An education loan for CA students in India covers up to ₹4 lakh without collateral for CA Foundation, Intermediate, and Final coaching plus ICAI fees, at interest rates of 9 to 12 percent. SBI Scholar, Canara, and Bank of Baroda offer dedicated CA schemes with a moratorium covering the course plus 6 months. Most banks treat CA as a professional course, so margin money requirements stay modest at 5 percent.

You have just registered for CA Foundation, the coaching institute quoted ₹55,000 for the classes, and your father did the quiet math out loud at the dinner table. He can manage it. He would just rather not break the FD he set aside for your sister’s wedding. So someone in the family said the obvious thing: take an education loan, the bank will give it for CA.

They will, but the picture is not the same as a degree loan, and a few of the assumptions floating around that dinner table are wrong. This post tells you exactly how an education loan for CA students works in India, what banks fund and what they quietly will not, and the one situation where I would tell you to wait.

Yes, CA students can get an education loan in India. The Chartered Accountancy course is recognised by banks as a professional course, and ICAI registration is the eligibility anchor. You can borrow roughly up to ₹7.5 lakh to 10 lakh without collateral and more against security, covering tuition, coaching, and exam fees. The catch is that loans for coaching alone, before you have cleared a single level, are the riskiest version of this.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

Other eligibility situations worth reading: the education loan rejection reasons india post, the education loan without ITR post, and the education loan for working professionals post.

Is the CA course actually loan-eligible?

The short answer is yes, and it is worth understanding why. The Institute of Chartered Accountants of India (ICAI) is a statutory body created by an Act of Parliament. When a bank assesses a loan application, a course run by a statutory professional body sits in the same recognised bucket as a university degree. The Indian Banks’ Association Model Education Loan Scheme, which most public sector banks follow and which is published on the IBA site, explicitly covers professional and technical courses, and CA qualifies.

So the eligibility anchor for an education loan for CA students is your ICAI registration. Once you are registered for CA Foundation, Intermediate, or Final, you have a recognised course in progress, an admission record, and a fee structure the bank can attach the loan to. That is the document that turns “I want to study CA” into a financeable application.

Here is the part most lender blogs skip. There are two very different things people lump together as a “CA loan”, and banks treat them differently.

| What you are funding | What it is | Who funds it well |

|---|---|---|

| ICAI course fees | Registration, exam fees, articleship-related costs, study material | Public sector banks, comfortably, under the Model Scheme |

| Private coaching fees | Foundation, Inter, and Final classes from a private coaching institute | Funded when bundled with the course, harder as a standalone |

| Coaching only, level not yet cleared | A loan purely for classes, before you have passed any CA level | NBFCs and some private banks, at higher rates |

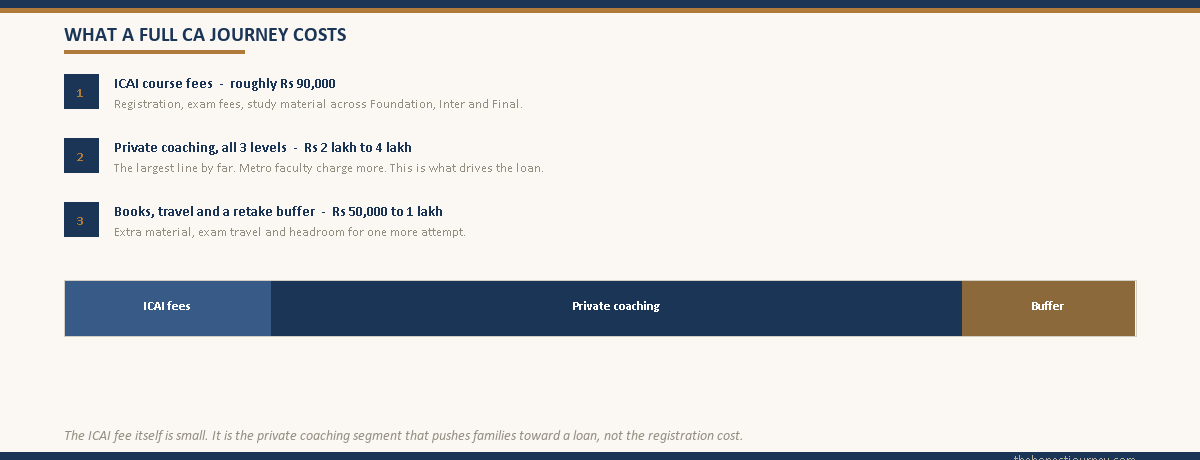

The ICAI course fees themselves are not large. CA Foundation registration, Intermediate, Final, and articleship registration together run well under ₹1 lakh across the whole journey. The number that pushes families toward a loan is private coaching. A full set of Foundation, Inter group classes, and Final classes from a well-known coaching brand can total ₹2 lakh to 4 lakh, and in metro cities the better-known faculty charge more. That coaching cost is the real reason most CA students look at a loan.

How much loan can a CA student actually get?

The loan amount for a CA student follows the same collateral logic as any education loan in India, and the thresholds are set by RBI and the IBA Model Scheme rather than invented by each bank.

| Loan slab | Security required | Typical rate band |

|---|---|---|

| Up to ₹4 lakh | No collateral, no third-party guarantee, co-applicant only | Around 9% to 11.5% at public sector banks |

| ₹4 lakh to 7.5 lakh | No collateral, but a third-party guarantee may be asked | Around 9.5% to 12% |

| Above ₹7.5 lakh | Tangible collateral usually required | 8.5% to 11% secured, higher at NBFCs unsecured |

For a domestic CA student, the realistic borrowing need is almost never above ₹7.5 lakh. The whole CA journey, ICAI fees plus full coaching plus a buffer for retakes and material, lands somewhere between ₹3 lakh and 7 lakh for most students. That keeps you inside the collateral-free zone, which is the comfortable place to be. You can read the deeper breakdown of how the no-collateral threshold works in the education loan without collateral guide, and the logic is the same for a CA loan even though that post is framed around abroad studies.

NBFCs will lend larger amounts for coaching, sometimes ₹10 lakh and above, and they will move faster than a public sector bank. The trade is rate. An NBFC coaching loan can sit at 12% to 15%, and some are structured more like a personal loan with a coaching label than a true education loan. Before you sign with an NBFC, check whether the product is registered as an education loan, because that classification is what decides your Section 80E tax benefit and your moratorium structure.

Faz's ruleFor most CA students the right loan is small, secured by nothing, and from a public sector bank.

The CA journey rarely needs more than ₹7 lakh. That keeps you in the collateral-free band where public sector banks lend at single-digit to low-double-digit rates. The moment you are quoted 14% by an NBFC for a coaching loan, ask why a small recognised-course loan needs an NBFC at all.

Who funds it: banks versus NBFCs

Public sector banks are the natural home for a CA education loan. State Bank of India, Bank of Baroda, Punjab National Bank, Canara Bank, and others run education loan products under the IBA Model Scheme, and a recognised professional course with ICAI registration fits cleanly. SBI’s education loan range is documented on its official education loans page, and the structure there, collateral-free up to a threshold then secured above it, is the template the sector follows.

The honest friction with public sector banks is process. They will ask for the full document set, they will want the co-applicant’s income proof, and they may take two to four weeks. They are also more comfortable when the loan is tied to the ICAI course with a clear fee schedule, and slightly less comfortable funding a standalone private coaching package with no university behind it.

NBFCs and some private banks fill that gap. They will fund a coaching-heavy package, they will decide faster, and they will lend larger amounts. You pay for that in rate and sometimes in structure. This is the same banks-versus-NBFC tension that runs through every education loan, and the documents both will ask for are listed in the documents required for education loan post.

The co-applicant matters more than students expect. A CA student is usually 18 to 21 years old with no income, so the loan is effectively underwritten on the parent or guardian who signs as co-applicant. Their income, their FOIR, and their credit history carry the file. If the co-applicant’s profile is thin, the loan will be smaller or rejected regardless of how good a CA candidate you are. The full picture of how this works is in the co-applicant education loan guide.

The articleship reality and when repayment starts

This is the section that separates an honest CA loan guide from a lender brochure, so read it slowly.

An education loan has a moratorium, a period during which you do not pay EMIs. For a degree loan it usually runs course duration plus six to twelve months. For CA the picture is messier, because the “course” includes three years of articleship, and articleship is when you earn a stipend, not a salary.

ICAI sets minimum monthly stipend rates for articled assistants, and they are modest. Depending on the city category and the year of articleship, the minimum stipend runs from a few thousand rupees to low five figures per month. Many firms pay above the minimum, and a student at a large firm in a metro can earn meaningfully more, but the honest planning number is that articleship income is small relative to a loan EMI.

So the question that decides whether a CA loan is comfortable is simple: when does your EMI start, and what is your income at that point?

| Moratorium ends | Your likely income then | How comfortable the EMI is |

|---|---|---|

| During articleship | ICAI stipend, modest | Tight. Interest may have capitalised, EMI feels heavy |

| Shortly after qualifying as CA | Fresher CA salary, ₹7 lakh to 12 lakh a year typical | Manageable if the loan was sized to roughly ₹5 lakh to 7 lakh |

| Student has not cleared a level yet | No qualification, no clear income path | This is the dangerous case. See below |

Interest accrues during the moratorium even though you are not paying EMIs, and on most loans it is added to your principal at the end of the moratorium. That mechanic, and why servicing the interest early matters, is explained in detail in the education loan moratorium and interest post. For a CA student the practical takeaway is this: if you can pay even the monthly interest out of your articleship stipend, do it. It stops the balance from compounding into a number that your fresher CA salary then struggles to service.

Faz's ruleServicing the interest during articleship is the single highest-value move a CA borrower can make.

Articleship pays a stipend, not a salary, but even a partial interest payment stops capitalisation. A student who services interest through three years of articleship starts EMIs on the original principal, not a balance inflated by 30 to 40 months of compounding. That gap is often ₹1 lakh to 2 lakh on a ₹6 lakh loan.

The honest caution: a coaching loan before you have cleared a level

Here is the one situation where I would tell a family to pause.

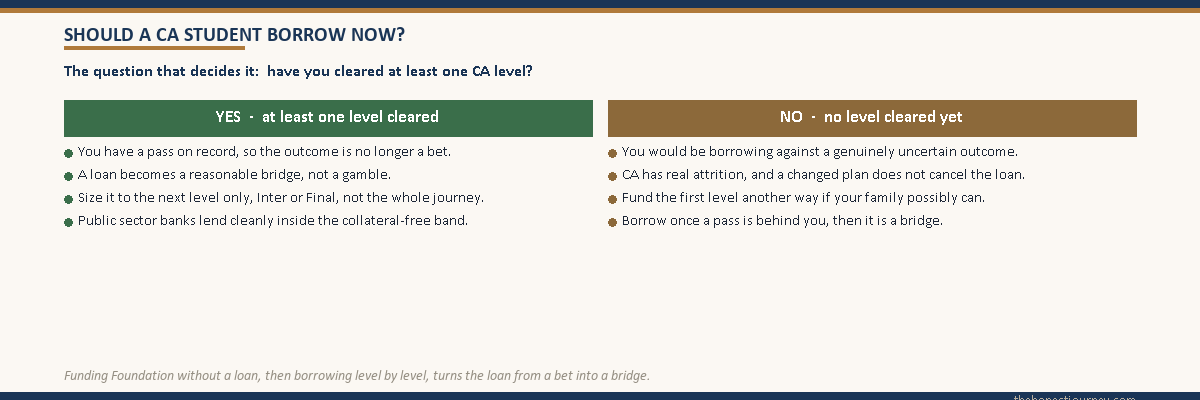

CA has a real and well-known attrition rate. A large share of students who register for Foundation do not clear it on the first attempt, and the funnel narrows again at Intermediate and Final. That is not a discouragement, it is just the reality of a tough professional exam. But it changes the risk of a loan.

If you take a loan purely to fund private coaching for CA Foundation, and you have not yet cleared a single level, you are borrowing against an outcome that is genuinely uncertain. If you clear, the loan was a sound bridge. If you do not clear and you decide CA is not your path, you are left servicing a loan with no qualification and no clear income from it. The loan does not disappear because the plan changed.

This is not a reason to never borrow for coaching. It is a reason to borrow proportionately. A few honest filters:

| Situation | Honest call |

|---|---|

| Family can fund Foundation coaching from income or a small saving | Do that. Borrow later for Inter and Final once you have cleared a level |

| You have cleared Foundation, now funding Inter and Final coaching | A loan is reasonable. You have proven you can clear levels |

| You have cleared Inter, articleship underway, funding Final | A loan is sound. You are deep in the course with income visible ahead |

| Borrowing the full CA journey upfront before clearing anything | The riskiest version. Borrow level by level instead |

The cleanest approach for many families is to fund the first level, Foundation, without a loan if at all possible, and then borrow for Intermediate and Final once the student has a pass on record. That sequencing turns the loan from a bet into a bridge.

Section 80E: the tax benefit on a CA loan

One genuine advantage of using a proper education loan rather than a personal loan or breaking an FD is the tax deduction. Section 80E of the Income Tax Act allows a deduction on the interest paid on an education loan taken for higher education, and the Chartered Accountancy course qualifies as higher education for this purpose.

The key features of Section 80E, confirmed on the Income Tax Department site, are worth knowing. The deduction is on the interest component only, not the principal. There is no upper limit on the interest amount you can claim. It can be claimed for up to eight years starting from the year repayment begins, or until the interest is fully repaid, whichever is earlier. It can be claimed by the person repaying the loan, which is usually the co-applicant parent during the early years.

One condition that matters: Section 80E only applies if the loan is taken from a bank or a notified financial institution, and only on a loan that is actually classified as an education loan. A personal loan dressed up as a coaching loan, or an informal family loan, does not qualify. This is another reason to keep the borrowing inside a real education loan product. The full mechanics are covered in the Section 80E tax benefit guide. Note also that the deduction only has value if the person repaying files under the old tax regime, since the new regime removes most such deductions.

Faz's ruleA proper education loan keeps Section 80E open. A personal loan for coaching closes it.

The interest on a recognised CA education loan is fully deductible under Section 80E for eight years. A personal loan at a higher rate with no 80E benefit is the worst of both worlds. If a lender offers you a quick coaching loan, ask in writing whether it is classified as an education loan.

Three CA students, three honest outcomes

Numbers are clearer with people attached, so here are three anonymised but realistic versions of how this plays out.

The first is a 19-year-old from a tier-2 city whose family funded Foundation coaching themselves, around ₹50,000, from monthly income. She cleared Foundation, then took a ₹5 lakh education loan from a public sector bank for Intermediate and Final coaching plus material. She serviced the interest during articleship from her stipend, modestly but consistently. She qualified, joined a mid-size firm at roughly ₹9 lakh a year, and the EMI on the original principal was comfortable. The loan did exactly what a loan should.

The second is a 21-year-old who took a ₹7.5 lakh loan covering the full CA journey upfront, including Foundation, from an NBFC at around 13.5%. He cleared all levels but took an extra attempt at Final, which extended his moratorium and let interest capitalise. He qualified, but started EMIs on a balance noticeably larger than ₹7.5 lakh. It worked out, his CA salary covered it, but he paid more than he needed to because the loan was oversized and the rate was high. A smaller, level-by-level loan from a bank would have cost him less.

The third is the case that should give every family pause. A 20-year-old borrowed ₹4 lakh purely for Foundation and Intermediate coaching, before clearing anything. After two unsuccessful attempts at Foundation he decided CA was not his path and moved to a different career. The qualification never arrived, but the loan did not go anywhere. His parents, the co-applicants, ended up repaying it from their own income. Nothing went wrong with the bank. The plan simply changed, and the loan was not built to flex with it.

The honest closing take

An education loan for CA students is a real, legitimate, and often sensible tool. The course is loan-eligible, the amounts needed are modest, public sector banks lend at reasonable rates inside the collateral-free band, and Section 80E gives a genuine tax benefit if you use a proper education loan.

What I would not do is borrow the entire CA journey upfront before you have cleared a single level. CA is a hard exam with real attrition, and a loan taken against an uncleared outcome is a bet, not a bridge. Fund the first level another way if your family possibly can, prove you can clear levels, then borrow for what is left. If you are already articled and funding Final, a loan is sound and you should service the interest from your stipend so the balance does not compound past you.

Size it small, keep it inside a recognised education loan product so 80E stays open, and match the EMI start to a point where you are a qualified CA earning a salary rather than an articled assistant on a stipend. Do that, and the loan is a tool. Get the timing and the size wrong, and it is a weight your co-applicant carries. You know your own exam confidence and your family’s finances better than any bank does. The decision is yours to make.

FAQ

Can CA students get an education loan in India?

Yes. The Chartered Accountancy course run by ICAI is a recognised professional course, and banks treat it like any other higher-education course for lending purposes. Your ICAI registration is the eligibility anchor. Public sector banks lend for CA under the IBA Model Education Loan Scheme, covering registration, exam, coaching, and material costs. The loan is underwritten largely on a co-applicant, usually a parent, because most CA students have no independent income at the time of borrowing.

Does an education loan cover CA coaching fees?

It can. Banks comfortably fund the ICAI course fees, and they will also fund private coaching when it is bundled into the loan with a clear fee schedule. A standalone coaching loan, with no ICAI course attached, is harder to get from a public sector bank and is more often funded by NBFCs at higher rates. Since coaching is usually the largest cost in a CA journey, it is the main reason families look at a loan in the first place.

How much loan can a CA student get?

Most CA students can borrow within the collateral-free band, which runs up to roughly ₹7.5 lakh, and the full CA journey rarely needs more than that. Loans up to ₹4 lakh need only a co-applicant, ₹4 lakh to 7.5 lakh may need a third-party guarantee, and amounts above ₹7.5 lakh usually require tangible collateral. NBFCs will lend larger sums for coaching but at notably higher interest rates, so larger borrowing is rarely necessary for a domestic CA student.

Is collateral needed for a CA education loan?

Usually not. Because the borrowing need for a CA course is modest, most students stay inside the collateral-free zone of up to about ₹7.5 lakh, where no property or asset needs to be pledged. A co-applicant with a stable income and a clean credit history is what carries the file. Collateral only comes into the picture if you borrow above the ₹7.5 lakh threshold, which is uncommon for a domestic CA student.

Can I claim Section 80E tax benefit on a CA education loan?

Yes. The CA course qualifies as higher education under Section 80E of the Income Tax Act, so the interest paid on a CA education loan is fully deductible, with no upper limit, for up to eight years from the year repayment starts. The deduction applies only to the interest, not the principal, and only if the loan is taken from a bank or notified financial institution. It has practical value only if the person repaying files under the old tax regime.

Which bank is best for a CA education loan?

There is no single best bank, but public sector banks such as State Bank of India, Bank of Baroda, Punjab National Bank, and Canara Bank are the natural choice for a CA loan. They lend under the IBA Model Scheme at reasonable rates and treat the ICAI course cleanly. They are slower and document-heavy compared with NBFCs, but for a modest, recognised-course loan the lower interest rate usually outweighs the slower process. Compare the rate and the moratorium terms before deciding.

Should I take a loan for CA coaching before clearing any level?

I would be cautious here. CA has real attrition, and a loan taken purely for coaching before you have cleared a single level is borrowing against an uncertain outcome. If you clear, it was a sound bridge. If you do not and you change paths, the loan still has to be repaid, usually by your co-applicant parent. Where possible, fund the first level another way and borrow level by level once you have a pass on record.

When does repayment start on a CA education loan?

Repayment is governed by the moratorium, which is the course period plus a grace window, typically six to twelve months. For CA the course period includes articleship, so EMIs often begin around the time you qualify or shortly after. Interest still accrues during the moratorium and is usually added to the principal at the end. Servicing even the monthly interest from your articleship stipend prevents that capitalisation and meaningfully lowers your eventual EMI.

Faz · The Honest Journey · 2026