A bonafide certificate for an education loan is an official letter from your university or college confirming that you are a genuinely enrolled student in a named course, signed and sealed by the registrar or principal. Indian banks following the IBA model scheme ask for it at initial sanction and often again at each tranche, because it is the only document that proves enrolment in the current term. It must carry the course name, duration, total fee structure, current year of study, attendance status, and the institution’s official seal with the registrar’s signature.

The first time I held a bonafide certificate in my hand, I thought it was a formality. The branch officer at my parents’ bank in Chennai handed it back across the counter the same afternoon and asked for a fresh one, because the date was three months old and the seal was a photocopy. That five-minute exchange added two weeks to my loan timeline.

This post is what I wish someone had told me before that counter visit. What a bonafide certificate actually is, what banks read on it, when in the loan lifecycle it gets asked for, and how to get a clean one out of a university that does not love issuing them.

The other paperwork that sits in the loan file: the education loan interest certificate post, the gap certificate for education loan post, and the demand letter education loan post.

What a bonafide certificate is and why the bank wants it

A bonafide certificate is a one-page institutional letter that states, in plain language, that a named person is a bonafide student of the institution in a named course. The word bonafide is the bank’s way of saying genuine, currently enrolled, in good standing. It is not the same as an admission letter, an offer letter, a fee receipt, a mark sheet, or an ID card, although the bank may ask for several of those alongside.

Banks ask for it for one straightforward reason. The sanction letter is the bank’s commitment to lend against your enrolment. If you are no longer enrolled, or were never genuinely enrolled, the entire loan basis collapses. The bonafide certificate is the only document a university issues that explicitly confirms current enrolment, dated to the moment of issue.

The Indian Banks Association model education loan scheme, which most public sector banks follow, names the bonafide certificate as a standard supporting document at both sanction and tranche release. Private banks and NBFCs follow the same convention, even though they are not formally bound by the IBA scheme.

What the bank actually expects on the certificate

Most universities issue a generic two-sentence bonafide (“This is to certify that X is a bonafide student of this institution”). That is fine for a visa, a hostel application, or a railway concession. It is usually not enough for an education loan, where the credit officer needs to match what the certificate says against what the sanction file claims.

The clauses a PSU bank credit officer reads on the certificate:

| Detail | Why the bank wants it |

|---|---|

| Full legal name of the student | Must match PAN, Aadhaar, and the sanction letter exactly |

| Course name with specialisation | Confirms the sanction was issued against the correct program |

| Course duration (start date and expected end date) | Sets the moratorium calendar and tranche schedule |

| Current year or semester of study | Maps to the tranche being released |

| Total fee structure (tuition, hostel, exam, other) | Cross-checks the sanctioned amount per head |

| Attendance status or enrolment status | Confirms the student is regular, not on leave or rusticated |

| Mode of study (regular, full-time) | PSU banks fund regular courses; distance and part-time are restricted |

| Registrar or principal signature with official seal | Authenticates the certificate as institutional |

| Date of issue and reference number | Banks reject anything older than 30 to 90 days at submission |

If the university’s standard certificate is missing two or three of these, the bank will usually accept it bundled with a separate fee structure letter and the latest admission letter. If it is missing five or more, you are looking at a request for a fresh, customised bonafide. I cover what that request looks like further down.

Faz's ruleAsk the university for a bonafide certificate that lists course name, duration, current year, fee structure, attendance status, and seal. Generic two-line certificates get returned by the bank.

The university registrar’s office issues two grades of bonafide: the short generic one for routine use, and a detailed one for loan and visa purposes. You almost always have to ask for the detailed version by name. The short one is the default because it is faster to print, and ninety percent of student requests do not need the long one.

When in the loan lifecycle the certificate is required

The bonafide certificate is not a one-time document. It comes up at predictable stages, and the bank treats each request as a fresh check.

At initial application, the bank asks for a bonafide certificate or the final admission letter, sometimes both. If your admission letter is conditional (offer subject to final mark sheet or visa), the bonafide is the document that converts it to confirmed enrolment in the bank’s eyes.

At the first tranche release, the bank asks for a current bonafide certificate dated within the last 30 to 90 days. Even if you submitted one at application, if more than three months have passed, expect a request for a fresh one. The bank wants to know you actually joined the course, not just secured admission.

From the second tranche onwards, most banks ask for a bonafide certificate alongside the previous semester’s mark sheet. The bonafide confirms continued enrolment in the current semester, the mark sheet confirms progression. Some banks (SBI, Canara) accept the mark sheet alone for domestic tranches; others (Bank of Baroda, Union Bank) want both. I cover the rest of the tranche flow in my education loan disbursement process walkthrough.

If you take a break (medical leave, semester drop, internship year out), the bank will ask for a fresh bonafide before resuming disbursement, explicitly stating that you have rejoined and are in good standing. Without it, the file sits.

How to request a bonafide certificate from an Indian university

Most Indian universities have a one-page form for bonafide requests, available at the registrar’s office, the student section, or the institute’s student portal. The mechanics vary, but the pattern is similar.

You fill the form with your roll number, course, current year, and the purpose (write “for education loan from XYZ Bank”). You attach a copy of your ID card and the previous semester’s mark sheet if you have one. You pay a nominal fee (usually ₹50 to ₹200) at the cash counter or online. The certificate is ready in 2 to 7 working days, sometimes same-day at smaller institutions.

Three things speed this up. Write the purpose specifically as “education loan” rather than leaving it blank, because the registrar’s office has a template for that purpose with the detailed clauses already in place. Attach the bank’s checklist if the bank gave you one, so the office knows exactly which fields to include. Pick up the certificate in person rather than requesting a postal copy, because the seal and signature are sharper on the original and banks sometimes reject scans.

If the university portal allows digital download, the certificate will be issued as a PDF with a QR code or unique verification number that the bank can verify online. Most PSU banks now accept these, but check with your branch first. A few branches still insist on a wet-signed hard copy, especially for first tranches.

How to request one from a university abroad

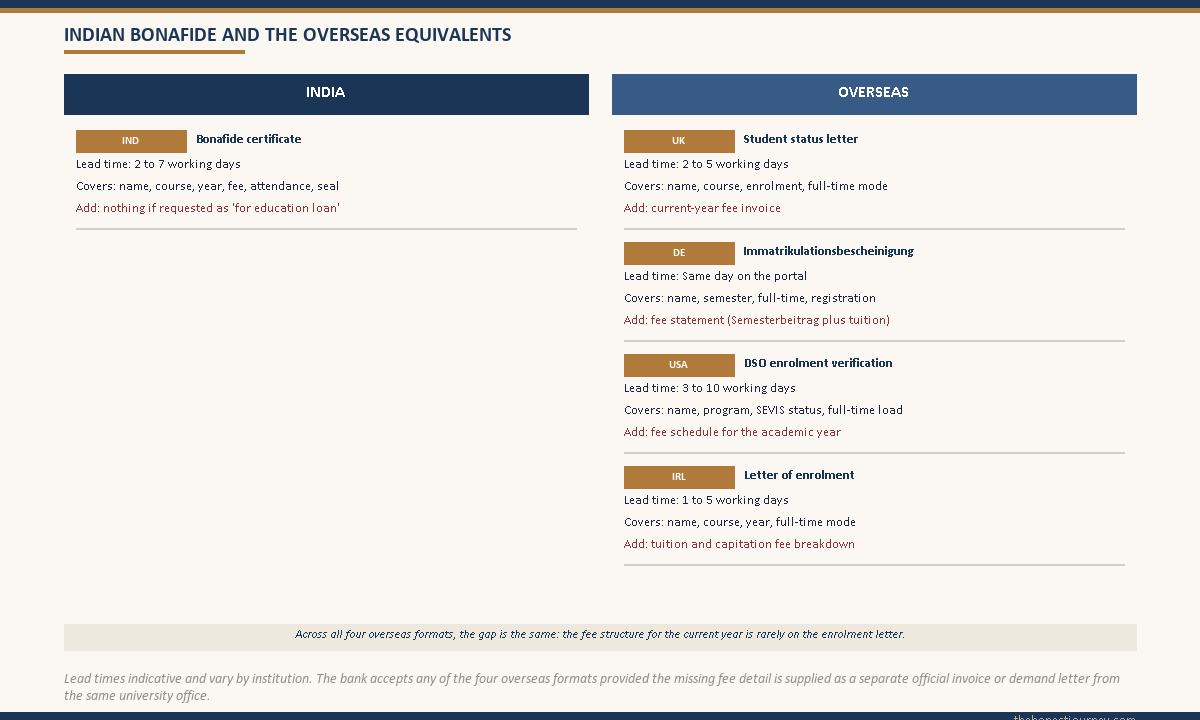

Universities abroad rarely use the term “bonafide certificate”. The equivalents are an enrolment confirmation letter, a student status letter, a Certificate of Enrolment, a CAS letter (UK), a Confirmation of Registration (Germany), or an I-20 with an active SEVIS status (USA, although the I-20 alone is not usually enough for an Indian bank).

The right office to ask depends on the country. In the UK, the international student office or the registry issues a status letter on request, usually free, ready in 2 to 5 working days. In Germany, the Immatrikulationsbescheinigung from the student secretariat is the standard enrolment proof, downloadable from the campus portal each semester. In Ireland, the international office issues a Letter of Enrolment, often available digitally. In the US, the Designated School Official (DSO) at the international office issues an enrolment verification letter that names the program and SEVIS status.

For the Indian bank, the letter must say the same things the Indian bonafide says: your name, course, duration, current year or semester, full-time mode, and good standing. Most overseas universities are used to issuing this for visa or sponsorship purposes and the language matches what the bank needs. The one thing to ask for explicitly is the fee structure for the current academic year, which many overseas letters omit by default. Combine the enrolment letter with the official fee invoice or demand letter, and the bank’s file is complete.

A sample bonafide certificate the bank will accept

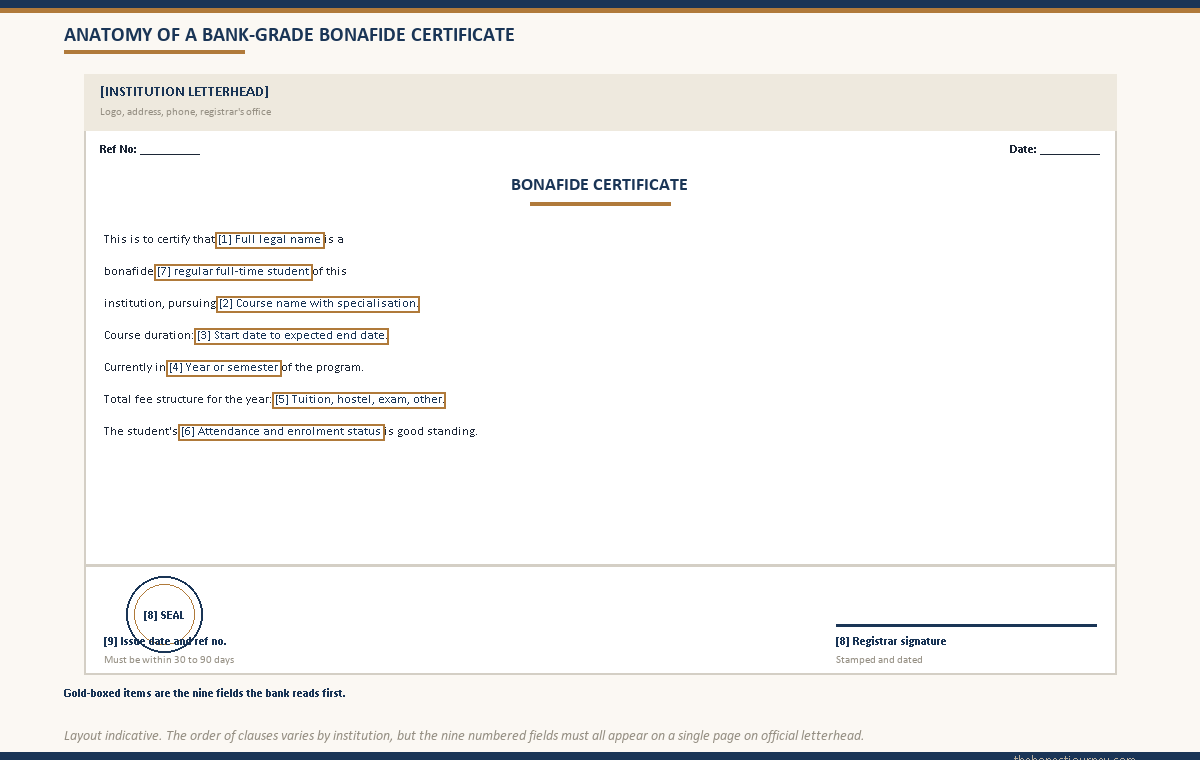

This is the format that works at PSU banks. I have masked the institution and student details. The structure and clauses are what matter.

[INSTITUTION LETTERHEAD WITH LOGO AND ADDRESS]

Ref No: [REGISTRAR REF NUMBER] Date: [DD/MM/YYYY]

BONAFIDE CERTIFICATE

This is to certify that Mr./Ms. [FULL LEGAL NAME OF STUDENT],

S/o or D/o [FATHER OR MOTHER NAME], bearing Roll Number

[ROLL NUMBER] and Registration Number [REGISTRATION NUMBER],

is a bonafide full-time regular student of this institution,

currently pursuing [FULL COURSE NAME WITH SPECIALISATION].

The course details are as follows:

Course duration: [START DATE] to [EXPECTED END DATE]

(Total [N] years, [M] semesters)

Current year of study: [CURRENT YEAR / SEMESTER]

Mode of study: Full-time, regular

Fee structure per academic year:

Tuition fee INR [AMOUNT]

Hostel fee INR [AMOUNT]

Examination fee INR [AMOUNT]

Other charges INR [AMOUNT]

Total per year INR [TOTAL]

The student's attendance and academic performance are

satisfactory and the student is in good standing.

This certificate is issued at the student's request for the

purpose of availing an education loan.

[REGISTRAR SIGNATURE]

[REGISTRAR NAME, DESIGNATION]

[OFFICIAL SEAL OF THE INSTITUTION]

Most PSU banks accept this format without further questions. The two clauses that matter most are the fee structure (matched against the sanction breakup) and the “good standing” line (which confirms the student is not rusticated, suspended, or on academic probation).

Faz's ruleSave the sample format above, show it to the registrar's office when you request the certificate, and ask for the wording to match. Most offices will adapt their template if you bring the structure to them.

Registrars do not write bonafide letters from scratch each time. They have a template. If your bank needs additional clauses, the cleanest path is to walk in with the exact format the bank wants, ask the office to incorporate the missing fields, and pay a slightly higher fee if needed. I have seen this done in twenty minutes at a Bengaluru engineering college and across two weeks at a Delhi central university. The variance is in the institution, not the request.

What to do when the university’s certificate is weak

Some universities, especially older state institutions and a few central universities, issue only the short generic bonafide and refuse to add clauses. The registrar’s stance is usually that the format is standardised and individual customisation is not possible. This is frustrating but not fatal.

Three workarounds I have seen work.

First, bundle the generic bonafide with two supporting documents the bank already accepts: the latest fee receipt or fee structure letter from the accounts section, and the latest admission or registration letter for the current term. Together, these cover the fields the bonafide misses. PSU banks like SBI under its Education Loan and Global Ed-Vantage products and Bank of Baroda under Vidya accept this bundling in practice, though the branch officer may need a polite explanation.

Second, request a separate fee structure certificate from the accounts office, on official letterhead with seal. This document explicitly lists tuition, hostel, exam and other fees for the current and remaining academic years. Combined with the short bonafide, it gives the bank everything it needs.

Third, if the bank is insistent on a single combined document, escalate to the dean or principal’s office rather than the registrar. Most academic heads have the authority to issue a custom bonafide on their own letterhead, even when the registry refuses. This is a last resort and works better at private universities than at central ones.

The path I have not seen work is arguing with the bank that the short bonafide should be enough. The branch officer is following a checklist set by the credit policy unit, and they cannot waive items on their own authority. Time spent arguing is time the file sits.

Validity, digital certificates, and common rejection reasons

Most banks treat a bonafide certificate as valid for 30 to 90 days from the date of issue. SBI typically wants something within the last 30 days at first tranche; Bank of Baroda accepts up to 90 days. Always check with your specific branch, because internal policy varies and a regional credit head can tighten the window.

Digital bonafide certificates with QR codes or unique verification IDs (now standard at most central universities under the UGC’s digital documents framework) are accepted by all PSU banks I have dealt with. Print the digital copy on plain paper, attach the QR code visible, and the bank verifies it online during processing. A handful of branches still insist on wet-signed hardcopies; this is becoming rare and usually limited to first sanctions at conservative branches.

Common reasons banks reject a bonafide certificate include the date being too old (the most common single reason), the seal being a photocopy rather than an original impression, the registrar’s signature missing or unsigned, the course name not matching the sanction letter exactly (a B.Tech CSE sanction with a B.Tech IT bonafide will be flagged), the attendance or enrolment clause missing entirely, and the certificate addressed to a different bank from the one processing your sanction.

The last one is the trap. If you collected a bonafide six months ago for a visa application, do not submit the same one to the bank. Some certificates are addressed “to whom it may concern”, which is fine. Others name the recipient explicitly, and a bonafide addressed to the embassy will not be accepted by SBI. Ask the registrar for a “to whom it may concern” addressing or a fresh one addressed to the bank.

The honest closing take

The bonafide certificate looks like a routine sheet of paper and most students treat it as such. The credit officer at the bank does not. For the officer, it is the single document that tells them whether the loan they sanctioned three months ago is still backed by a real student in a real course. Everything else in the file (admission letter, mark sheets, fee invoices, ID proof) is supporting evidence; the bonafide is the assertion of current enrolment.

Get the long-form version, get it dated close to your submission, get it signed and sealed in original, and get it in time. The cleanest education loan files I have seen are the ones where the student walked into the branch with a 60-day-old bonafide, a fresh fee invoice, the previous semester’s mark sheet, and the request letter, all stapled in order. The messy ones are where the student turned up with a three-line certificate from a year ago and expected the bank to accept it.

I also cover the wider documents required for an education loan, the most common education loan rejection reasons in India, and the role of the co-applicant in an Indian education loan in separate posts. Together with this one, they cover what the bank actually looks at, in the order it looks.

FAQ

What is a bonafide certificate for an education loan?

A bonafide certificate is an official letter from the educational institution stating that the named person is a genuinely enrolled, full-time, regular student of a specified course at that institution. For an education loan, banks use it to confirm current enrolment, the course duration, the year of study, the fee structure, and the student’s good standing. It is distinct from an admission letter, a mark sheet, or an ID card. Indian banks following the IBA model scheme treat the bonafide as a standard supporting document at both initial sanction and each tranche release during the course.

What details must the bonafide certificate contain for a bank?

The certificate should carry the full legal name of the student, the course name with specialisation, the start and expected end dates of the course, the current year or semester of study, the mode of study (regular and full-time), the fee structure broken into tuition and other heads, an attendance or enrolment status clause, and the registrar’s or principal’s signature with the official institutional seal. A clear date of issue and a reference number are standard. The bank’s credit officer matches each field against the sanction file, so a generic two-line certificate is usually returned.

Who issues the bonafide certificate at a university abroad?

The equivalent overseas document is issued by different offices depending on the country. In the UK, the international student office or the registry issues a status or CAS letter. In Germany, the student secretariat issues the Immatrikulationsbescheinigung, downloadable from the campus portal. In the US, the Designated School Official at the international student office issues an enrolment verification letter. In Ireland, the international office issues a Letter of Enrolment. The wording differs, but the content the Indian bank needs (name, course, duration, current year, full-time status) is the same.

Is a bonafide certificate the same as an admission letter?

No. An admission letter confirms that the institution has offered a seat in a course and that the student has accepted, usually issued at the start of the program. A bonafide certificate confirms that the student is currently enrolled and in good standing at the time the certificate is issued, which can be any point during the course. Banks ask for both at initial sanction because they answer different questions: the admission letter shows the basis of the loan, and the bonafide shows that the student actually joined and is continuing.

How long is a bonafide certificate valid for an education loan?

Most Indian banks treat a bonafide certificate as valid for 30 to 90 days from the date of issue. SBI typically wants something within the last 30 days at first tranche under its Global Ed-Vantage and domestic education loan products. Bank of Baroda’s Baroda Vidya and Baroda Scholar accept up to 90 days. The window can tighten if the regional credit head is being conservative. For each new tranche, expect to produce a fresh certificate; the one used at sanction is rarely accepted six months later. Always confirm the validity window with your specific branch.

Can the bonafide certificate be issued digitally?

Yes. Most central universities and many state universities now issue bonafide certificates digitally through their student portals, with a QR code or a unique verification ID that allows the bank to authenticate the certificate online. PSU banks under the IBA model scheme accept digitally signed bonafides as a standard practice. A handful of conservative branches, mostly at first sanction, still ask for a wet-signed hard copy with an original seal impression. If your university only issues digital certificates, print the copy and attach the verification ID visibly; the branch can verify it during processing.

What if the university issues only a generic bonafide certificate?

Bundle the short generic bonafide with two supporting documents: the latest fee structure letter from the accounts section on official letterhead, and the latest registration or admission letter for the current term. Together these cover the fields the short bonafide omits. Public sector banks following the IBA model scheme accept this bundling in practice. If the bank insists on a single combined document, request a custom bonafide from the dean’s or principal’s office rather than the registry, since academic heads usually have authority to issue customised letters on their own letterhead.

Do I need a fresh bonafide certificate for each tranche?

In most cases yes. From the second tranche onwards, banks ask for a current bonafide certificate alongside the previous semester’s mark sheet. The bonafide confirms continued enrolment in the new semester; the mark sheet confirms academic progression. Some banks like SBI and Canara accept the mark sheet alone for domestic tranches, while Bank of Baroda and Union Bank usually want both. After a break in studies (medical leave or a semester drop), the bank will always ask for a fresh bonafide stating that the student has rejoined and is in good standing before resuming disbursement.

Faz · The Honest Journey · 2026