An InCred education loan is an unsecured loan from InCred Finance, the NBFC, that will fund the full certified cost of your course, collateral-free up to a high amount, against a co-applicant’s income. The convenience is real and the foreclosure terms are genuinely good, charged with no prepayment penalty. The catch is the price and the uncertainty: InCred does not publish a fixed rate, the rate is floating and risk-graded to your profile, and the processing fee runs about 1 to 1.5 percent on provisional approval. So it is faster and more flexible than a PSU bank, but it costs more than a secured PSU loan. Confirm your exact reducing-balance rate, the reset terms, and the collateral-free limit on your sanction letter, because that is where the real cost hides.

A reader messaged me last winter, two weeks from a fee deadline and out of patience. He had an admit to a one-year Master’s in Ireland, no property the family wanted to pledge, and a father whose income was strong but self-employed and awkward for a bank to read. A PSU branch had stalled him for a month. Someone pointed him at InCred, told him it was collateral-free and quick, and quoted him a rate that sounded fine. The sanction was indeed quick. The rate on the letter was not the rate he had been told, it was floating, and he had not understood the processing fee was a percentage of the whole loan until he saw the number.

This post is the honest picture of what an InCred education loan actually is, who it genuinely fits, and where the cost sits that the brochures gloss over. I do not earn a rupee if you borrow from InCred or from anyone else. This is the conversation I would have with that reader before he signed, not after.

To compare this NBFC against the alternatives: the leap finance education loan post and the auxilo education loan post.

What InCred actually is, and which InCred

First, clear up the name, because there are several InCreds and people borrow from the wrong mental model. The lender here is InCred Financial Services Limited, an NBFC registered with the Reserve Bank of India, formerly known as KKR India Financial Services. That is the entity that lends you the money. It is not InCred Money or InCred Wealth, which are the investment platforms, and it is not InCred Capital, which is the investment bank. When I say InCred in this post I mean InCred Finance, the NBFC, the one whose education loan you sign for.

InCred Finance, the NBFC, offers personal loans, business loans, and education loans. The education loan is a focused product that funds students against a co-applicant’s income, the same broad category as HDFC Credila, Avanse, or Auxilo: a lender that underwrites the student and the family rather than a bank with a loan desk on the side. That focus is the whole character of the product. It moves faster than a PSU bank, it is friendlier to irregular income, it lends collateral-free at higher amounts, and in exchange it charges more.

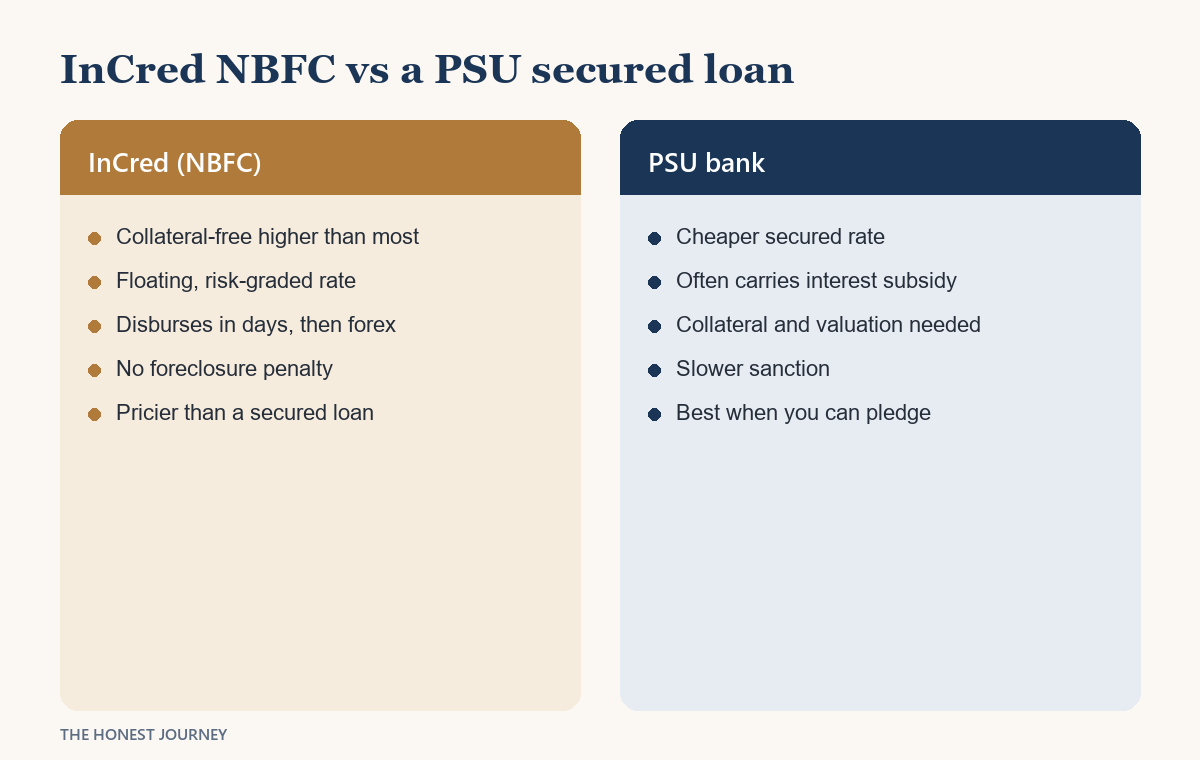

The practical difference between an NBFC like InCred and a PSU bank comes down to four things: collateral, rate, speed, and the central interest subsidy. An NBFC lends bigger amounts unsecured, sanctions faster, and is more flexible on profile, but it charges a higher rate and its loans generally sit outside the government’s interest subsidy scheme. A PSU bank is the mirror image, cheaper and subsidy-eligible, but slower and collateral-hungry above ₹7.5 lakh. If you want the full landscape before you narrow to one lender, the education loan India complete guide lays out the whole field, and the PSU bank versus NBFC education loan post is the single most useful thing to read alongside this one.

The headline that draws people in

InCred’s appeal is real, so let me state it fairly before I get to the price. It lends collateral-free up to a high ceiling, reported around ₹1.5 crore for strong profiles, which is far above the PSU unsecured wall of ₹7.5 lakh. Collateral is optional rather than mandatory, and providing it can earn you a better rate or a higher amount, but the unsecured appetite is why most people come to InCred in the first place.

The loan is sized to the full cost of attendance certified by your school for all years, minus any scholarships or grants. That covers tuition, fees, housing, meals, books and a laptop, travel, insurance, and incidentals, which is the whole spread a student actually spends, not just tuition. It lends across the usual abroad destinations, including the United States, Canada, Australia, Germany, Ireland, New Zealand, Singapore, Hong Kong, and the Netherlands, as well as study within India. Course levels run from bachelor through master’s to doctoral, and certifications and diplomas are eligible too.

For a student with no collateral and a hard deadline, that combination is genuinely valuable. The question is never whether InCred can fund you. It usually can. The question is what that funding costs, and whether you are actually buying the part you need.

How InCred’s interest rate really works

This is the section the brochures skip, so read it twice. InCred does not publish a fixed interest rate range the way a PSU bank publishes its card rate. InCred’s rate is floating, and it is completely risk-graded, set against the student’s scholastic performance, the future potential to repay, the co-applicant’s credit history and employment, and any security provided. Two students at the same university can be quoted different rates because their files are different.

So when you see a confident single percentage on an aggregator site, treat it with suspicion. Those numbers are not published by InCred. They are estimates, and because the rate is individual to your profile, they disagree with each other. The only number that means anything is the one InCred puts on your sanction letter, and the only structure that matters is whether it is quoted on a reducing balance. Ask for that explicitly, because a rate that sounds reasonable on a flat basis is far more expensive than the same number on reducing balance.

The second thing to understand is that the rate floats. It moves with InCred’s benchmark. If the benchmark rises, your rate rises, and either your EMI climbs or your tenure stretches. That is normal for an NBFC, but it means the number you sign is a starting point, not a fixed cost for the life of the loan. A PSU secured loan also floats, but it typically starts two to four percentage points lower, and over a long repayment that gap is large. Because I cannot confirm a specific rate range on InCred’s own pages, I will not print one. Confirm yours in writing.

Faz's ruleInCred does not publish a fixed rate, so the only rate that exists for you is the one on your sanction letter. Ask the relationship manager three direct questions: what is my reducing-balance rate, what is it graded against, and how often can it reset? If any answer is vague, that vagueness is the product.

Every NBFC that risk-grades its rate has an incentive to keep the number soft until you are committed. Pin it down. Get the reducing-balance rate, the reset frequency, and the processing fee in writing on the same page, then run the total-interest number yourself. The line nobody volunteers is the total interest over the full tenure, and it is the only line that decides whether this loan is worth it.

The fees you should know about

InCred’s fee structure has one genuine advantage and one thing to watch, and you should know both.

The advantage is foreclosure. InCred allows you to foreclose or prepay the loan at any point with no additional penalty or charge. On a floating-rate loan that is worth having, because prepaying is your main defence against a rising rate. If you come into money, a bonus, a windfall, or a higher salary after the course, you can throw it at the principal and shrink the loan without a penalty eating the benefit. That is a real, borrower-friendly feature and I will give InCred full credit for it.

The thing to watch is the processing fee. InCred charges a processing or administration fee of about 1 to 1.5 percent of the loan amount. The good news is it is not an upfront fee: it is payable only upon provisional loan approval, so you are not paying it just to apply. The honest caution is that on a large sanction even 1.5 percent is a meaningful sum. On a loan of ₹40 lakh that is up to ₹60,000. Confirm the exact percentage and the precise point at which it becomes payable, and confirm in writing what happens to it if the loan is later withdrawn or does not disburse, because those terms vary and you want them clear before, not after.

Collateral, co-applicant, and the structure

InCred treats collateral as optional. You can take the loan fully unsecured up to its collateral-free ceiling, or you can pledge security to push the rate down or the amount up. So the first decision is not your rate but your route: do you actually need the unsecured option, or do you have collateral you could pledge anyway? Because if collateral is on the table, a PSU secured loan at a lower rate becomes the obvious benchmark to compare against.

The co-applicant is the spine of the sanction. InCred generally requires one or both parents to co-sign, and in certain circumstances other blood relations, a sibling or a spouse, may qualify. The co-applicant should be an income-earning family member willing and able to take on repayment, with an operative Indian rupee bank account. As with every NBFC, the strength of that co-applicant file, the income, the credit history, the stability, is what drives both the approval and the rate you are offered. A thin or shaky co-applicant pushes the rate to the top of InCred’s risk band, which is exactly where the value disappears.

On structure: for master’s and graduate loans, EMIs begin after a moratorium of up to 36 months from the first disbursement, though interest or part of it may need to be serviced during the in-school period, so confirm whether yours is a full or partial moratorium. The total repayment tenure runs 5 to 12 years, up to a maximum of 15. Disbursement is roughly 5 days after approval, plus another 3 to 5 days for forex conversion and the international transfer, so InCred itself recommends starting 12 to 14 days before any fee-payment deadline. If the absence of collateral is your whole reason for considering InCred, read the education loan for abroad studies without collateral post alongside this one, because it weighs the unsecured route across every lender, not just this one.

The worked INR example, InCred versus a PSU secured loan

Take a real-shaped case. A student needs ₹40 lakh for a Master’s abroad. The family has no property it wants to pledge, so the realistic choice is an InCred unsecured loan against a PSU secured loan if collateral could be arranged. InCred does not publish a rate, so I have used an indicative 13 percent purely to show the shape of the gap, and you must replace it with the actual rate on your own sanction letter. The PSU secured rate is indicative at 10 percent. Assume a ten-year repayment in both cases for a clean comparison.

| Item | InCred (NBFC unsecured) | PSU (secured) |

|---|---|---|

| Loan amount | ₹40,00,000 | ₹40,00,000 |

| Indicative interest rate | ~13.0% (floating, risk-graded, confirm yours) | ~10.0% (floating) |

| Tenure | 10 years | 10 years |

| Approx EMI | ~₹59,700 | ~₹52,860 |

| Approx total interest paid | ~₹31.6 lakh | ~₹23.4 lakh |

| Processing fee (~1 to 1.5%) | ~₹40,000 to 60,000, on provisional approval | Often lower or capped |

| Central interest subsidy | Generally not available | Available if eligible |

The interest gap alone is roughly ₹8 lakh over the life of the loan in this illustration, before you count the processing fee or the lost subsidy. That is the real price of the unsecured convenience. It does not make InCred wrong. It makes InCred a considered choice rather than a default. If the family genuinely cannot pledge collateral and the program needs funding now, that extra interest is the cost of getting the student there at all, and it can be entirely worth it. If the family could have pledged a property and simply did not want the paperwork, that gap is avoidable. And remember the number above uses an assumed rate: your true gap depends entirely on the figure on your letter. To see how these rate bands stack across the whole market, the education loan interest rate comparison post puts PSU, private bank, and NBFC rates side by side.

Faz's ruleRun the total-interest number on your actual sanction letter, not on a website estimate, and do it before you commit. A two to three percent rate difference is a small number that hides a very large rupee gap over ten years, and with a floating risk-graded rate that gap can widen.

The rate band you read online is not the rate on your sanction letter, because InCred does not publish one. Get the exact reducing-balance rate, the fee, and the tenure in writing, put them through an EMI calculator yourself, and only then decide. The order matters: confirm, then commit, never the reverse. The foreclosure freedom is your friend here, so plan to prepay whenever you can.

Speed and flexibility, the genuine upside

Where InCred earns its keep is turnaround and flexibility, the same place every good NBFC does. A secured PSU sanction means valuation visits, legal vetting of the property, and weeks of branch back-and-forth. InCred, underwriting mainly on the co-applicant’s documents, can move much faster when the file is clean, with application processing in roughly five working days and disbursement following soon after. For a student staring at a deposit deadline or a visa timeline that will not wait, that speed is not a luxury, it is the difference between making the intake and deferring a year.

It is also more flexible on profile. A self-employed parent with strong but irregular income, exactly the file a PSU credit officer treats with suspicion, is the profile an NBFC is built to underwrite. InCred will look at the business, the returns, and the repayment capacity and lend where a bank hesitates. The collateral-free ceiling well above the PSU wall, and the full cost-of-attendance sizing, mean a student can fund tuition and living costs in one sanction rather than scraping together a top-up later. That flexibility is real value for the families it is designed for.

What borrowers actually complain about

I will not name-and-shame, and I will not pass off anonymous review-site sentiment as fact. But there are recurring themes in borrower feedback worth raising honestly, because they are about the part of the relationship that starts after the sanction, when the agent has moved on. Some borrowers report that the effective rate or the fee felt higher than they expected once the loan ran its course, some report documentation that felt heavy and repetitive, and some report firm collection calls when an EMI slipped. None of this is unique to InCred and none of it makes InCred a bad lender. NBFC rates float and are risk-graded, documentation is thorough because the loan is unsecured, and collection follow-up is what every regulated lender does. The lesson is defensive, not damning. For each theme, the constructive tip is the same shape: get the reducing-balance rate and reset terms in writing so the effective cost holds no surprise, assemble the full document set once so you are not chasing paper twice, and never let an EMI bounce, because a clean record is your best protection. Forewarned is the entire point.

InCred versus PSU versus the other NBFCs and no-cosigner lenders

InCred does not exist in a vacuum, so place it on the map before you sign. Against a PSU bank, the trade-off is the familiar one: InCred is faster, collateral-free at a far higher ceiling, and friendlier to irregular income, but it costs more and generally forgoes the central interest subsidy. The natural PSU benchmark to compare any InCred quote against is in the SBI education loan for abroad studies post.

Against the other dedicated education-loan NBFCs, InCred sits in the same bracket as HDFC Credila, the largest of them, and Avanse. The honest move here is to get quotes from at least two of them on the same file, because the rate is profile-specific and one will usually beat the others for your particular co-applicant and program. Do not assume any single NBFC is cheapest for you. Make them compete.

And if your real problem is that you have no Indian co-applicant at all, InCred is not your lender, because it requires one. That is the territory of the no-cosigner lenders that underwrite the student’s future earnings instead, covered in the MPower Financing and Prodigy Finance reviews. They cost more again, but they solve a problem InCred cannot.

Who an InCred loan genuinely fits

Being honest about fit is the whole point of this site, so here it is plainly. An InCred loan fits you when several of these are true at once:

- You have no tangible collateral to pledge, or none worth the legal and valuation hassle, and you need an amount well above the ₹7.5 lakh PSU unsecured ceiling.

- You have a strong income-earning co-applicant, typically a parent, with clean credit and demonstrable income, because that is what the unsecured sanction rests on.

- The student has a solid program admit, which is what unlocks a better grade on the risk-graded rate.

- You are against a hard deadline and PSU processing speed is a genuine risk to making the intake.

- Your co-applicant is self-employed with strong but irregular income that a PSU bank struggles to assess.

- You expect to be able to prepay, because InCred’s no-penalty foreclosure lets you shorten a floating-rate loan whenever cash allows.

Who it does NOT fit

This is the section the agents skip, so read it twice. An InCred loan is the wrong choice when:

- You have a pledgeable property, FD, or LIC and the time to arrange a secured PSU loan. The collateral route at a lower rate will save you several lakh in interest, and the only thing it costs you is paperwork.

- You are rate-sensitive and the loan is large with a long repayment, because a floating, risk-graded rate compounds over years into a serious sum and you cannot lock a published number in advance.

- You qualify for the central interest subsidy, which applies to scheduled-bank loans and generally not to NBFC loans. Giving up the subsidy to save paperwork is rarely worth it.

- Your co-applicant income is thin or credit is weak, in which case the rate climbs to the top of the band and the value disappears.

- You have no eligible Indian co-applicant at all, in which case InCred cannot fund you and a no-cosigner lender is the route to look at instead.

The cleanest mental test: if a PSU secured loan is genuinely available to you, default to it on cost, and treat InCred as the fallback for when collateral or speed makes the PSU route impossible. Compare any InCred quote both against the PSU benchmark and against at least one other NBFC, and gather the paperwork early using the documents required for education loan post so a clean file gets you the better rate.

Where InCred sits in the rulebook

InCred Financial Services Limited operates as an NBFC under the Reserve Bank of India’s regulatory framework. It is an RBI-registered NBFC; confirm the exact registration number on InCred’s own RBI disclosure page rather than relying on a number quoted elsewhere, and the current NBFC rules sit on the RBI site. If a grievance is not resolved by InCred’s own redressal process, it escalates to the RBI Ombudsman under the Reserve Bank’s Integrated Ombudsman Scheme, which is the formal route every regulated lender’s customer has and which is worth knowing exists before you need it. The product facts in this post, the collateral-free terms, the fee, the moratorium, the tenure, and the country list, are published on InCred’s own site at incred.com, and you should confirm the live numbers there and on your sanction letter, because they move.

The honest take

InCred Finance, the NBFC, is a serious education-loan lender that will fund the full certified cost of your course, collateral-free at a high ceiling, against a co-applicant’s income, and let you prepay with no penalty. For a family with no collateral, a strong co-applicant, and a deadline, that is a genuinely useful product, and the speed and flexibility are worth paying for when they are the thing you actually need.

But it is not the cheap option, and there is no advertised rate to anchor to. Your rate is floating and risk-graded, you only see it on the sanction letter, and the processing fee of 1 to 1.5 percent is real money on a large loan. If you can pledge collateral and you have time, a PSU bank will likely cost you several lakh less over the life of the loan, and it may carry an interest subsidy InCred cannot. Use InCred when the collateral-free speed is the thing you need, not because the paperwork felt lighter. Confirm the reducing-balance rate, the reset terms, and the collateral-free limit in writing, run the total-interest number yourself, compare it against a PSU quote and one other NBFC, and sign with the real cost in front of you, not behind you.

FAQ

What is the interest rate on an InCred education loan?

InCred does not publish a fixed interest rate range. Its rate is floating and completely risk-graded, set against the student’s scholastic performance, the future potential to repay, and the co-applicant’s credit and employment, so two students at the same university can be quoted different rates. Any single percentage you see on an aggregator site is an estimate, not an InCred-published figure, and the only number that means anything is the reducing-balance rate on your own sanction letter. Ask for that rate, what it is graded against, and how often it can reset, all in writing, before you commit.

Is InCred a bank or an NBFC, and which InCred is it?

The lender is InCred Financial Services Limited, a non-banking financial company registered with the Reserve Bank of India, formerly known as KKR India Financial Services. It is not a bank, and it is not InCred Money or InCred Wealth, which are investment platforms, nor InCred Capital, the investment bank. As InCred Finance, the NBFC, it offers personal, business, and education loans. Being an NBFC means bigger collateral-free amounts and faster sanctions than a PSU bank, but at a higher rate and generally without the central interest subsidy, so the question is cost and fit rather than safety.

Does InCred give collateral-free education loans, and up to how much?

Yes. InCred treats collateral as optional and lends unsecured up to a high ceiling, reported around ₹1.5 crore for strong profiles, far above the PSU unsecured wall of ₹7.5 lakh. Providing collateral is not required, but it can earn a better rate or a higher amount, and partial collateral is accepted in some cases. Confirm the exact collateral-free limit for your country and profile with the lender, because the figure quoted online varies and the real number is the one on your sanction. If collateral is available to you anyway, compare a PSU secured loan first.

What is InCred’s processing fee, and when is it charged?

InCred charges a processing or administration fee of about 1 to 1.5 percent of the loan amount. The borrower-friendly part is that it is not an upfront fee: it is payable only upon provisional loan approval, so you are not paying just to apply. On a large sanction even 1.5 percent is a meaningful sum, so confirm the exact percentage, the precise point at which it becomes payable, and what happens to it if the loan is later withdrawn. The fee that works in your favour is foreclosure, which InCred does not charge, so you can prepay the loan at any time without penalty.

What does an InCred education loan cover, and which countries?

InCred sizes the loan to the entire cost of attendance certified by your school for all years, minus scholarships and grants, covering tuition, fees, housing, meals, books and a laptop, travel, insurance, and incidentals. It lends across major destinations including the United States, Canada, Australia, Germany, Ireland, New Zealand, Singapore, Hong Kong, and the Netherlands, as well as for study within India, at bachelor, master’s, and doctoral levels, with certifications and diplomas eligible. Confirm the current covered-country list and any destination-specific conditions with the lender, because terms can vary by country.

What is the moratorium and repayment tenure on an InCred loan?

For master’s and graduate loans, EMIs begin after a moratorium of up to 36 months from the first disbursement, though interest or part of it may need to be serviced during the in-school period, so confirm whether yours is a full or partial moratorium. The total repayment tenure runs 5 to 12 years, up to a maximum of 15. Disbursement is roughly 5 days after approval, plus another 3 to 5 days for forex conversion and the international transfer, which is why InCred recommends starting the process 12 to 14 days before any fee-payment deadline.

Should I choose InCred or a PSU bank?

If a PSU secured loan is genuinely available to you, with collateral to pledge and time to process it, default to the PSU bank on cost, because the lower rate saves several lakh over a long repayment and may carry the central interest subsidy. Choose InCred when you have no usable collateral, a strong income-earning co-applicant, a good admit, and a deadline that PSU processing would put at risk. Because InCred’s rate is risk-graded and unpublished, also get a quote from at least one other NBFC on the same file and compare, rather than assuming InCred is cheapest for your profile.

Faz · The Honest Journey · 2026