A Leap Finance education loan is a collateral-free, US-focused loan for master’s students that is denominated in US dollars and sent straight to your university, with amounts from 15,000 to 100,000 US dollars and an advertised rate starting around 8.45 percent. The honest catch is buried in the fine print. That rate is floating, tied to the 30-day CME Term SOFR benchmark and reset every quarter, and because you repay in dollars, a weaker rupee quietly raises your real cost at home. So the 8.45 percent is a best-case floor, not the number most students get, and the true price depends on where SOFR and the rupee go over the next few years. Confirm your personalised rate, the reset terms, and the dollar repayment math before you sign, because that is where the real cost hides.

A reader messaged me last year with an admit to a one-year analytics master’s in the United States, no property the family wanted to pledge, and two PSU branches that had gone quiet on him. Someone pointed him at Leap Finance, and the pitch landed well: no collateral, money straight to the university, a sanction in days, and a rate “starting at 8.49 percent” that sounded better than anything a domestic lender had quoted. He was ready to sign. Then I asked him one question. What currency is the loan in? He did not know. It is in dollars. And the moment a loan is in dollars, the rupee in your salary account becomes part of the deal whether you planned for it or not.

This post is the honest picture of what a Leap Finance loan actually is, who it genuinely fits, and where the cost sits that the brochures gloss over. I do not earn anything if you borrow from Leap Finance or from anyone else. This is the conversation I would have with that reader before he signed, not after.

To compare this NBFC against the alternatives: the avanse education loan post, the InCred education loan post, and the auxilo education loan post.

What Leap Finance actually is

Leap Finance is a Bengaluru-based fintech, founded in 2019, that lends to Indian students going abroad, with a heavy focus on master’s programs in the United States. It is not a traditional bank and it is not one of the established Indian education-loan NBFCs like HDFC Credila or Avanse. It is a newer, cross-border lender whose whole model is built around one idea: underwrite the student on academic potential and future earning power rather than on family wealth or a pledged property, and lend in dollars directly into the US system.

That model is genuinely different from the domestic options, and the difference is the whole story. A domestic lender, PSU bank or NBFC, gives you rupees in India, and you or your family carry the loan in rupees. Leap Finance gives you dollars in America. That changes who carries the currency risk, how the rate is set, and even how you build credit while you study. If you want the full landscape of Indian education loans before you narrow to one lender, the education loan India complete guide lays out the whole field, and the PSU bank versus NBFC education loan post is the single most useful thing to read alongside this one.

The headline that draws people in

Leap Finance’s appeal is real, so let me state it fairly before I get to the price. It is genuinely collateral-free. No Indian house, flat, or fixed deposit is pledged, which matters enormously for families who have income but no asset they want tied to a loan. The underwriting weights the student’s academic record and potential over the family’s economic background, so a strong applicant from a modest household can qualify where a domestic bank would have asked for security. The loan range runs from 15,000 to 100,000 US dollars, covering tuition, administration, and lodging and living costs for the course duration, and the funds go directly to the institution rather than passing through the student’s hands.

There is one more feature that is quietly clever. During your studies you make a token payment of about 100 US dollars per month from the very first month, and that small, regular payment helps you build a US credit history. For a student arriving in America with no credit file at all, that head start is worth real money later, when you want an apartment, a car, or a US credit card. Full EMIs do not begin until 36 months in, after the course, so the heavy repayment is pushed to when you are earning. For a strong student with a US admit and no collateral, that combination is genuinely attractive. The question is never whether Leap can fund you. It often can. The question is what that funding costs once the dollar and the floating rate are in the picture.

The currency catch nobody explains

Here is the single biggest under-explained fact about this loan, and it is the reason I wrote this post. Your loan is in US dollars. You borrow dollars, you owe dollars, and eventually you repay dollars. If you stay and work in the United States and earn in dollars, that is clean and natural, your salary and your loan are in the same currency. But if you return to India, or you ever need to service the loan from rupee income, the exchange rate becomes a silent third party in the deal.

When the rupee weakens against the dollar, and over the long run it has tended to, every dollar of EMI costs you more rupees than it did when you signed. The interest rate on the loan does not change because of this. The dollar amount does not change. But the rupee cost of clearing it quietly climbs. Nobody puts that on the sanction summary, because technically the loan terms have not moved. Your real burden has. This is not a reason to walk away. It is a reason to go in with your eyes open and to think honestly about whether you will be earning in dollars or in rupees when the EMIs start.

How Leap Finance’s interest rate really works

This is the section the marketing skips, so read it twice. Leap Finance advertises a rate “starting at” roughly 8.45 to 8.49 percent. Read the word “starting” carefully, because it is doing a lot of work. That is a best-case floor for a top profile, not the rate most students sign. The on-site FAQ itself shows the band running up toward 9.99 percent, and the rate is personalised from about nine factors, including your university and its placement record, your course, the country, your GRE and academic record, your loan tenure, and whether the loan is collateral-free. A no-collateral loan for a mid-tier program will not get the floor rate.

There is also a labelling issue worth flagging honestly. One Leap page describes the rate as fixed, while the dedicated SOFR page makes clear it is floating. The SOFR page is the accurate one. The rate is variable, linked to the 30-day CME Term SOFR benchmark, and it is reset every quarter on the 1st of January, April, July, and October, using the benchmark disclosed on the preceding business day. So your rate today is a starting point, not a fixed cost for the life of the loan. If SOFR rises, your rate rises and your EMI or tenure stretches with it. If it falls, you benefit. That is normal for a US-style student loan, but it is the opposite of the fixed-rate certainty some borrowers assume they are getting.

Faz's ruleThe advertised rate is a floor, and it floats. Get your personalised rate in writing, confirm it is linked to SOFR and reset quarterly, and ask the lender to show you what your EMI looks like if SOFR rises two points. If the answer is vague, that vagueness is the product.

Every lender advertises its best-case rate, and every borrower assumes it applies to them. With Leap there are two layers to pin down: the personalised spread that turns 8.45 percent into your actual number, and the SOFR reset that can move it later. Ask the relationship manager to walk you through a rate-rise scenario in dollars and then in rupees at a weaker exchange rate. The number that matters is your worst realistic case, not the brochure floor.

The fee you should know about

Leap Finance charges a processing fee of 3 percent of the loan, and it is split: 1 percent at sanction and the remaining 2 percent when you actually request the funds. On a 50,000 US dollar loan that is 1,500 dollars in fees, which at a weak rupee is a meaningful sum in Indian terms. It is not unusual for a cross-border fintech loan, but it is higher than the 1 to 2 percent that established Indian NBFCs typically charge, so factor it into your comparison rather than treating it as a rounding error.

The structure is at least sensible. You pay the smaller 1 percent slice at sanction and the larger 2 percent only when you draw the money, so if your plans change before disbursal you have not paid the full fee. Still, confirm the exact fee, when each slice is due, and whether any part is refundable, in writing, before you commit.

How the money flows, and why that is a feature

One thing Leap Finance does well is disbursement. The loan is sent directly to your university or institution, not into your account, before you arrive. For tuition that is genuinely useful, because it removes the scramble of moving large sums across borders yourself and it satisfies the university’s payment deadlines cleanly. It also covers lodging and living costs for the course duration, so the structure is built around the real shape of a master’s program rather than just tuition.

The repayment design is borrower-friendly on paper too. There are two modes. In the Pre-EMI mode you pay only the interest on what has been disbursed while you study, which keeps the burden light and chips away at the cost. In the Full EMI mode you pay principal plus interest, but only after the full loan has been disbursed and the course is done. Combined with the 100 US dollar monthly token payment that builds your US credit, the design clearly assumes a student who will be earning in dollars by the time full EMIs begin. That assumption is the quiet condition under which this loan makes the most sense.

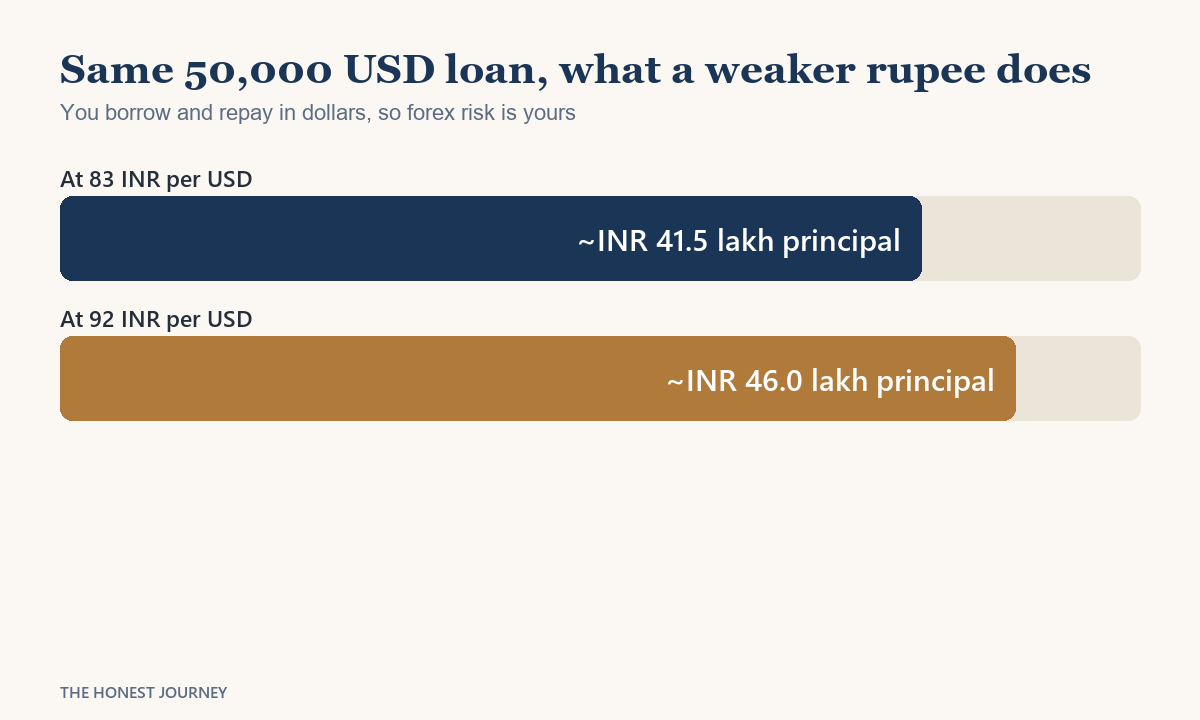

The worked example, when the rupee weakens

Take a real-shaped case to make the currency point concrete. A student borrows 50,000 US dollars. Imagine, for a clean illustration, that the total dollars repaid over the life of the loan, principal plus interest, come to about 70,000 US dollars. The dollar figure is fixed by the loan. What is not fixed is what those dollars cost in rupees, and that depends entirely on the exchange rate when you pay.

| Item | If repaid at 83 INR per USD | If repaid at 92 INR per USD |

|---|---|---|

| Loan principal | USD 50,000 | USD 50,000 |

| Illustrative total repaid (principal plus interest) | USD 70,000 | USD 70,000 |

| Assumed exchange rate at repayment | 83 | 92 |

| Total rupee cost of clearing the loan | ~₹58.1 lakh | ~₹64.4 lakh |

| Extra rupee cost from a weaker rupee | baseline | ~₹6.3 lakh more |

The interest rate did not change. The dollar amount did not change. Yet a rupee that weakened from 83 to 92 against the dollar added roughly 6.3 lakh rupees to the real cost of the same loan, paid by a borrower servicing it from rupee income. These figures are illustrative, not a quote, and the floating SOFR rate could push the total dollars repaid higher or lower than my round 70,000 assumption. The point stands regardless. If you will earn in dollars, this risk barely touches you. If you will earn in rupees, it is real, and it belongs in your decision. To see how Leap’s rate band compares against domestic options, the education loan interest rate comparison post puts PSU, private bank, and NBFC rates side by side.

Faz's ruleBefore you sign a dollar-denominated loan, answer one question honestly: will you be earning in dollars or in rupees when the EMIs start. If dollars, the currency risk is small and Leap's structure fits beautifully. If rupees, run the repayment at a meaningfully weaker exchange rate and see if you can still carry it.

The lender will show you the dollar EMI because that is what it controls. Nobody at the loan desk owns the rupee. So you have to own it yourself. Take the dollar EMI, multiply it by an exchange rate ten percent worse than today’s, and ask whether that rupee number is comfortable on the income you actually expect. If it is, sign with confidence. If it is not, a rupee loan from a domestic lender removes the currency risk entirely, and that is worth comparing.

Speed and the credit head start, the genuine upside

Where Leap Finance earns its keep is the online process and the US credit head start. The application is digital, the sanction is fast when the file is clean, and a personalised rate is quoted quickly. For a student facing a US deposit deadline or an I-20 timeline that will not wait, that speed is not a luxury, it is the difference between making the intake and deferring a year.

The 100 US dollar monthly token payment is the other genuine benefit, and it is underrated. Arriving in America with no credit history is a real handicap. Every apartment lease, phone contract, and credit card application runs into a thin or empty credit file. By making a small, on-time payment every month from the start, you build a US credit record while you study, which makes the rest of your financial life in America easier and cheaper. A domestic rupee loan does nothing for your US credit. This one does, and for a student who intends to stay and work in the United States, that is a meaningful edge.

Who a Leap Finance loan genuinely fits

Being honest about fit is the whole point of this site, so here it is plainly. A Leap Finance loan fits you when several of these are true at once:

- You are doing a master’s level program, ideally STEM, at a US university that Leap supports, since the product is built around exactly this profile.

- You have no collateral to pledge and you want to keep family assets out of the loan entirely.

- You have a strong academic record, because the underwriting rewards academic potential over family wealth, and that is what earns a better rate.

- You realistically expect to stay and earn in US dollars after graduation, which neutralises the currency risk and matches the dollar-denominated structure.

- You value the US credit-building head start and a fast, online sanction against a hard deadline.

Who it does NOT fit

This is the section the marketing skips, so read it twice. A Leap Finance loan is the wrong choice when:

- You expect to return to India and repay from rupee income, because then the dollar denomination puts the currency risk squarely on you and a rupee loan removes it.

- You can pledge collateral and have time to arrange a secured PSU loan, which will usually carry a lower effective rate and may carry a central interest subsidy Leap cannot offer.

- You are studying outside the United States, or at a program or country level Leap does not support, since the product is narrow by design.

- You want fixed-rate certainty, because this rate floats with SOFR and resets quarterly, so your EMI can rise during repayment.

- You are highly fee-sensitive, since the 3 percent processing fee runs above what established domestic NBFCs typically charge.

The cleanest mental test: if you are US-bound, STEM, collateral-free, and likely to earn in dollars, Leap is built for you and the currency risk is small. If any of those is not true, especially the dollar-income part, compare a rupee loan carefully before you commit.

Leap Finance versus the alternatives

It helps to place Leap among the realistic options rather than judging it alone. Against the other cross-border, future-earnings lenders, Prodigy Finance and MPower Financing, Leap sits in the same broad category: collateral-free, dollar-denominated, profile-based underwriting aimed at international students. The exact rates, fees, and eligibility differ by lender and by profile, so do not trust any third-party number you read about those two. Confirm their figures on their own official sites. If you are weighing the cross-border route, read the MPower Financing review and the Prodigy Finance review next to this one, because they share the same currency and floating-rate trade-offs.

Against domestic lenders the contrast is sharper. An Indian NBFC like HDFC Credila lends in rupees, so there is no currency risk, but it usually leans on a co-applicant’s income and often a property for larger amounts. A PSU bank like SBI for abroad studies is cheaper still and may carry a central interest subsidy, but it is slower and collateral-hungry above the small-ticket tier. The genuine question is not which lender is best in the abstract. It is whether you want a rupee loan that keeps the currency risk off your plate, or a dollar loan that matches a dollar income and builds US credit. For the collateral angle specifically, the education loan for abroad studies without collateral post weighs the no-security route across every lender, and the education loan for USA post covers the US-specific landscape in full.

The TCS and forex angle from the India side

There is one more piece that applies from the Indian end. When money moves abroad for education under the Liberalised Remittance Scheme, it can attract tax collected at source, or TCS. The rules and thresholds sit on the official Reserve Bank of India site for the LRS framework, and the practical detail is in the TCS on education loan India post. With a dollar loan disbursed directly to the university, the forex conversion and any associated TCS sit at the point of remittance, and the exchange-rate risk on repayment sits with you. None of this is a reason to avoid Leap. It is a reason to budget for the full picture, fee, forex, and TCS, rather than just the headline rate.

What borrowers actually report

I will not name-and-shame, and I will not pass off anonymous review-site sentiment as fact. But there are recurring themes in borrower feedback worth raising honestly, because they concern the part of the relationship that starts after the sanction, when the excitement has faded. Some borrowers report communication gaps and slower-than-hoped responses on post-sanction service, and some were surprised later by the floating rate moving, having assumed it was fixed. None of this makes Leap a bad lender, and a newer fintech scaling quickly will have growing pains that an established bank may not. The lesson is defensive, not damning. Pin down the rate structure and reset terms in writing, keep your relationship manager’s contact, understand the dollar repayment math before you sign, and you remove most of the surprises that the complaints are really about.

Where Leap Finance sits in the rulebook

Because the loan is cross-border and dollar-denominated, the regulatory picture is not the same as a domestic NBFC loan, and the remittance side is governed by the RBI’s Liberalised Remittance Scheme, the framework for which is published on the RBI site. The product facts in this post, the dollar range, the floating SOFR-linked rate, the 3 percent fee, the token payment, and the eligibility rules, are published on Leap Finance’s own site at leapfinance.com, and you should confirm the live numbers there and on your sanction letter, because they move. Note the genuine gap I found while researching this: the eligibility page softens the co-signer to “you may require a co-signer,” while the homepage and the MS-in-USA page state plainly that a co-signer is required. Treat a co-signer as required and confirm it directly, rather than assuming the softer wording applies to you.

The honest take

Leap Finance is a serious, well-built cross-border lender that does something genuinely useful: it funds US master’s students with no collateral, underwrites on academic potential rather than family wealth, sends the money straight to the university, and gives you a head start on US credit while you study. For a strong student bound for a US program, with no asset to pledge and a plan to stay and earn in dollars, it is a genuinely good fit, and the speed and the credit-building are real benefits worth having.

But it is not the simple, low-rate loan the headline suggests. The 8.45 percent is a best-case floor, your real rate is personalised and floats with SOFR, the rate resets every quarter, and the loan is in dollars, so a weaker rupee quietly raises your real cost if you ever repay from rupee income. The 3 percent fee runs above domestic NBFCs, and a co-signer is required despite some softer marketing language. None of these is a dealbreaker. They are trade-offs. Decide whether you will earn in dollars or rupees, get your personalised rate and the reset terms in writing, run the repayment at a meaningfully weaker exchange rate, and sign with the real cost in front of you, not behind you.

FAQ

Is a Leap Finance education loan really collateral-free?

Yes. Leap Finance does not require any collateral, so no Indian house, flat, or fixed deposit is pledged against the loan. Instead it underwrites on the student’s academic record and potential rather than the family’s economic background, which is why a strong applicant from a modest household can qualify where a domestic bank would have demanded security. That said, a co-signer is required to share the repayment, so collateral-free does not mean co-signer-free. Treat the loan as genuinely unsecured but plan for a co-signer with a clean credit history.

Does Leap Finance require a co-signer?

In practice, yes, and this is worth flagging because the wording on Leap’s own pages is inconsistent. The eligibility page softens it to “you may require a co-signer,” while the homepage and the MS-in-USA page state plainly that a co-signer is required to share the loan repayment. The safe assumption is that you will need a co-signer with a good credit history, so line one up early and confirm the requirement directly with the lender rather than relying on the softer phrasing, which could leave you scrambling at sanction time.

What currency is the Leap Finance loan in, and why does that matter?

The loan is denominated in US dollars, with amounts from 15,000 to 100,000 US dollars, and the funds go directly to your university. This matters because you repay in dollars. If you earn in dollars after graduation, your loan and your income are in the same currency and the structure works cleanly. But if you repay from rupee income, a weaker rupee raises the real cost of clearing the loan even though the dollar amount and the interest rate have not changed. The currency risk is the single most under-explained part of this loan, so factor it in before you sign.

Is the Leap Finance interest rate fixed or floating?

It is floating, despite one Leap page describing it as fixed. The accurate description, on Leap’s dedicated SOFR page, is that the rate is variable and linked to the 30-day CME Term SOFR benchmark, reset every quarter on the 1st of January, April, July, and October. The advertised rate starting around 8.45 percent is a best-case floor personalised from about nine factors, and the on-site FAQ shows the band running up toward 9.99 percent. Because the rate floats and resets, the number you sign is a starting point, not a fixed cost, so confirm your personalised rate and the reset terms in writing.

What is the Leap Finance processing fee?

Leap Finance charges a processing fee of 3 percent of the loan, split into 1 percent at sanction and 2 percent when you request the funds. On a 50,000 US dollar loan that is 1,500 dollars in total, which is a meaningful sum in rupee terms and runs above the 1 to 2 percent that established Indian NBFCs typically charge. The split structure is at least reasonable, since you pay the larger slice only when you actually draw the money. Confirm the exact fee, the timing of each slice, and whether any part is refundable before you commit.

How does repayment work, and what is the 100 dollar token payment?

During your studies you make a token payment of about 100 US dollars per month from the very first month, which helps build a US credit history that makes the rest of your financial life in America easier. Full EMIs do not begin until 36 months in, after the course, so the heavy repayment is pushed to when you are earning. There are two modes: Pre-EMI, where you pay only interest on what has been disbursed while you study, and Full EMI, where you pay principal plus interest after the full loan is disbursed. The design assumes a student who will be earning in dollars by the time full EMIs start.

Who should choose Leap Finance over a domestic lender?

Choose Leap Finance if you are doing a US master’s, ideally STEM, at a supported university, have no collateral to pledge, have a strong academic record, and realistically expect to stay and earn in US dollars. In that case the dollar denomination matches your income, the credit-building token helps you in America, and the fast online sanction suits a tight deadline. Prefer a domestic rupee loan if you expect to return to India and repay from rupee income, if you can pledge collateral for a cheaper PSU loan, or if you want fixed-rate certainty, since those needs sit outside what Leap is built to do.

Faz · The Honest Journey · 2026