An education loan without a co-applicant is almost impossible from an Indian bank, but it is genuinely available from USD lenders like Prodigy Finance and MPOWER Financing, which underwrite your admit and future earnings instead of a family signatory. The other real routes are pledging collateral held in your own name, or stacking a scholarship with personal savings. Each route has one hard qualifying condition you cannot work around.

I get a version of this email almost every week. A student writes to say they have an admit, sometimes a very good one, but no one who can sign as a co-applicant. The father has passed away. The parents are estranged. The family is overseas with no Indian income. Or the parents simply do not earn enough to clear the bank’s income checks. The question underneath every one of these emails is the same: can I get an education loan without a co-applicant at all?

The honest answer is harder than the question, so this post does not pretend otherwise. I will tell you exactly where the door is shut, where it is genuinely open, and how students with no eligible co-applicant actually fund a degree abroad.

If you are in this spot, you are not out of options. You are just out of the easy ones.

An education loan without a co-applicant is rare for an Indian-bank loan, where a co-applicant is effectively mandatory for an unsecured loan. The real routes are USD lenders like Prodigy Finance and MPOWER Financing, which lend on your admit and future earnings rather than a family signatory, a scholarship plus savings stack, or pledging collateral held in your own name. Each route has a hard qualifying condition.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

Other eligibility situations worth reading: the education loan rejection reasons india post, the education loan without ITR post, and the education loan for working professionals post.

Why Indian banks insist on a co-applicant

Start with the why, because it explains everything that follows. When an Indian bank or NBFC sanctions an education loan, the borrower is a student with no income and no credit history. The bank is lending on a future that has not happened yet. The co-applicant, almost always a parent or close relative, is the bank’s actual recovery path if that future does not pay off the way everyone hoped.

This is why the co-applicant’s income, credit score, and existing obligations get scrutinised harder than the student’s marksheet. The bank runs a FOIR check (fixed obligation to income ratio) on the co-applicant, not on you, and the co-applicant is the one the recovery team calls if EMIs stop. For the full picture of how this works, the co-applicant education loan guide walks through who qualifies and why.

So when a student asks for a loan with no co-applicant, they are asking the bank to lend with no recovery path. For a standard unsecured loan, the Indian banking system simply does not do this. The Indian Banks’ Association model education loan scheme, which most public sector banks follow, is built around a co-applicant. You can read the framework on the Indian Banks’ Association site, and the broader regulatory backdrop on the Reserve Bank of India site. Neither leaves much room for a no-co-applicant unsecured loan.

That is the wall. Now let us find the gates in it.

Faz's ruleNo co-applicant and no collateral means no Indian-bank loan. Stop knocking on that door and walk to a different one.

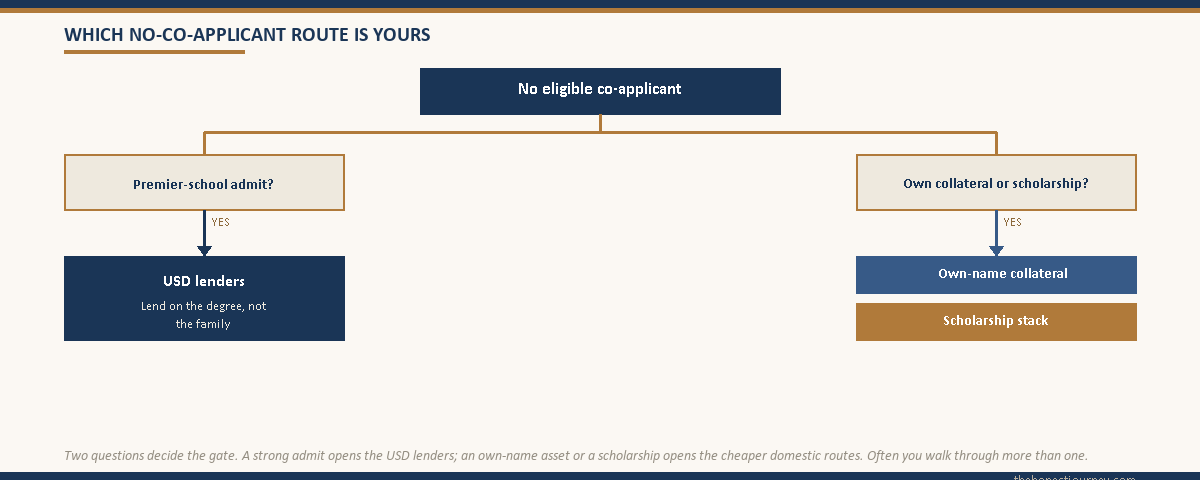

Indian banks lend against a recovery path, and for an unsecured loan that path is the co-applicant. If you have neither a co-applicant nor collateral, the answer from every public sector bank and NBFC will be no. The good news is that two real alternatives exist, and they do not need a family signatory at all.

Route one: USD lenders that do not need a co-applicant

This is the route that genuinely works for the no-co-applicant student, and it is the one most families have never heard of. A small set of international lenders fund Indian students based on the student’s admit and projected post-graduation earnings, not on a co-applicant’s income. The two names you will run into are Prodigy Finance and MPOWER Financing.

Their model is different by design. Instead of asking who will pay if you cannot, they ask how much you are likely to earn after the degree. They underwrite the program and the school. A student admitted to a top-ranked MBA, a strong STEM master’s, or a recognised graduate program at a school on their eligible list can borrow without a co-applicant, without collateral, and without an Indian credit history.

The catch is in that last paragraph: the program and the school. These lenders are selective about which degrees they fund. They concentrate on master’s and MBA programs at well-ranked universities in the US, UK, Canada, and a few other markets, where the earnings data supports the loan. If your admit is to a lesser-known school or a field with weak salary outcomes, you may not qualify, because the entire model rests on your future income clearing the debt.

| Factor | Prodigy Finance | MPOWER Financing |

|---|---|---|

| Co-applicant required | No | No |

| Collateral required | No | No |

| Underwriting basis | School, program, future earnings | School, program, future earnings |

| Typical focus | Postgrad and MBA at ranked schools | Postgrad and select undergrad at approved schools |

| Loan currency | USD | USD |

| Main cost to watch | Higher interest, USD repayment, FX risk | Higher interest, USD repayment, FX risk |

Two costs are not on the brochure. First, the interest is usually higher than a collateral-backed Indian loan. You are paying a premium for the absence of a co-applicant and collateral, which is fair, because the lender is carrying more risk. Second, the loan is in dollars and you repay in dollars. If you earn in rupees after returning to India, every repayment is exposed to the rupee-dollar rate, and the rupee has historically weakened against the dollar over time. A loan that looked affordable at sanction can grow heavier in rupee terms across a ten-year repayment.

So this route is real, but it is conditional. It opens for the strong-admit student and stays shut for the marginal one. If your admit is to a school these lenders cover, this is very likely your cleanest path to a degree abroad with no co-applicant. To check whether your target universities are the kind that attract loan funding at all, the approved foreign universities for education loans guide is the place to start.

Faz's ruleUSD lenders bet on your degree, not your family. That only works if the degree is strong.

Prodigy and MPOWER replace the co-applicant with your future salary as the security. The trade is a higher rate and dollar-denominated repayment, with real FX risk if you earn in rupees. For a premier-school admit it is often the only no-co-applicant route that actually funds. For a weak admit it will not open.

Route two: pledge collateral in your own name

Here is a route people miss because they assume a co-applicant and collateral are the same thing. They are not. A co-applicant is a person who promises to repay. Collateral is an asset that secures the loan regardless of who promises anything. If you own an asset, you can sometimes use it to secure a loan even without a strong co-applicant.

This matters most for two groups. NRI students or returning students who have built up their own savings, fixed deposits, or property, and students who have inherited an asset such as a flat, a plot, or a substantial FD held in their own name. If a property or a fixed deposit in your name covers the loan amount, the bank’s recovery problem is largely solved, because the asset is the recovery path. The need for a strong income-earning co-applicant drops sharply.

Be clear about the limits. Most Indian banks still want a co-applicant on the paperwork even for a secured loan, but with full collateral the income bar for that co-applicant falls dramatically. A retired parent with a pension, or a relative with modest income, can sometimes serve as co-applicant when the loan is fully secured, because the asset, not the person, is now the recovery path. So if your problem is not the absence of any relative but the absence of one who earns enough, collateral in your own name can be the lever that gets the loan through.

If you do have an asset to pledge, a secured loan from a public sector bank is also far cheaper than a USD lender, often by several percentage points, which over a full repayment tenure is a large sum. The trade-off between secured and unsecured loans, and what happens when you have neither collateral nor a co-applicant, is covered in detail in the education loan without collateral guide.

Route three: the scholarship plus savings stack

The third route is not a loan at all, and for students with no co-applicant and no collateral, it is sometimes the only one left. It is the stack: a scholarship that covers a large chunk of tuition, plus your own savings, plus a smaller loan or none at all.

This sounds like a consolation prize. It is not. A student with a strong enough profile to win a tuition waiver or a partial merit scholarship has converted the loan problem into a much smaller one. If a scholarship covers half your tuition, the amount you actually need to borrow may fall low enough that a USD lender approves it comfortably, or that your own savings plus a modest secured loan cover the gap entirely.

The honest part is that this route demands lead time and a strong application. Scholarships are competitive, deadlines run months ahead of intake, and you cannot assemble this stack in the final weeks before a term starts. If you are reading this early, before you have applied, treat the scholarship search as seriously as the loan search, because for a no-co-applicant student the scholarship is not extra money. It is the thing that makes the rest of the funding possible.

For a full map of how scholarships, savings, loans, and other sources combine into a realistic funding plan, the how to fund study abroad guide lays out the complete picture and where each source realistically fits.

Special cases: orphans, estranged families, and NRIs

The students who write to me usually fall into one of three situations, so let me speak to each plainly.

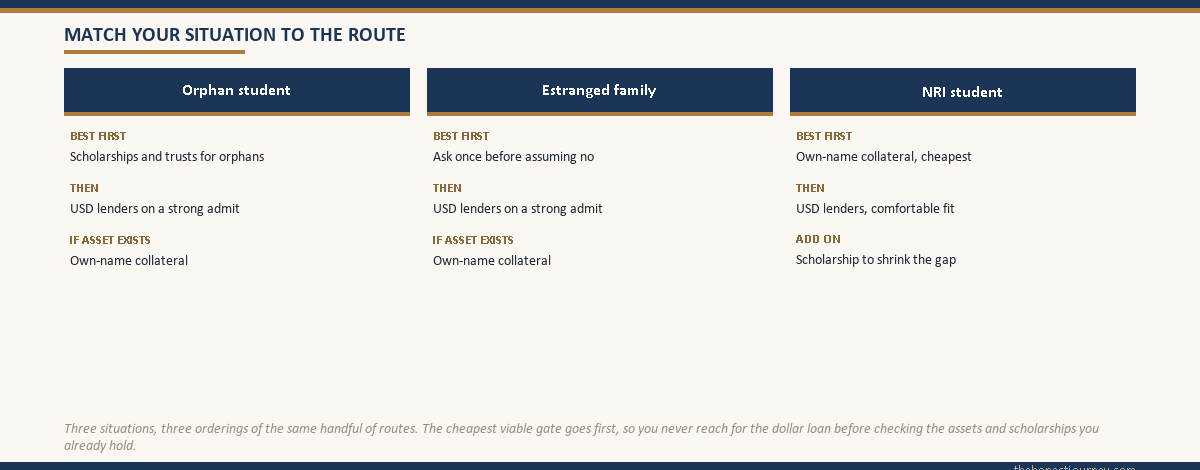

Orphan students or students who have lost both parents. This is the hardest case for the Indian banking system, because the standard co-applicant simply does not exist. A legal guardian can sometimes act as co-applicant, but only if that guardian has the income and willingness to take on the obligation. If no such guardian exists, the realistic paths are the USD lenders for a strong admit, or collateral in the student’s own name if any asset was inherited. There are also a small number of trusts and foundation scholarships aimed specifically at orphaned students, and for this group those are worth pursuing aggressively, because a scholarship removes the need for a loan entirely.

Students with estranged or non-cooperative families. If a parent exists but will not sign, the bank treats this the same as no co-applicant, because it cannot compel anyone to guarantee a loan. The routes here are identical to the orphan case: USD lenders, own-name collateral, or a scholarship stack. The one thing I will say gently is that some students assume a parent will refuse before they have actually asked. If there is any chance of a conversation, have it, because a reluctant co-applicant is still a co-applicant, and the Indian-bank route is far cheaper than the dollar route.

NRI students or students with overseas parents. If your parents live abroad and have no Indian income, most Indian banks will not accept them as co-applicants for a standard scheme, because they cannot assess foreign income easily. But NRI families often have an advantage the others do not: savings or property, sometimes held in the student’s own name. This makes the collateral route genuinely viable. NRI students are also frequently strong candidates for USD lenders, since those lenders are comfortable underwriting students with international backgrounds and dollar earning potential.

Faz's ruleMatch the route to your real situation, not to the loan you wish existed.

An orphan with a top admit should go straight to the USD lenders and the scholarship route. An NRI student with family savings should look at own-name collateral first, because it is cheaper. A student with an estranged parent should at least ask before assuming no, since an Indian-bank loan beats a dollar loan on cost every time.

The honest closing take

The phrase education loan without a co-applicant sets up an expectation I cannot honestly meet: that an Indian bank will hand a student an unsecured loan on the strength of an admit alone. It will not, and any agent who tells you otherwise is selling you something. The co-applicant is the recovery path the entire unsecured-lending model rests on, not a formality the banks could waive if they felt like it.

But the question behind the phrase, how do I fund a degree abroad when I have no eligible co-applicant, has real answers. If your admit is strong, the USD lenders will lend on your future rather than your family. If you hold an asset in your own name, collateral can carry the loan where a co-applicant cannot. And if neither applies, a scholarship that shrinks the borrowing need can turn an impossible loan into a manageable one. Often the answer is a combination of all three.

What does not work is waiting for a bank to make an exception it is not built to make. The students who get abroad in this situation accept the wall early and walk to a different gate, rather than spending months arguing the wall down. Pick the route that fits your situation, start on it early, and treat the scholarship search as part of the funding plan rather than a nice-to-have.

FAQ

Can I get an education loan without a co-applicant?

For a standard unsecured loan from an Indian bank or NBFC, no. A co-applicant is effectively mandatory because the student has no income and the co-applicant is the bank’s recovery path. The real no-co-applicant routes are USD lenders such as Prodigy Finance and MPOWER Financing, which lend on your admit and future earnings, or pledging collateral held in your own name. A scholarship-plus-savings stack can also reduce or remove the need for a loan entirely.

Which lenders do not need a co-applicant?

The main lenders that fund Indian students without a co-applicant are international USD lenders, primarily Prodigy Finance and MPOWER Financing. They underwrite based on your school, program, and projected post-graduation earnings rather than a family signatory or collateral. The trade-off is a higher interest rate than a collateral-backed Indian loan and repayment in dollars, which carries currency risk if you later earn in rupees. They also fund only certain schools and programs.

Can an orphan get an education loan?

It is harder, because the standard parental co-applicant does not exist, but it is possible. A legal guardian with sufficient income can sometimes act as co-applicant. Failing that, the realistic routes are USD lenders for a strong admit, or collateral in the student’s own name if any asset was inherited. There are also trusts and foundation scholarships aimed specifically at orphaned students, and these are worth pursuing first, since a scholarship can remove the need for a loan entirely.

Do USD lenders like Prodigy and MPOWER need a co-applicant?

No. That is the core of their model. Instead of a co-applicant or collateral, they assess your school, your program, and your likely earnings after graduation. This makes them the cleanest route for students with no eligible co-applicant, but only if your admit is to a school and program they cover. They concentrate on well-ranked master’s and MBA programs where the salary data supports the loan, so a weaker admit may not qualify.

Can I use my own collateral instead of a co-applicant?

Often yes, and it is an underused route. Collateral and a co-applicant are different things: a co-applicant promises to repay, while collateral is an asset that secures the loan regardless. If you hold a property or fixed deposit in your own name that covers the loan, the bank’s recovery problem is largely solved and the income requirement on any co-applicant drops sharply. A retired parent or modest-income relative can then sometimes serve as the formal co-applicant.

Is a co-applicant mandatory for abroad education loans?

For loans from Indian banks and NBFCs, effectively yes, especially for unsecured loans, because the model follows the Indian Banks’ Association framework built around a co-applicant. It is not mandatory for the international USD lenders, which do not use co-applicants at all. So the honest answer is that it depends on the lender: mandatory for the Indian-bank route, not required for the Prodigy and MPOWER route.

What is the difference between a co-applicant and a guarantor?

A co-applicant is a joint borrower on the loan from day one, equally responsible for repayment, and usually a parent or close relative whose income is assessed during sanction. A guarantor is a fallback who becomes liable only if the borrower defaults. Most Indian education loans require a co-applicant rather than a guarantor for abroad studies. For the full breakdown of who can be a co-applicant and what is checked, see the dedicated co-applicant guide.

Will a scholarship help if I have no co-applicant?

Significantly. A scholarship does not replace a co-applicant directly, but it shrinks the amount you need to borrow. If a scholarship covers a large share of tuition, the remaining gap may be small enough for a USD lender to approve comfortably, or for your own savings plus a modest secured loan to cover. For a student with no co-applicant and no collateral, a strong scholarship is sometimes the single thing that makes the entire funding plan work, so treat the search seriously and start early.

Faz · The Honest Journey · 2026