An education loan for Australia from an Indian PSU bank typically sanctions up to ₹1.5 crore for a Master’s, but the unsecured ceiling without collateral stays around ₹7.5 lakh at PSU banks and ₹40 to 75 lakh at NBFCs for ranked universities. Australia’s total cost for a coursework Master’s runs AUD 54K to 79K a year including tuition (AUD 30K to 50K) and living (AUD 24K to 29K). At ₹55 per Australian dollar, that’s roughly ₹29.7 lakh to ₹43.5 lakh, which means most students need either tangible collateral or a strong parent co-applicant to bridge everything above ₹7.5 lakh.

A cousin’s son got into Monash for a Master’s in IT last year. He had a Canada plan running in parallel, but the Provincial Attestation Letter mess pushed him toward Melbourne instead. By the time his CoE came through, three things had caught the family off guard: how much the living-cost evidence mattered for the visa, the OSHC line that nobody had budgeted for, and the gap between what the bank sanctioned and what the year actually cost.

This post is the loan-side picture I wish the family had in hand before they signed the sanction letter, the kind of detail that changes whether you walk in with collateral ready or get caught short in June.

For the wider picture on Australia beyond the borrowing: the Canada vs Australia comparison and the study in Australia guide.

Why an education loan for Australia plays out differently

Australia sits in the top three destinations for Indian students alongside the US and Canada, and the PSU banks know it. SBI, Bank of Baroda, Canara and Union all classify Australia as tier-1 under their flagship overseas products, which means the full ceiling and the full covered-heads list apply. The universities that Indian students actually target (Melbourne, Sydney, UNSW, Monash, ANU, Queensland, UWA, Adelaide, plus the larger metropolitan ones like RMIT, Deakin, UTS and Macquarie) all sit on every bank’s approved list.

What makes the Australia loan story specific is the document the bank sanctions against and the cost evidence the visa demands. For Australia the sanction basis is the CoE, the Confirmation of Enrolment. And the visa side now runs on the Genuine Student requirement, which replaced the older Genuine Temporary Entrant test in 2024. Both of these shape how much you borrow and how the paperwork has to line up, so it is worth walking through each.

What an education loan for Australia actually covers

PSU banks treat Australia under their tier-1 overseas bucket, eligible under SBI Global Ed-Vantage and Bank of Baroda’s Baroda education loan, with Canara’s IBA Premier and Union Bank’s Special Education Loan as alternatives. The covered heads on a tier-1 sanction usually include:

- Full tuition for the entire program duration.

- Living expenses up to a stated annual cap, often 20 to 30 percent of tuition.

- Overseas Student Health Cover (OSHC), which is mandatory for the entire visa duration.

- Visa application fee and biometrics.

- One return economy airfare per year.

- Laptop and study material against bills, capped.

- The living-cost evidence the visa requires you to demonstrate before grant.

Two of those heads matter more for Australia than for most destinations: OSHC and the living-cost evidence. OSHC is not optional and not cheap, and the savings-evidence threshold is now a hard number the visa officer checks. The detail on funds evidence is in the health insurance for study abroad post, which covers how OSHC sits inside the wider insurance picture.

The CoE as the sanction basis: what the bank reads

The Confirmation of Enrolment is the official document the Australian education provider issues once you have accepted your offer and paid the initial tuition deposit. It carries a CoE number, the course name and CRICOS code, the start and end dates, the total tuition for the course, and the OSHC details if the university arranged the cover. This is the document the bank treats as the spine of the sanction file.

Here is the sequencing trap. The CoE usually requires an upfront tuition deposit (often the first semester, AUD 10K to 20K) before the university issues it. But the bank often wants the CoE before final disbursement. So families end up paying the deposit from their own funds or a pre-CoE tranche, then the bank disburses the balance once the CoE is in hand. Get this order clear with your branch early, because a CoE delay can stall the whole visa timeline.

The CoE total tuition figure is what the bank uses to size the tuition head of the loan. It will not sanction tuition higher than what the CoE states. Living expenses are added on top, capped by the bank’s own internal percentage, and OSHC is added as a separate line if you ask for it to be included. The full mechanics of how money actually moves are in the education loan disbursement process post.

Faz's ruleGet your CoE issued before you finalise the loan disbursement schedule, not after. The bank disburses against the CoE total, and a delayed CoE delays your visa lodgement and your tranche release together.

The CoE deposit comes out of your pocket or a first tranche, and only then does the university issue the CoE that the bank needs to release the balance. Map this order with your branch in your first meeting. Families that assume the bank pays the deposit directly lose two to three weeks they did not have.

The real cost math: tuition, living and OSHC

Here is what a one-year slice of a coursework Master’s at an Australian metropolitan university looked like for 2025 entry, based on the published tuition pages and the living-cost guidance on studyaustralia.gov.au.

| Cost head | AUD range (per year) | INR at 55 per AUD |

|---|---|---|

| Tuition (Master’s, coursework) | 30,000 to 50,000 | 16.50 lakh to 27.50 lakh |

| Accommodation (metro, 12 months) | 15,600 to 19,200 | 8.58 lakh to 10.56 lakh |

| Food and groceries | 4,800 to 6,000 | 2.64 lakh to 3.30 lakh |

| Transport (concession card) | 1,000 to 1,500 | 55,000 to 82,500 |

| OSHC (single, 12 months) | 650 to 800 | 35,750 to 44,000 |

| Visa application fee | 1,600 | 88,000 |

| Books, setup, flight | 2,500 to 3,500 | 1.38 lakh to 1.93 lakh |

| Total one-year cost | 56,150 to 82,600 | 30.88 lakh to 45.43 lakh |

Two things to call out. Tuition at a Group of Eight university like Melbourne or Sydney for a Master’s in IT or Engineering sits at the top of the range (AUD 45K to 50K a year), while a similar program at a larger metropolitan university like Deakin, RMIT or UTS sits closer to AUD 32K to 38K. The spread across two years of a coursework Master’s can be AUD 25K, which is roughly ₹13.75 lakh on the loan. And the visa fee jumped to AUD 1,600 in 2024, which is a line families used to ignore and now cannot. For the full picture beyond the loan, our breakdown of the cost of studying in Australia for Indian students lays out every head.

The Genuine Student requirement and the savings evidence

In 2024 the Department of Home Affairs replaced the Genuine Temporary Entrant test with the Genuine Student requirement, the GS. The shift matters for two reasons. First, the GS asks you to demonstrate that you are coming primarily to study, through a set of targeted questions in the visa application about your circumstances, your course choice, your ties, and your understanding of the conditions. Second, and more relevant for the loan, the savings-evidence threshold was raised. The official figures on the student visa subclass 500 are published on immi.homeaffairs.gov.au, and the funds requirement is the number that has to line up with your loan.

For the loan story, the GS savings evidence means the bank’s sanction letter does heavy lifting. The visa wants to see that you can fund the first year’s living costs on top of tuition. A PSU bank sanction letter that explicitly states the loan covers tuition plus living expenses plus OSHC is the cleanest way to satisfy this, because it shows funded capacity without the family having to park a large cash balance in the student’s account for weeks. Ask your branch for a sanction letter worded to cover all three heads, not just tuition.

Faz's ruleAsk the bank to word your sanction letter to cover tuition, living costs and OSHC together. A tuition-only sanction letter does not satisfy the Genuine Student savings evidence, and you will scramble to show separate cash.

The visa officer under the GS wants funded capacity for the whole first year, not just the fees. A sanction letter that names all three heads turns your loan into the funds evidence and saves the family from parking a large lump sum in the student’s account. This is a one-line request to your branch that prevents a real headache at lodgement.

OSHC bundling: the line nobody budgets for

Overseas Student Health Cover is compulsory for the full duration of your student visa, from the day you arrive to the day your visa ends. You cannot get the visa granted without it, and the policy has to cover the entire stay, not just the course. For a single student on a two-year Master’s, OSHC runs roughly AUD 1,300 to 1,600 across the two years, which is ₹71,500 to ₹88,000.

The bundling question is whether OSHC sits inside your loan or outside it. PSU banks will include OSHC as a covered head if you ask, since it is a mandatory visa cost, but it is easy to leave off the loan application and then find it as an out-of-pocket surprise. The university often arranges OSHC with a default provider and adds it to the CoE, which makes it cleaner to fund through the loan because it shows on the same document the bank is sanctioning against. If you arrange OSHC separately you can sometimes get it cheaper, but then it sits outside the CoE and you fund it from your own pocket or a separate tranche.

The practical move is to let the university bundle OSHC onto the CoE for the loan application, get the bank to fund it, and only switch providers later if you find the saving worth the paperwork. Modelling it as a loan head from the start keeps the funds evidence clean and stops the AUD 1,500 from becoming a June surprise.

PSU sanction limits and where the math breaks

The PSU education loan products that cover Australia follow the IBA framework on collateral and ceiling:

| Loan tier | Terms | Collateral required |

|---|---|---|

| Up to ₹4 lakh | Margin nil, no third-party guarantee | None |

| Above ₹4 lakh to ₹7.5 lakh | Third-party guarantee, parent co-applicant | Often no tangible collateral |

| Above ₹7.5 lakh to ₹1.5 crore (Global Ed-Vantage tier) | Tangible collateral mandatory (property, FD, LIC) | Yes, at 100 percent of loan amount |

The wall most Australia-bound students hit is right there. A two-year Monash Master’s costing ₹60 lakh total sits far above the ₹7.5 lakh unsecured ceiling at PSU banks, which means you either bring tangible collateral (typically property worth ₹60 lakh or more after the bank’s haircut) or you split the funding across a PSU loan up to ₹7.5 lakh plus family contribution, or you go to an NBFC for an unsecured top-up.

NBFCs (Avanse, HDFC Credila, Auxilo, InCred) sanction unsecured loans up to ₹40 to 75 lakh for ranked Australian universities against parent co-applicant income, but at interest rates 200 to 400 basis points higher than PSU floating rates, and without the CSIS subsidy benefit. The honest picture on NBFC versus PSU economics is in the education loan for abroad studies without collateral post.

Worked example: Monash Master’s, total cost vs PSU sanction

Take a real-shaped case. Student admitted to a Master of Information Technology at Monash, Melbourne, two-year coursework program, starting July 2025. Tuition AUD 45,000 a year, so AUD 90,000 across the course. Estimated total cost across both years AUD 1,08,000.

| Item | AUD (2 years) | INR (at 55) |

|---|---|---|

| Tuition (Monash, MIT) | 90,000 | 49,50,000 |

| Accommodation Melbourne (24 months) | 34,000 | 18,70,000 |

| Food + groceries | 11,000 | 6,05,000 |

| Transport, books | 4,000 | 2,20,000 |

| OSHC (single, 24 months) | 1,500 | 82,500 |

| Visa + biometrics | 1,700 | 93,500 |

| Flight + setup | 3,000 | 1,65,000 |

| Total cost | 1,45,200 | 79,86,000 |

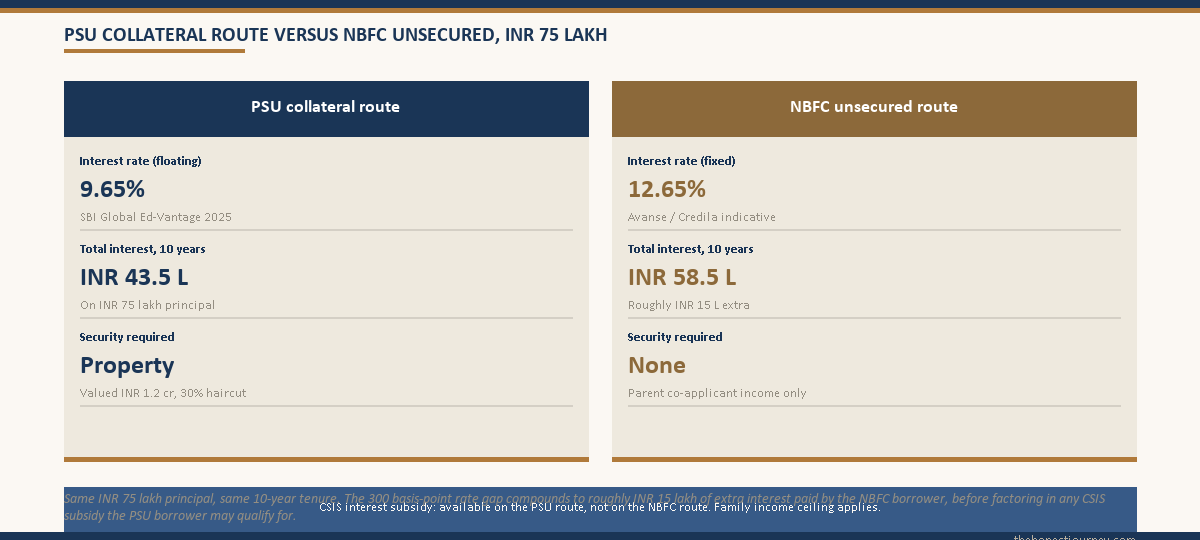

This student goes to SBI for a Global Ed-Vantage loan. The total ask is around ₹80 lakh. SBI can sanction the full amount because it sits inside the ₹1.5 crore Global Ed-Vantage ceiling, but because it is far above ₹7.5 lakh, tangible collateral is mandatory. The family pledges a residential property valued at ₹1.2 crore. SBI applies a haircut (commonly 25 to 30 percent), so the security value the bank counts is around ₹84 to 90 lakh, comfortably above the loan.

The CoE shows tuition of AUD 90,000, which the bank uses to size the tuition head. Tuition is wired to Monash’s account in semester tranches via SWIFT against the CoE. OSHC is bundled onto the CoE and funded by the loan. The living-expenses head is released as tranches to the student’s Australian bank account once it is open, and the SBI sanction letter naming all three heads serves as the GS savings evidence at visa lodgement.

If the family had no property to pledge, the same case at an NBFC would mean an unsecured sanction in the ₹60 to 75 lakh band against the parent’s income (typically needing CTC of ₹15 lakh or more and clean CIBIL above 750), at an interest rate of 12 to 13.5 percent versus SBI’s roughly 9.65 percent floating. Over a 10-year repayment, that 300 basis point gap on ₹75 lakh is roughly ₹14 to 16 lakh of extra interest, which is the number that should drive whether collateral is worth arranging.

The subclass 485 post-study visa and the repayment runway

The Temporary Graduate visa, subclass 485, is the post-study work visa that lets you stay and work in Australia after you finish. For loan-funded students it is the actual ROI window, because the repayment runway depends on how long you can earn in Australian dollars before the loan moratorium ends. The details on the 485 are published on immi.homeaffairs.gov.au, and they have moved more than once in recent years, so the honest framing matters.

For a Master’s by coursework, the Post-Higher Education Work stream of the 485 has typically given two to three years of stay-back, with the exact length tied to the qualification level and policy at the time you apply. The age limit and English requirements also apply. Two changes are worth flagging. The age cut-off for eligibility was lowered, and the extra stay-back that was offered for select STEM and regional graduates has been wound back. So do not model your repayment plan on the most generous version of the 485 you read about from an older batch. Check the current stream lengths on the official portal at the time you apply, because the runway between graduation and the first EMI is the single biggest variable in whether the loan stays comfortable.

The honest point is this. Australia works as a loan-funded destination when the post-study work window is real for your field. Software, data, engineering, nursing, accounting and the trades have defensible pathways in the Australian market. Outside those, the 485 window can pass without a graduate job that services an ₹75 lakh loan, and that is when families end up servicing EMIs from India. Treat the 485 as the repayment plan, not as a bonus.

Faz's ruleModel your repayment runway on the current subclass 485 stream length at the time you apply, not the version an older batch enjoyed. The stay-back has been trimmed, and your first EMI lands sooner than you think.

The gap between graduation and your first EMI is the most important number in the whole plan. If the 485 gives you two to three years of Australian-dollar earning before the moratorium ends, the loan stays comfortable. If your field has no clear path inside that window, the family services the EMI from India. Check the official portal, not a forum.

What banks check on Australia-specific paperwork at sanction

For an Australian university Master’s, the documents that go into the sanction file beyond the standard ones include:

- The unconditional offer letter from the Australian provider, on letterhead.

- The CoE once issued, showing the CoE number, CRICOS code, course dates and total tuition.

- The OSHC policy details, either bundled on the CoE or arranged separately.

- Proof that the provider is CRICOS-registered and the course is listed.

- The living-cost estimate, from the university or from studyaustralia.gov.au.

- For collateralised loans, the property documents and the empanelled valuer’s report.

The point banks scrutinise most is the alignment between the CoE tuition figure, the sanction amount and the visa funds requirement. The bank sizes tuition to the CoE, adds living and OSHC, and issues a sanction letter that should name all three so it doubles as the GS savings evidence. Get this triangle to line up before lodgement and the whole sequence runs smoothly. Leave any of the three loose and you end up reworking the file under time pressure with a visa deadline looming.

The honest take on Australia as a loan-funded destination

Australia works well as a loan-funded destination for an Indian student in a field with a real Australian job market, provided two things hold. One, the family can either pledge collateral for the amounts above ₹7.5 lakh or accept the higher NBFC rate and the lost CSIS subsidy. Two, the student treats the subclass 485 window as the actual repayment runway, not a fallback.

What does not work is treating Australia as a guaranteed migration path. The points-based skilled migration system is separate from the student and 485 visas, and it has tightened. Plenty of graduates finish the 485 window and return to India or move on without permanent residency. That is fine if the degree and the Australian-dollar earnings during study and post-study work have serviced a meaningful chunk of the loan. It is a problem if the entire loan math assumed a smooth path to PR that never materialised.

If your loan plan only works because you assumed three years of post-study work and a clear path to residency, redo the math with the current subclass 485 stream length and a conservative job-market view before you sign the sanction letter. The numbers should hold even if the optimistic version does not arrive. The full picture on borrowing limits across destinations is in the maximum education loan amount in India post.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for Australia is in the Australia student visa guide.

FAQ

What is the maximum education loan for Australia from Indian banks?

SBI Global Ed-Vantage and Bank of Baroda’s overseas product both sanction up to ₹1.5 crore for tier-1 destinations including Australia, provided collateral and co-applicant income support the amount. The unsecured ceiling at PSU banks stays at ₹7.5 lakh; anything above needs tangible security like property, FD or LIC. NBFCs such as Avanse and HDFC Credila sanction unsecured loans up to ₹40 to 75 lakh for ranked Australian universities against parent co-applicant income, at interest rates higher than PSU banks.

Do Indian banks sanction loans on the CoE for Australia?

Yes. The Confirmation of Enrolment is the document PSU banks treat as the spine of the Australia sanction file. The CoE shows the course, CRICOS code, dates and total tuition, and the bank sizes the tuition head to that figure. The sequencing trap is that the CoE needs an upfront tuition deposit before the university issues it, while the bank often wants the CoE before disbursing the balance. Map this order with your branch early to avoid a visa-timeline delay.

How much living cost do I need to show for an Australia student visa?

Under the Genuine Student requirement that replaced the Genuine Temporary Entrant test in 2024, the savings-evidence threshold was raised, and the current figure is published on immi.homeaffairs.gov.au for the subclass 500 visa. The cleanest way to satisfy it is a PSU bank sanction letter that explicitly covers tuition, living expenses and OSHC together, which shows funded capacity without the family parking a large cash balance in the student’s account for weeks before lodgement.

Is OSHC part of the education loan?

It can be, and it usually should be. Overseas Student Health Cover is compulsory for the full visa duration and runs roughly AUD 1,300 to 1,600 across a two-year Master’s. PSU banks will include OSHC as a covered head if you ask, since it is a mandatory visa cost. The cleanest route is to let the university bundle OSHC onto the CoE so it shows on the same document the bank sanctions against, then fund it through the loan rather than as an out-of-pocket surprise.

What is the Genuine Student requirement for Australia?

The Genuine Student requirement, the GS, replaced the older Genuine Temporary Entrant test in 2024. It asks the applicant to demonstrate, through targeted questions in the subclass 500 application, that they are coming primarily to study, with attention to course choice, circumstances, ties and understanding of visa conditions. It also raised the savings-evidence threshold. For loan-funded students, a sanction letter naming tuition, living costs and OSHC is the practical way to satisfy the funds side of the GS.

What is the subclass 485 post-study visa?

The Temporary Graduate visa, subclass 485, lets you stay and work in Australia after finishing your degree. For a coursework Master’s, the Post-Higher Education Work stream has typically given two to three years of stay-back, with age and English conditions. The stay-back lengths and the extra STEM and regional concessions have been trimmed since 2024, so check the current stream length on immi.homeaffairs.gov.au at the time you apply rather than relying on an older batch’s experience.

What is the total cost of a Master’s in Australia for Indian students?

One-year cost ranges from AUD 56,150 to AUD 82,600 depending on university and city. Tuition runs AUD 30,000 to 50,000, metropolitan accommodation AUD 15,600 to 19,200, food and groceries AUD 4,800 to 6,000, transport AUD 1,000 to 1,500, OSHC AUD 650 to 800, visa AUD 1,600, and books, setup and flight AUD 2,500 to 3,500. In INR at 1 AUD equals 55, that is roughly ₹30.9 lakh to ₹45.4 lakh a year. A two-year coursework Master’s roughly doubles the tuition and living lines.

Is a collateral-free education loan possible for Australia?

Up to ₹7.5 lakh from PSU banks without tangible collateral, but you still need a parent co-applicant. Beyond that, NBFCs like Avanse, HDFC Credila, Auxilo and InCred sanction unsecured loans up to ₹40 to 75 lakh for ranked Australian universities against co-applicant income, typically requiring parent CTC of ₹15 lakh or more and clean CIBIL above 750. Interest rates run 200 to 400 basis points higher than PSU floating rates, and you lose the CSIS interest subsidy. The trade-off is worth modelling on a 10-year repayment. The framework on rates is set by the RBI.

Faz · The Honest Journey · 2026