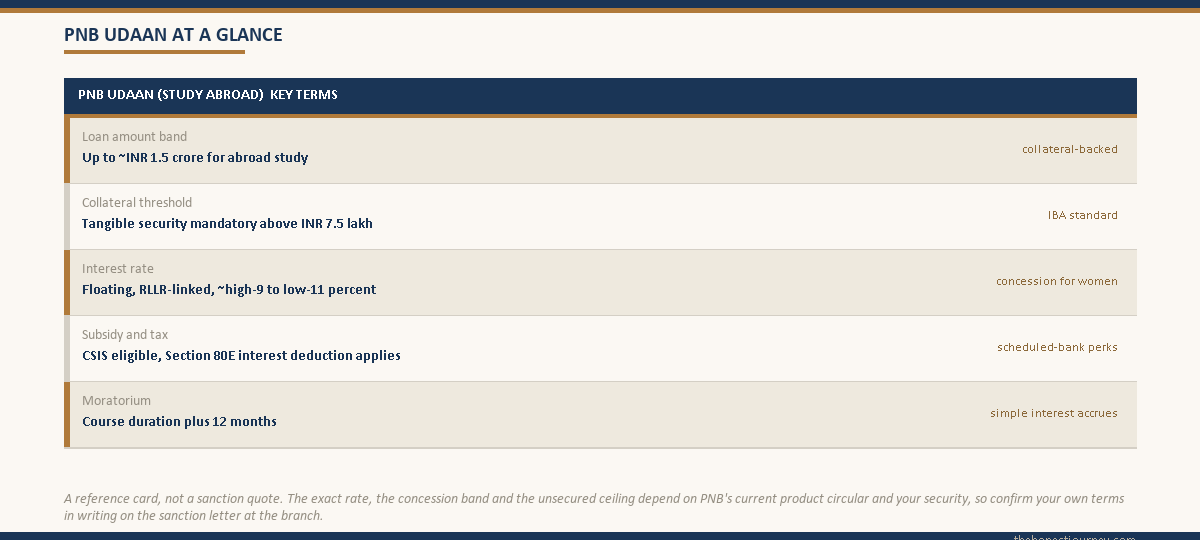

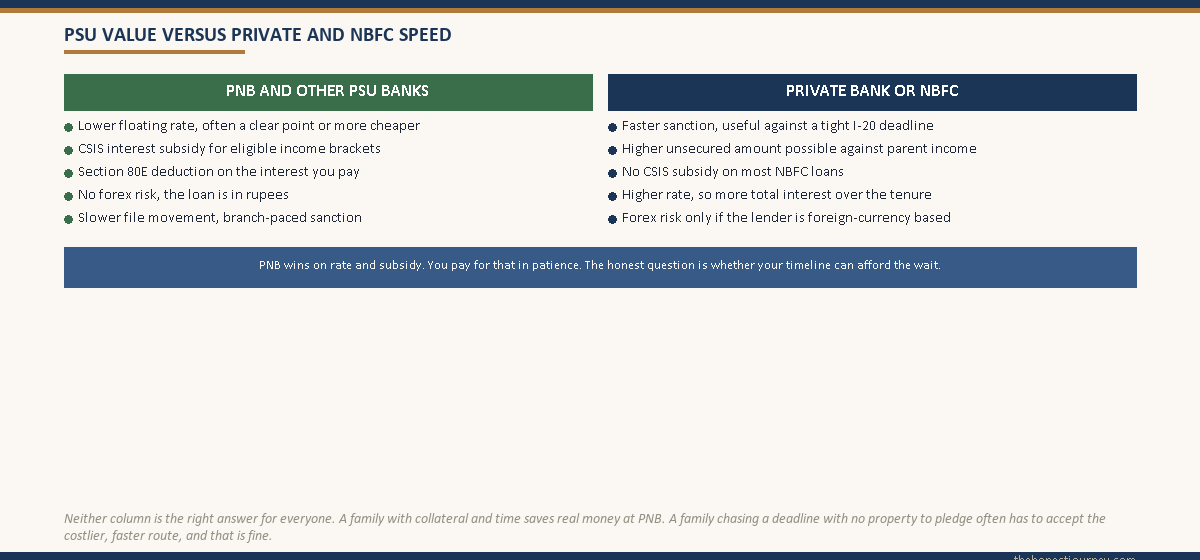

A PNB education loan follows the Indian Banks’ Association model scheme, so its unsecured ceiling stays around ₹7.5 lakh and secured study-abroad loans run up to roughly ₹1.5 crore against tangible collateral. The interest rate is floating and RLLR-linked, usually in the high-9 to low-11 percent band, lower than most NBFCs. PNB loans are CSIS subsidy eligible and qualify for the Section 80E interest deduction. The trade-off is speed: a PSU sanction moves at branch pace, not at the pace of a deadline.

A neighbour’s son got into a one-year Master’s in the UK and went to his local PNB branch with the offer letter, expecting a quick yes because the family already banked there. It was not quick. The valuation of the pledged flat took its own time, the file went up for a sanction approval above the branch limit, and the whole thing closed about six weeks after he started. He got a good rate and the CSIS subsidy in the end, but he spent those six weeks anxious about the university deposit deadline.

That is the honest shape of a PNB education loan. It is one of the cheaper, cleaner ways to fund a degree abroad, and it carries genuine subsidy and tax benefits that no NBFC can match. It is also slower and more collateral-hungry than the private alternatives, and for some students that matters more than the rate. This guide lays out who it really fits and who is better off elsewhere.

To weigh this lender against the others: the secured vs unsecured education loan post, the canara bank education loan post, and the bank of baroda education loan post.

How a PNB education loan is structured

Punjab National Bank is a public sector bank, so its education loan products sit on the Indian Banks’ Association model scheme that every PSU bank follows. For study abroad, PNB runs its IBA-scheme abroad loan alongside the “Udaan” branding for overseas education. The official product details live on the PNB website, and you should always read the live page because rates and caps change with each circular.

The structure splits by amount, and which band you land in decides your collateral, your margin and your effective rate.

- Up to ₹4 lakh: no margin, no collateral, parent as co-applicant. Almost no abroad program fits here.

- Above ₹4 lakh to ₹7.5 lakh: co-applicant plus, in many cases, a third-party guarantee, usually without tangible collateral. Still below a real abroad ticket.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory. This is where every realistic abroad Master’s lands.

The ₹7.5 lakh line is the wall, and it is not PNB being difficult. It is the IBA standard that all PSU banks apply. The broader ceiling picture across lenders sits in our maximum education loan amount in India guide, and the full mechanics of bank loans are in the education loan India complete guide.

The PNB rate, and why it tends to beat NBFCs

PNB prices its education loan off the Repo Linked Lending Rate (RLLR) plus a spread, so the rate floats with the RBI repo rate. In practice that has kept the headline education loan rate in the high-9 to low-11 percent range, with concessions in some circulars for women borrowers and for students at listed premier institutes. The regulatory frame for how banks set these floating rates sits with the RBI.

Compare that to an NBFC like Credila or Avanse, which typically prices unsecured abroad loans in the 11.5 to 13.5 percent band, and the PNB rate advantage is real. Over a long repayment that gap compounds into several lakh of extra interest on a large loan. The full lender-by-lender picture is in our education loan interest rate comparison.

But the rate only helps you if you can clear the collateral bar. The cheaper money at PNB is collateral money. If you have no property, FD or LIC to pledge above ₹7.5 lakh, the PNB rate is academic, because the bank will not sanction the amount you need unsecured.

Faz's ruleThe PNB rate advantage is only available to families who can pledge collateral. If you have nothing tangible to secure, the low PSU rate is not actually on the table for the amount you need, so do not anchor your budget on it.

I have watched families assume they will get the cheap PSU rate, plan their finances around it, and then discover at the branch that the unsecured ceiling caps them at ₹7.5 lakh. The rate you can actually access depends entirely on what you can secure. Settle your collateral question before you settle your rate expectation.

CSIS subsidy and the Section 80E benefit

This is where a PSU bank like PNB pulls genuinely ahead, and it is the part NBFC borrowers usually miss. PNB loans are eligible for the Central Sector Interest Subsidy (CSIS) for students from eligible income brackets, which covers the interest during the moratorium period for qualifying borrowers. The IBA administers the model scheme these benefits flow through, and the details are on the Indian Banks’ Association site. Most NBFC loans do not qualify for CSIS at all, which is a real cash difference, not a technicality.

Separately, the interest you pay on a PNB education loan qualifies for the Section 80E deduction, with no upper cap on the interest amount, for up to eight years of repayment. The mechanics of claiming it are in our CSIS interest subsidy guide. Stack the lower rate, the possible CSIS subsidy and the 80E deduction together, and the true after-benefit cost of a PNB loan can be meaningfully below an NBFC loan even before you count the headline rate gap.

The worked INR example: PNB versus an NBFC

Take a real-shaped case. A student admitted to a two-year Master’s abroad with a total funding need of ₹40 lakh. The family owns a flat they can pledge. We compare a PNB secured loan against an unsecured NBFC loan for the same amount, both over a 10-year repayment after the moratorium, to show the honest gap.

| Parameter | PNB (secured) | NBFC (unsecured) |

|---|---|---|

| Loan amount | ₹40,00,000 | ₹40,00,000 |

| Collateral | Flat pledged, above 7.5 lakh tier | None, parent co-applicant income |

| Indicative rate | ~10 percent floating | ~12.5 percent |

| Processing fee | Modest, often waived for some profiles | ~1 to 2 percent of loan |

| CSIS subsidy | Eligible if income criteria met | Generally not eligible |

| Section 80E | Applies | Applies (notified NBFCs) |

At roughly 10 percent over a 10-year repayment, the PNB loan carries materially less interest across its life than the same ₹40 lakh at 12.5 percent. The difference on a loan this size runs into several lakh of rupees over the full tenure, before you even add the CSIS subsidy advantage. Here is the rough shape of the interest difference.

| Funding layer | PNB at ~10 percent | NBFC at ~12.5 percent |

|---|---|---|

| Principal | ₹40,00,000 | ₹40,00,000 |

| Approx total interest over 10 years | ~₹23,00,000 | ~₹30,00,000 |

| Approx total repaid | ~₹63,00,000 | ~₹70,00,000 |

| Plus possible CSIS benefit | Reduces PNB cost further | Not available |

The numbers are indicative and depend on the exact rate, tenure and your repayment behaviour, so treat them as the shape of the gap, not a quote. What they show is that for a family with collateral, the PNB route is the cheaper one by a clear margin. The catch is everything that is not in the table: the speed, the paperwork patience and the branch process.

Margin and moratorium on a PNB abroad loan

For studies abroad, PNB asks for margin money, the family’s own contribution, typically 15 percent on the amount above ₹4 lakh. Margin is paid alongside each disbursement, not as one upfront lump, so on a ₹40 lakh loan you contribute roughly ₹6 lakh across the disbursement schedule while the bank funds the rest tranche by tranche.

The moratorium, the repayment holiday, runs for the course duration plus 12 months under the IBA scheme. Simple interest accrues during the moratorium. If you can service that simple interest while studying, you reduce the amount that capitalises into your principal, which lowers the total you eventually repay. Many families overlook this and let it all capitalise, which quietly inflates the loan.

Faz's ruleService the simple interest during your moratorium if you can, even partially. Letting it all capitalise into the principal is the most common way a cheap PSU loan quietly becomes an expensive one.

The moratorium feels like free breathing room, and it is, but the interest does not pause. Every rupee of moratorium interest you can pay while studying is a rupee that does not get added to your principal and then charged interest again. Even a parent paying it from home makes a difference over a two-year course.

Who a PNB education loan actually fits

A PNB education loan is a strong fit when several things line up together.

- The family has tangible collateral to pledge for the inevitable above-INR-7.5-lakh amount, so the cheaper secured rate is genuinely accessible.

- The student qualifies, or might qualify, for the CSIS subsidy on income grounds, which is a benefit only scheduled banks carry.

- The timeline has room. The admission was confirmed early enough that a six-week branch process will not collide with a deposit deadline.

- The family values the lowest total cost over speed, and is willing to do the paperwork and follow up at the branch to get there.

- The student wants the Section 80E deduction and the comfort of an established PSU lender.

This is the classic profile our SBI abroad study loan guide describes too. PNB sits comfortably alongside the other PSU banks as an option. If your branch relationship is with PNB, there is little reason to shop the other PSU banks unless their rate is clearly lower for your profile.

Who a PNB education loan does NOT fit

Being honest about the misfits matters more than the sales pitch, so here is where PNB is the wrong choice.

- Families with no collateral who need more than ₹7.5 lakh. PNB will not sanction a large unsecured loan against parent income the way an NBFC will. If you have nothing to pledge and need ₹30 lakh, PNB is structurally not your lender, and the unsecured route in our no-collateral education loan guide is where you should look.

- Students against a hard deadline. If your admission came late and you have weeks, not months, the PNB branch process can be too slow. A faster private bank or NBFC sanction can be worth the higher rate purely to secure the seat.

- Anyone whose program needs a sanction larger and faster than a PSU comfortably gives, such as a premier global Master’s where an NBFC will sanction unsecured to a much higher amount.

None of this makes PNB a bad lender. It makes it a specific kind of lender: cheaper, subsidy-bearing and slower, built for the family with collateral and time. Forcing it onto a no-collateral, deadline-driven case is where the frustration comes from.

The honest take on a PNB education loan

PNB is one of the most cost-effective ways an Indian family can fund a degree abroad, provided two conditions hold: you can pledge collateral for the amount above ₹7.5 lakh, and your timeline can absorb a branch-paced sanction. When both hold, the lower rate, the possible CSIS subsidy and the Section 80E deduction stack into a genuinely cheaper loan than any NBFC will give you.

When either condition fails, push back on your own instinct to chase the cheapest rate. A loan you cannot get sanctioned in time, or cannot get sanctioned at all without collateral you do not have, is not cheaper. It is unavailable. In those cases the higher-rate, faster, unsecured route is the honest answer, even though it costs more. Match the lender to your real situation, not to the lowest number on a comparison page.

FAQ

What is the maximum PNB education loan for studying abroad?

PNB sanctions study-abroad education loans up to around ₹1.5 crore under the IBA scheme, provided tangible collateral and co-applicant income support the amount. The unsecured ceiling stays at roughly ₹7.5 lakh, in line with the IBA model that all PSU banks follow. Anything above ₹7.5 lakh needs security such as property, fixed deposit or LIC. The exact cap for your profile depends on PNB’s current circular and your collateral value, so confirm it on the sanction letter.

What interest rate does PNB charge on an education loan?

PNB prices its education loan off the Repo Linked Lending Rate plus a spread, so it floats with the RBI repo rate. In recent circulars that has kept the rate in roughly the high-9 to low-11 percent band, often with a concession for women borrowers or students at listed premier institutes. This is generally lower than NBFC abroad rates of 11.5 to 13.5 percent. Read the live rate on the official PNB page, since it changes whenever the repo rate or the bank’s spread changes.

Is a PNB education loan eligible for the CSIS subsidy?

Yes, as a scheduled public sector bank PNB participates in the Central Sector Interest Subsidy scheme, so students from eligible income brackets can claim the moratorium-period interest subsidy on a qualifying loan. This is a real advantage over most NBFC loans, which generally do not qualify for CSIS. You must meet the scheme’s income and program criteria, and the subsidy is processed through the bank, so raise it at sanction and confirm your eligibility in writing rather than assuming it applies.

Does the Section 80E deduction apply to a PNB education loan?

Yes. The interest you pay on a PNB education loan qualifies for the Section 80E income tax deduction, with no upper limit on the interest amount, claimable for up to eight years from when repayment begins. It is the interest, not the principal, that is deductible. This applies to loans from scheduled banks and notified financial institutions taken for higher education, so a PNB loan is squarely covered. Keep your annual interest certificate from the bank to claim it.

How much collateral does PNB need for an abroad loan?

For any amount above ₹7.5 lakh, PNB requires tangible collateral such as residential property, a fixed deposit or an LIC policy, valued comfortably above the loan after the bank’s valuation haircut. Below ₹7.5 lakh the loan can be unsecured with a co-applicant and sometimes a third-party guarantee, but almost no abroad program costs that little. So in practice every realistic study-abroad PNB loan is a secured, collateral-backed loan, which is the main reason families without property look at NBFCs instead.

How long does a PNB education loan take to sanction?

A PNB sanction typically takes a few weeks, longer than a private bank or NBFC, because the file moves at branch pace and a secured loan adds a property valuation step plus, for larger amounts, an approval above the branch limit. Plan for four to six weeks from a complete application, and apply the moment your admission is confirmed. If your deadline is tight, the slower PSU timeline is the single biggest reason to consider a faster, costlier lender instead.

Is PNB better than an NBFC for an education loan?

It depends on your collateral and your timeline. PNB is cheaper, carries the CSIS subsidy and offers the Section 80E benefit, so for a family with collateral and time it is the lower total-cost choice by a clear margin. An NBFC is faster and lends larger amounts unsecured against parent income, so for a no-collateral or deadline-driven case it is often the only workable route despite the higher rate. Neither is universally better; match the lender to your situation.

What is the moratorium period on a PNB education loan?

Under the IBA model scheme PNB follows, the moratorium runs for the course duration plus 12 months, during which you are not required to pay EMIs. Simple interest accrues throughout the moratorium, however, and if left unpaid it capitalises into your principal once repayment begins. Servicing even part of the moratorium interest while studying reduces the total you eventually repay, so it is worth paying what you can rather than letting all of it capitalise into the loan balance.

Faz · The Honest Journey · 2026