Every major Indian lender keeps its own list of approved foreign universities for education loans, and the list decides one thing: how much they fund without collateral. SBI funds up to ₹1.5 crore unsecured at its 400-odd premier institutes, HDFC Credila goes up to ₹50 lakh at its A-list, and Avanse caps non-listed schools at ₹20 lakh with collateral. The list, not the country, sets your ceiling.

The first time I saw the phrase “list of approved foreign universities for education loan,” I assumed it was a single national list maintained by some regulator. It is not. Every major Indian lender keeps its own list, calls it something different, and uses it to decide one thing: how much they will lend you without collateral.

This post pulls those lists into one place, shows the country-by-country pattern, explains what “premier” actually unlocks in rupee terms, and tells you honestly what happens if your university is not on any of them. The list of approved foreign universities for education loan eligibility is not one document. It is at least four, one per major bank.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

What the “approved list” actually does for you

Every bank that funds abroad studies maintains a tiered classification of foreign universities. The names vary. SBI calls its top tier the Premier Institution List under Global Ed-Vantage. Bank of Baroda calls it the Baroda Scholar list with A, B, and C categories. Bank of India runs Star Vidya with a Premier Educational Institutions schedule. PNB runs Pratibha and Udaan with similar grading. The framework follows the IBA model education loan scheme.

The list does one thing: it changes your loan terms. A premier-list university unlocks a higher unsecured limit, a lower rate, faster processing, and sometimes a longer grace period. A non-list university requires collateral, attracts a higher rate, and caps unsecured borrowing at a far lower number.

Here is the structural pattern before we get into specific universities.

| Bank scheme | List name | Unsecured limit (list) | Unsecured limit (non-list) |

|---|---|---|---|

| SBI Global Ed-Vantage | Premier Institution List (List AA, A, B) | Up to ₹50 lakh | ₹7.5 lakh (collateral above) |

| Bank of Baroda Baroda Scholar | Premier A / B / C list | Up to ₹80 lakh (Category A) | ₹7.5 lakh (collateral above) |

| Bank of India Star Vidya | Premier Educational Institutions schedule | Up to ₹40 lakh | ₹7.5 lakh (collateral above) |

| PNB Pratibha / Udaan | PNB approved institution list | Up to ₹40 lakh | ₹7.5 lakh (collateral above) |

The pattern is identical across all four. Below ₹7.5 lakh, no collateral. Above ₹7.5 lakh, the lender wants either (a) your university on its premier list, in which case the higher unsecured limit unlocks, or (b) tangible collateral worth roughly 100 to 125 percent of the loan amount. There is no third path inside public sector banks.

Faz's ruleThe approved list is not a quality stamp. It is a credit policy shortcut for the bank.

The bank is not certifying that your university is good. It is saying its risk team has decided your university’s graduates earn enough to repay an unsecured loan. That is why the Ivy League and Oxbridge are on every list, and why some excellent regional universities are not.

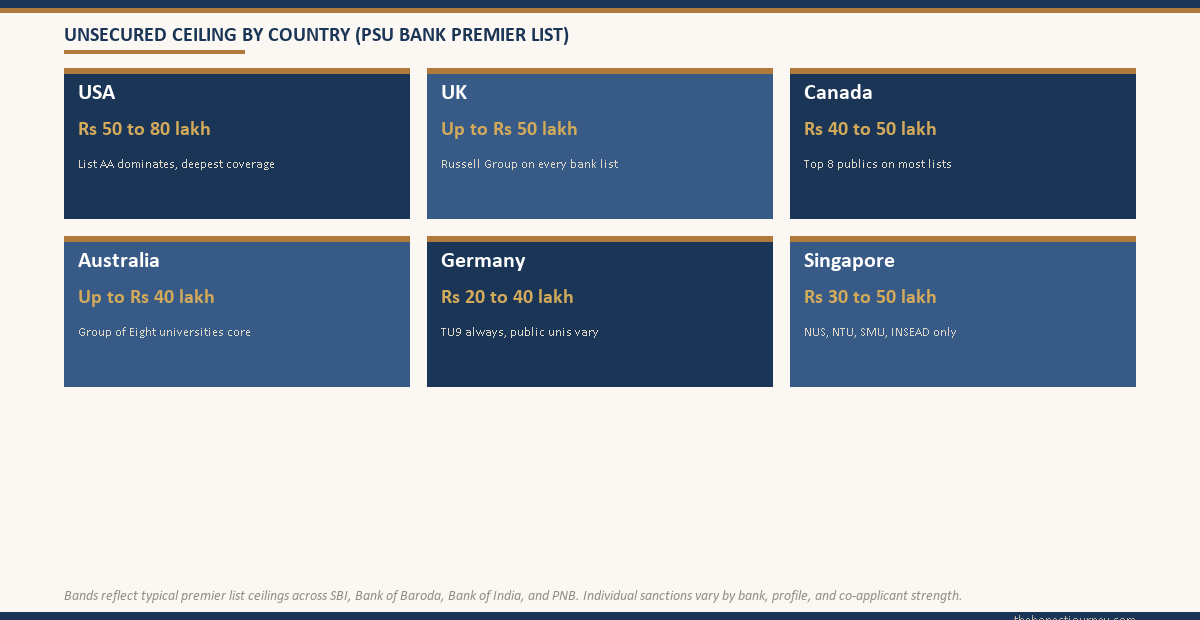

USA: the country with the deepest list

The US dominates every bank’s premier list. SBI’s Global Ed-Vantage List AA alone runs to roughly 200 US universities, and the broader Premier list adds another 400. Here is a representative cross-section that appears on virtually every major Indian bank’s premier list.

| University | On SBI Premier? | On BoB Cat A? | Typical unsecured ceiling |

|---|---|---|---|

| Harvard University | Yes (List AA) | Yes | ₹50 lakh to 80 lakh |

| Stanford University | Yes (List AA) | Yes | ₹50 lakh to 80 lakh |

| MIT | Yes (List AA) | Yes | ₹50 lakh to 80 lakh |

| Carnegie Mellon University | Yes | Yes | ₹50 lakh to 80 lakh |

| Columbia University | Yes (List AA) | Yes | ₹50 lakh to 80 lakh |

| University of California, Berkeley | Yes | Yes | ₹50 lakh to 80 lakh |

| Northeastern University | Yes | Yes | ₹50 lakh |

| University of Texas, Dallas | Yes | Yes (Cat B) | ₹40 lakh to 50 lakh |

Across the four major schemes, the US list overlap is roughly 85 to 90 percent for the top 100. The divergence happens lower down. A second-tier state university on SBI’s Premier B list might be off Bank of India’s Star Vidya schedule entirely. That is the level at which it pays to pull two or three bank lists.

UK: smaller list, cleaner tiering

The UK list is shorter and more predictable. Russell Group universities are almost universally on every Indian bank’s premier list. Oxbridge plus LSE plus Imperial plus UCL sits at the top tier. Then a band of Russell Group institutions, then a long tail of post-92 universities that may or may not appear.

| University | SBI tier | Notes |

|---|---|---|

| University of Oxford | List AA | Top tier on all 4 banks |

| University of Cambridge | List AA | Top tier on all 4 banks |

| Imperial College London | List AA | Top tier on all 4 banks |

| London School of Economics | List AA | Top tier on all 4 banks |

| University College London | List AA | Top tier on all 4 banks |

| King’s College London | Premier A | On all 4, slightly lower limit |

| University of Edinburgh | Premier A | On all 4 banks |

| University of Manchester | Premier B | On SBI and BoB, check BOI/PNB |

If you are looking at a UK university outside the Russell Group, do not assume it is on any list. Verify before you build a financial plan around an unsecured ₹30 lakh approval.

Canada, Australia, Germany, Singapore

The non-US, non-UK lists are where the lists get thinner and the gaps between banks get wider. Here is a representative slice. This is not exhaustive, just the universities that appear on multiple banks’ premier schedules.

| Country | Universities on most premier lists |

|---|---|

| Canada | University of Toronto, McGill University, University of British Columbia, University of Waterloo, University of Alberta, McMaster University, Western University, Queen’s University |

| Australia | University of Melbourne, Australian National University, University of Sydney, University of New South Wales, University of Queensland, Monash University, University of Western Australia |

| Germany | Technical University of Munich, RWTH Aachen, Heidelberg University, LMU Munich, Humboldt University Berlin, Karlsruhe Institute of Technology |

| Singapore | National University of Singapore, Nanyang Technological University, Singapore Management University, INSEAD (Asia campus) |

Germany is the most uneven of the four. Some banks list only the TU9 group. Others include Heidelberg, LMU, and Humboldt. Tuition-free public universities still qualify for a loan because funding covers living expenses, visa fees, and travel, which routinely add up to ₹18 lakh to 22 lakh over a two-year master’s.

Faz's ruleTwo lenders can give you very different answers for the same university. Apply to two before you sign with one.

I have seen the same student get ₹30 lakh unsecured from one PSU bank and ₹7.5 lakh plus collateral from another, for the same University of Manchester offer. The bank’s internal list is the variable, not your profile.

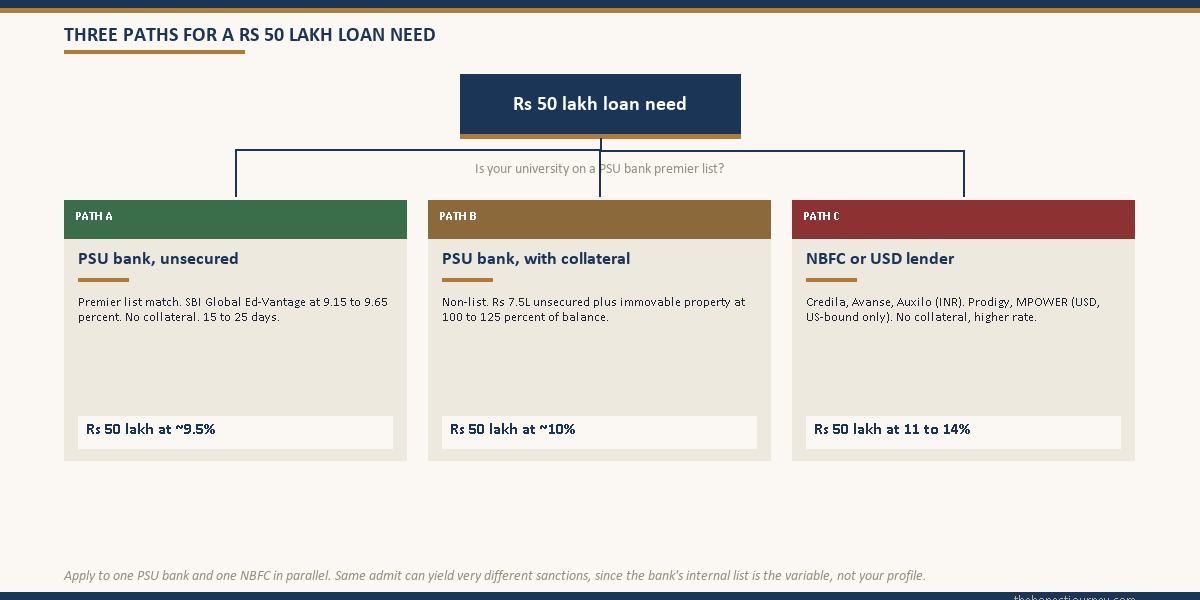

What “premier” actually unlocks: a worked example

Let us put numbers on this. You have an admit at Northeastern University for an MS in Computer Science. Total cost of attendance is ₹65 lakh over two years. Your family can arrange ₹15 lakh upfront. You need a ₹50 lakh loan.

Northeastern is on SBI’s Premier list. Under Global Ed-Vantage, SBI can sanction up to ₹50 lakh unsecured at roughly 9.65 percent, no collateral, with the standard parent co-applicant. Processing takes 15 to 25 working days from a complete file.

Same student, same ₹50 lakh need, with an admit at a non-premier US university. SBI caps the unsecured portion at ₹7.5 lakh. The remaining ₹42.5 lakh requires collateral, typically immovable property with a market value of at least ₹50 lakh to 55 lakh after the legal title check. Processing time stretches to 30 to 45 days.

Third path. No collateral, university not on a premier list. PSU bank options end here. You move to NBFCs or USD lenders.

What happens when your university is not on any list

Most students panic at this point. Do not. Off-list does not mean unfundable. It means the funding path changes, and the cost goes up, and you need to know what you are signing for.

NBFC route. HDFC Credila, Avanse Financial Services, and Auxilo Finserve are the three largest education-loan NBFCs in India. They do not use a strict premier list in the way PSU banks do. They underwrite university by university, factoring in employability data and historical recovery from that institution. They will fund universities that SBI will not. The tradeoff is rate: Credila and Avanse typically price between 10.75 and 13.5 percent depending on profile, against 9.5 to 10.5 percent at SBI for a premier-list student.

NBFCs are also faster (10 to 15 days) and more flexible on co-applicant documentation (GST returns or CA-certified statements rather than ITRs). For more on that flexibility, see the education loan for abroad studies without collateral post.

USD lender route (US-specific). If your admit is in the US and you cannot get a rupee loan that covers the gap, two lenders fund Indian students directly in USD: Prodigy Finance and MPOWER Financing. Both lend without an Indian co-signer and without collateral, basing approval on the admit, the university’s employment outcomes, and projected post-graduation income.

| Lender | Currency | Co-signer | Typical rate | Best for |

|---|---|---|---|---|

| Prodigy Finance | USD | None required | SOFR + 5 to 8 percent | STEM masters at top US schools |

| MPOWER Financing | USD | None required | Fixed 12 to 14 percent | Undergrad and masters at US schools |

| HDFC Credila (INR) | INR | Yes, parent | 10.75 to 12.5 percent | Non-list universities in any country |

| Avanse / Auxilo (INR) | INR | Yes, parent | 11 to 13.5 percent | Non-list universities in any country |

USD lenders remove the collateral requirement and the Indian co-applicant requirement. They cost more, and on a depreciating rupee the effective INR cost of a USD loan is higher than the headline rate suggests. But for a student with strong admits, no collateral, and a co-applicant who does not meet income criteria at Indian banks, this path exists.

Faz's ruleOff-list does not mean unfundable. It means the route shifts from PSU bank to NBFC, and the cost goes up by 1.5 to 3 percent per year.

On a ₹40 lakh loan over 10 years, a 2 percent rate difference is roughly ₹6 lakh in extra interest. Worth knowing before you assume the NBFC offer is your only option. Always apply to one PSU bank too, even if you expect a rejection, just to see the actual answer.

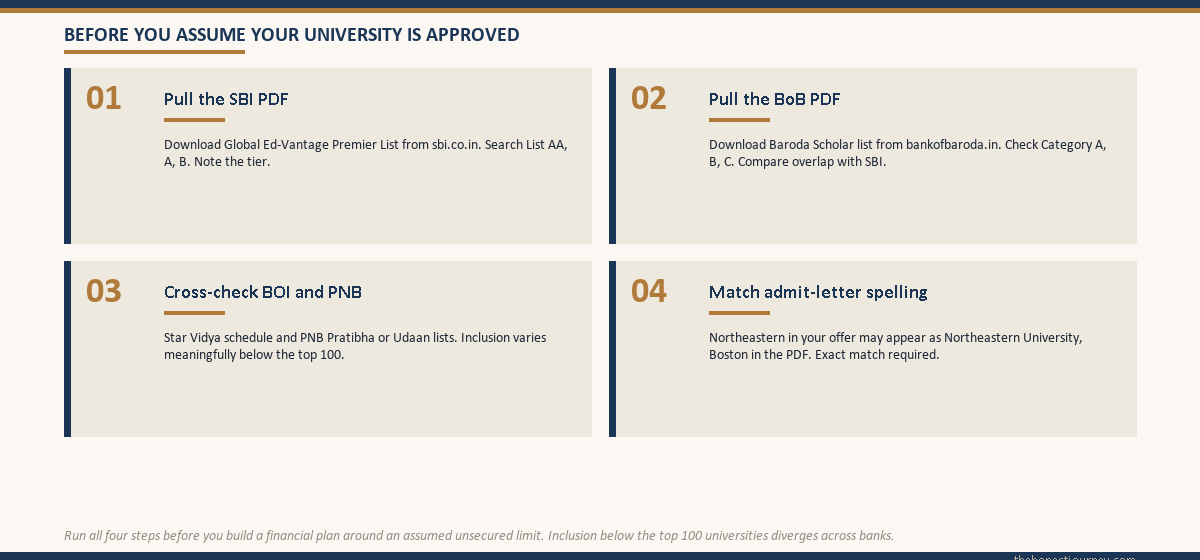

How to actually check if your university is on a list

Three steps, in order. None of them involve an agent or a consultancy.

Step 1. Go to the official bank page and download the latest PDF. SBI publishes the Global Ed-Vantage Premier List on sbi.co.in. Bank of Baroda publishes the Baroda Scholar list on bankofbaroda.in. These PDFs update periodically. The version on a consultancy’s blog may be six months stale. Pull the original.

Step 2. Search the PDF for your university name exactly as it appears in your admit letter. “Northeastern” in your admit might appear as “Northeastern University, Boston” in the PDF. Spelling matters.

Step 3. If your university appears, note the tier (AA, A, B, or C). If it does not appear, cross-check Bank of Baroda’s Category A/B/C list and Bank of India’s Star Vidya schedule. Inclusion varies meaningfully across banks.

For the documentation checklist, see documents required for an education loan. If you are still in the country selection phase, the best country to study abroad for Indian students guide covers how the loan landscape differs by country.

Rates and how the list affects them

A premier-list classification does not just affect loan limit. It often affects rate too. Public sector banks under the IBA model education loan scheme price differently for premier and non-premier institutions, and the gap is usually 25 to 75 basis points.

| Lender + scheme | Rate for premier list student | Rate for non-list student |

|---|---|---|

| SBI Global Ed-Vantage | 9.15 to 9.65 percent | 9.65 to 10.40 percent (with collateral) |

| Bank of Baroda Baroda Scholar | 9.20 to 9.85 percent (Cat A) | 9.85 to 10.50 percent (Cat C / non-list) |

| HDFC Credila | 10.75 to 11.75 percent | 11.50 to 13.50 percent |

| Avanse / Auxilo | 11.00 to 12.50 percent | 12.00 to 13.75 percent |

For a deeper rate-by-rate comparison across lenders, see the education loan interest rate comparison. The point worth carrying from this post: the bank’s list is not just a yes/no gate. It is also a price tier inside the yes.

The honest closing take

The “list of approved foreign universities for education loan” question is really three nested questions stacked together.

First, is my university on a PSU bank’s premier list? If yes, take it. SBI Global Ed-Vantage at sub-10 percent on ₹50 lakh unsecured is the best available financing for an Indian student going abroad.

Second, if it is not on a premier list but my family has collateral, am I willing to pledge it? PSU banks will still fund you at near-premier rates, but the family home is on the loan agreement. That is a real decision, not a paperwork formality.

Third, if neither applies, which NBFC or USD lender fits? Credila, Avanse, Auxilo, Prodigy, and MPOWER each fit a different shape of student. The off-list student is not unfunded. The off-list student is on a different curve.

The list is a filter, not a verdict on your future. The same Northeastern admit on a premier list and on no list is the same admit. The only thing that changes is how expensive the next two years are going to be.

FAQ

Which foreign universities are approved for an Indian education loan?

There is no single national list. Each major Indian bank maintains its own. SBI’s Global Ed-Vantage Premier List covers roughly 600 universities globally across Lists AA, A, and B. Bank of Baroda’s Baroda Scholar list runs to a similar size in Categories A, B, and C. The top 200 universities globally are on virtually every bank’s premier list. Below that, inclusion varies, so check two or three lists before assuming a university is unfundable.

What is the SBI premier institution list?

SBI’s Global Ed-Vantage Premier Institution List is an internal tiering of foreign universities (AA, A, B) that sets the unsecured loan limit and rate for that institution. List AA includes top US, UK, and Canadian universities like Harvard, Oxford, and University of Toronto. Premier list students borrow up to ₹50 lakh without collateral. Non-premier students are capped at ₹7.5 lakh unsecured. The official PDF lives on sbi.co.in.

Does my university need to be on an approved list to get a loan?

No. Approval just changes the terms. If your university is on a premier list, you can borrow larger amounts unsecured at a lower rate. If it is not, you can still borrow, but either (a) you pledge collateral worth roughly the loan amount, or (b) you use an NBFC like HDFC Credila or Avanse, which underwrites university by university rather than using a strict list. For US-bound students, USD lenders like Prodigy and MPOWER also fund off-list universities directly in USD without an Indian co-applicant.

How does the Bank of Baroda Scholar list compare to the SBI premier list?

BoB’s Baroda Scholar uses Categories A, B, and C. Category A unlocks up to ₹80 lakh unsecured, higher than SBI’s ₹50 lakh ceiling. The overlap with SBI’s List AA is roughly 90 percent at the top. Rate range is similar (9.20 to 9.85 percent for Category A). For a high-value loan in the ₹50 lakh to 80 lakh range, BoB is worth a parallel application.

What if my university is not on any approved list?

You have three options. One, pledge collateral and take a PSU bank loan at near-premier rates. Two, go to an NBFC (HDFC Credila, Avanse, Auxilo), which will price you 1.5 to 3 percent higher but does not require collateral or a strict list match. Three, for US-bound students specifically, use a USD lender (Prodigy Finance or MPOWER Financing), which lends without an Indian co-applicant or collateral, based on the admit and projected post-graduation income. Off-list does not mean unfunded.

Can I get an SBI Global Ed-Vantage loan for any foreign university?

Technically yes, but terms change sharply off the premier list. For a premier university, SBI offers up to ₹50 lakh unsecured at roughly 9.15 to 9.65 percent. For a non-premier university, the unsecured cap drops to ₹7.5 lakh, and any amount above that needs immovable property as collateral valued at 100 to 125 percent of the loan. SBI funds 35 plus countries but the premier list is heaviest in the US, UK, Canada, Australia, and Singapore.

How often are the approved lists updated?

PSU banks revise their premier lists once or twice a year, usually before the January and June admission cycles. Universities get added when alumni employment outcomes improve, and occasionally removed when defaults rise. Always download the latest PDF from the bank’s official site at the time you apply. A list on a consultancy’s blog six months ago may not match current policy.

Is there a single Indian government list of approved foreign universities for education loans?

No. The Indian Banks’ Association publishes a model education loan scheme that all member banks broadly follow, but the specific approved institution lists are bank-specific, not government-issued. The Ministry of Education and UGC maintain lists of foreign qualifications recognised in India for employment or further study, but these are not loan-eligibility lists. For loan purposes, only the individual bank’s published list matters.

Faz · The Honest Journey · 2026