An education loan for Singapore from an Indian PSU bank sanctions up to around ₹1.5 crore secured, but the unsecured ceiling without collateral stays at ₹7.5 lakh at PSU banks and runs to ₹50 lakh or more at NBFCs. A non-subsidised SGD 45,000 Master’s is roughly ₹28 lakh of tuition at ₹62 per Singapore dollar, so most students need collateral or an NBFC. The MOE Tuition Grant shrinks the loan, but it binds you to a three-year service bond.

A reader wrote to me last year, panicking, because his bank had sanctioned a loan against the full SGD 45,000 tuition on his NTU offer, and then he discovered he qualified for the MOE Tuition Grant, which would more than halve the tuition. He had over-borrowed before the grant was applied, and unwinding a sanction is far slower than sizing it right the first time. The grant changes the loan, so you have to settle the grant question before you fix the loan amount, not after.

This is the loan-product picture for Singapore. Which lenders fund it, how much, the collateral wall, the Student Pass funds proof, and how the MOE Tuition Grant changes the size of the loan you actually raise. The destination side, the universities, the cost, the bond, sits in the companion piece on studying in Singapore for Indian students.

How banks classify Singapore

PSU banks treat Singapore as a Tier-1 study destination, the same top bucket as the USA, UK, Canada and Australia. The flagship products are SBI Global Ed-Vantage, Bank of Baroda’s Baroda education loan for studies abroad, and Canara Bank’s IBA Premier scheme. Union Bank and PNB run parallel overseas products on the same Indian Banks’ Association framework.

Tier-1 classification matters because it sets the ceiling and the collateral logic. For studies abroad the sanction structure splits into three layers, and which layer your Singapore ticket lands in decides almost everything about your rate, your collateral and your repayment runway.

- Up to ₹4 lakh: no margin, no collateral, no third-party guarantee. No Singapore Master’s fits here.

- Above ₹4 lakh to ₹7.5 lakh: parent co-applicant and a third-party guarantee, usually no tangible collateral. Still well below a Singapore ticket.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory at PSU banks. This is where a non-subsidised Singapore Master’s lands.

The wider ceiling picture across destinations sits in the post on the maximum education loan amount in India. For Singapore the practical takeaway is that an unsubsidised tuition clears the ₹7.5 lakh unsecured wall, so you are choosing between PSU collateral or an NBFC.

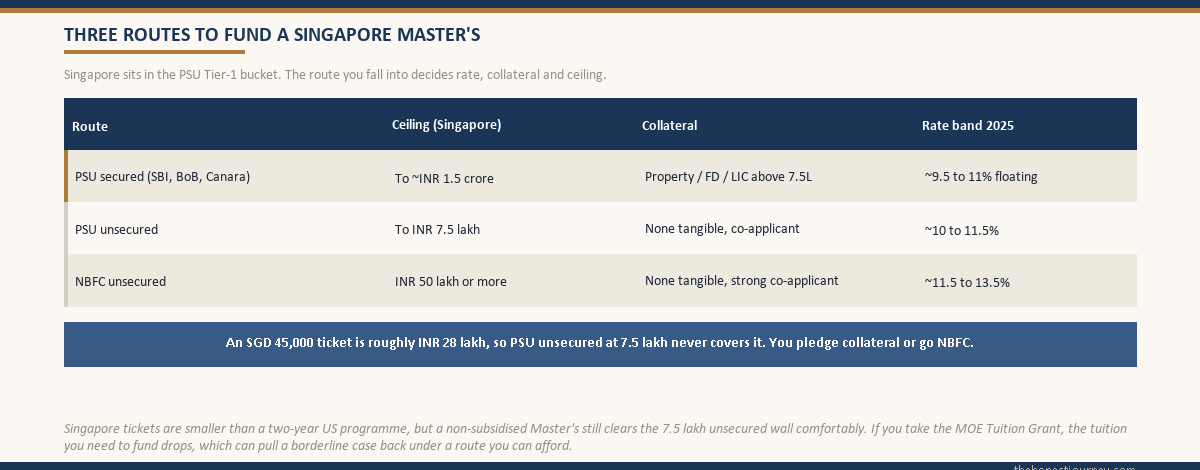

The three routes, by ceiling and collateral

Here is the route map for a Singapore loan. The numbers below are the typical product positions, not a regulator’s caps.

| Route | Typical ceiling (Singapore) | Collateral | Rate band (2025) |

|---|---|---|---|

| PSU secured (SBI, BoB, Canara) | To around ₹1.5 crore | Property, FD or LIC mandatory above ₹7.5 lakh | ~9.5 to 11 percent floating |

| PSU unsecured | To ₹7.5 lakh | None tangible, co-applicant required | ~10 to 11.5 percent |

| NBFC unsecured | ₹50 lakh or more | None tangible, strong co-applicant income | ~11.5 to 13.5 percent |

A non-subsidised SGD 45,000 Master’s is roughly ₹28 lakh of tuition alone at ₹62 per Singapore dollar, before living. That is far above the ₹7.5 lakh unsecured PSU ceiling, so a family with property to pledge takes the cheaper PSU secured route, while a family without tangible collateral goes to an NBFC such as Avanse, HDFC Credila, Auxilo or InCred and pays the higher rate. NBFCs lean on the programme’s ranking and the graduate’s earning potential, so a strong NUS, NTU or SMU offer supports a larger unsecured sanction against a clean parent co-applicant with a CIBIL above 750.

The RBI sets the regulatory framework these lenders operate under, and the IBA model scheme is the template PSU banks follow. The current rules are on the RBI site and the model educational loan scheme is published by the Indian Banks’ Association. Neither caps the Singapore sanction amount; the ceiling comes from each bank’s product policy and your collateral.

The Student Pass funds proof

Singapore’s Student Pass process expects evidence that you can fund your studies and living, and the sanctioned education loan is a primary part of that evidence. Unlike the US, where the bank reads a certified Form I-20 cost of attendance as the sanction ceiling, Singapore works off the university’s offer letter and published fees plus a living estimate. So the bank sizes the loan from the offer’s fee schedule, and that sanction letter then supports your Student Pass application.

The practical sequence is that you settle the loan before you complete the pass application, because the proof of funds wants the sanction in hand. The funds-evidence side is covered in the companion piece on studying in Singapore. The point for the loan is timing: get the sanction letter early enough that it can sit inside your pass file.

Faz's ruleSettle the MOE Tuition Grant question before you fix the loan amount, never after. Over-borrowing against full tuition and then qualifying for the grant means unwinding a sanction, which is slow and painful.

The grant can more than halve your tuition, so a loan sized on full tuition before the grant is decided is a loan that is too big. Tell your bank you are applying for the grant, and size the sanction on the tuition you will actually pay. Unwinding an oversized sanction wastes weeks you do not have before the intake.

How the MOE Tuition Grant changes the loan size

This is the Singapore-specific lever and it is large. The Ministry of Education Tuition Grant subsidises tuition at Singapore’s publicly funded universities for eligible students, including international students who accept its three-year service bond. The grant cuts the tuition you owe, often by roughly half, which directly shrinks the loan you need to raise.

The catch is the bond. Taking the grant commits you to work for a Singapore-registered company for three years after you graduate, repaying the grant with interest if you break it. So the grant is a loan-reducer only if the bond fits your plan. The full bond picture is in the destination post on studying in Singapore. For the loan, the message is mechanical: a smaller tuition means a smaller sanction, a smaller margin contribution and a smaller EMI.

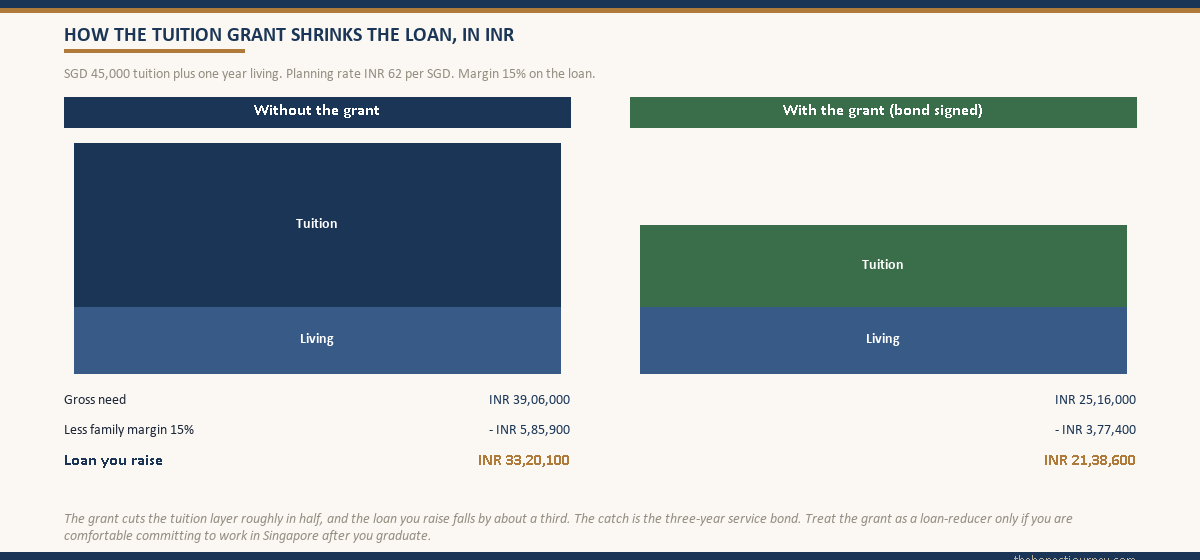

The worked INR example for an SGD 45,000 Master’s

Take a real-shaped case. Student admitted to a one-year Master’s at NTU for the August intake. Tuition is SGD 45,000 non-subsidised, and a realistic living budget for the year is SGD 18,000. At a planning rate of ₹62 per Singapore dollar, that is ₹27.9 lakh tuition and ₹11.16 lakh living, an all-in gross need of about ₹39.06 lakh.

| Item | SGD | INR (at 62) |

|---|---|---|

| Tuition (non-subsidised) | 45,000 | 27,90,000 |

| Living, one year | 18,000 | 11,16,000 |

| Gross need | 63,000 | 39,06,000 |

This student goes to SBI for a Global Ed-Vantage loan. Because the amount is above ₹7.5 lakh, tangible collateral is mandatory, so the family pledges a residential property. Now the margin money. For studies abroad PSU banks ask for 10 to 15 percent margin on amounts above ₹4 lakh, contributed by the family alongside each disbursement rather than upfront. At 15 percent margin on the ₹39.06 lakh gross need, the family contributes about ₹5.86 lakh across the tranches, and the loan raised is about ₹33.2 lakh.

| Funding layer (no grant) | INR | Notes |

|---|---|---|

| Gross need (tuition + living) | 39,06,000 | The amount to fund |

| Family margin (15 percent) | ~5,85,900 | Paid alongside disbursements |

| Loan you raise | ~33,20,100 | Disbursed per the fee schedule |

| Collateral pledged | Property, above the loan | After valuation haircut |

Now apply the MOE Tuition Grant. If the subsidised tuition falls to about SGD 22,500, roughly ₹14 lakh, the gross need drops to about ₹25.16 lakh, the 15 percent margin falls to about ₹3.77 lakh, and the loan you raise falls to about ₹21.4 lakh. The grant has cut the loan by roughly a third. The trade is the three-year service bond, so this only makes sense if working in Singapore after graduation already fits your plan.

| Funding layer (with grant) | INR | Notes |

|---|---|---|

| Gross need (subsidised tuition + living) | ~25,16,000 | Tuition roughly halved |

| Family margin (15 percent) | ~3,77,400 | Falls with the gross need |

| Loan you raise | ~21,38,600 | Roughly a third smaller |

| Service bond | 3 years in Singapore | The price of the grant |

Faz's ruleModel the EMI on the loan you actually raise after margin and grant, not the headline tuition. The difference between ₹33 lakh and ₹21 lakh of loan is a different EMI and a different life for five years.

A ₹33 lakh loan at around 10 percent over ten years is a serious monthly commitment; a ₹21 lakh loan is far lighter. The grant changes which of those two you live with. Decide the bond on career grounds, then let the loan math follow, and always confirm at the branch how margin and any grant or scholarship are folded into the calculation.

The collateral-free route and where it bites

If the family has no property, FD or LIC to pledge, the same case at an NBFC means an unsecured sanction of around ₹33 lakh against the parent’s income, typically needing a clean CIBIL above 750 and demonstrable repayment capacity, at an interest rate of 11.5 to 13.5 percent versus SBI’s floating rate near 9.65 percent. Over a long repayment that spread is several lakh of extra interest. The honest economics of the unsecured route are in the post on an education loan for abroad studies without collateral.

The NBFC appetite for Singapore is healthy because NUS, NTU and SMU rank well and the Singapore job market pays well, so the lender’s bet on the graduate’s earning power is sound. But the rate is the rate. If you can pledge collateral, the PSU route saves real money. If you cannot, the NBFC route keeps the door open at a cost you should price into the decision before you sign.

Disbursement and the forex mechanics

For a Singapore loan the bank disburses tuition by SWIFT wire to the university per the fee schedule, usually in one or two tranches for a one-year programme, with living costs released as needed. The remittance runs under the Liberalised Remittance Scheme, so the forex and the A2 form paperwork matter; that mechanism is covered in the post on the A2 form, LRS and forex for students, and how the money actually moves is in the post on the education loan disbursement process. The Singapore-specific point is that the Student Pass needs the sanction in place first, so settle the loan, then let the disbursement follow the fee schedule once you are enrolled.

The honest take on a Singapore education loan

A Singapore loan is more manageable than a US one for two reasons. The ticket is smaller, because the programmes are one year and the all-in cost is below a two-year US Master’s. And the repayment runway is solid, because a graduate in a demanded field earns a good Singapore salary that services a ₹20 to 35 lakh loan comfortably. That combination is why Singapore loans tend to repay cleanly when the field and the job market line up.

The thing to get right is the grant. Size the loan after you have decided the grant, not before, because the grant can cut the loan by a third and unwinding an oversized sanction is slow. And decide the grant on career grounds, because the three-year service bond is the real price, not a footnote. Pledge collateral if you can, to take the cheaper PSU rate; go NBFC with eyes open on the spread if you cannot. Get those three calls right, and Singapore is one of the more financeable top-tier destinations an Indian student can choose.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for Singapore is in the Singapore student pass guide.

FAQ

Can I get an education loan for Singapore from Indian banks?

Yes. All major PSU banks, including SBI, Bank of Baroda, Canara, Union and PNB, cover Singapore under their Tier-1 overseas education loan products, and NBFCs like Avanse, HDFC Credila, Auxilo and InCred fund it unsecured. PSU banks sanction up to around ₹1.5 crore with collateral and up to ₹7.5 lakh without tangible security. A non-subsidised Singapore Master’s clears the unsecured wall, so most students either pledge collateral at a PSU bank or take an NBFC unsecured loan.

What is the maximum loan for Singapore from Indian banks?

PSU banks such as SBI Global Ed-Vantage sanction up to around ₹1.5 crore for Singapore, provided collateral and co-applicant income support the amount. The unsecured ceiling at PSU banks stays at ₹7.5 lakh, so anything above needs tangible security such as property, fixed deposit or LIC. NBFCs sanction unsecured loans of ₹50 lakh or more for strong programmes against a clean parent co-applicant, at interest rates higher than PSU floating rates.

How does the MOE Tuition Grant change my loan?

The grant subsidises tuition at Singapore’s publicly funded universities, often cutting it by roughly half, which directly shrinks the loan you need. In the worked example a non-subsidised SGD 45,000 ticket needs a loan of about ₹33.2 lakh, while the same case with the grant drops the loan raised to about ₹21.4 lakh. The catch is a three-year service bond to work in Singapore, so take the grant as a loan-reducer only if that obligation fits your plan.

Is collateral needed for a Singapore education loan?

At PSU banks, yes, for almost every Singapore Master’s. The unsecured ceiling is ₹7.5 lakh, and a non-subsidised programme runs far above that at roughly ₹28 lakh of tuition alone, so any amount above ₹7.5 lakh needs tangible collateral such as property, fixed deposit or LIC. NBFCs sanction unsecured up to ₹50 lakh or more against parent income and a clean CIBIL, but at higher interest rates, so weigh the PSU collateral route against the NBFC rate spread.

How much margin money do I need for a Singapore loan?

For studies abroad, PSU banks ask for 10 to 15 percent margin money on the loan amount above ₹4 lakh. Margin is the family’s own contribution, paid alongside each disbursement rather than upfront, so on a ₹39 lakh gross need at 15 percent you contribute roughly ₹5.86 lakh across the tranches. Some banks fold a scholarship or the MOE Tuition Grant into the margin calculation, so confirm at the branch exactly how your margin is computed before you sign.

Does the Student Pass need the loan sanction?

Yes, in effect. Singapore’s Student Pass process expects evidence that you can fund your studies and living, and the sanctioned education loan is a primary part of that proof of funds. Unlike the US, where the bank reads a certified Form I-20, Singapore sizes the loan from the university offer and fee schedule. So settle the sanction early enough that the letter can sit inside your pass application, because the proof of funds wants it in hand before you complete the formalities.

What interest rate applies to a Singapore education loan?

PSU secured loans for Singapore run roughly 9.5 to 11 percent floating, PSU unsecured around 10 to 11.5 percent, and NBFC unsecured around 11.5 to 13.5 percent. The difference between a PSU secured rate near 9.65 percent and an NBFC rate above 12 percent is several lakh of extra interest over a long repayment, so if you can pledge collateral the PSU route saves real money. Always confirm the prevailing rate and reset frequency at the branch before signing.

Is a Singapore education loan easier to repay than a US one?

Generally yes. The Singapore ticket is smaller because programmes are one year, so the loan is below a two-year US Master’s, and graduates in demanded fields earn good Singapore salaries that service a ₹20 to 35 lakh loan comfortably. The repayment runway is solid when the field and the job market line up. The main risk is over-borrowing before the MOE Tuition Grant is decided, since the grant can cut the loan by a third and unwinding an oversized sanction is slow.

Faz · The Honest Journey · 2026