An Auxilo education loan is a loan from a dedicated education-loan NBFC that will fund the full cost of your course, secured or unsecured, with no margin money and no foreclosure charge. The catch is the price. Auxilo’s benchmark lending rate is 15.10 percent and your actual rate is that benchmark plus a profile-based spread, so the “starts from 9.5 percent” you see advertised is a best-case floor, not the number most students get. The rate also floats, which means it can reset upward during your repayment. Confirm your exact spread, the reset terms, and whether your country forces a secured loan on the sanction letter, because that is where the real cost hides.

A reader wrote to me last year, halfway panicked. He had an admit to a taught Master’s in Ireland, no property to pledge, and a co-applicant father whose income was strong but self-employed and hard for a bank to read. Two PSU branches had effectively said no. An agent pointed him at Auxilo, quoted him “around 9.5 percent,” and told him the sanction would be quick. The sanction was quick. The rate on the letter was not 9.5 percent. It was closer to 13, floating, and he only noticed the floating part when I asked him to read me the rate clause.

This post is the honest picture of what an Auxilo loan actually is, who it genuinely fits, and where the cost sits that the agent brochures gloss over. I do not earn anything if you borrow from Auxilo or from anyone else. This is the conversation I would have with that reader before he signed, not after.

To compare this NBFC against the alternatives: the MPOWER financing education loan post, the prodigy finance education loan post, and the leap finance education loan post.

What Auxilo actually is

Auxilo Finserve Private Limited is a non-banking financial company, an NBFC, registered with the Reserve Bank of India, that does only one thing: education loans. It launched in 2017, so it is younger than HDFC Credila or Avanse, but it sits in the same category, a focused education-loan lender rather than a bank with a loan desk on the side. That focus is the whole character of the product. It underwrites students and their co-applicants, it moves faster than a PSU bank, and it is more flexible on profile, and in exchange it charges more.

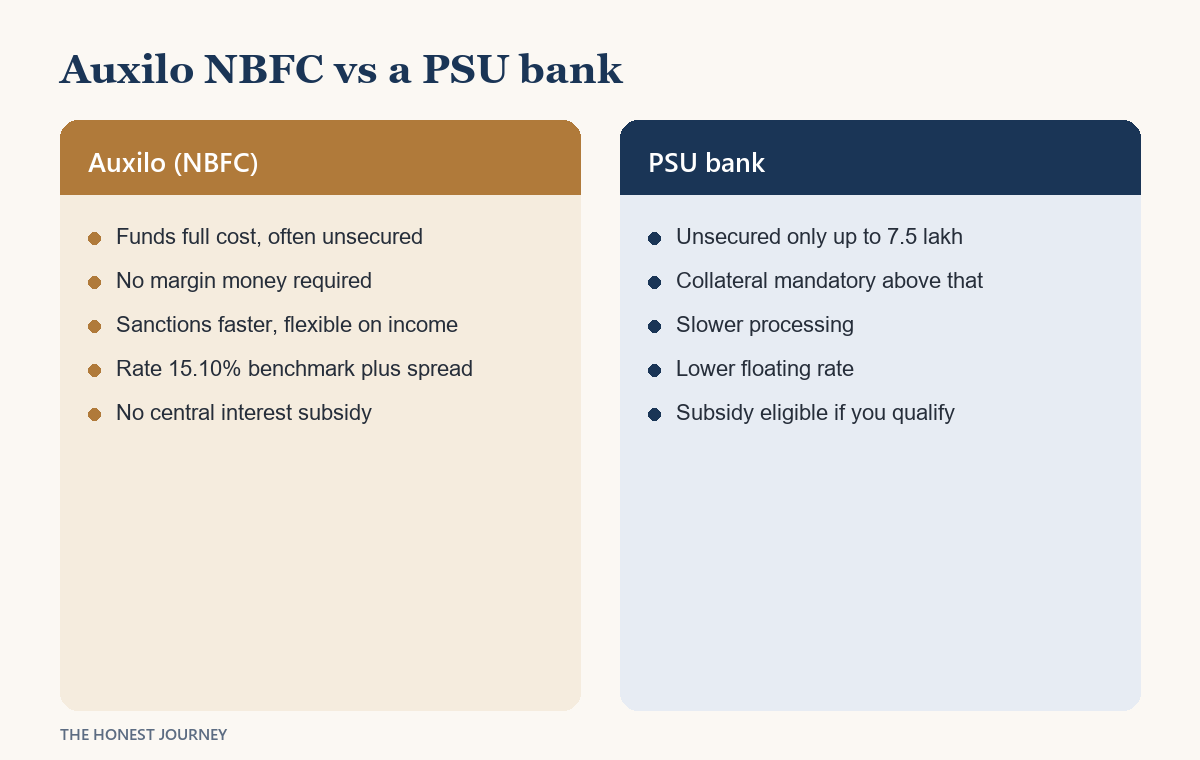

The practical difference between an NBFC like Auxilo and a PSU bank comes down to four things: collateral, rate, speed, and the central interest subsidy. An NBFC lends bigger amounts unsecured, sanctions faster, and is friendlier to irregular income, but it charges a higher rate and its loans sit outside the government’s interest subsidy scheme. A PSU bank is the mirror image, cheaper and subsidy-eligible, but slower and collateral-hungry above ₹7.5 lakh. If you want the full landscape before you narrow to one lender, the education loan India complete guide lays out the whole field, and the PSU bank versus NBFC education loan post is the single most useful thing to read alongside this one.

The headline that draws people in

Auxilo’s appeal is real, so let me state it fairly before I get to the price. It offers both secured and unsecured loans and says plainly that it has no fixed upper limit, that it will fund your total cost of education. It asks for no margin money, the borrower contribution that PSU banks usually demand on larger loans. It covers the full spread of expenses, tuition, examination fees, living costs, travel, pre-admission costs, and other course-related costs. It accepts multiple co-applicants, even across cities, and the co-applicant can be a parent, sibling, parent-in-law, or spouse, which is more flexible than most banks. It lends across more than 25 countries, including all the usual abroad destinations and India study as well.

For a student with no collateral and a hard deadline, that combination is genuinely valuable. The question is never whether Auxilo can fund you. It usually can. The question is what that funding costs, and whether you are actually buying the part you need.

How Auxilo’s interest rate really works

This is the section the brochures skip, so read it twice. Auxilo’s rate is not a single advertised number. It is built in two parts: a benchmark lending rate, which Auxilo publishes, plus a spread that Auxilo sets individually for your file based on your credit profile and your course. As of writing, the published Auxilo benchmark lending rate is 15.10 percent. Your final rate is that benchmark plus your spread, and the interest is charged as simple interest with monthly rest.

So where does “starts from 9.5 percent” come from? It is the best-case floor on Auxilo’s study-abroad page, the rate a top-tier profile at a premier program might be offered. It is not wrong, but it is not typical, and it is not what most students sign. The aggregator sites that rank for “Auxilo interest rate” quote everything from 11 to 14.5 percent precisely because the spread is profile-specific, so they all disagree. The only number that matters is the one on your sanction letter.

The second thing to understand is that the rate floats. It moves with the benchmark. If Auxilo’s benchmark rises, your rate rises, and your EMI or your tenure stretches with it. That is normal for an NBFC, but it means the number you sign is a starting point, not a fixed cost for the life of the loan. A PSU secured loan also floats, but it starts two to four percentage points lower, and over a long repayment that gap is large.

Faz's ruleThe advertised rate is a floor, not your rate. Your rate is the published benchmark plus a spread you only see on the sanction letter. Get that exact number, the spread, and the reset terms in writing before you sign anything.

Every NBFC advertises its best-case rate, and every borrower assumes it applies to them. It usually does not. Ask the relationship manager one direct question: what is my spread over the benchmark, and how often can it reset? If the answer is vague, that vagueness is the product. The total interest line is the one nobody volunteers, and it is the only one that matters.

The fees you should know about

Auxilo’s fee structure has one genuine advantage and one genuine trap, and you should know both.

The advantage is foreclosure. Auxilo charges no prepayment or foreclosure penalty on its student education loans. If you come into money and want to clear the loan early, you can, without a penalty eating the benefit. On a floating-rate loan that is worth having, because prepaying is your main defence against a rising rate.

The trap is the processing fee. Auxilo charges a processing fee of 2 percent of the sanctioned amount, and it is non-refundable regardless of whether your loan is approved, rejected, or withdrawn. Read that again. If you pay the fee and the loan falls through, the fee does not come back. On a ₹40 lakh sanction that is ₹80,000 at risk. Two other charges to note: a late payment penalty of 18 percent per annum plus tax on overdue amounts, and a bounce charge of ₹400 plus tax per failed EMI. Neither is unusual, but both are worth knowing before you set up the mandate.

Secured, unsecured, and the country catch

Auxilo does both secured and unsecured loans, and the unsecured appetite is why most people come to it. But the unsecured route is not open everywhere. Auxilo treats some destinations as secured-only, New Zealand being one it names, where it will want collateral regardless of your profile. For collateral it accepts a fixed deposit, a flat, a house, non-agricultural land, or a shop. So the first thing to check is not your rate but your route: for your specific country and profile, is Auxilo offering you unsecured, or is collateral mandatory? That single answer changes the entire comparison, because if collateral is on the table anyway, a PSU secured loan at a lower rate becomes the obvious benchmark.

If the absence of collateral is your whole reason for considering Auxilo, read the education loan for abroad studies without collateral post alongside this one, because it weighs the unsecured route across every lender, not just this one, and the maximum education loan amount in India post shows where the unsecured walls sit across the market.

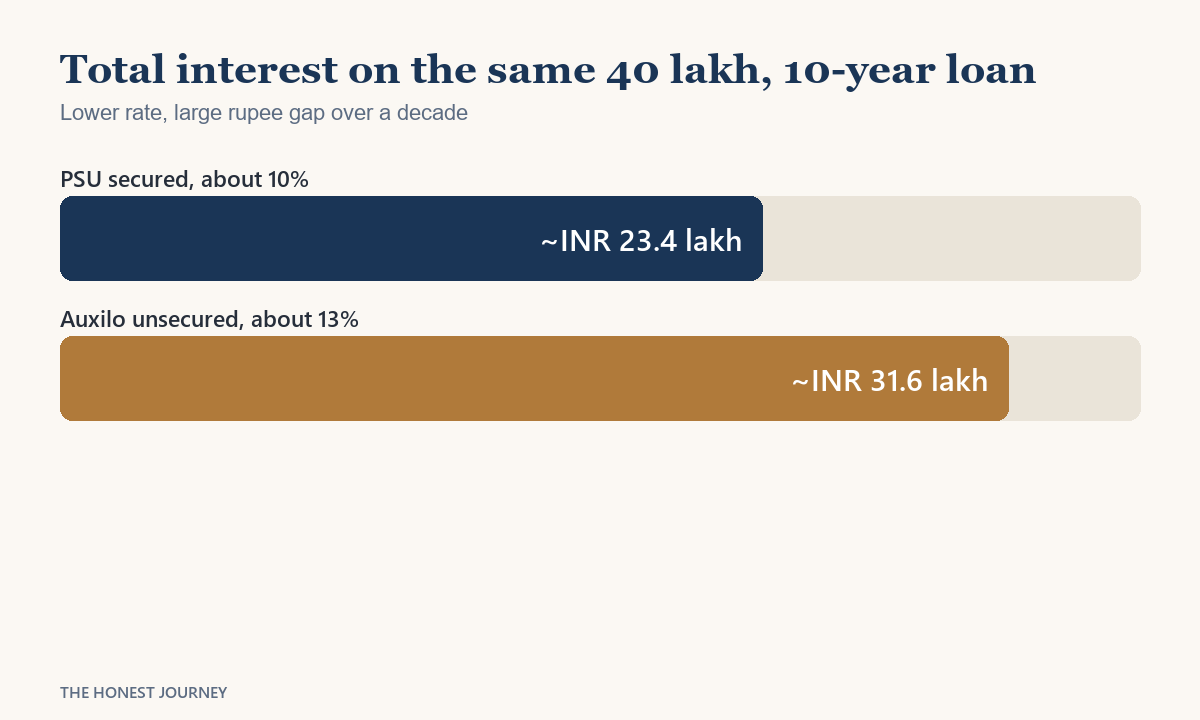

The worked INR example, Auxilo versus a PSU secured loan

Take a real-shaped case. A student needs ₹40 lakh for a Master’s abroad. The family has no property it wants to pledge, so the realistic choice is an Auxilo unsecured loan at, say, 13 percent against a PSU secured loan at 10 percent if collateral could be arranged. Assume a ten-year repayment in both cases for a clean comparison.

| Item | Auxilo (NBFC unsecured) | PSU (secured) |

|---|---|---|

| Loan amount | ₹40,00,000 | ₹40,00,000 |

| Indicative interest rate | ~13.0% (floating) | ~10.0% (floating) |

| Tenure | 10 years | 10 years |

| Approx EMI | ~₹59,700 | ~₹52,860 |

| Approx total interest paid | ~₹31.6 lakh | ~₹23.4 lakh |

| Processing fee (2%) | ~₹80,000, non-refundable | Often lower or capped |

| Central interest subsidy | Not available | Available if eligible |

The interest gap alone is roughly ₹8 lakh over the life of the loan, before you count the higher processing fee or the lost subsidy. That is the real price of the unsecured convenience. It does not make Auxilo wrong. It makes Auxilo a considered choice rather than a default. If the family genuinely cannot pledge collateral and the program needs funding now, that extra interest is the cost of getting the student there at all, and it can be entirely worth it. If the family could have pledged a property and simply did not want the paperwork, that ₹8 lakh is avoidable. To see how these rate bands stack across the whole market, the education loan interest rate comparison post puts PSU, private bank, and NBFC rates side by side.

Faz's ruleRun the total-interest number on your actual sanction letter, not on a website estimate, and run it before you pay the non-refundable processing fee. A two to three percent rate difference is a small number that hides a very large rupee gap over ten years.

The rate band you read online is not the rate on your sanction letter, and the processing fee is gone the moment you pay it whether the loan completes or not. Get the exact rate, the spread, the fee, and the tenure in writing, put them through an EMI calculator yourself, and only then decide. The order matters: confirm, then pay, never the reverse.

Speed and flexibility, the genuine upside

Where Auxilo earns its keep is turnaround and flexibility, the same place every good NBFC does. A secured PSU sanction means valuation visits, legal vetting of the property, and weeks of branch back-and-forth. Auxilo, underwriting mainly on the co-applicant’s documents, can move much faster when the file is clean. For a student staring at a deposit deadline or a visa timeline that will not wait, that speed is not a luxury, it is the difference between making the intake and deferring a year.

It is also more flexible on profile. A self-employed parent with strong but irregular income, exactly the file a PSU credit officer treats with suspicion, is the profile an NBFC is built to underwrite. Auxilo will look at the business, the returns, and the repayment capacity and lend where a bank hesitates. The multi-co-applicant flexibility helps too, because a thin single income can be strengthened by adding a second earning family member to the file. That flexibility is real value for the families it is designed for.

Who an Auxilo loan genuinely fits

Being honest about fit is the whole point of this site, so here it is plainly. An Auxilo loan fits you when several of these are true at once:

- You have no tangible collateral to pledge, or none worth the legal and valuation hassle, and you need an amount well above the ₹7.5 lakh PSU unsecured ceiling.

- You have a strong co-applicant, or two, with clean credit and demonstrable income, because that is what the unsecured sanction rests on.

- The student has a solid program admit, which is what unlocks a better spread over the benchmark.

- You are against a hard deadline and PSU processing speed is a genuine risk to making the intake.

- Your co-applicant is self-employed with strong but irregular income that a PSU bank struggles to assess.

Who it does NOT fit

This is the section the agents skip, so read it twice. An Auxilo loan is the wrong choice when:

- You have a pledgeable property, FD, or LIC and the time to arrange a secured PSU loan. The collateral route at a lower rate will save you several lakh in interest, and the only thing it costs you is paperwork.

- You are rate-sensitive and the loan is large with a long repayment, because the benchmark-plus-spread structure and the floating rate compound over years into a serious sum.

- You qualify for the central interest subsidy, which applies to scheduled-bank loans and generally not to NBFC loans. Giving up the subsidy to save paperwork is rarely worth it.

- Your country is one Auxilo treats as secured-only, in which case you are pledging collateral anyway and should compare a PSU secured loan directly.

- Your co-applicant income is thin or credit is weak, in which case the spread climbs to the top of the band and the value disappears.

The cleanest mental test: if a PSU secured loan is genuinely available to you, default to it on cost, and treat Auxilo as the fallback for when collateral or speed makes the PSU route impossible. The natural PSU benchmark to compare any Auxilo quote against is in the SBI education loan for abroad studies post, and if you are weighing Auxilo against the other big NBFCs, read it next to the HDFC Credila and Avanse reviews.

What borrowers actually complain about

I will not name-and-shame, and I will not pass off anonymous review-site sentiment as fact. But there are recurring themes in borrower feedback that are worth raising honestly, because they are about the part of the relationship that starts after the sanction, when the agent has moved on. The common threads: a floating rate that rose during the loan and surprised borrowers who thought their rate was fixed, communication gaps after disbursal, and collection pressure when an EMI slipped. None of this makes Auxilo a bad lender. NBFC loans float, that is the nature of the product, and collection follow-up is what every lender does. The lesson is defensive, not damning. Pin down the rate-reset terms in writing, keep the relationship manager’s contact, and never let an EMI bounce, because the ₹400 charge is the least of it. Forewarned is the entire point.

Where Auxilo sits in the rulebook

Auxilo operates as an NBFC under the Reserve Bank of India’s regulatory framework, and the current NBFC rules and registration details sit on the RBI site. If a grievance is not resolved by Auxilo’s own redressal process, it escalates to the RBI Ombudsman under the Reserve Bank’s Integrated Ombudsman Scheme, which is the formal route every regulated lender’s customer has and which is worth knowing exists before you need it. The product facts in this post, the benchmark rate, the fee structure, and the country list, are published on Auxilo’s own site at auxilo.com, and you should confirm the live numbers there and on your sanction letter, because they move.

The honest take

Auxilo is a serious, focused education-loan NBFC that will fund the full cost of your course with no margin money and no foreclosure penalty, and for a family with no collateral, a strong co-applicant, and a deadline, that is a genuinely useful product. The flexibility on profile and the speed are real, and for the right borrower they are worth paying for.

But it is not the cheap option, and the advertised rate is not your rate. Your rate is the 15.10 percent benchmark plus a spread you only see on the letter, it floats, and the 2 percent processing fee is gone the moment you pay it whether the loan completes or not. If you can pledge collateral and you have time, a PSU bank will cost you several lakh less over the life of the loan, and it may carry an interest subsidy Auxilo cannot. Use Auxilo when the unsecured speed is the thing you actually need, not because the paperwork felt lighter. Confirm the spread, the reset terms, and the route in writing, run the total-interest number yourself, and sign with the real cost in front of you, not behind you.

FAQ

What is the interest rate on an Auxilo education loan?

Auxilo’s rate is built as its published benchmark lending rate, currently 15.10 percent, plus a spread set individually for your profile and course, and the interest is charged as simple interest with monthly rest. The “starts from 9.5 percent” you see advertised is a best-case floor for top-tier profiles, not the rate most students get. Because the spread is individual and the rate floats with the benchmark, the only reliable number is the one on your sanction letter, so ask for your exact spread and the reset terms in writing before you sign.

Is Auxilo a bank or an NBFC, and is it safe?

Auxilo Finserve Private Limited is a non-banking financial company, an NBFC, registered with and regulated by the Reserve Bank of India, that specialises only in education loans and has operated since 2017. It is not a bank, so its loans are NBFC products: bigger unsecured amounts and faster sanctions than a PSU bank, but at a higher rate and without the central interest subsidy. As a regulated NBFC it falls under the RBI’s framework and its customers can escalate unresolved complaints to the RBI Ombudsman, so it is a legitimate lender, the question is cost and fit rather than safety.

Does Auxilo give collateral-free education loans?

Yes, Auxilo offers unsecured education loans and states it has no fixed upper limit, funding the total cost of education for strong profiles. However, the unsecured route is not open for every destination: Auxilo treats some countries, such as New Zealand, as secured-only, where collateral is mandatory regardless of profile. So the first thing to confirm is whether your specific country and profile qualify for unsecured, because if collateral is required anyway, a PSU secured loan at a lower rate is usually the better comparison.

What is Auxilo’s processing fee, and is it refundable?

Auxilo charges a processing fee of 2 percent of the sanctioned loan amount, and it is non-refundable regardless of whether the loan is approved, rejected, or withdrawn. On a large sanction that is a meaningful sum at risk, so the order of operations matters: confirm your rate, spread, and tenure and run the numbers before you pay the fee, never the other way around. The one fee that works in your favour is foreclosure, which Auxilo does not charge, so you can prepay the loan early without penalty.

What does an Auxilo education loan cover, and which countries?

Auxilo covers the full range of education expenses: tuition, examination fees, living costs, travel, pre-admission costs, and other course-related costs, with no margin money required. It lends across more than 25 countries, including the United States, Canada, the United Kingdom, Germany, Ireland, Australia, Singapore, New Zealand, the United Arab Emirates, France, the Netherlands, Switzerland, Spain, and Sweden, as well as for study within India. Confirm the current covered-country list and any destination-specific conditions on auxilo.com, because the unsecured terms vary by country.

How is Auxilo different from a PSU bank like SBI?

The trade-off is the same one that defines every NBFC against a PSU bank. Auxilo lends larger amounts unsecured, asks for no margin money, accepts multiple and irregular-income co-applicants, and sanctions faster, which suits families with no collateral or a tight deadline. A PSU bank like SBI is cheaper, starting two to four percentage points lower, and can carry a central interest subsidy, but it caps unsecured lending at ₹7.5 lakh, demands collateral above that, and processes slowly. If you can pledge collateral and have time, the PSU route usually wins on cost, so use Auxilo when speed or the absence of collateral genuinely makes the bank route impossible.

What documents does Auxilo need?

Auxilo leans on the co-applicant, so it wants the co-applicant’s income proof, income tax returns, and bank statements alongside the student’s admission letter, the program cost breakdown, and standard KYC such as Aadhaar and PAN for both. For a self-employed co-applicant it will assess the business returns and repayment capacity, which is one of its strengths, and for a secured loan it additionally needs the property documents and a valuation. A clean, complete co-applicant file is what drives the fast sanction the NBFC is known for, and the full checklist is in the documents required for education loan post.

Faz · The Honest Journey · 2026