Health insurance for study abroad is mandatory for the student visa in every major destination, and your home-country travel insurance does not satisfy the requirement. The UK charges a flat Immigration Health Surcharge of GBP 776 per year at the visa stage, Australia mandates OSHC at AUD 600 to 850 per year, Germany requires statutory cover at around EUR 120 per month, and US universities bundle their own plans at USD 2,000 to 4,000 per year. Most policies exclude pregnancy in the first 12 months, pre-existing conditions and routine dental or vision.

When my younger cousin landed in Manchester for her master’s, she carried a glossy Indian travel insurance policy her father had bought at the airport, convinced she was covered. Six weeks in, she had a chest infection, walked into a GP surgery and learned that the policy was useless because she was already paying the NHS surcharge baked into her visa fee, and the travel policy did not cover anything past the first 90 days anyway.

This post walks through health insurance for study abroad country by country, what the visa rules actually require, what the policies cover and exclude, and where students keep losing money by buying the wrong thing.

Why home-country travel insurance does not count for any student visa

Student visa officers in the UK, Schengen states, Australia, New Zealand, Ireland and Canada all reject travel insurance bought in India as proof of health cover. The reasons are consistent across destinations. Travel policies are short-duration products, usually capped at 180 days. They cover emergencies and repatriation, not routine care, mental health, maternity or chronic-condition management. They pay the hospital after the fact rather than giving you access to a public or contracted private network. And they end the moment you become a resident for tax purposes, which in most countries happens at the 183-day mark.

The visa requirement is not just proof of insurance. It is proof of a specific kind of insurance: long-duration, in-country, contracted with either the public health system or a regulator-approved private insurer. A travel policy from an Indian general insurer cannot meet that test, no matter how comprehensive the wording looks. The visa officer is not reading the policy document. They are checking the issuer name against a country-specific list.

The same logic applies in reverse to overseas student insurance. Once you buy local cover, the home-country travel policy becomes redundant. Most families keep paying for both out of habit. You can cancel the Indian travel cover after the local policy is active and the residence permit is in hand.

United Kingdom: the IHS at the visa stage and how NHS access works

The UK does not run a separate student health insurance scheme. Instead, every visa applicant pays the Immigration Health Surcharge upfront when applying for the student visa, currently GBP 776 per year of the course duration. This is added to the visa fee and is non-refundable once the visa is granted. A two-year master’s plus the four-month grace period rounds up to three years of IHS, which is GBP 2,328 paid in one shot.

The surcharge gives you full access to the National Health Service from the day you land, on the same terms as a UK resident. GP visits are free, hospital treatment is free, prescriptions cost GBP 9.90 per item in England and are free in Scotland, Wales and Northern Ireland. The gov.uk healthcare immigration page has the live surcharge rate and the application steps.

What the IHS does not cover is routine dental beyond NHS-band emergency work, optical care, prescription glasses, and most fertility treatment. International students who want comprehensive dental and vision usually take a small top-up private policy at around GBP 15 to 30 per month. Pre-existing conditions are not excluded by the NHS itself, but if you arrive with a specific condition that needs an expensive specialist medication, the NHS may take three to six months to confirm prescription continuity.

Canada: provincial plans plus the UHIP gap in Ontario

Canada is the most fragmented of the major destinations because health insurance is provincial. British Columbia (MSP), Alberta (AHCIP), Saskatchewan and Manitoba enrol international students into the provincial plan after a waiting period of one to three months, usually free or at a nominal cost. Quebec has its own provincial plan (RAMQ) and treats Indian students under the bilateral social-security framework, meaning most Indian students pay into a private group plan instead.

Ontario is the destination that catches the most students out. The provincial plan (OHIP) does not cover international students at all. Every Ontario university enrols students automatically into the University Health Insurance Plan, billed at around CAD 756 per year for a single student and added to the tuition invoice. UHIP is contracted with Sun Life and covers GP visits, specialist referrals, emergency room, hospital admission and most prescriptions, with the standard exclusions for pregnancy in the first 12 months, pre-existing conditions and dental or vision.

Most Canadian universities also bundle a separate student union health and dental plan on top of the provincial or UHIP layer, costing CAD 200 to 400 per year. This is where dental cleanings, glasses and mental-health counselling get covered. You can opt out of this top-up if you can show equivalent private cover, but you cannot opt out of UHIP or the provincial plan. The canada.ca study pages outline how provincial enrolment works for new arrivals.

Faz's ruleCheck whether your destination province enrols international students into the public plan or makes you buy private cover. The cost gap is CAD 700 to 800 per year and it changes the math on where you study.

A friend’s daughter chose between Waterloo (Ontario, UHIP mandatory) and McMaster (also Ontario, also UHIP) versus an Alberta option. Once she added UHIP to Ontario tuition, the cost difference shrank. Nobody at the application stage flagged this, and most counsellors do not either. The provincial layer matters.

United States: the university plan you cannot opt out of unless you have equivalent cover

US universities run their own mandatory student health insurance plans, billed directly to your student account at the start of each semester or year. The cost runs USD 2,000 to 4,000 per year depending on the university, with private research universities like Columbia, NYU and USC at the top of the range and large public universities like Texas A&M or UIUC at the lower end.

The plans are usually administered by Aetna, UnitedHealthcare, BlueCross or Cigna under the university’s branding. Coverage includes the on-campus health centre at no extra cost, referrals to in-network specialists, emergency room visits with a copay (typically USD 100 to 250), hospital admission, and prescriptions through a contracted pharmacy. Mental-health counselling on campus is usually free for the first 8 to 12 sessions. Pregnancy is covered after a waiting period that varies by plan.

You can opt out of the university plan only if you can show equivalent or better private cover that meets the school’s published waiver standards. The waiver standards are deliberately strict: minimum annual benefit of USD 500,000, medical evacuation cover, low deductibles, and the policy must be from a US-licensed insurer. Indian or international travel policies almost never qualify. Some Indian banks and education loan NBFCs have started offering bundled US-licensed plans, but pricing is rarely cheaper than the university plan once you add comparable benefits.

The visa itself, the F-1, does not require proof of insurance at the embassy stage. The university enforces the requirement after you arrive, and you cannot register for classes the next semester if your insurance has lapsed.

Germany: statutory public versus private and the EUR 120 monthly reality

Germany makes student health insurance mandatory for university enrolment and for the residence permit. The default option for non-EU students under 30 is statutory public health insurance (gesetzliche Krankenversicherung) through one of the Krankenkassen, the most common being TK (Techniker Krankenkasse), AOK and Barmer. Public student rates are roughly EUR 120 to 130 per month, fixed by federal regulation, regardless of which Krankenkasse you choose.

Public cover gives you full access to the German health system: GP visits, specialists, hospital admission, prescriptions at small copays, dental basics, mental-health treatment with a referral. The plan stays valid as long as you are enrolled as a student under 30. After 30, or if you switch to a non-student visa category, you move to the regular adult statutory rate (around EUR 200 to 250 per month).

Private student insurance (often marketed under brand names like Mawista or Care Concept) is cheaper at around EUR 35 to 60 per month, but it is a short-term bridge product, designed for language-course students or those preparing for university enrolment. The catch is that once you accept private cover at the start of your stay, German law makes it very difficult to switch back to public cover later in your studies, even if your situation changes. The standard advice from the DAAD is to take public cover from day one for degree programs and use private cover only for short pre-university stays.

Exclusions on public student plans are minimal: cosmetic dental, premium private hospital rooms, alternative medicine beyond what is reimbursed by statute. Pre-existing conditions are covered with no waiting period.

Australia: OSHC, the providers, and the bundled visa requirement

Overseas Student Health Cover is a visa condition for the subclass 500 student visa. You must hold OSHC for the entire duration of your visa, and the policy must come from one of the five approved providers (Bupa, Medibank, Allianz Care, nib, ahm). Annual cost is AUD 600 to 850 for a single student, depending on the provider and the level of cover, and you typically pay upfront for the full visa period at the time of visa application.

OSHC covers GP visits (with rebates that often leave a small out-of-pocket gap), public hospital care, ambulance, most prescriptions, and emergency dental. The standard exclusions apply: pregnancy is covered only after a 12-month waiting period, pre-existing conditions have a 12-month waiting period for related claims, routine dental and optical are not covered. Most students add a small Extras policy at around AUD 200 to 400 per year for dental cleanings, glasses and physiotherapy.

The visa requires the OSHC start date to match the visa grant date and the end date to be at least to the end of the course plus the visa grace period. If you let the policy lapse, you breach visa condition 8501 and can have the visa cancelled. The privatehealth.gov.au portal lists every approved provider and the standardised benefits table.

Faz's ruleBuy OSHC for the full visa period from a single provider, not in yearly chunks from different providers. The 12-month waiting period for pre-existing conditions resets if you switch insurers.

Students try to save AUD 50 to 100 by changing providers between years one and two of a Master’s. The waiting periods then restart, so a condition that would have been covered in year two is suddenly excluded again. Pick the provider once based on hospital network in your city and stay put.

Ireland: private cover at the visa stage and what the rules actually demand

Ireland requires non-EU students to hold private medical insurance for the duration of the residence permit. There is no public student health scheme for non-EU students. Cost runs EUR 150 to 300 per year for the standard student plans, sold by providers like StudyAndProtect, Allianz Care and VHI. The policy must cover hospital admission, GP care and prescription drugs, and must be valid in the Republic of Ireland.

You buy the policy before applying for the IRP (Irish Residence Permit) card, present it at the registration appointment alongside the proof of EUR 10,000 in your account, and renew it each year when the IRP is renewed. The inis.gov.ie guidance lists the minimum benefit standards: a single inpatient stay must be covered, day-case treatment, and full repatriation in case of death.

The exclusions are similar to other countries: pregnancy first 12 months, pre-existing conditions usually with a 12-month waiting period, routine dental and vision. Mental-health treatment is covered up to a low annual cap (typically EUR 1,500 to 3,000), which is one of the weaker points compared to NHS or German statutory cover. Students with ongoing mental-health needs sometimes pay out of pocket for a private therapist in addition to the policy.

New Zealand: mandatory insurance and the limited public access

New Zealand requires international students to hold approved medical and travel insurance for the duration of the student visa, billed at NZD 600 to 850 per year. Approved providers include Studentsafe, Uni-Care, OrbitProtect and Southern Cross. Universities usually bundle the insurance into the tuition invoice or require proof at enrolment.

Public healthcare in New Zealand is funded through ACC for accident-related treatment, which does cover international students for accident injuries. But routine illness, GP visits, hospital admission for non-accident conditions and prescriptions are not covered by the public system for student visa holders. The private student policy fills that gap. The immigration.govt.nz visa pages list the cover requirement and the approved insurer list.

Exclusions follow the same pattern: pregnancy first 12 months, pre-existing conditions usually with a waiting period or a higher premium, dental and optical not covered. The one New Zealand specific note: adventure sports and skiing accidents are sometimes excluded from the cheaper student plans, which matters because students do travel and ski. Confirm the activity cover in the policy schedule before buying.

What is commonly excluded across every country

Across the UK NHS, Canadian provincial plans, US university plans, German statutory, Australian OSHC, Irish private and New Zealand approved policies, the exclusion list converges:

| Exclusion | Typical rule | What it means in practice |

|---|---|---|

| Pregnancy in the first 12 months | 12-month waiting period before maternity benefits trigger | If you become pregnant in year one, the policy will not pay for delivery or prenatal care |

| Pre-existing conditions | 12-month waiting period or higher premium; full exclusion on cheaper plans | Asthma, diabetes, thyroid, depression already diagnosed in India may not be covered |

| Routine dental | Not covered on base plan; available as separate Extras at extra cost | Cleanings, fillings, root canal paid out of pocket unless you add a dental policy |

| Routine optical | Not covered on base plan | Eye tests and glasses paid out of pocket |

| Cosmetic and elective | Always excluded | Procedures done by choice rather than medical necessity |

| Fertility treatment | Usually excluded or capped | IVF and assisted reproduction limited or full out-of-pocket |

The pre-existing conditions clause is the one that costs students the most money. If you have asthma, thyroid, depression, ADHD or any condition for which you took prescription medication in India in the 12 months before departure, declare it on the application. Hiding it and then claiming later is a clean path to a rejected claim and sometimes a cancelled policy. Most insurers will issue cover with a waiting period or a small premium loading rather than refuse.

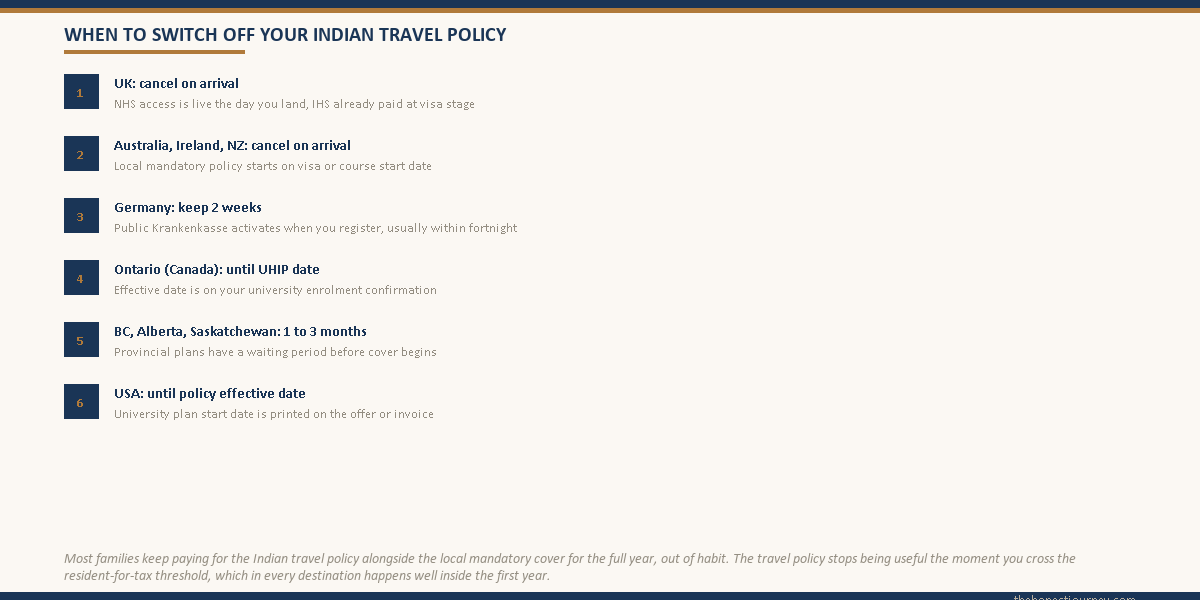

When to switch from a home-country travel policy to the local plan

Most families buy a 30 to 90-day travel policy from an Indian insurer for the journey out, and that is reasonable as a bridge. The travel policy covers the flight, the first few days of arrival, the initial accommodation period, and the gap before the local policy activates. The mistake is keeping it running for the full year.

The switch points by country:

UK. The NHS access is automatic from the day you land, since the IHS was paid at the visa stage. Cancel the travel policy on arrival.

Canada. Provincial plans have a one to three-month waiting period in BC, Alberta and Saskatchewan. Keep the travel policy active until provincial cover begins, then cancel. In Ontario, UHIP starts on the date listed on the university enrolment confirmation, usually 2 to 4 weeks before classes begin.

US. The university plan activates on the policy effective date in your offer letter, usually a few days before orientation. Cancel travel cover after that date.

Germany. Public student insurance activates the day you sign up with the Krankenkasse, which you usually do within the first two weeks of arrival as part of the residence-permit registration. Travel cover is the bridge for those first two weeks only.

Australia, Ireland, New Zealand. The local mandatory policy starts on visa or course start date, so the travel policy is only needed for the journey itself.

For a full breakdown of the costs around visa, insurance and the first few months in each destination, the cost of studying in UK for Indian students, cost of studying in Canada and cost of studying in USA posts have country-specific budget worked examples, and the proof of funds for student visa guide covers the bank balance side of the visa file.

Faz's ruleDeclare every pre-existing condition on the insurance application. The waiting period or small premium loading is cheaper than a rejected claim three years later.

I have seen two cases of claim rejection because a student did not declare a thyroid condition or a previous depression diagnosis. The insurer pulled medical history from the home-country GP records during the claim review and voided the policy. Disclose everything, even the things that feel embarrassing or minor.

The honest closing take

Health insurance for study abroad is one of those line items families treat as a checkbox on the visa application. The cheapest policy that gets the visa stamped feels like the right answer. It usually is not. A USD 2,500 university plan with a contracted on-campus health centre, mental-health counselling included and a clear network of specialists is worth more than a USD 1,500 third-party plan with high deductibles and a thin network.

The math gets clearer when you treat health insurance as part of the total cost of education rather than a separate expense. Add the annual premium to the tuition, look at the all-in number, and the gap between the university plan and the cheapest waiver-compliant alternative is rarely worth the trade-off in coverage and friction.

The students who handle this well are the ones who read the policy schedule, understand the exclusions, declare their medical history honestly when they sit the medical test required for the student visa, and know which clinic or hospital to walk into on day one. The ones who struggle are the ones who carried an Indian travel policy assuming it would do, or skipped the dental top-up to save USD 200 and then paid USD 800 for a single filling.

FAQ

Is health insurance mandatory for student visa?

Yes, in every major study destination. The UK collects the Immigration Health Surcharge at the visa application stage, currently GBP 776 per year of the course, which gives NHS access. Australia requires OSHC for the duration of the subclass 500 visa. Germany mandates statutory or approved private cover for enrolment and the residence permit. Ireland and New Zealand require private cover before issuing the residence permit. Canada and the US enforce it through provincial plans or university mandates after arrival rather than at the visa stage.

How much is UK NHS surcharge for students?

The Immigration Health Surcharge for students is GBP 776 per year of the visa, including the post-study grace period, paid as a single upfront amount with the visa application. A one-year master’s plus the four-month grace period rounds to two years, so GBP 1,552. A two-year course with grace rounds to three years at GBP 2,328. The surcharge is non-refundable once the visa is granted and gives full NHS access from day one with no waiting period.

Is OSHC mandatory in Australia?

Yes. Overseas Student Health Cover is a hard requirement for the subclass 500 student visa, attached to visa condition 8501. The policy must come from one of the five approved providers (Bupa, Medibank, Allianz Care, nib, ahm), must cover the entire visa period including the buffer at the end, and must start on or before the visa grant date. Single-student cover costs AUD 600 to 850 per year. Letting OSHC lapse is grounds for visa cancellation.

Is German public health insurance compulsory for students?

Public health insurance is compulsory for university enrolment and the residence permit, and for non-EU degree students under 30 it is also the default option. Rates are fixed at around EUR 120 to 130 per month across providers like TK, AOK and Barmer. Private student insurance is allowed but is usually only suitable for short pre-university stays. Once you accept private cover, switching back to public during your studies is administratively very difficult, so degree students should take public from day one.

What does student health insurance NOT cover?

Across every major destination, student plans exclude pregnancy in the first 12 months, pre-existing conditions (usually with a 12-month waiting period or a premium loading), routine dental cleanings and treatment, routine optical care including eye tests and glasses, cosmetic procedures, and most fertility treatment. Mental-health cover varies: NHS and German statutory cover it broadly, US university plans include 8 to 12 sessions on campus, OSHC and Irish private plans cover it with annual caps. Always read the schedule of exclusions in the policy document.

Does Indian travel insurance count for student visa?

No. Student visa officers in the UK, Schengen states, Australia, New Zealand, Ireland and Canada reject travel policies bought in India as proof of student health cover. Travel policies are short-duration, capped at around 180 days, cover only emergencies and repatriation, and end when you become a tax resident in the destination country. The visa requires long-duration in-country cover from either the public health system or a regulator-approved private insurer. A travel policy is fine as a bridge for the first 2 to 4 weeks only.

What is UHIP in Ontario and is it mandatory?

The University Health Insurance Plan is the mandatory private health plan for international students at all Ontario universities, since the provincial OHIP plan does not cover non-residents. UHIP is contracted with Sun Life, costs around CAD 756 per year for a single student, and is added automatically to your university tuition invoice. It covers GP visits, specialist referrals, emergency room, hospital admission and most prescriptions. You cannot opt out. Other provinces like BC, Alberta and Saskatchewan enrol international students into the public plan instead.

When should I switch from Indian travel insurance to local cover?

Switch as soon as the local mandatory cover activates. In the UK, that is the day you land since the IHS was paid at the visa stage. In Germany, within the first two weeks when you sign up with a Krankenkasse. In Ontario, on the UHIP effective date in your university enrolment confirmation. In BC, Alberta and Saskatchewan, after the provincial waiting period of one to three months ends. In Australia, Ireland and New Zealand, the local policy starts on visa or course start date, so the travel cover is only needed for the flight and first few days.

Faz · The Honest Journey · 2026