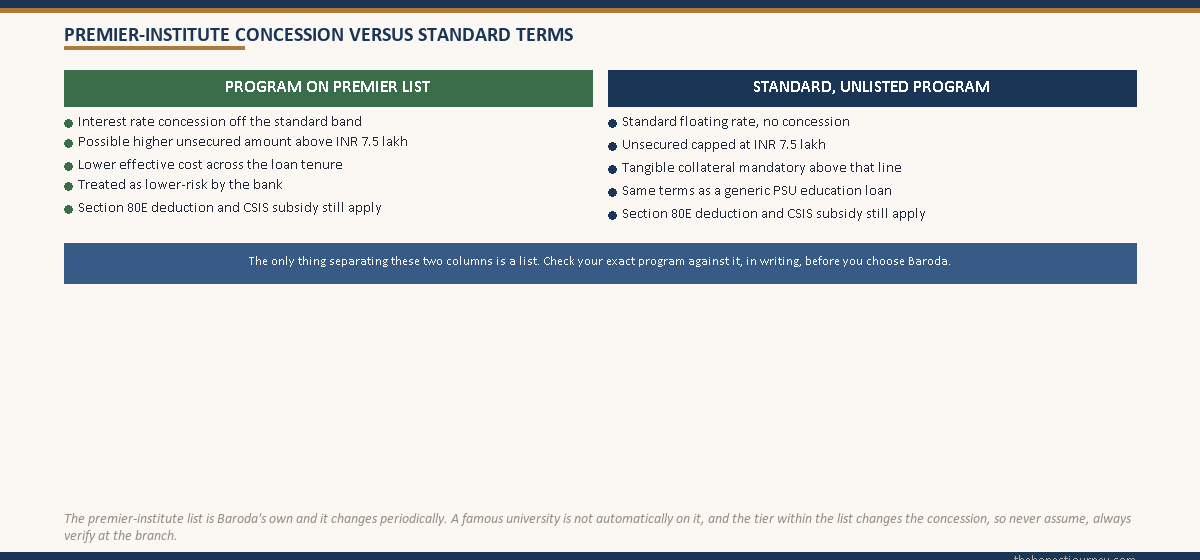

This is the one feature that genuinely distinguishes the Baroda scheme from a generic PSU loan. Bank of Baroda maintains a published list of premier institutes, both Indian and selected foreign ones, and students admitted to a program on that list get better terms than the standard borrower.

The concession works on two fronts. First, the interest rate. A listed-institute borrower gets a rate concession, often in the range of a quarter to close to a full percentage point off the standard rate, because the bank treats the program as lower risk. Second, for some listed programs the bank is willing to extend a larger unsecured amount than the ₹7.5 lakh standard ceiling, which is the part that can save a family from pledging property.

Here is the honest caveat. The list is specific, it changes, and the exact concession depends on the institute’s tier within the list and the bank’s current policy. Do not assume your university is on it because it is well known. Check the current list at the branch, in writing, before you build your plan around the concession. A program that feels prestigious to you may not be on Baroda’s list, and the standard terms then apply with no exceptions.

Faz's ruleConfirm in writing whether your exact program is on Baroda's premier-institute list before you choose this bank for the concession. The rate cut and the higher unsecured ceiling only exist for listed programs, and the list is narrower than most families assume.

A university being famous does not mean it is on the list. The list is Baroda’s own, it is updated periodically, and the tier within it changes the concession. Ask the branch to show you the current list and your program on it, then get the applicable rate quoted in writing on the sanction terms.

Rate, margin and moratorium

The interest is floating, linked to the bank’s external benchmark lending rate, the way all PSU education loans are now priced. For 2026 the effective rate for an abroad loan sits broadly in the high-9 to low-11 percent range depending on the loan amount, the collateral and whether the premier concession applies. A listed-institute borrower sits at the lower end of that band, a standard borrower nearer the upper end. Because it is floating, the rate moves when the benchmark moves, so model your repayment with a buffer rather than today’s exact number.

Margin money is the family’s own contribution. For studies abroad it is set at 15 percent of the loan amount above ₹4 lakh, paid alongside each disbursement rather than handed over upfront. On a ₹40 lakh loan that is roughly ₹6 lakh of family contribution spread across the disbursement schedule. Banks may fold a scholarship into the margin calculation, so confirm at the branch how yours is computed.

The moratorium, the period before you start full repayment, runs for the course duration plus an additional twelve months under the current IBA framework, or six months after getting a job, whichever is earlier. Simple interest accrues during the moratorium, and servicing that interest while you study reduces the amount that capitalises, so it is worth doing if the family can. How a comparable PSU rate stacks against the alternatives is laid out in the education loan interest rate comparison.

A worked INR example for a UK Master’s

Take a real-shaped case. Student admitted to a one-year taught Master’s at a UK university for the 2026 intake. The university total comes to GBP 35,000, made up of GBP 24,000 tuition and roughly GBP 11,000 of living and other costs that the bank will count. At ₹108 per pound that is ₹37.8 lakh.

| Item | GBP | INR (at 108) |

|---|---|---|

| Tuition and fees | 24,000 | 25,92,000 |

| Living, travel, other eligible costs | 11,000 | 11,88,000 |

| Total program cost | 35,000 | 37,80,000 |

This is above ₹7.5 lakh, so unless the program is on Baroda’s premier list with a higher unsecured ceiling, tangible collateral is mandatory. Say the university is not listed. The family pledges a residential flat valued at ₹70 lakh. Baroda applies a valuation haircut, counts a security value comfortably above the loan, and sanctions the ₹37.8 lakh. The standard floating rate applies, near the upper part of the band.

Now suppose instead the university is on Baroda’s premier list. The rate concession applies, dropping the effective rate, and depending on the institute’s tier the bank may extend a larger unsecured amount, reducing or removing the collateral need. The table below shows what the concession is worth on this same ticket.

| Scenario | Indicative rate | Collateral | Margin (15 percent) |

|---|---|---|---|

| Standard, unlisted program | ~10.75 percent | Property pledge mandatory | ~₹5,67,000 |

| Premier-list program | ~9.9 percent | Reduced or unsecured if listed tier allows | ~₹5,67,000 |

On a ₹37.8 lakh loan over a typical repayment, a rate gap of close to a percentage point is worth several lakh of interest across the life of the loan. That is the real value of the premier list, and it is why the single most important thing a Baroda applicant can do is confirm whether their program is on it.

Faz's ruleService the simple interest during the moratorium if the family can spare it. Interest that you pay while studying does not capitalise, which shrinks the balance you repay once the EMI begins.

The moratorium feels like free breathing room, but interest is quietly accruing the whole time. Paying even part of it monthly while you study means a smaller principal when full repayment starts. On a ₹40 lakh loan that habit can save a noticeable chunk over the full tenure.

Who the Baroda education loan fits, and who it does not

The honest fit test for Baroda Scholar comes down to two questions: is your program on the premier list, and does your family have collateral.

Baroda fits well if your program is on the premier-institute list, because then you get the rate concession and possibly a higher unsecured ceiling, which is a genuinely better deal than a generic PSU loan or an NBFC. It also fits the standard case where the family has tangible collateral to pledge and wants the lower PSU floating rate plus the 80E and CSIS benefits, and is not in a rush.

It does not fit, or fits poorly, in a specific situation. If your program is not on the premier list, your family has no collateral, and the ticket is well above ₹7.5 lakh, Baroda cannot do much for you. The standard unsecured ceiling is ₹7.5 lakh, the same as every PSU bank, so a large unsecured need pushes you toward an NBFC instead, which prices on the program’s earning potential rather than your collateral. The trade-offs of that unsecured route are covered honestly in the education loan for abroad studies without collateral post.

This is not a knock on Baroda. No PSU bank gives a large unsecured loan, so the limitation is structural, not specific to this bank. The point is to know which situation you are in before you spend three weeks in a branch queue for a loan the scheme cannot give you.

The tax and subsidy benefits, and what they are worth

Because Baroda is a PSU bank, the interest you pay qualifies for the Section 80E income tax deduction. The whole of the interest paid in a financial year is deductible from taxable income for up to eight years from the year repayment begins, with no upper cap on the amount. For a family in a higher tax bracket repaying a large loan, that deduction is a real reduction in the effective cost of the loan. The mechanics of claiming it are in the Section 80E tax benefit post.

Separately, eligible families may claim the central interest subsidy during the moratorium under the government scheme, which pays the interest that accrues while you study for borrowers within the income criteria. This is a PSU-only benefit that NBFC loans do not carry, and it is one of the honest reasons a slightly slower PSU sanction can beat a faster NBFC one for families who qualify. The official regulatory framework for these schemes sits on the RBI site and the model loan template is published by the Indian Banks’ Association.

The honest take on the Baroda education loan

Bank of Baroda’s education loan for abroad studies is a solid, standard PSU product with one feature that can make it the clear winner: the premier-institute concession. If your program is on that list, the rate cut and the possibility of a higher unsecured ceiling make Baroda genuinely worth choosing over a generic PSU loan, and the 80E and CSIS benefits stack on top.

If your program is not on the list, Baroda is simply one PSU bank among several, all priced and structured almost identically under the same IBA model. There is no special reason to prefer it over SBI or Canara in that case, so pick on branch responsiveness and your existing banking relationship rather than the brand. If branch speed is your real worry, a private bank like the ICICI Bank education loan processes faster than a PSU for a modestly higher rate, which can be the better trade when your term start is close. And if you have a large unsecured need with no collateral, no PSU bank, Baroda included, will solve it. That is an NBFC conversation.

The single action that decides whether Baroda is the right bank for you is checking the premier-institute list against your exact program, in writing, before you commit. Do that first. Everything else follows from the answer.

FAQ

What is the maximum Bank of Baroda education loan for abroad studies?

Under the Baroda Scholar scheme, Bank of Baroda sanctions up to around ₹1.5 crore for studies abroad, provided collateral and co-applicant income support the amount. The unsecured ceiling for most students stays at ₹7.5 lakh, the standard IBA figure, with tangible collateral such as property, fixed deposit or LIC required above that. For some programs on Baroda’s premier-institute list a higher unsecured amount may apply, so the exact ceiling depends on whether your program is listed.

What is the Baroda premier-institute list?

It is a published list Bank of Baroda maintains of premier Indian and selected foreign institutes whose students get better loan terms. Listed-program borrowers receive an interest rate concession, often a quarter to close to a full percentage point off the standard rate, and for some listed programs the bank may extend a higher unsecured amount than the ₹7.5 lakh standard. The list is specific and changes periodically, so confirm your exact program is on the current list at the branch before relying on the concession.

What interest rate does Bank of Baroda charge on an education loan?

The rate is floating, linked to the bank’s external benchmark lending rate. For 2026 an abroad education loan sits broadly in the high-9 to low-11 percent range, with listed-institute borrowers at the lower end and standard borrowers nearer the upper end. Because the rate floats with the benchmark, it moves over the life of the loan, so model your repayment with a buffer rather than assuming today’s exact rate holds for the whole tenure.

Is collateral needed for a Bank of Baroda abroad education loan?

For most students, yes. Any amount above ₹7.5 lakh needs tangible collateral such as property, fixed deposit or LIC, and almost every abroad program runs above that figure. The exception is some programs on Baroda’s premier-institute list, where a higher unsecured amount may apply and reduce or remove the collateral need. If your program is unlisted and the ticket is large, expect to pledge collateral, the same as at any PSU bank.

How much margin money does Bank of Baroda require?

For studies abroad the margin is 15 percent of the loan amount above ₹4 lakh, contributed by the family alongside each disbursement rather than upfront. On a ₹40 lakh loan that is roughly ₹6 lakh of family contribution spread across the disbursement schedule. Banks may fold any scholarship into the margin calculation, so confirm at the branch exactly how your margin is computed before you sign the sanction terms.

Does a Bank of Baroda education loan qualify for tax benefits?

Yes. Because Bank of Baroda is a public sector bank, the interest you pay qualifies for the Section 80E income tax deduction, which allows the full interest paid in a financial year to be deducted from taxable income for up to eight years from when repayment begins, with no upper limit. Eligible families may also claim the central interest subsidy during the moratorium, a benefit that NBFC loans do not carry.

What is the moratorium period on a Baroda education loan?

The moratorium, the period before full repayment begins, runs for the course duration plus an additional twelve months under the current IBA framework, or six months after getting a job, whichever is earlier. Simple interest accrues during this time, so servicing even part of it while you study reduces the balance that capitalises. Paying down the moratorium interest where the family can afford it lowers the principal you eventually repay once the EMI starts.

Should I choose Bank of Baroda over another PSU bank?

It depends on the premier-institute list. If your program is listed, Baroda’s rate concession and possible higher unsecured ceiling make it a genuinely better deal than a generic PSU loan. If your program is unlisted, Baroda is one of several near-identical PSU options under the same IBA model, so choose on branch responsiveness and your existing relationship rather than the brand. If you need a large unsecured loan with no collateral, no PSU bank can help, and an NBFC is the right conversation.

Faz · The Honest Journey · 2026