Education loan remittances under the Liberalised Remittance Scheme (LRS) attract TCS at just 0.5 percent on amounts above ₹7 lakh per financial year, not the 20 percent rate that applies to other LRS spending. The TCS shows up in your Form 26AS under the PAN of whoever paid (student or co-applicant), and you reclaim it as a credit while filing that person’s ITR. If TCS exceeds total tax liability, the balance is refunded to the bank account on your ITR. Most students get the full amount back.

I keep seeing the same panic message in family WhatsApp groups every June. Parent forwards a screenshot from a banking app showing ₹40,000 deducted as TCS on a ₹15 lakh tuition wire, and someone in the chain says “the new 20 percent rule has kicked in.” It almost never has, not for education loan money.

The TCS on education loan rules are honestly simple once you separate them from the 20 percent rule that applies to non-education LRS remittances. This post walks through the actual rate, where it shows up in your tax records, and how to claim it back in the right person’s ITR.

What TCS on education loan actually is

Tax Collected at Source (TCS) under Section 206C(1G) of the Income Tax Act is collected by an authorised dealer (your bank) when you remit money abroad under LRS. It is not a tax. It is a prepayment that gets adjusted against your final income tax liability for the year. If you owe nothing, it gets refunded in full.

For education remittances funded by an education loan from a scheduled financial institution covered under Section 80E, the TCS rate is 0.5 percent on the amount exceeding ₹7 lakh in a financial year. For education remittances paid from any other source (self-funded, parent’s savings, FD break), the rate is 5 percent on the amount above ₹7 lakh. Both sit far below the 20 percent rate that applies to everything else under LRS. Reference text on incometaxindia.gov.in.

The 7 lakh threshold is per remitter, per PAN, per financial year. Two parents wiring separately can each use their own 7 lakh limit. Once you cross it, TCS applies only on the excess, not on the full amount.

Faz's ruleThe 20 percent TCS panic does not apply to education loan remittances. It applies to overseas tour packages, foreign stock purchases, and other non-education LRS outflows above ₹7 lakh.

I have watched families abandon perfectly good remittance plans because someone in the chain mixed up the education rate with the tour package rate. 0.5 percent on a ₹25 lakh education loan transfer above the threshold is ₹9,000. The same ₹25 lakh wired for a non-education purpose at 20 percent would be ₹3.6 lakh. The rate you face depends entirely on what the remittance is classified as.

The rate structure: 0.5 percent, 5 percent, 20 percent

The Finance Act 2023 (effective 1 October 2023) cleaned up the TCS rates after a year of confusion. Here is what currently applies for the 2025 to 2026 financial year, as confirmed in the Income Tax Department’s circulars on the e-filing portal.

| Purpose of LRS remittance | Up to ₹7 lakh / FY | Above ₹7 lakh / FY |

|---|---|---|

| Education funded by loan from approved institution (80E qualifying) | Nil | 0.5% |

| Education funded from own funds (savings, FD, gift) | Nil | 5% |

| Medical treatment abroad | Nil | 5% |

| Overseas tour package | 5% | 20% |

| Any other LRS purpose (investments, gifts, property) | Nil | 20% |

For an education loan disbursement going directly to a foreign university (the bank pays the university, the loan account funds the wire), the 0.5 percent rate applies above ₹7 lakh per FY. The bank deducts TCS at the remittance stage and deposits it against the PAN of the loan account holder, typically the student.

For tuition you pay from your own bank account using a forex wire, with no education loan involved, the 5 percent rate applies above ₹7 lakh per FY. Here the TCS goes against the PAN of the remitter, which is usually the parent or whoever owns the funding bank account.

The 5 percent vs 0.5 percent distinction is why the funding source paperwork matters at the remittance stage. The bank classifies the transaction based on what you declare in the LRS Form A2 and the supporting documents. An education loan sanction letter and disbursement reference let the bank apply the 0.5 percent rate. Without those, it defaults to 5 percent. More on the sanction letter side in my TCS on education loan India post.

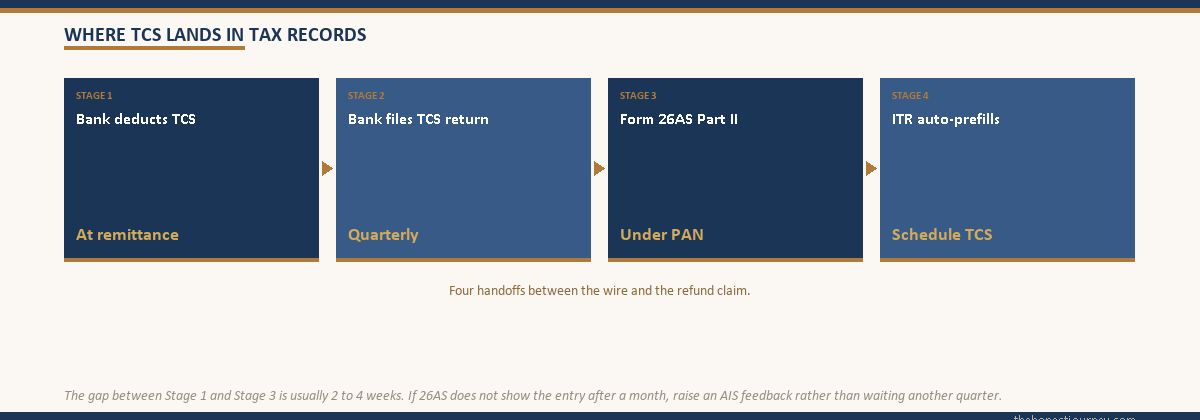

Where the TCS shows up: Form 26AS and AIS

Every TCS deduction by the bank gets reported to the Income Tax Department under the PAN of the person whose account funded the remittance. It appears in two places when you log into the e-filing portal.

Form 26AS (Part II for TCS). This is the consolidated tax statement under your PAN. The TCS entry shows the deductor (bank name and TAN), the date, the amount remitted, and the tax collected. It usually reflects within 2 to 4 weeks of the remittance, after the bank files its quarterly TCS return.

Annual Information Statement (AIS). The AIS is the broader information statement and shows the same TCS entry, plus the underlying foreign remittance. If the bank’s report and your records do not match, you flag a feedback through AIS itself.

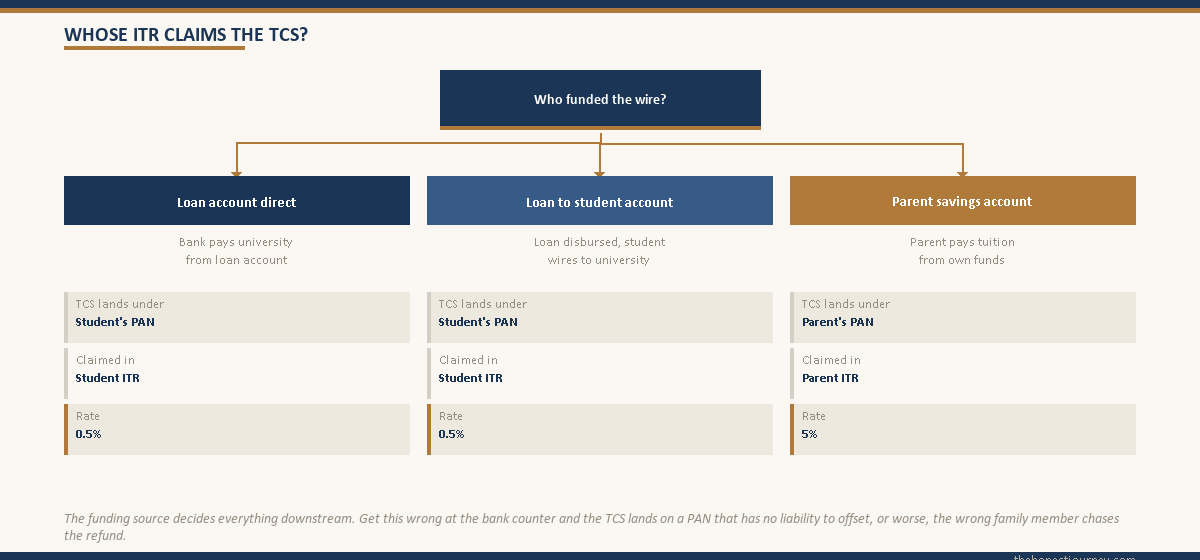

The critical thing: TCS lands under the PAN of whoever’s bank account funded the remittance, not always the student. If the parent’s savings account paid the wire and the student is the beneficial owner of the education, the TCS is in the parent’s 26AS, and the parent claims it in their ITR. If the student’s loan account funded the wire directly, the TCS is in the student’s 26AS. Track this at the remittance stage so you know whose ITR carries the credit.

How to claim TCS refund in the ITR

Claiming the TCS as a credit or refund is a routine line item in the ITR, not a separate refund application. The mechanics:

Step 1. Log into the e-filing portal using the PAN under which the TCS was deducted. Confirm the TCS entry in Form 26AS Part II for the relevant assessment year.

Step 2. Start the relevant ITR (typically ITR-1 for salaried, ITR-2 if there is capital gains or foreign assets, ITR-3 if there is business income). The portal auto-prefills the TCS amount from 26AS into Schedule TCS of the return.

Step 3. Cross-check the prefilled TCS amount against your bank remittance receipts and Form 26AS. If anything is missing, edit Schedule TCS manually with the deductor’s TAN, the amount of TCS, and the financial year.

Step 4. Compute total tax liability for the year. The TCS amount is treated like a prepaid tax (similar to TDS and advance tax) and reduces the final liability. If TCS plus TDS plus advance tax exceeds total tax owed, the excess becomes a refund.

Step 5. Pre-validate the bank account where you want the refund credited. The refund processes after the Centralised Processing Centre (CPC) verifies the return, usually 20 to 90 days from e-verification.

Faz's ruleA student with no other income gets the full TCS amount back as a refund, because their total tax liability is zero.

This is the most common case I see. The student has the loan in their name, the bank wires tuition from the loan account directly to the foreign university, the 0.5 percent TCS gets reported under the student’s PAN. The student has no salary, no other income, no tax liability. They file a NIL return claiming the TCS, and the full amount lands in their bank account 2 to 3 months later.

Student ITR vs co-applicant ITR: who claims the refund

This is where most families get stuck. The TCS credit belongs to whoever’s PAN it sits under in Form 26AS, which is whoever’s bank account funded the remittance. Pick the wrong person to claim it, and the refund stalls.

Three common scenarios:

Scenario A: Loan disbursed directly to university by the bank. The loan account is in the student’s name (most education loans are structured this way, with the parent as co-applicant). TCS is reported under the student’s PAN. Student files ITR claiming the credit. If the student has no other income, the full TCS amount comes back as refund.

Scenario B: Loan disbursed to the student’s savings account, student wires the money. Same outcome. TCS lands under student’s PAN, student claims in student’s ITR.

Scenario C: Co-applicant (parent) pays tuition from their own account, separate from the loan. Even if there is an education loan in the background, if the actual remittance was funded by the parent’s savings account, the TCS is in the parent’s 26AS. Parent claims it in their ITR against their salary tax liability. The rate here is 5 percent, not 0.5 percent, because the bank classifies it as self-funded education, not loan-funded.

Worth flagging: if the student is going abroad mid-year and will become a non-resident for tax purposes, the TCS still gets claimed in whatever ITR is filed for the relevant financial year. Residency status affects which income is taxable, not whether TCS credit can be claimed. The student files an Indian ITR for the year and reclaims TCS even if they have no Indian income, since TCS is a prepaid tax against zero liability and becomes a refund.

Pre-2023 vs post-2023 confusion

The reason families are still confused is the rules changed twice in 18 months. The original Section 206C(1G) introduced 0.5 percent TCS on education-loan-funded remittances and 5 percent on self-funded education remittances in October 2020, with a ₹7 lakh annual threshold.

The Finance Act 2023 (Budget February 2023) proposed raising the rate on most LRS remittances to 20 percent with no threshold, but after public backlash, the Finance Ministry clarified through press releases and circulars that education and medical remittances would stay at the concessional rates (0.5 percent and 5 percent respectively, above ₹7 lakh). The 20 percent rate was kept for non-education and non-medical LRS outflows, with the effective date pushed to 1 October 2023.

So the current state, in force since 1 October 2023 and still applicable:

- Education funded by loan: 0.5 percent above ₹7 lakh

- Education funded from own funds: 5 percent above ₹7 lakh

- Tour packages: 5 percent up to ₹7 lakh, 20 percent above

- Everything else under LRS: 20 percent above ₹7 lakh

The old “uniform 5 percent on all education above ₹7 lakh” rule no longer applies. The new structure separates loan-funded from self-funded, with loan-funded getting the cheaper 0.5 percent rate. This is a real concession that rewards using a formal education loan, and it stacks neatly with the Section 80E interest deduction available on the same loan.

Direct tuition payment by bank vs forex by family

One common question: does TCS apply if the bank pays the university directly from the loan account, with no money passing through anyone’s savings account?

Yes. The TCS trigger is the LRS outflow from India to a foreign jurisdiction, regardless of which Indian account it leaves from. A bank wiring tuition directly to a US or UK university from the loan account is still an LRS remittance, and TCS at 0.5 percent applies above the ₹7 lakh threshold. The bank deducts it before the wire goes out and credits it to the student’s PAN in 26AS.

If a family wires tuition from a parent’s NRE account (the parent is an NRI), the LRS rules do not apply (LRS is a resident-only scheme), so no TCS is collected. NRI parents paying for resident students should keep this in mind. For more on resident-status and forex movement, see my how much money to carry abroad as a student post.

The RBI’s LRS framework, governed under the Foreign Exchange Management Act, sits separately from the TCS provisions but the bank applies both at the same remittance point, which is also where you sign the A2 form under the LRS to send money abroad as a student. Reference on rbi.org.in for the LRS master direction, and the IBA circulars for the bank-side implementation.

Timing and refund speed

Practical timing notes that matter when you are planning:

TCS deducted at remittance. The bank holds back the TCS amount from your wire at the time of remittance. So if you ask for a ₹20 lakh wire and you are ₹13 lakh above the ₹7 lakh threshold for the year, the bank deducts ₹6,500 (0.5 percent of ₹13 lakh) and wires ₹19,93,500 to the university. Build this into your tuition cushion so the university gets the exact amount needed.

Form 26AS reflects in 2 to 4 weeks. The bank files its TCS return quarterly, so the entry usually shows up after the quarter ends.

ITR can be filed once the assessment year opens. For financial year 2025 to 2026, ITR filing opens around April 2026 (assessment year 2026 to 2027). File early to start the refund clock.

Refund processing. The CPC at Bengaluru typically processes refunds within 30 to 90 days of e-verification of the return. Refunds under ₹1 lakh process faster than larger ones. Bank account pre-validation must be complete or the refund stalls.

The honest verdict

TCS on education loan remittances is a 0.5 percent concessional rate that exists because the government wants to encourage formal education borrowing. The 20 percent rate that triggers panic does not apply here. The amount deducted is genuinely small (0.5 percent of the excess above ₹7 lakh per FY), it sits as a credit against the relevant PAN, and it comes back as a refund through the standard ITR filing process.

The two things to get right are: track whose PAN the TCS lands under (it is whoever’s account funded the wire), and file that person’s ITR with the TCS credit claimed. A student with no other income typically gets the full amount back. A salaried parent who paid from their account adjusts it against their salary tax liability. Neither is complicated.

What gets people in trouble is mixing this up with the 20 percent rate on non-education LRS, or assuming the TCS is a lost cost instead of a refundable credit. It is not lost. It is a few thousand rupees parked with the government for a year, returned through the ITR. See the broader education loan India complete guide for how this fits into the overall borrowing picture.

FAQ

What is the TCS rate on education loan remittances in 2026?

The TCS rate on LRS remittances funded by an education loan from a scheduled financial institution is 0.5 percent on the amount exceeding ₹7 lakh in a financial year. Below ₹7 lakh per FY, no TCS applies. This rate is significantly lower than the 5 percent that applies to self-funded education remittances and the 20 percent that applies to most other LRS outflows like overseas tour packages or foreign investments. The 0.5 percent rate has been in force since 1 October 2023 under Section 206C(1G).

Can I get a refund of TCS deducted on my education loan?

Yes. TCS is not a tax. It is a prepayment of income tax that gets credited against the final tax liability of whoever’s PAN the TCS was deducted under. When you file the ITR for that PAN, the TCS amount is offset against any tax owed, and any excess is refunded to your pre-validated bank account. A student with no other income usually gets the full TCS amount back, since their total tax liability is zero. The refund typically processes within 30 to 90 days of e-verifying the return.

How do I claim TCS refund in my ITR?

Log into the e-filing portal at incometax.gov.in using the PAN under which the TCS was deducted, start the relevant ITR (ITR-1, ITR-2, or ITR-3 depending on income type), and confirm the TCS entry in Schedule TCS, which is auto-prefilled from Form 26AS. Cross-check the amount against your bank remittance receipts. The TCS is treated as a prepaid tax and reduces final liability. If TCS exceeds total tax owed, the balance is refunded to your bank account after CPC processes the return.

Does TCS apply if the bank pays tuition directly to the foreign university?

Yes. The TCS trigger is the LRS outflow from India to a foreign jurisdiction, not the route the money takes within India. A bank wiring tuition directly from the loan account to a foreign university is still an LRS remittance, so TCS at 0.5 percent applies above the ₹7 lakh annual threshold. The bank deducts it before the wire and credits it to the loan account holder’s PAN, typically the student’s. Build this into your tuition cushion so the university receives the exact amount required.

What is Form 26AS and how does it show TCS?

Form 26AS is the consolidated tax statement available on the e-filing portal under your PAN. It shows all TDS deducted by employers and others, all TCS collected by banks on your remittances, advance tax paid, and refunds received. TCS appears in Part II of Form 26AS, listing the deductor’s name and TAN, date of collection, amount remitted, and tax collected. The entry reflects 2 to 4 weeks after the remittance, once the bank files its quarterly TCS return.

Who can claim TCS refund: student or parent?

Whoever’s PAN the TCS is reported under in Form 26AS, which is whoever’s bank account funded the remittance. If the loan account or student’s savings account paid the wire, TCS lands under the student’s PAN and the student claims it. If a parent paid tuition from their own savings account separately from any loan, the TCS lands under the parent’s PAN and the parent claims it. Track the funding source at the remittance stage so the correct person files the claim in their ITR.

Is the 20 percent TCS rate applicable to education remittances?

No. The 20 percent rate applies to non-education LRS outflows above ₹7 lakh per financial year (foreign investments, gift remittances, property purchases, most other LRS uses). For education remittances, the rate is either 0.5 percent (if funded by an education loan from a notified institution) or 5 percent (if funded from own savings), and only on the amount exceeding ₹7 lakh per FY. Overseas tour packages have a separate structure with 5 percent below ₹7 lakh and 20 percent above.

Does TCS rate change if the student becomes a non-resident during the year?

No. TCS at the remittance stage is governed by the LRS classification of the transaction, not by the eventual residency status of the student. Even if the student becomes a non-resident for tax purposes during the same financial year, the 0.5 percent rate on loan-funded education remittances above ₹7 lakh continues to apply. The student can still file an Indian ITR for the relevant year and reclaim the TCS as a refund, because TCS is a prepaid tax against any tax liability, and a non-resident with no Indian income simply gets it all back.

Faz · The Honest Journey · 2026