An Avanse education loan is an unsecured loan from one of India’s major dedicated education-financing NBFCs, sanctioning up to around ₹50 lakh to 75 lakh for strong profiles against a co-applicant’s income, at an interest rate band of roughly 11.5 to 13.5 percent with a processing fee near 1 to 2 percent. It is quicker and more flexible on profile than a PSU bank, but it carries no central interest subsidy, so over a long repayment it costs noticeably more than a collateral-backed PSU loan. The 80E interest deduction does apply. Always confirm the exact rate and fee on your sanction letter, because these numbers change.

I sat with a family last year whose daughter had an admit for a Master’s in Canada and a father whose salary was solid but whose only asset was the flat they lived in, which they were not willing to pledge. The PSU branch was polite and immovable: above ₹7.5 lakh, no collateral, no loan. Avanse looked at the father’s salary slips and tax returns, ran the daughter’s program, and sanctioned an unsecured loan that got her there. The family was grateful and rightly so. They also paid a rate that, over the repayment, will cost them more than a secured PSU loan would have. Both of those things are true at once, and that is the honest frame for this lender.

This post is what an Avanse education loan really is, the worked cost against a PSU loan, and the plain list of who it fits and who it does not. No endorsement, no sales tone, just the conversation I would want a family to have before signing.

To compare this NBFC against the alternatives: the PSU bank vs NBFC education loan post, the MPOWER financing education loan post, and the prodigy finance education loan post.

What Avanse actually is

Avanse is a non-banking financial company, an NBFC, focused on education financing. Like the other dedicated education-loan NBFCs, such as the Auxilo education loan and the InCred education loan, it does not run a general banking business; it underwrites students and families. That single focus shapes the product. It lends larger unsecured amounts than a PSU bank, moves faster, and is more flexible on the kind of income profile it will accept, in exchange for a higher rate and a place outside the government’s interest subsidy scheme.

The four levers that separate any NBFC from a PSU bank are collateral, rate, speed, and the central interest subsidy. Avanse, like HDFC Credila, lends unsecured well above the PSU ceiling, sanctions quickly, and accepts profiles a bank might decline, but it charges more and its loans generally sit outside the subsidy. The mirror-image PSU loan is cheaper and subsidy-eligible but slower and collateral-hungry above ₹7.5 lakh. If you want the full structure of Indian education loans before narrowing to one lender, the education loan India complete guide covers the whole field.

How much Avanse lends, and on what basis

The reason families come to Avanse is the unsecured ceiling. Where a PSU bank stops unsecured lending at ₹7.5 lakh, Avanse will sanction unsecured up to roughly ₹50 lakh, and for very strong profiles at premier programs higher, toward ₹75 lakh. It also offers secured loans against property for larger amounts, but the unsecured appetite is the headline draw.

That sanction is built on the co-applicant. Avanse underwrites the parent or guardian’s income, repayment capacity, and credit history, together with the quality of the program and university the student is admitted to. A clean CIBIL above 750, stable demonstrable income, and a solid admit are what unlock the larger unsecured numbers. For a weaker co-applicant income or a lower-ranked program the unsecured ceiling falls quickly, which is the honest counterweight to the headline figure. The market-wide view of how far any lender will go, and where the unsecured walls sit, is in the maximum education loan amount in India post.

The rate, the fee, and the real cost

Avanse’s interest rate typically lands in the band of 11.5 to 13.5 percent, set per profile and reviewed periodically, plus a processing fee usually around 1 to 2 percent of the sanctioned amount. The rate you actually get depends on the co-applicant strength, the program, and the prevailing rate environment, so any single number online is indicative only.

The honest comparison is with a PSU secured loan, which runs at a floating rate closer to 9.5 to 11 percent. That two to three percentage point spread looks minor and is not, once you apply it to a large loan over a long repayment. The 80E income tax deduction on education loan interest does apply to loans from notified NBFCs, and Avanse qualifies, so part of the interest returns as a tax benefit during the eight-year window. The mechanics are in the education loan tax benefit Section 80E post. What 80E does not do is close the gap with a PSU loan, because the PSU borrower claims the same deduction on lower interest. To compare these bands across the market, see the education loan interest rate comparison post.

Faz's ruleThe unsecured sanction is what you are buying. The higher rate is the price. Make sure you actually need the unsecured part before you pay for it.

Plenty of families with a pledgeable asset drift to an NBFC because the process feels lighter and the sanction arrives faster. If you have collateral and time, that convenience can quietly cost you several lakh in extra interest. The NBFC premium earns its keep when you genuinely have no collateral and a real deadline, not when you simply want to skip the paperwork.

The worked INR example, Avanse versus a PSU secured loan

Take a real-shaped case. A student needs ₹35 lakh of funding for a Master’s abroad. The family will not, or cannot, pledge property, so the realistic choice is an Avanse unsecured loan at, say, 12.75 percent versus a PSU secured loan at 10 percent if collateral could be arranged. Assume a ten-year repayment in both cases for a clean comparison.

| Item | Avanse (NBFC unsecured) | PSU (secured) |

|---|---|---|

| Loan amount | ₹35,00,000 | ₹35,00,000 |

| Indicative interest rate | ~12.75% | ~10.0% |

| Tenure | 10 years | 10 years |

| Approx EMI | ~₹51,600 | ~₹46,250 |

| Approx total interest paid | ~₹26.9 lakh | ~₹20.5 lakh |

| Processing fee (~1.5%) | ~₹52,500 | Often lower or capped |

| Central interest subsidy (CSIS) | Not available | Available if eligible |

The interest gap is roughly ₹6.4 lakh over the life of the loan, before the processing fee or the forgone subsidy. That is the price of the unsecured convenience. It does not make Avanse the wrong choice. It makes it a considered one. If the family truly cannot pledge collateral and the program needs funding now, that extra interest is the cost of getting the student there at all, and it can be entirely justified. If the family could have pledged a property and simply preferred to avoid the process, that ₹6.4 lakh is avoidable money. If the whole reason you are here is the no-collateral route, read the education loan for abroad studies without collateral post, which weighs the unsecured option across every lender.

Faz's ruleGet the exact rate, fee and tenure in writing and run the total-interest line yourself before signing. A small rate difference hides a large rupee gap over a decade.

The band you read online is not the rate on your sanction letter. Ask for the precise figure, the processing fee and the tenure, then put them through an EMI calculator. The total interest paid is the number that decides whether the NBFC premium is worth it, and it is the number nobody offers up unprompted.

Speed and flexibility, the genuine upside

Avanse earns its place on turnaround and on the profiles it will accept. A secured PSU loan means property valuation, legal vetting, and weeks of branch work, while an NBFC underwriting mainly on the co-applicant’s documents can sanction in days when the file is clean. For a student against a deposit deadline or a visa timeline, that speed can decide whether they make the intake or lose a year.

It is also more flexible on income shape. A self-employed parent with strong but lumpy income, the profile a PSU credit officer treats cautiously, is exactly what an NBFC is built to assess. Avanse will look at the business, the returns, and the repayment capacity and lend where a bank hesitates. For the families it is designed for, that flexibility is real value, not marketing.

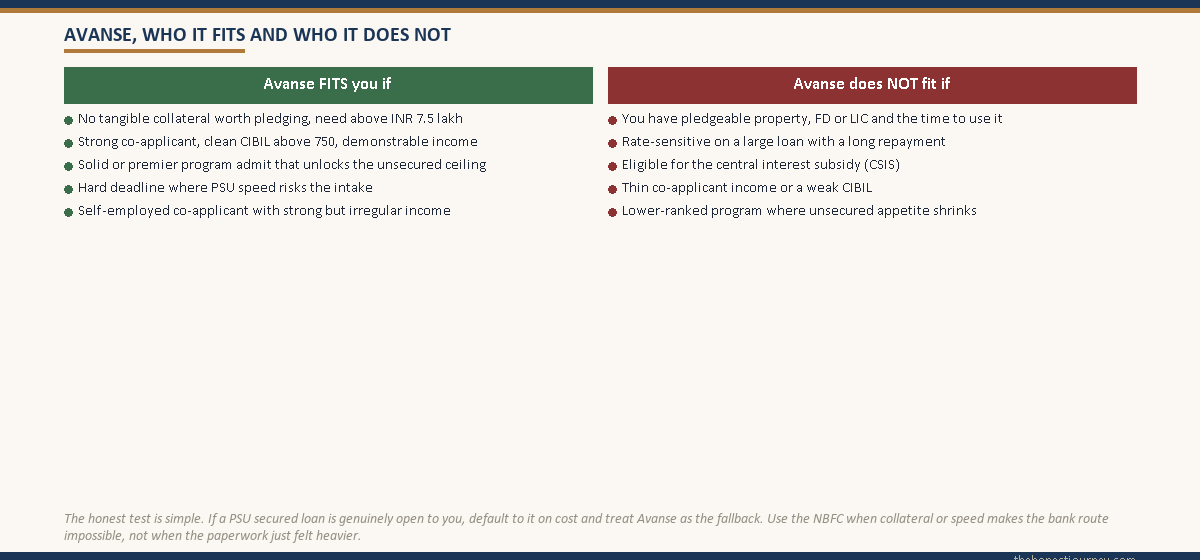

Who an Avanse loan genuinely fits

Here is the honest fit, stated plainly. An Avanse loan fits when several of these hold together:

- You have no tangible collateral worth pledging and you need an amount well above the ₹7.5 lakh PSU unsecured ceiling.

- You have a strong co-applicant with a clean CIBIL above 750 and demonstrable income, since that is what the unsecured sanction rests on.

- The student has a solidly ranked or premier program admit, which unlocks the larger unsecured numbers.

- You face a hard deadline where PSU processing speed is a genuine risk to the intake.

- The co-applicant is self-employed with strong but irregular income that a PSU bank struggles to assess.

Who it does NOT fit

This is the section worth reading twice. An Avanse loan is the wrong choice when:

- You have a pledgeable property, FD, or LIC and the time to arrange a secured PSU loan. The collateral route at a lower rate saves several lakh in interest, and it costs you only paperwork.

- You are rate-sensitive and the loan is large with a long repayment, because the NBFC premium compounds over years into a serious sum.

- You qualify for the central interest subsidy, which applies to scheduled-bank loans and generally not to NBFC loans. Surrendering the subsidy to save time is rarely worth it.

- Your co-applicant income is thin or the CIBIL is weak, in which case the unsecured sanction is either small or priced at the top of the band, and the value evaporates.

- The program is lower ranked, where the unsecured appetite shrinks and the headline amount may not materialise.

The cleanest test is the same for any NBFC: if a PSU secured loan is genuinely available to you, default to it on cost, and treat Avanse as the fallback for when collateral or speed makes the PSU route impossible. Avanse and HDFC Credila are close cousins in profile, so if you are choosing between the two, get a sanction quote from each and compare the exact rate, fee, and tenure rather than the marketing. The companion HDFC Credila education loan post covers that lender on the same honest terms.

Where Avanse sits in the rulebook

Avanse operates as an NBFC under the Reserve Bank of India’s regulatory framework, and the current NBFC rules and registration details are on the RBI site. The model educational loan scheme that PSU banks follow, which frames the subsidy and collateral conventions Avanse sits outside of, is published by the Indian Banks’ Association. Reading the IBA scheme is the quickest way to see exactly what the PSU route gives you that the NBFC route does not, which is the comparison this whole post turns on. If the subsidy is the deciding factor for your family, the detail of claiming it is in the CSIS interest subsidy how to claim post.

The honest take

Avanse is a serious, focused education-financing NBFC. For a family with no usable collateral, a strong co-applicant, a good admit, and a deadline, it is often the realistic way to fund a large abroad loan, and the speed and flexibility genuinely earn the premium. That is an honest use case and the relief it brings is real.

But it is not the cheap option and it is not the default. The rate premium over a PSU secured loan is two to three percentage points, which becomes several lakh of extra interest over a long repayment, and you forgo the central interest subsidy. If you can pledge collateral and you have time, a PSU bank costs you less. Use Avanse when the unsecured speed is the thing you actually need. Get the total-interest number on the real sanction letter, set it against a PSU quote and an Avanse-versus-Credila quote, and sign with the gap in front of you, not behind you.

FAQ

What is Avanse and is it a bank?

Avanse is a non-banking financial company, an NBFC, focused on education financing, and it is one of the major dedicated education-loan lenders in India. It is not a bank and does not run general banking services. The practical effect is that it lends unsecured at higher amounts and faster than a PSU bank, but at a higher interest rate and generally without the central interest subsidy that scheduled-bank loans can carry. Treat it as an NBFC product, with the trade-offs that label implies.

How much can I borrow from Avanse without collateral?

Avanse will sanction unsecured up to roughly ₹50 lakh for strong profiles, and for very strong co-applicants at premier programs higher, toward ₹75 lakh. The sanction rests on the co-applicant’s income, credit history, and the quality of the program and university. A clean CIBIL above 750 and demonstrable income unlock the larger numbers, while a weaker co-applicant or a lower-ranked program reduces the unsecured ceiling considerably. Always confirm the exact sanctioned amount on the letter rather than relying on the headline figure.

What interest rate does Avanse charge?

Avanse’s interest rate typically sits in the band of roughly 11.5 to 13.5 percent, set per profile and reviewed periodically, plus a processing fee of around 1 to 2 percent of the sanctioned amount. The exact rate depends on the co-applicant strength, the program, and the rate environment, so any single online figure is only indicative. This band runs two to three percentage points above a typical PSU secured loan, which is the core trade-off to weigh before choosing the NBFC route over a bank.

Does Avanse qualify for the 80E tax deduction?

Yes. The Section 80E income tax deduction on education loan interest applies to loans from banks and notified NBFCs, and Avanse qualifies, so you can claim the interest deduction for up to eight years. However, 80E does not close the cost gap with a PSU loan, because the PSU borrower claims the same deduction on their lower interest. Treat 80E as a benefit available on both routes rather than a reason to prefer the NBFC over a bank.

Does Avanse get the central interest subsidy?

Generally no. The central interest subsidy schemes apply to education loans from scheduled commercial banks under the IBA model scheme, and NBFC loans like Avanse’s typically fall outside them. If you are eligible for the subsidy on income or category grounds, surrendering it to take a faster NBFC loan is rarely worth the cost. Check your eligibility for the subsidy on a scheduled-bank loan before defaulting to an NBFC, because the subsidy can meaningfully reduce the effective cost of a PSU loan.

Is Avanse faster than a PSU bank?

Usually yes. Because Avanse underwrites mainly on the co-applicant’s documents rather than on collateral valuation and legal vetting, a clean file can be sanctioned in days rather than weeks. For a student facing a deposit deadline or a visa timeline that will not wait, that speed can be the difference between making the intake and deferring a year. The speed is genuine value, but it comes with the higher rate, so weigh both together rather than choosing on turnaround alone.

Avanse or HDFC Credila, which is better?

They are close cousins in profile: both are dedicated education-loan NBFCs lending unsecured well above the PSU ceiling, at similar rate bands, with no central interest subsidy and 80E applicable. There is no universal winner. Get a sanction quote from each and compare the exact interest rate, processing fee, and tenure on the actual letters, because the better deal for your specific co-applicant and program is the one that comes back cheaper on total interest, not the one with the better marketing.

What documents does Avanse need?

Avanse leans heavily on the co-applicant, so it wants the co-applicant’s income proof, income tax returns, bank statements, and a credit report, alongside the student’s admission letter, the program cost breakdown, and standard KYC for both. For self-employed co-applicants it assesses the business returns and repayment capacity, which is one of its strengths. For secured loans it additionally needs property documents and a valuation. A clean, complete co-applicant file is what drives the fast sanction the NBFC is known for.

Faz · The Honest Journey · 2026