Studying abroad is worth it only with a clear career destination, a funding plan that does not bet the family home, and a realistic work or PR pathway. It is not worth it as a status purchase or an escape. For roughly half the readers who write to me, a strong Indian degree plus exposure later wins. Start with why you are going, then run the 7-question framework in this guide.

Every week I get the same message in some form. “Faz, I have an offer from a university in Canada (or the UK, or Germany, or Australia). My parents are willing. The agent says I will get PR in three years. Should I go?” The honest answer is that I do not know, and neither does the agent, and neither do your parents. What I do know is the shape of the decision, the questions that separate the people for whom this works out from the people who come back at 26 with ₹40 lakh of debt and a story that did not land the way they thought it would.

This guide is the page I wish someone had handed me, and the page I now hand to every reader who emails me before they sign a single university acceptance. It will not tell you to go. It will not tell you not to go. It will give you the framework to decide honestly.

Studying abroad is worth it only if you have a clear career destination (not just “go abroad”), a workable funding plan that does not bet the family home on a single outcome, and a realistic post-study work or PR pathway in your target country. It is not worth it as a default route after Class 12, as a status purchase, or as an escape from a problem at home. For roughly half the readers who write to me, the honest answer is that the same money invested in a strong Indian degree plus international exposure later will produce a better life.

What this guide covers: why you are actually going, the honest ROI math, when to go, which country fits which profile, destination snapshots with work and PR data, the loan vs self-funding decision, the during-study reality, the after-study reality of return or stay, red flags that should make you say no, and a 7-question decision framework you can run in one evening.

1. The question to answer first: why are you actually going?

Before any conversation about countries, courses, costs, or loans, sit with this one question for a week. Not in your head. On paper. Write the answer down. Read it back to yourself the next morning. Is it still true?

In ten years of watching people make this decision, I have seen the same handful of real reasons come up. A specific career outcome that genuinely requires a foreign degree or foreign work experience (research roles tied to a particular lab, certain finance and tech roles in specific geographies, healthcare regulated by foreign licensing). A clear pathway to permanent residency in a country where you have looked at the actual immigration rules and feel the trade-off is right for the life you want. An academic program with a depth, faculty, or industry connection you cannot get at any institution in India.

I have also seen the reasons that do not survive contact with reality. “Everyone in my batch is going.” “My agent said it is the best time.” “I want to escape family pressure for a few years.” “My parents will be proud.” “I do not know what to do after graduation, so I will do a master’s abroad and figure it out.” Every one of those reasons can produce a sanction letter. None of them will pay your EMI.

The test I use with readers: if your foreign degree gave you no advantage at all in your career and you still came home to start over in India, would the experience itself have been worth ₹40 lakh and three years? If the honest answer is yes, you have an experiential reason and that is valid. If the honest answer is no, then your decision is a career bet and the entire rest of this guide is about whether the bet is well sized.

If you want help thinking through this part more deeply, the is studying abroad worth it post breaks the question into seven sub-questions you can journal through.

2. Is studying abroad worth it? The honest ROI math

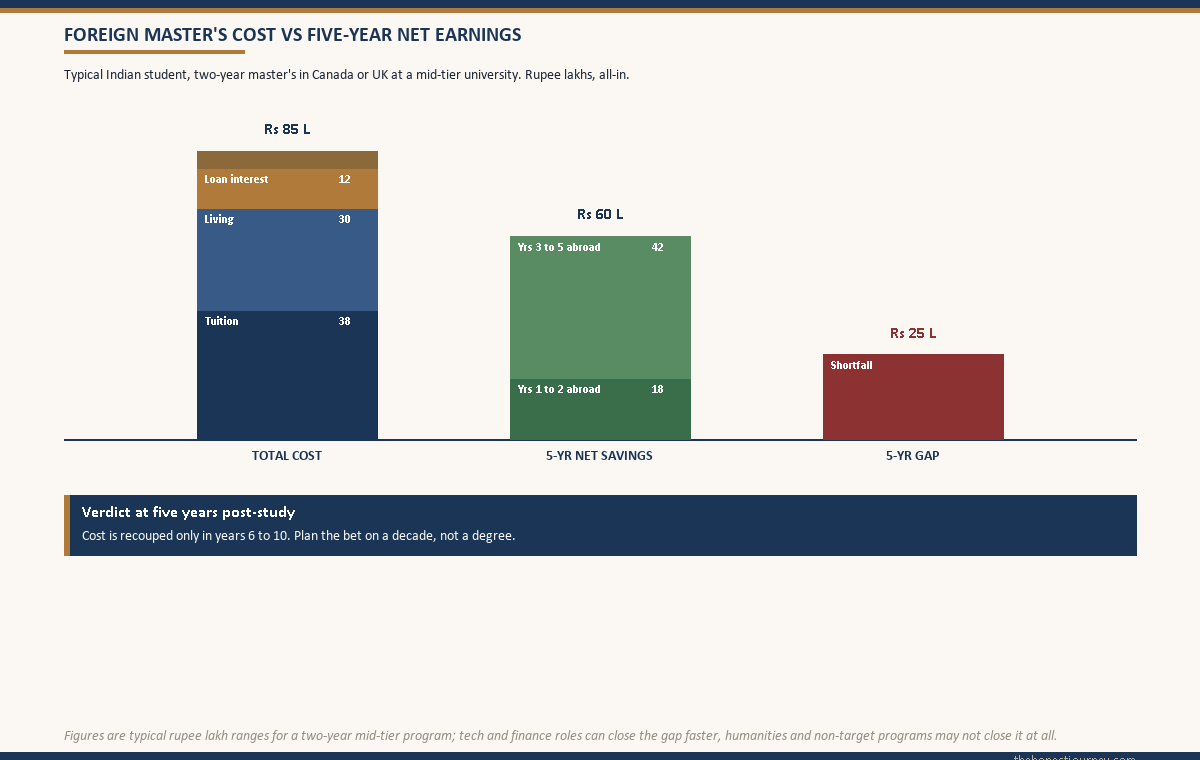

Let me give you the math nobody else seems to want to do publicly. Take a typical two-year master’s in Canada or the UK at a mid-tier university. Tuition is roughly ₹30 to 45 lakh. Living costs run ₹12 to 18 lakh per year, so call it ₹24 to 36 lakh over the program. One-time costs (visa, flights, GIC, insurance, first-month deposits, forex) add another ₹4 to 6 lakh. Add the TCS on foreign remittance, which under current rules sits at 5% above the LRS threshold for non-loan funding (see the Income Tax Department for current rates). All-in, you are looking at ₹60 to 90 lakh per program.

Now run the income side. A new master’s graduate in Canada or the UK in a typical non-tech field starts at the equivalent of ₹35 to 55 lakh per year before tax. Rent, transport, groceries, and basic life in Toronto, London, Vancouver, or Manchester eat 55 to 70% of that. Net savings in the first two years are realistically ₹6 to 12 lakh per year if you live carefully.

If you took a loan for ₹40 lakh of that cost at 11.5%, your EMI starting after the moratorium is roughly ₹56,000 per month for ten years. That is ₹6.7 lakh per year of pre-tax income going to the loan, for a decade. The moratorium interest math means you actually repay closer to ₹85 lakh on a ₹40 lakh borrowed amount.

So the honest ROI question becomes: does the foreign master’s plus the post-study work experience add enough lifetime earnings (over the Indian alternative) to repay ₹85 lakh, and still leave you ahead? For some career paths and some countries, yes, clearly. For others, the gap is much narrower than the agent’s slide deck suggests, and for a few it is actually negative once you price in the lost compounding on the family savings that went into the down payment.

If you want the full ROI breakdown including a worked example for engineering, MBA, and humanities profiles, read is studying abroad worth it: the honest ROI math.

Study abroad vs study in India: the honest comparison

The dominant question behind every email I get is not really “should I go abroad,” it is “is abroad better than staying in India.” Those are different questions, and the honest answer is that India has closed a lot of ground while staying far cheaper, but it has not closed the gap on a few things that genuinely matter. Here is the comparison I run with readers, with fair weight given to what India does well and what only going abroad can buy you.

| Factor | Study in India | Study abroad |

|---|---|---|

| Cost | A strong Indian degree runs ₹2 to 25 lakh end to end at most private and public institutions, a fraction of the abroad number. No forex, no TCS, no decade-long loan in most cases. | ₹20 to 90 lakh all-in for a two-year master’s depending on country, almost always loan-funded, with the moratorium and EMI weight that follows. |

| Course quality and brand | At the very top, the IITs, IIMs, AIIMS, NLUs, and ISB are genuinely world-class with global recognition and recruiter pull. Below that tier, quality and placement strength fall off faster than the brochures admit. | Strong depth, modern labs, and industry links at mid-tier and top universities alike, plus a globally portable brand. The catch is that a non-elite foreign degree carries less weight than people assume. |

| Career and PR pathway | A clear Indian career with no visa risk, and rising salaries in tech, finance, and consulting. No permanent residency angle, which matters only if living abroad is the actual goal. | The real differentiator. A post-study work visa and a possible PR route in Canada, Australia, or Germany is something no Indian degree can offer. This is the single honest reason abroad wins for many readers. |

| Family proximity | Close to home, lower emotional and logistical cost, easier to support ageing parents and stay woven into family life. | Distance is real. Time zones, expensive flights, and missed family events are a genuine cost that rarely makes it onto the agent’s slide. |

| Global exposure and network | Growing, especially at ISB, the IIMs, and institutions with strong exchange programs, but a domestic peer network by default. | Strongest here. A genuinely international peer group, cross-border professional network, and lived experience of another culture and work system that pays off for decades if you use it. |

Give the non-financial column its fair weight. The global network, the PR optionality, and the exposure are real assets that a spreadsheet undercounts, and for some readers they are the whole point. But weigh them against the honest ROI math from the section above, not against the brochure. A foreign degree that buys you a network and a PR pathway you actually use is worth the premium. A foreign degree bought for the brand alone, at a non-elite university, funded by a loan your starting salary cannot service, is the most expensive way to acquire exposure you could have gotten more cheaply later.

My honest read after a decade of these conversations: if your target is a top Indian institution and your career will live in India, staying is very often the better financial and life decision. If your target abroad is a strong program with a credible work and PR pathway, and you have answered the funding question honestly, abroad can clear the bar that the ROI math sets. The deciding factor is rarely the country. It is whether the specific program plus pathway justifies the specific price.

Faz's ruleDo not compare 'abroad' to 'India' in the abstract. Compare your actual foreign offer to your actual best Indian alternative, at their real prices, with their real outcomes.

The abstract comparison always flatters abroad because it pits a top foreign university against an average Indian one. Run it the honest way, your real options side by side, and the answer changes for about half the readers I talk to.

3. When to go: after Class 12 or after a Bachelor’s?

This is the single most-asked question in my inbox, and the agents have an enormous incentive to push you toward going earlier rather than later, because the fees for a four-year undergraduate placement are larger than for a two-year master’s placement. The honest answer is more nuanced than they will tell you.

Going for an undergraduate degree directly after Class 12 makes sense in a narrow set of cases. You have a specific program (Ivy League, Oxbridge, top-15 US engineering, a few Canadian and Australian institutions with strong industry pipelines) where the brand carries demonstrable career weight globally. You have full or near-full funding through scholarship or family wealth that does not require a loan that compounds for the next decade. You have clarity at 18 about what you want to do for the next ten years, which is genuinely rare and not something to fake.

For everyone else, the math on a master’s-first route is much cleaner. You complete a Bachelor’s in India at one-tenth the cost. You work for one to three years, which both clarifies what you actually want to specialise in and gives you real CV material that improves your master’s admissions and post-study job outcomes. You arrive abroad at 23 to 25 rather than 18, with maturity, savings, and a specific reason for being there. The loan is sized to a two-year program, not four, and the moratorium math is half as brutal.

The trap to avoid: a four-year Bachelor’s abroad funded entirely by a loan, at a non-elite university, with no concrete career pipeline at the end. That combination has produced more “I came back at 23 with ₹50 lakh of debt and no Indian work experience” stories than any other route I see.

For the full discussion including profiles where each path works, see study abroad after Class 12: when it makes sense and when it does not.

Faz's ruleThe right time to study abroad is the moment you can answer 'what specifically am I going to do with this degree' in one clear sentence. Until then, you are paying ₹60 lakh to find out.

I have watched too many 18-year-olds go abroad to “explore” and come back at 22 having explored, with debt, no Indian campus network, and the realisation that the answer was always going to come from doing, not from another degree.

4. Which country fits which profile

The country question is downstream of the why question. Once you know what you are optimising for, the country mostly chooses itself. Here is the honest matrix.

If you are optimising for lowest cost with a viable work pathway, Germany is the strongest answer for STEM, engineering, and increasingly data and CS, where public universities charge near-zero tuition and the post-study work visa is 18 months. The catch is that German-language ability shifts from “nice to have” to “essential” the moment you start interviewing. The cheapest country to study abroad post lays out the trade-offs honestly.

If you are optimising for likelihood of permanent residency, Canada and Australia have historically led, with Germany emerging as a strong third for STEM. Canada’s Express Entry pathway and the post-graduation work permit have been the most generous large-scale PR route for international students, though policy is tightening as of 2025-26 and you should check current rules at canada.ca rather than rely on what your agent told you. Australia’s post-study work visa and skilled migration pathway are documented at immi.homeaffairs.gov.au.

If you are optimising for brand and global mobility, the US and UK still dominate at the top end, with the trade-off being much higher total cost, more variable PR pathways (US in particular is brutal on H-1B luck), and a job market increasingly competitive for international graduates. The UK graduate route currently allows two years post-study work; verify current rules at gov.uk.

If you are optimising for European exposure with English-taught programs, the Netherlands and Ireland are the cleanest answers, with strong industry links (tech in both, finance and pharma in Ireland) and post-study work options of 12 to 24 months.

The full decision tree by reader profile is in best country to study abroad for Indian students: the honest matrix.

5. Destination snapshots: cost, work rights, PR odds

Quick comparison of the five destinations where most of my readers end up. Numbers are 2025-26 typical ranges. Always verify with the official immigration site at the time you apply, because policy in this space changes every 12 to 18 months.

| Country | Total program cost (2-yr master’s, all-in) | Part-time work hours/week | Post-study work visa | PR realism (2026) |

|---|---|---|---|---|

| Canada | ₹50 to 75 lakh | 24 hours during term, full-time on breaks | Up to 3 years (PGWP) | Possible but tightening |

| Germany | ₹20 to 35 lakh | 20 hours during term | 18 months | Strong for STEM, requires German |

| Australia | ₹55 to 85 lakh | 48 hours per fortnight during term | 2 to 4 years | Possible via skilled migration |

| Ireland | ₹45 to 65 lakh | 20 hours during term | 2 years (Stamp 1G) | Possible via Critical Skills list |

| Netherlands | ₹35 to 50 lakh | 16 hours during term | 1 year (Orientation Year) | Moderate, depends on employer sponsorship |

Three things to note. First, “PR realism” is my honest read of the 2026 policy environment, not a guarantee. Canada has tightened its PGWP and PR criteria materially in the last 18 months. Australia is mid-review on skilled migration thresholds. UK and US numbers are not in this table because they are the highest-cost and most policy-volatile, and I want you reading their specific posts before making that call.

Second, the part-time work hours look generous on paper but they cover roughly 30 to 60% of your living cost in most of these cities. They do not cover tuition. Plan the budget assuming part-time work fills the cushion, not the gap.

Third, the post-study work visa is necessary but not sufficient for PR. It buys you the time to qualify; the qualification itself depends on the job you land, the salary band, the occupation list, and in some cases the language test score. Treat the work visa as a door, not a destination.

For deep country-by-country detail, see the destination posts: Canada, Germany, Australia, Ireland, and Netherlands.

6. The funding decision: loan or self-funding

If your family can comfortably fund the program from existing liquid savings without dipping into retirement money, the family home, or fixed deposits earmarked for a sibling’s marriage or education, self-funding is almost always the better answer. You save the 11.5% loan interest, you save the moratorium capitalisation, and you save the decade of monthly EMI pressure that shapes every career decision you make after graduation.

If you cannot comfortably self-fund, the question becomes: how much can the family contribute up front, and what is the smallest loan amount that bridges the gap? The temptation, encouraged by both banks and consultants, is to take the maximum loan you qualify for and “keep family savings as a buffer.” That logic is upside-down. The family savings sitting in an FD earning 7% pre-tax are losing money relative to a loan compounding at 11.5%. Apply as much family contribution as you can spare without touching emergency reserves, take the smallest loan possible, and treat the loan as the expensive last-resort fuel it actually is.

There are real cases where a loan is structurally the right answer. Tax planning when the co-applicant is a high earner on the old regime and the Section 80E deduction on interest is meaningful. Liquidity preservation when the family runs a business and cash flow matters more than total cost. Risk distribution when the family does not want to concentrate too much capital on one child’s outcome.

What is almost never the right answer: a fully-funded loan against the family home when the program is at a non-elite university, the post-study work pathway is uncertain, and the expected starting salary cannot service the EMI at under 35% of take-home.

The full loan vs self-funding decision, including a side-by-side worked example, is in education loan vs self-funding. For the broader funding mix question (loan plus savings plus scholarship plus part-time work), see how to fund study abroad: the realistic mix.

Faz's ruleNever take the maximum loan the bank will approve. Take the minimum loan the program actually requires after every other source has been exhausted.

The bank approves on FOIR. You repay on starting salary. Those two numbers are not the same and the bank is not the one who lives with the gap.

7. The during-study reality: part-time work and living cost

The agent slide on “earn while you study” is technically true and practically misleading. Yes, every country in our list allows international students to work part-time. Yes, you can earn the local equivalent of ₹80,000 to ₹1.5 lakh per month at the legal hour limit in most of them. No, that does not cover what you think it covers, and it absolutely does not cover tuition.

Run the math for a typical reader. Canada, 24 hours a week at CAD 17 minimum wage, gives you roughly CAD 1,700 per month pre-tax, which is roughly ₹1 lakh. Rent in a shared apartment in Toronto, Vancouver, or Mississauga is ₹50,000 to 70,000 per month for your share. Groceries, transit, phone, and basic life add another ₹25,000 to 40,000. You are at break-even on living cost with zero margin. If you work full-time during the four months of break, you can save ₹2 to 4 lakh per year. That is a real contribution but it is not what closes the ₹60 lakh program cost.

The deeper issue is academic. A master’s program at a Canadian, Australian, or European university is genuinely demanding. The students who push part-time work to the upper limit during term often do it at the cost of their grades, their internship pipeline, and their post-study job offers. The right mental model: part-time work covers your incidental living costs and gives you local work experience for your CV. Treat it as cushion, not as funding.

The countries where the math is most generous for part-time work are Canada and Australia. The countries where it is most constrained are the Netherlands (16 hours) and the UK (20 hours during term, with non-trivial restrictions on the type of work). Germany allows 20 hours per week or 120 full days per year, which is workable but heavily dependent on local language for non-STEM roles.

The full part-time work picture by country, including realistic monthly earnings and tax handling, is in part-time work while studying abroad.

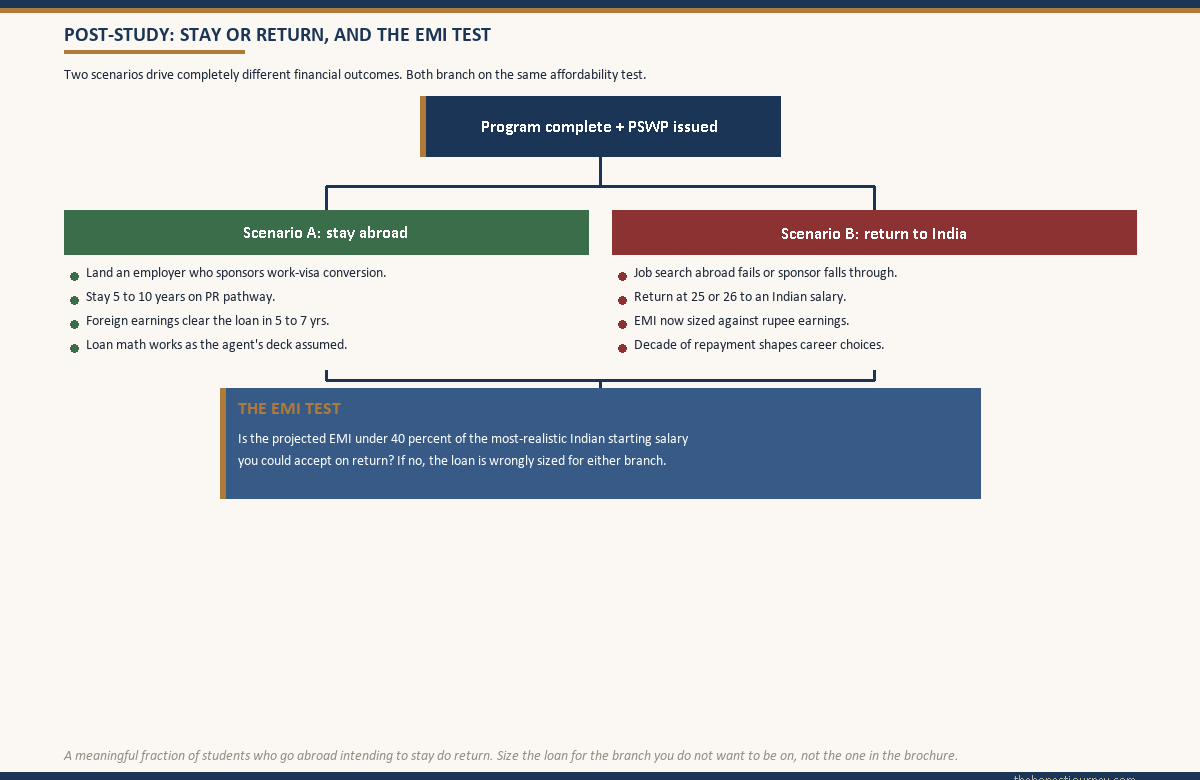

8. The post-study reality: return to India or stay?

This is the part of the decision almost nobody runs at the start, and it is the part that determines whether the entire bet paid off. Two scenarios, two completely different financial outcomes.

Scenario A: you land a job in your destination country during the post-study work visa, you successfully transition to a PR or work-visa pathway, you stay for five to ten years (or permanently). The foreign earnings, even after the high cost of living, allow you to clear the loan in five to seven years rather than ten, build savings in a stronger currency, and the original loan math works out cleanly. This is the outcome the agent’s slide deck assumed.

Scenario B: you complete the program, the post-study job search is harder than expected, you cannot land an employer who will sponsor work-visa conversion, your post-study work visa runs out, and you return to India. You are now starting an Indian career at 25 or 26 with two years of foreign experience that some Indian employers value and some do not, a master’s that some Indian employers value and some do not, and a loan being repaid in rupees against an Indian salary. The math here is much tighter. A ₹36,000 EMI on a ₹8 to 12 lakh starting salary in India is 30 to 45% of take-home before rent, and that stays true for ten years.

The honest truth I have learned watching this play out: a meaningful fraction of students who go abroad with the intention of staying do come back. Not because they failed, but because the policy environment shifted, the job market in their field tightened, family circumstances changed, or they simply decided they preferred building their adult life in India. None of these are bad outcomes. But they are different financial outcomes than the one the loan was sized for.

The question to ask yourself before signing: if I had to come back to India after the post-study work visa with my best-realistic Indian starting salary, can I still service this loan at under 40% of take-home? If yes, the bet is well sized. If no, you are betting the family’s financial security on Scenario A working out.

For the full discussion of return scenarios and how to plan for both outcomes, see return to India after studying abroad: the honest framework.

9. Red flags that should make you say no

I have learned, often the hard way through reader stories that arrived too late, to flag certain patterns as near-automatic stop signs. If three or more of these describe your situation, please pause and reconsider before signing your university acceptance.

You cannot name the specific career outcome. “I want to do a master’s in business analytics in Canada and then get a job” is not a career outcome. “I want to work as a senior data analyst at a Canadian bank, which requires a Canadian master’s because they sponsor work visas almost exclusively for graduates of Canadian programs, and I have spoken to three people in this exact role” is a career outcome. The first sentence is a fantasy; the second is a plan.

The funding requires putting the family home up as collateral and the program is at a non-elite university with an uncertain job market. The collateral loan reduces your interest rate but does not change the underlying bet. If the outcome does not pay off, you are not just personally indebted; you have put the family’s primary asset at risk. The risk-reward only works at universities and programs with genuine pipeline strength.

You are going because someone else (parent, partner, friend group) wants you to. The person who pays for the EMI for ten years should be the same person who made the decision. If you are doing this because your mother has dreamed of it since you were ten, or because your fiancee is already abroad, or because everyone in your engineering batch is going, the chances that you sustain through the hard middle of the program (when the homesickness, the academic pressure, and the financial weight all peak at once) drop sharply.

You are using “study abroad” as a fix for a different problem. If the real reason is that you do not want to be in your current city, or you do not know what to do next, or your family relationships are difficult, a ₹60 lakh degree is the most expensive possible answer to those problems. Therapy, a different city in India, a job change, time, or all of the above will address them far better and leave you in a stronger position to actually use a foreign degree later, if you still want to.

The agent’s projections seem too clean. “100% PR pathway.” “Guaranteed job placement.” “Easy visa.” If you hear any version of these phrases, you are talking to someone whose incentive is to close your enrolment, not to advise you. Walk out. The official immigration sites (canada.ca, gov.uk, immi.homeaffairs.gov.au) and the Indian Ministry of External Affairs are where the truth lives.

The total loan EMI will exceed 40% of your most-realistic Indian starting salary. Run this number with brutal honesty. Not the salary the agent quoted. Not the salary the placement report from the university listed. The salary you would actually accept if you came back to India tomorrow with the degree in hand. If the EMI breaks 40% of that number, the loan is wrongly sized.

You are not eligible for the destination’s mainstream post-study work visa. Some country-program combinations sit outside the normal post-study work pathway (certain professional accreditations, part-time programs, programs below a certain credit threshold). Confirm before you enrol. Check the government immigration site directly, not the university brochure.

10. A 7-question decision framework

Use this in one sitting, on paper, with no one else in the room. Answer each question honestly. If you cannot answer five of seven cleanly, you are not yet ready to sign.

1. What is the specific career outcome this degree enables that no Indian alternative can? One sentence. Specific role, specific industry, specific geography.

2. Have I spoken to at least three people who currently hold that role or a comparable one, and confirmed the pathway from this degree to that role? LinkedIn is built for this. Cold outreach works.

3. What is the total all-in cost (tuition + living + one-time + TCS) and what is the funding mix? Write down rupee amounts for family contribution, scholarship (if real, with award letter in hand), part-time work projection (cushion only), and loan principal.

4. What is the projected EMI after the moratorium, and is it under 40% of the most-realistic Indian starting salary I could accept on return? Use the EMI calculator and the cost of studying abroad calculator to run both numbers.

5. What does the official immigration site of my target country say about the post-study work visa today (not what the agent said)? Cite the URL, the date you checked, and the specific clause that applies to my program.

6. If everything goes wrong (no job in destination country, return to India at 25), can I still service the loan without putting family finances at risk? If no, the loan is wrongly sized.

7. Am I willing to live with the answer to question 1 being wrong? Career plans at 23 do not always survive contact with reality. If you would resent the loan in five years if the original plan changes, the decision needs more time.

If you can answer all seven cleanly and the answers point to “go,” go with confidence. If you can answer most of them but a few are shaky, work on the shaky ones before signing. If most of them are shaky, the honest answer is that this is not the right decision in its current form, and it is far cheaper to find that out now than two years and ₹30 lakh from now.

Faz's ruleThe best filter for whether you should go is whether you can write the answer to question 1 in a single specific sentence, today, without help from an agent.

If the sentence sounds like an aspiration rather than a plan, you are not ready. If it sounds like a plan, you probably already know your answer.

Once you have decided, the application itself comes down to two documents you write and one you ask for. See the statement of purpose and the letter of recommendation.

Where to go next

Depending on where you are in the decision, the following are the best next reads.

If you are still on the should-I-go question: start with is studying abroad worth it and then study abroad after Class 12.

If you have decided to go and are picking a country: best country to study abroad followed by the specific destination posts for your shortlist.

If you are deep into funding: education loan vs self-funding and the broader how to fund study abroad guide.

If you are already abroad and thinking about staying or returning: return to India after studying abroad and part-time work while studying abroad.

If you are weighing one specific cheaper destination: cheapest country to study abroad for Indian students.

Faz's ruleThere is no shame in deciding not to go. The shame is in going for the wrong reasons and discovering it at 26.

The strongest career stories I have seen from readers are evenly split between people who went abroad and people who built their lives in India. The common thread is honesty with themselves at 22 about what they actually wanted.

Your answer depends on which of these you are. Read the version written for engineering graduates, working professionals weighing an MBA, tier-2 college students, students with an average academic record, non-STEM and commerce graduates, anyone applying in their 30s, or the parents carrying the cost.

FAQ

Is studying abroad worth it for Indian students in 2026?

It is worth it for students with a specific career destination that requires a foreign degree or foreign work experience, a funding plan that does not put the family home at structural risk, and a realistic post-study work or PR pathway in the target country verified against the official immigration site. It is not worth it as a default route after Class 12, as a status purchase, or as an escape from a problem at home. For roughly half the readers who write to me, the more honest answer is that the same money invested in a strong Indian degree plus international exposure later produces a better life.

Should I study abroad right after Class 12 or after a Bachelor’s in India?

For most students, a Bachelor’s in India followed by a master’s abroad at 23 to 25 is the cleaner financial and life decision. The loan is sized to two years rather than four, you arrive with maturity and savings, your post-study job outcomes are stronger because of prior work experience, and the program choice is informed by what you actually want to do. Direct undergraduate abroad makes sense only when the program is at a clearly elite institution with demonstrable career weight, funding does not require a decade-long loan, and you have rare clarity at 18 about your career direction.

Which country is best for Indian students to study abroad?

There is no single best country. Germany leads for low-cost STEM education with German-language commitment. Canada and Australia lead for PR pathways, though both are tightening policy as of 2025-26. The US and UK lead for brand and global mobility at the highest cost and most variable post-study outcomes. Ireland and the Netherlands are strong for English-taught European options with industry links. The right country is downstream of your career destination, your funding situation, and your tolerance for language acquisition.

How much does it cost to study abroad from India?

Typical 2-year master’s programs run ₹50 to 85 lakh all-in for English-speaking destinations (Canada, UK, Australia, Ireland), ₹35 to 50 lakh for the Netherlands, and ₹20 to 35 lakh for Germany at public universities with low or zero tuition. All-in means tuition plus living costs (₹12 to 18 lakh per year in most cities) plus one-time costs (visa, flights, GIC, insurance, forex, first-month deposits) plus TCS on foreign remittance under the LRS rules from RBI. Numbers are 2025-26 typical ranges and shift annually.

Can I work part-time while studying abroad and cover my expenses?

Part-time work at the legal hour limit (16 to 24 hours per week in most destinations) typically covers 30 to 60% of living costs, not tuition. Canada and Australia have the most generous limits. The Netherlands and UK are tighter. Germany allows 20 hours per week or 120 full days per year. The honest mental model: part-time work is cushion for incidental costs and CV material for local work experience, not a funding source for the program. Pushing work hours to the upper limit also risks academic outcomes and post-study job pipeline.

Will I get permanent residency in Canada or Australia after studying there?

Possibly, but not guaranteed, and the policy environment has tightened materially in the last 18 months. Canada’s PGWP and Express Entry pathway has been the most generous large-scale PR route for international students, though category-specific draws, language test thresholds, and occupation lists are all in flux. Australia’s skilled migration pathway depends on the occupation list and points score. Always verify current rules at the official immigration sites (canada.ca, immi.homeaffairs.gov.au) rather than rely on agent projections. Treat the post-study work visa as a door, not a destination.

Is it better to take an education loan or self-fund a study abroad program?

If your family can self-fund from existing liquid savings without touching emergency reserves, retirement money, or assets earmarked for other commitments, self-funding is almost always better. You save the 11.5% interest, the moratorium capitalisation, and a decade of EMI pressure on your career choices. A loan is structurally correct when the family income justifies the Section 80E tax benefit, when liquidity preservation matters (family business cash flow), or when risk distribution is the right call. Never take the maximum loan the bank approves; take the smallest loan that bridges the actual gap after every other source is exhausted.

What is the TCS on foreign remittance for education abroad?

Under current LRS rules from the Reserve Bank of India and the Income Tax Act, Tax Collected at Source applies to foreign remittances for education above specified thresholds, with different rates for loan-funded versus non-loan-funded transfers. The exact rates and thresholds have been revised multiple times in recent years and should be verified at incometaxindia.gov.in at the time you plan your transfer. TCS paid is creditable against your final tax liability, so it is a cash flow cost rather than a permanent tax cost for most families, but the cash flow cost itself is significant on ₹50 to 80 lakh of remittance over a program.

What happens if I cannot get a job abroad after my master’s and have to return to India?

You return with a foreign master’s and (depending on the country) up to two years of foreign work experience that some Indian employers value and some do not. Starting salaries in India for a returning master’s graduate are typically ₹8 to 18 lakh per year depending on field and institution, against an EMI that was sized for foreign earnings. If the EMI was kept under 40% of your most-realistic Indian starting salary at the time of loan sizing, this scenario is manageable. If not, it becomes a decade of financial strain. The full discussion of return planning is in the return to India after studying abroad post.

What are the red flags that I should not go abroad to study?

Multiple red flags compound. You cannot name the specific career outcome the degree enables. The funding requires putting the family home up as collateral for a non-elite program. You are going because someone else wants you to, not because you do. You are using study abroad to escape a different problem (relationships, lack of direction, family pressure). The agent uses phrases like “guaranteed PR” or “100% placement.” The projected EMI exceeds 40% of your most-realistic Indian starting salary. If three or more of these describe your situation, pause and reconsider before signing the university acceptance.

Are there scholarships that meaningfully reduce the cost of studying abroad?

Yes for a minority of students, mostly at the top end of academic merit, financial need, or specific government-to-government programs. Realistic scholarships fall into a few categories: university-specific merit awards (typically 20 to 50% tuition reduction at the offer stage, awarded automatically), need-based aid (rare for international students at most universities), and government programs (Chevening for the UK, Fulbright for the US, DAAD for Germany, Endeavour for Australia). The honest read: never plan your funding mix assuming a scholarship until you have the written award letter in hand. Treat scholarship as upside, not as base case.

Do I need an agent or consultant to apply for studying abroad?

No. Every step of the process (university shortlisting, application, visa filing, loan application, accommodation booking) can be done directly by you and your family with the official sources (university websites, the official immigration sites, the lender’s branch). Agents add value primarily for students who genuinely cannot navigate the process themselves or who are applying to large numbers of universities in parallel. The trade-off is that an agent’s incentive is your enrolment, not your decision quality. If you do use one, pay a flat fee rather than a commission-based fee, and never let the agent’s projections substitute for the official immigration site for visa and post-study work questions.

You have the framework. You have the numbers. You have the questions. The decision is yours, and only you live with the answer. I trust you to be honest with yourself.

Faz · The Honest Journey · 2026