Prodigy Finance is a UK-based lender that funds admitted students at select top global Master’s with no cosigner and no collateral, but it lends in dollars, pounds or euros, so you carry the forex risk on repayment. The effective APR usually runs around 11 to 13 percent plus an origination fee. For families with collateral or a strong co-applicant, a rupee loan costs less.

A friend from my undergraduate batch got into a one-year MBA at a well-ranked European business school. His family had no property to pledge and his father’s income would not clear an NBFC’s unsecured underwriting for the full ticket. He had run out of rupee options when someone pointed him to Prodigy Finance. The loan came through on the strength of his admit and his expected post-MBA salary, with no cosigner and nothing pledged. He was relieved, and rightly so. But two years later he was sending dollar EMIs back from a euro salary, watching the rupee weaken, and quietly recalculating what the loan had actually cost him.

This post is the honest picture of what Prodigy Finance is, who it genuinely helps, and the real catch that nobody selling it to you will spell out. It is not an endorsement. It is the math and the risk laid flat.

To compare this NBFC against the alternatives: the PSU bank vs NBFC education loan post, the avanse education loan post, and the MPOWER financing education loan post.

What Prodigy Finance actually is

Prodigy Finance is a private lender headquartered in the United Kingdom. It does not work like an Indian bank or an Indian NBFC. The core difference, and the reason it exists at all, is its underwriting model. A PSU bank wants collateral above ₹7.5 lakh. An NBFC like HDFC Credila or Avanse wants a strong co-applicant whose income carries the loan. Prodigy wants neither.

Instead, it underwrites on two things: the school you got into and your projected future earnings from that specific program. It lends to admitted students at a defined list of high-ranked global Master’s programs, weighted heavily toward MBA, finance, engineering and other STEM fields where graduate salaries are predictable and high. If your program is on the list and you have the admit, your nationality, your family’s net worth and your lack of a cosigner do not block the loan. That is the genuine, real advantage, and for a narrow set of students it is the only door that opens.

The loans are denominated in US dollars, pounds sterling or euros depending on where you study. This single fact, the currency of the loan, is the hinge the whole honest assessment turns on, and I will come back to it.

How Prodigy underwrites: school plus earnings, not collateral

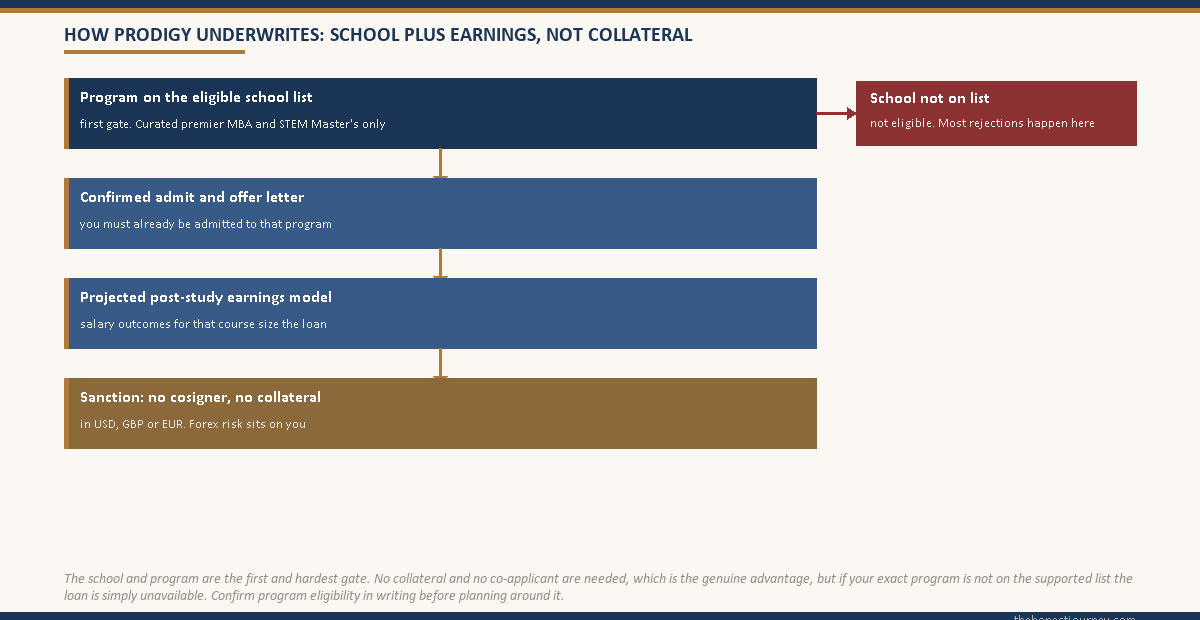

It helps to see the underwriting as a flow, because it explains both why some students sail through and why others are simply not eligible no matter how genuine their need.

The first gate is the school and program. If your program is not on Prodigy’s supported list, the conversation ends there. This is the most common reason Indian students are turned away. The list skews toward elite MBA programs and top-ranked STEM and finance Master’s at well-known universities in the US, UK, Europe and a handful of other markets. A mid-ranked Master’s, almost any undergraduate degree, and most non-listed programs do not qualify.

The second gate is the admit itself, confirmed by the offer letter. The third is the projected earnings model for that program, which Prodigy builds from salary outcomes data for graduates of that course. A program with strong, well-documented salary outcomes supports a larger loan. The loan amount is capped against the cost of attendance and against what the earnings model says you can repay.

What is striking is what does not feature: no property pledge, no fixed deposit lien, no parent co-applicant signing as guarantor. For a student with a premier admit and no collateral and no strong co-applicant, this is the entire value proposition. The honest unsecured rupee alternative, where it exists, is laid out in the education loan for abroad studies without collateral guide, and the no-co-applicant route is in the education loan without a co-applicant post.

Faz's ruleCheck whether your exact program is on the eligible list before you build any plan around Prodigy. The school list is the first and hardest gate, and most rejections happen right there.

People assume that a no-cosigner lender will fund anyone with a good admit. It will not. If your Master’s is not on the supported list, no amount of academic record changes the answer. Confirm eligibility for your specific program in writing before you treat this as a funding source.

The real catch: you repay in foreign currency

Here is the part that gets buried. A rupee loan from SBI or Avanse is denominated in rupees. You earn, you repay, in the same currency, and the exchange rate is irrelevant to your EMI. A Prodigy loan is denominated in dollars, pounds or euros. Your EMI is a fixed foreign-currency amount. If you return to India and earn in rupees, every single repayment first has to be converted from rupees into that foreign currency at whatever the exchange rate is on the day. The forex risk sits entirely on you.

This matters because the rupee has weakened against the dollar over almost every long stretch of the last two decades. If you borrow when the dollar is ₹84 and you repay over the following years while it drifts to ₹90 or beyond, your rupee cost of every dollar EMI rises even though the dollar loan terms never changed. You signed up for a dollar number, and the rupee cost of that number keeps climbing.

The honest way to see this is to run the same loan under two exchange-rate scenarios.

| Item | Scenario A: rupee stable | Scenario B: rupee weakens |

|---|---|---|

| Loan amount | USD 50,000 | USD 50,000 |

| Indicative APR | 12 percent | 12 percent |

| Tenure | 7 years | 7 years |

| Monthly EMI (USD) | ~USD 883 | ~USD 883 |

| Exchange rate at repayment | ₹84 per USD | ₹92 per USD |

| Monthly EMI in rupees | ~₹74,170 | ~₹81,230 |

| Total repaid (USD) | ~USD 74,170 | ~USD 74,170 |

| Total repaid in rupees | ~₹62.3 lakh | ~₹68.2 lakh |

The dollar terms are identical in both columns. The dollar EMI never changes. Yet the rupee cost of the loan rises by roughly ₹5.9 lakh purely because the rupee weakened by eight rupees over the repayment years. Nobody can predict the exact rate. The honest point is that the entire spread of that uncertainty is your problem, not the lender’s. If you will earn in the same currency you borrowed, in dollars in the US for instance, this risk largely cancels out. If you plan to come home and earn in rupees, it does not, and you must budget for the bad scenario, not the calm one.

Faz's ruleBudget the loan at a rupee that is weaker than today's, not at today's rate. The forex risk on a foreign-currency loan is yours alone, and the rupee has trended weaker, not stronger.

Run your repayment math at an exchange rate several rupees worse than the day you borrow. If the loan only looks affordable at today’s rate, it is too tight. The borrower who plans for the calm scenario and gets the stormy one is the borrower who struggles. Plan for the storm.

The cost beyond the headline rate

The APR is only part of the cost. Prodigy loans carry a one-time origination fee, charged as a percentage of the loan and typically deducted up front, which means you receive slightly less than you borrow but pay interest on the full amount. Built into the effective cost, this pushes the true APR above the headline interest figure. The rate itself is usually a floating base rate plus a margin, so it can move over the life of the loan.

There is also the tax angle. Section 80E of the Income Tax Act allows an Indian borrower to deduct education-loan interest from taxable income, but it applies to loans taken from Indian banks and notified Indian financial institutions. A loan from a foreign lender like Prodigy generally does not qualify for the 80E deduction, which quietly removes a benefit that a rupee loan from an Indian bank or notified NBFC would have given you. Confirm your own position with a tax advisor, because it changes the after-tax cost comparison.

And the central interest subsidy schemes that can apply to scheduled-bank education loans in India do not apply here either. So when you compare Prodigy to a rupee loan, you are comparing a higher headline rate, plus an origination fee, plus forex risk, plus the loss of 80E and any subsidy, against a lower rupee rate that keeps all those benefits. The headline numbers understate the gap.

A worked example: Prodigy versus a rupee loan

Take a concrete case. A student admitted to a one-year MBA at a top European school, cost of attendance roughly USD 50,000 of fundable need. She has no property to pledge and her father’s income would not support a full unsecured NBFC sanction. Prodigy offers USD 50,000 at an indicative 12 percent APR over seven years, with an origination fee deducted up front.

Compare this to a hypothetical rupee NBFC loan of the same ₹42 lakh equivalent at 12.5 percent. On paper the rupee rate is even slightly higher. But the rupee borrower repays in rupees with zero forex exposure, may claim 80E on the interest, and faces no origination fee of the foreign kind. If she returns to India and the rupee weakens over the seven years, the Prodigy dollar loan can end up costing several lakh more in rupee terms despite the lower headline rate, as the two-scenario table above shows.

The honest conclusion from the math: Prodigy wins decisively on one axis only, access. If no rupee lender will fund you because you have no collateral and no strong co-applicant, then a workable Prodigy loan beats no loan and a missed admit. But if a rupee route is genuinely open to you, the rupee loan almost always costs less once forex risk and lost tax benefits are counted. The destination-level funding picture for the US, where many Prodigy borrowers head, sits in the education loan for USA guide and the all-in numbers are in the cost of studying in the USA post.

The forex mechanics you have to handle yourself

Disbursement and repayment of a foreign-currency loan both run through the forex system, and that adds friction a rupee loan never has. On the way out, the loan disburses in foreign currency to the school. On the way back, if you repay from India, every EMI is a foreign-currency outward remittance under the Liberalised Remittance Scheme, which carries its own paperwork and limits. The mechanics of the A2 form, the LRS limit and student remittances are covered in the A2 form and LRS forex guide, and the regulatory framework for all of this is set by the central bank, whose rules sit on the RBI website.

The practical upshot is that a Prodigy loan is not just a higher-risk loan, it is also a more operationally involved one for an India-based repayer. Bank charges on each outward remittance, currency conversion spreads on every EMI, and the LRS reporting all add small recurring costs and effort that a rupee EMI by simple auto-debit does not.

Who Prodigy Finance genuinely fits

I want to be fair here, because for a specific student this lender is a real solution, not a trap. Prodigy fits when several things are all true at once. You have an admit to a program that is actually on the supported list, usually a premier MBA or top STEM Master’s. You have no collateral to pledge and no co-applicant strong enough to carry a full unsecured rupee loan, so rupee lenders cannot fund you. And, ideally, you plan to work and earn in the same currency you borrowed, in the US on a dollar loan for example, so the forex risk on repayment is largely neutralised.

For that student, with a top admit, no rupee access, and a likely foreign-currency income, Prodigy is a clean way to fund a high-return program that would otherwise be out of reach. That is the case it was built for, and it works. If your admit is specifically to a US Master’s, it is worth putting Prodigy next to our Leap Finance education loan guide, another collateral-free dollar lender whose SOFR-linked floating rate sometimes lands cheaper for US-bound students.

Who it does NOT fit

It does not fit the larger group of students who reach for it out of convenience rather than necessity.

- Anyone who can pledge collateral and access a PSU bank. The PSU rupee rate plus 80E plus possible subsidy will beat Prodigy comfortably, with no forex risk.

- Anyone with a co-applicant strong enough for an unsecured NBFC rupee loan. The rupee NBFC route keeps you in your own currency and your 80E deduction.

- Anyone who plans to return to India and earn in rupees while repaying a dollar or euro loan. You will carry pure forex risk on every EMI for years, with no income hedge against it.

- Students at programs that are not on the supported list. You are simply not eligible, and building hope around it wastes time you could spend on a rupee sanction.

- The forex-risk-averse, or anyone whose repayment plan only works if the exchange rate stays exactly where it is today. The honest plan assumes a weaker rupee, and if that breaks the budget, this loan is not for you.

The honest summary is narrow on purpose. Prodigy is a door for students who have no other door. If you do have another door, walk through the rupee one.

FAQ

Is Prodigy Finance good for Indian students?

It is genuinely useful for a narrow group: students with an admit to a supported premier program, no collateral and no strong co-applicant, so no rupee lender will fund them. For that student it can be the only workable loan. For everyone else with access to a PSU bank or an unsecured NBFC rupee loan, it is usually more expensive once forex risk, the origination fee and the loss of the 80E tax deduction are counted. Eligibility depends on your specific program being on its list.

Does Prodigy Finance need a cosigner or collateral?

No. That is its defining feature. Prodigy underwrites on the school you got into and your projected post-study earnings for that program, not on a co-applicant or pledged security. There is no property to mortgage and no parent signing as guarantor. This is the entire reason it exists, and the reason students with no collateral and no strong co-applicant turn to it. The trade-off is a higher effective cost and the forex risk that comes with a foreign-currency loan.

What currency does Prodigy Finance lend in?

It lends in US dollars, pounds sterling or euros, depending on where you study, not in rupees. This is the single most important thing to understand. Your loan amount and every EMI are fixed in that foreign currency. If you later earn in rupees and repay from India, you convert rupees to that currency at the prevailing rate on each payment, so a weakening rupee raises your real rupee cost even though the foreign-currency terms never change. The forex risk is entirely yours.

What is the interest rate on a Prodigy Finance loan?

The effective APR typically lands around 11 to 13 percent, usually structured as a floating base rate plus a margin, so it can move over the life of the loan. On top of the headline rate there is a one-time origination fee deducted up front, which raises the true effective cost above the stated interest figure. Always confirm the exact APR, the margin, the base rate and the fee on your own sanction document, because terms vary by program and change over time.

Can I claim Section 80E tax benefit on a Prodigy loan?

Generally no. Section 80E allows deduction of education-loan interest from taxable income, but it applies to loans from Indian banks and notified Indian financial institutions. A loan from a foreign lender like Prodigy usually does not qualify, which removes a benefit a rupee loan from an Indian bank or notified NBFC would have given you. This quietly widens the real cost gap against a rupee loan. Confirm your specific position with a qualified tax advisor before deciding.

Which schools and programs does Prodigy Finance fund?

It funds a curated list of high-ranked global Master’s programs, weighted heavily toward elite MBA, finance and STEM courses at well-known universities. It does not fund most undergraduate degrees, mid-ranked programs, or any course not on its supported list. The school and program are the first and hardest eligibility gate, and most Indian students who are turned away fail at this step. Confirm in writing that your exact program is eligible before you treat Prodigy as a funding source.

Is Prodigy Finance cheaper than an Indian education loan?

Rarely, once everything is counted. The headline APR can look competitive, but the foreign-currency denomination adds forex risk, there is an origination fee, and you usually lose the 80E tax deduction and any central interest subsidy that a scheduled-bank rupee loan would carry. For a borrower who returns to India and earns in rupees, a weakening rupee can push the real cost several lakh above a comparable rupee loan. Prodigy wins on access, when no rupee lender will fund you, not on price.

How do I repay a Prodigy loan from India?

You repay each EMI as an outward foreign-currency remittance under the Liberalised Remittance Scheme, converting rupees to the loan currency on each payment. This involves the A2 form, LRS reporting, bank remittance charges and a currency conversion spread on every EMI, none of which a simple rupee auto-debit needs. The regulatory framework is set by the RBI. Budget for these recurring costs and the operational effort, because they add to the real cost of a foreign-currency loan repaid from India.

Faz · The Honest Journey · 2026