MPOWER Financing is a US-based lender that funds international students at approved US and Canada schools with a fixed-rate dollar loan, no cosigner and no collateral, usually for the final year or two. The fixed APR is high, often around 12 to 15 percent, and the dollar loan leaves the forex risk on you. For families with collateral or a strong co-applicant, a rupee loan costs less.

I have watched two students take the MPOWER route, and they could not have had more different outcomes. The first was a Master’s student who stayed and worked in the US after graduation, earning in dollars, repaying a dollar loan, with the forex risk neutral because income and debt were in the same currency. For her it worked cleanly. The second came home after his program, took a rupee salary, and spent the next few years sending dollar EMIs back across a weakening rupee, paying more in real terms every year than the headline rate suggested. Same lender, same product, two very different costs, decided almost entirely by where they ended up earning.

This post is the honest read on MPOWER Financing: what it is, the genuine advantages, the real catch, and the specific students it fits versus the larger group who would be better off elsewhere. It is not an endorsement and there is no affiliate angle. It is the cost and the risk, laid out plainly.

To compare this NBFC against the alternatives: the PSU bank vs NBFC education loan post, the avanse education loan post, and the InCred education loan post.

What MPOWER Financing actually is

MPOWER Financing is a private lender based in the United States. Like Prodigy Finance, its whole reason for existing is that it lends to international students without a cosigner and without collateral, which most US lenders will not do. It serves international and DACA students at a list of approved universities in the United States and Canada, and it underwrites on the student’s academic profile and future earning potential rather than on a US-based guarantor or pledged security.

Two features set it apart from Prodigy and from rupee lenders. First, its loans are fixed-rate, so the APR is locked for the life of the loan and does not float, which gives certainty on the dollar EMI even if it gives no protection from forex movement. Second, MPOWER typically funds the final one or two years of a program rather than the whole degree, and it caps the amount it will lend, so it often sits as a top-up alongside other funding rather than as the sole source. It also reports to US credit bureaus, so on-time repayment helps an international student build a US credit history, which is a genuine and underrated benefit if you intend to stay and work in the US.

And, like every foreign lender, the loans are in US dollars. That is the hinge the honest assessment turns on.

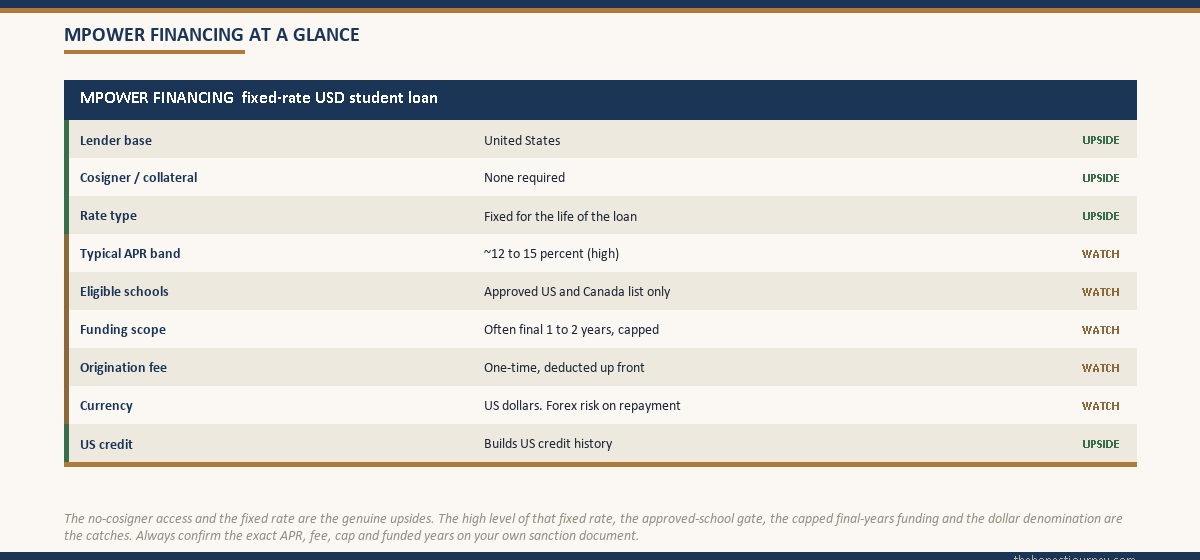

The MPOWER spec, at a glance

It helps to see the core terms as a single card, because the shape of this loan, fixed-rate, dollar-denominated, no cosigner, capped, final-years, is what determines whether it fits you.

Read down that card and the trade-offs are visible at once. The no-cosigner, no-collateral access is the upside, and for a student with no US guarantor and no Indian collateral it is the door that opens. The fixed rate is a comfort, you know the dollar EMI. But the rate is high, the fee is real, the school must be on the approved list, the coverage is capped and usually limited to the final years, and the dollar denomination means forex risk on every repayment made from India.

Faz's ruleTreat MPOWER as a top-up for the final years, not as full funding for the whole degree. It caps the amount and often funds only the last one or two years, so you need a plan for the rest.

Many students discover late that MPOWER will not cover the entire program. Map your full multi-year funding before you rely on it, because a gap in year one that you expected MPOWER to fill can leave you scrambling. Know the cap and the funded years in writing first.

How MPOWER underwrites, and why the school matters

MPOWER underwrites without a cosigner by leaning on the same logic Prodigy uses: the strength of the school and program, plus the student’s projected post-study earning power, stand in for a guarantor. It assesses your academic record and the salary outcomes typical of your program, then sizes the loan against the cost of attendance and its own cap.

The hard gate is the approved-school list. MPOWER lends only to students at universities it has approved in the US and Canada. If your school is not on the list, you are not eligible, full stop. This is the most common reason an applicant is turned away, exactly as with Prodigy. So the first thing to confirm, before any planning, is whether your specific university is approved. The broader no-collateral landscape for Indian students sits in the education loan for abroad studies without collateral guide, and the no-co-applicant angle is in the education loan without a co-applicant post.

The real catch: high fixed APR plus forex risk

The fixed rate is genuinely reassuring, but do not let it disguise two things. First, the level of that fixed rate is high, often in the 12 to 15 percent band, well above a PSU rupee floating rate near 9.5 to 11 percent. A fixed rate that is fixed at a high number is still a high cost. Second, fixing the dollar rate does nothing about forex risk. The rate is locked in dollars, but the rupee cost of each dollar EMI still moves with the exchange rate.

The honest way to show this is to run the same MPOWER loan under two exchange-rate scenarios.

| Item | Scenario A: rupee stable | Scenario B: rupee weakens |

|---|---|---|

| Loan amount | USD 40,000 | USD 40,000 |

| Fixed APR | 13.5 percent | 13.5 percent |

| Tenure | 10 years | 10 years |

| Monthly EMI (USD) | ~USD 609 | ~USD 609 |

| Exchange rate at repayment | ₹84 per USD | ₹92 per USD |

| Monthly EMI in rupees | ~₹51,160 | ~₹56,030 |

| Total repaid (USD) | ~USD 73,080 | ~USD 73,080 |

| Total repaid in rupees | ~₹61.4 lakh | ~₹67.2 lakh |

The fixed dollar APR and the dollar EMI are identical in both columns. The fix did its job: the dollar cost is locked. But the rupee cost rises by roughly ₹5.8 lakh purely because the rupee weakened by eight rupees over the repayment years. A fixed rate protects you from rate movement, not from currency movement. If you earn in dollars in the US while repaying, this risk largely disappears because income and debt share a currency. If you return to India on a rupee salary, you carry the full forex spread, and you must budget for the weak-rupee column, not the calm one.

Faz's ruleA fixed dollar rate is not a fixed rupee cost. Budget the loan at a weaker rupee than today, because the currency risk survives even when the interest rate is locked.

The fixed rate lulls people into thinking the cost is settled. It is settled in dollars, not in rupees. If you will repay from India, run the math at an exchange rate several rupees worse than today. The student who plans for the calm scenario and meets the stormy one is the one who feels squeezed.

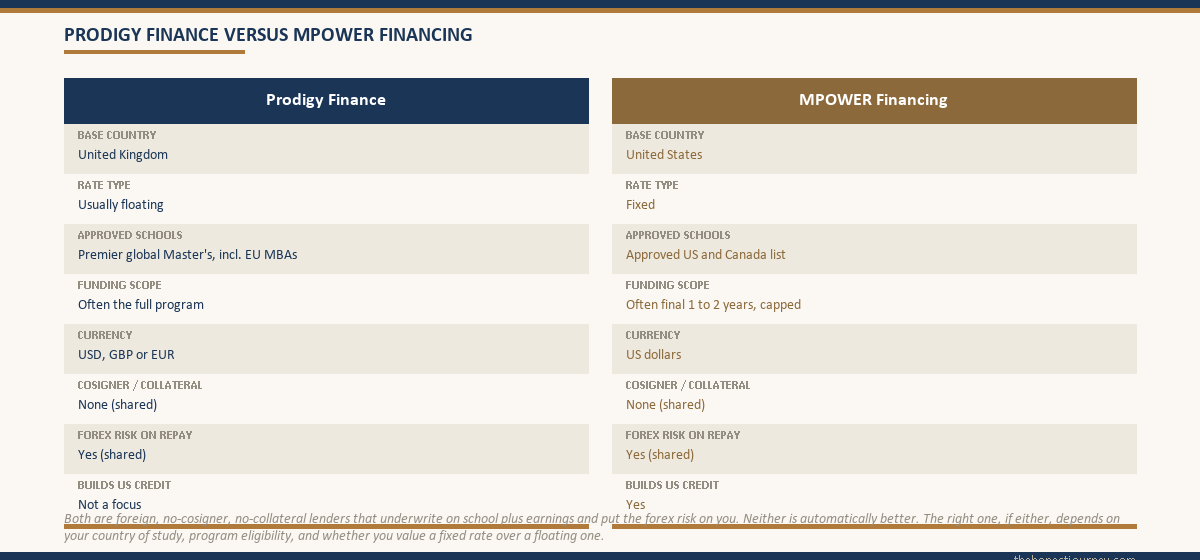

Prodigy versus MPOWER, side by side

Because students often weigh these two together, the honest comparison is worth being explicit about. Both are foreign, no-cosigner, no-collateral lenders that underwrite on school plus earnings, and both put the forex risk on you. The differences are in the details. Prodigy is UK-based, tends to be floating-rate, funds a curated set of premier global Master’s including European MBAs, and lends in dollars, pounds or euros. MPOWER is US-based, is fixed-rate, focuses on approved US and Canada schools, often funds only the final years up to a cap, and builds US credit. Neither is automatically better. The right one, if either, depends on your country of study, your program’s eligibility, and whether you value a fixed rate over a floating one. The full honest write-up of the UK-based option sits in the Prodigy Finance guide. If you are set on a US Master’s and want one more collateral-free dollar option to weigh, our Leap Finance education loan guide covers a SOFR-linked floating-rate route that some students compare against MPOWER’s fixed rate.

The cost beyond the rate, and the tax angle

As with any foreign loan, the origination fee adds to the true cost. MPOWER charges a one-time fee as a percentage of the loan, typically deducted up front, so you receive less than you borrow while paying interest on the full amount, which lifts the effective APR above the headline fixed rate.

The tax picture also works against it for an Indian borrower. Section 80E of the Income Tax Act lets you deduct education-loan interest from taxable income, but it applies to loans from Indian banks and notified Indian financial institutions. A loan from a US lender like MPOWER generally will not qualify, so you lose a deduction a rupee loan would have carried. The central interest subsidy schemes for scheduled-bank loans in India do not apply either. Confirm your own position with a tax advisor, because losing 80E quietly widens the real gap against a rupee loan.

One benefit genuinely sits on MPOWER’s side: building US credit. If you intend to stay and work in the US, a record of on-time repayment reported to US bureaus helps you later rent, get a US card, or borrow domestically. For a student returning to India, that benefit is largely irrelevant.

A worked example: MPOWER versus a rupee loan

Take a student admitted to a two-year STEM Master’s at an approved US university, with a USD 40,000 gap for the final stretch that no rupee lender will fund because the family has no collateral and a modest co-applicant income. MPOWER offers USD 40,000 at a fixed 13.5 percent over ten years, origination fee deducted up front.

Against this, imagine a rupee NBFC loan of the same ₹33.6 lakh equivalent at, say, 13 percent. The headline rates are close. But the rupee borrower repays in rupees with no forex exposure, can likely claim 80E on the interest, and pays no foreign-style origination fee. If our student returns to India and the rupee weakens over the decade, the dollar loan can cost several lakh more in rupee terms despite the similar headline rate, exactly as the two-scenario table shows. If instead she stays and earns in dollars, the forex risk cancels and MPOWER becomes a reasonable choice with the bonus of US credit.

So the verdict mirrors Prodigy’s. MPOWER wins on access, when no rupee lender will fund you, and on US-credit building if you stay. It loses on price for a borrower who returns to India and earns in rupees. The destination-level funding picture for the US is in the education loan for USA guide, and the all-in cost numbers are in the cost of studying in the USA post. The regulatory framework for the forex side of all this is set by the central bank, on the RBI website.

Who MPOWER Financing genuinely fits

To be fair, there is a real student for whom MPOWER is the right call. It fits when your university is on the approved list, you have no US cosigner and no Indian collateral so no rupee lender will fund the gap, you need to cover the final one or two years rather than the whole degree, and, ideally, you plan to stay and work in the US after graduation. For that student, MPOWER funds an otherwise unfundable gap, the fixed rate gives EMI certainty, the dollar income neutralises forex risk, and the US-credit reporting is a genuine bonus.

For that profile it is a clean, sensible tool, and I would not talk anyone out of it.

Who it does NOT fit

It does not fit the larger group who reach for it before exhausting cheaper routes.

- Anyone who can pledge collateral and access a PSU bank. The PSU rupee rate, plus 80E and possible subsidy, beats a 12 to 15 percent fixed dollar loan comfortably, with no forex risk.

- Anyone with a co-applicant strong enough for an unsecured NBFC rupee loan. The rupee route keeps you in your own currency and keeps your 80E deduction.

- Anyone who plans to return to India and earn in rupees. You will carry pure forex risk on a high fixed-rate dollar loan for years, with no income hedge and no US-credit benefit you can use.

- Students at schools that are not on the approved list. You are simply not eligible.

- Students who need the whole degree funded. MPOWER caps the amount and often funds only the final years, so it cannot be your sole source for a full multi-year program.

- Anyone whose budget only works at today’s exchange rate. The honest plan assumes a weaker rupee, and if that breaks the math, this loan is not for you.

The honest line is the same as for any foreign no-cosigner lender. MPOWER is a door for students who have no cheaper door and, ideally, a dollar income to repay with. If a rupee route is open and you are coming home, take the rupee route.

FAQ

Is MPOWER Financing good for Indian students?

It genuinely helps a narrow group: students at approved US or Canada schools with no cosigner and no collateral, so no rupee lender will fund them, especially those who plan to stay and earn in dollars. For that student the fixed-rate dollar loan plus US-credit building is sensible. For everyone with access to a PSU bank or an unsecured NBFC rupee loan, MPOWER is usually more expensive once its high fixed APR, the origination fee, the forex risk and the loss of the 80E deduction are all counted.

Does MPOWER need a cosigner or collateral?

No. That is its defining feature. MPOWER underwrites international and DACA students on academic profile and projected earnings rather than on a US guarantor or pledged security, so there is no cosigner and nothing to mortgage. This is why students with no US contacts and no Indian collateral turn to it. The trade-off is a high fixed APR, a coverage cap, an origination fee, and the forex risk that comes with a US dollar loan repaid from India.

What is the interest rate on an MPOWER loan?

MPOWER lends at a fixed rate, often in the 12 to 15 percent band, locked for the life of the loan. The fix gives certainty on the dollar EMI, but the level is high compared with a PSU rupee floating rate near 9.5 to 11 percent. There is also a one-time origination fee deducted up front, which raises the true effective cost above the headline fixed rate. Confirm the exact fixed APR and fee on your own sanction document, because terms vary and change.

Does MPOWER fund the whole degree?

Usually not. MPOWER typically funds the final one or two years of a program and caps the amount it will lend, so it often works as a top-up alongside other funding rather than as the sole source for a full multi-year degree. This matters for planning: if you expect MPOWER to cover an early year and it will not, you can face a funding gap. Confirm the cap and the exact funded years in writing before you rely on it.

Does MPOWER charge forex risk to the borrower?

Yes, in effect. The loan is denominated in US dollars and the rate is fixed in dollars, but if you repay from India you convert rupees to dollars at the prevailing rate on each EMI. A fixed rate locks the dollar cost, not the rupee cost, so a weakening rupee raises your real repayment even though the dollar terms never change. The forex risk sits entirely on you. If you earn in dollars in the US, the risk largely cancels; if you earn in rupees, it does not.

Can I claim Section 80E on an MPOWER loan?

Generally no. Section 80E allows deduction of education-loan interest, but it applies to loans from Indian banks and notified Indian financial institutions. A loan from a US lender like MPOWER usually does not qualify, so you lose a benefit a rupee loan from an Indian bank or notified NBFC would have given you. This widens the real cost gap against a rupee loan. Confirm your specific position with a qualified tax advisor before you decide.

Does MPOWER help build US credit?

Yes, and this is a genuine benefit if you intend to stay in the US. MPOWER reports repayment to US credit bureaus, so a record of on-time EMIs helps an international student build a US credit history, which makes it easier later to rent, get a US credit card, or borrow domestically. If you plan to return to India after your program, however, this benefit is largely irrelevant, and it should not by itself justify choosing a high fixed-rate dollar loan over a cheaper rupee one.

Is MPOWER cheaper than an Indian education loan?

Rarely, once everything is counted. The fixed APR is high, there is an origination fee, you usually lose the 80E deduction and any central interest subsidy, and a dollar loan repaid from India carries forex risk. For a borrower who comes home and earns in rupees, a weakening rupee can push the real cost several lakh above a comparable rupee loan. MPOWER wins on access when no rupee lender will fund you, and on US-credit building if you stay in the US, not on price.

Faz · The Honest Journey · 2026