An education loan against property (LAP) typically cuts your interest rate from around 12 percent unsecured to 9 to 10 percent secured, which saves ₹7 lakh to ₹10 lakh on a ₹40 lakh, 10 year loan. The lender funds up to 65 to 70 percent of the flat’s market value. It only makes sense above ₹20 lakh and when the property is fully paid off.

A father in Pune called me with a question that comes up often. His daughter had an admit to a UK master’s program, total cost ₹48 lakh, and the SBI unsecured offer had landed at 12.25 percent. He owned a flat in Baner, fully paid off, market value ₹1.4 crore. Could he pledge the flat and bring the rate down?

Yes. The longer answer, which nobody at the branch had walked him through, is what this post is about. An education loan against property (LAP) can save ₹7 lakh to 10 lakh in interest on a typical abroad-studies amount, but the family home goes on the line. Honest math, honest friction, honest decision frame.

An education loan against property is a secured loan where you pledge a residential or commercial property as collateral. Interest rates run 8.5 to 10 percent versus 12 to 14 percent on unsecured loans, amounts go up to 60 to 70 percent of property value, and tenure stretches to 10 to 15 years. The catch: a default puts the property at risk under SARFAESI.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on collateral and how much you can borrow: the maximum education loan amount india post.

What an education loan against property actually is

Two routes lead to the same destination, and they get confused all the time. The first is a regular education loan that simply uses property as collateral. The bank still treats it as an education loan product, with a moratorium, Section 80E benefits, and education-loan-style disbursement to the institution. The second is a pure loan against property (LAP) where the bank lends you a lump sum against the property and you decide where it goes, including education. Same collateral, different product mechanics.

The first option is what most public sector banks offer on amounts above ₹7.5 lakh: SBI Scholar, Bank of Baroda Vidya, PNB Saraswati, BoI Star Vidya. The rate sits at 8.5 to 10 percent depending on co-applicant CIBIL. Property is registered with a memorandum of deposit of title deeds (MODT), released only on full repayment. The IBA model education loan scheme is the reference framework public banks follow.

The second option, a standalone LAP routed to education, lives at every bank and NBFC. Rates 9 to 11 percent. No moratorium. EMIs start the month after disbursement. You lose tax benefits unless the lender markets the product as an education loan.

Faz's ruleA secured education loan and a LAP routed to education are not the same product.

The first keeps the moratorium and the Section 80E benefit. The second gives you a lump sum to spend, no moratorium, EMIs from month one. Ask which one the branch is actually selling you before you sign anything.

The math: LAP at 9 percent vs unsecured at 12 percent

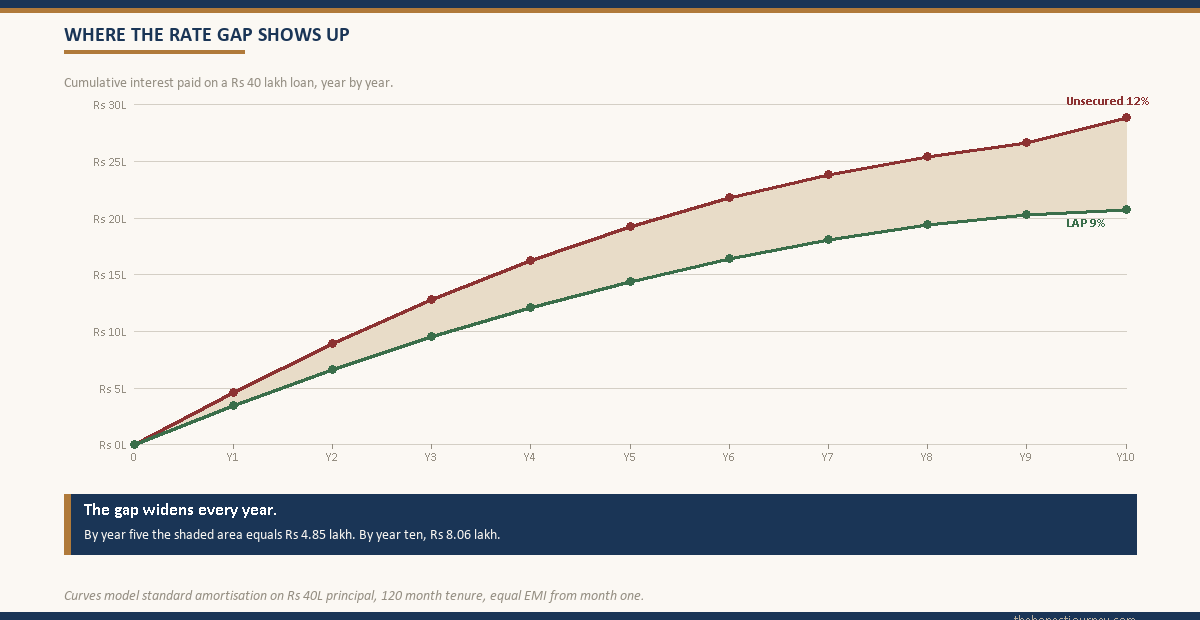

Let me run the case that comes up most often. A ₹40 lakh loan, 10-year tenure, EMI-from-month-one (assume the student is already abroad or the family is servicing interest, so we are comparing on equal terms). The unsecured offer at 12 percent versus the LAP-style secured offer at 9 percent.

| Variable | LAP at 9 percent | Unsecured at 12 percent |

|---|---|---|

| Principal | ₹40,00,000 | ₹40,00,000 |

| Tenure | 120 months | 120 months |

| Monthly EMI | ₹50,668 | ₹57,388 |

| Total repaid | ₹60,80,160 | ₹68,86,560 |

| Total interest | ₹20,80,160 | ₹28,86,560 |

| Interest saved with LAP | ₹8,06,400 | |

Roughly ₹8 lakh saved over the loan, EMI ₹6,720 lighter. On a 15-year tenure, the gap widens to about ₹13.5 lakh because compounding has more time. That is why LAP gets pushed hard when relationship managers see a clean property document on file.

Two caveats. The 9 percent rate assumes co-applicant CIBIL above 750 and no title disputes. Murkier files land at 9.5 to 10.5 percent, narrowing the gap to ₹5 lakh to 6 lakh. The 12 percent unsecured assumes a public sector bank on a premier-list university. NBFC unsecured rates run 12.5 to 13.5 percent, widening the LAP advantage. Run your own numbers.

What property qualifies, and what does not

Banks accept residential (self-occupied or rented) and commercial property, and sometimes industrial property or vacant land. They do not accept agricultural land in most cases, ancestral property with unclear title, property with a sitting tenant under old Rent Control acts, or property in a society where the share certificate is missing. Under-construction property is accepted only if the builder is RERA-registered and the loan is structured as a tripartite agreement.

Loan-to-value ratios sit at 60 to 70 percent for residential, 50 to 60 percent for commercial, and 40 to 50 percent for industrial or vacant land. On the Pune flat (market value ₹1.4 crore), the maximum drawable would be ₹84 lakh to ₹98 lakh, plenty for a ₹48 lakh requirement. Fair market value is what the bank-empanelled valuer writes after a site visit, not the neighbour’s asking price. Valuers run conservative, so build your calculation off the report figure.

The friction: title report, valuation, time, cost

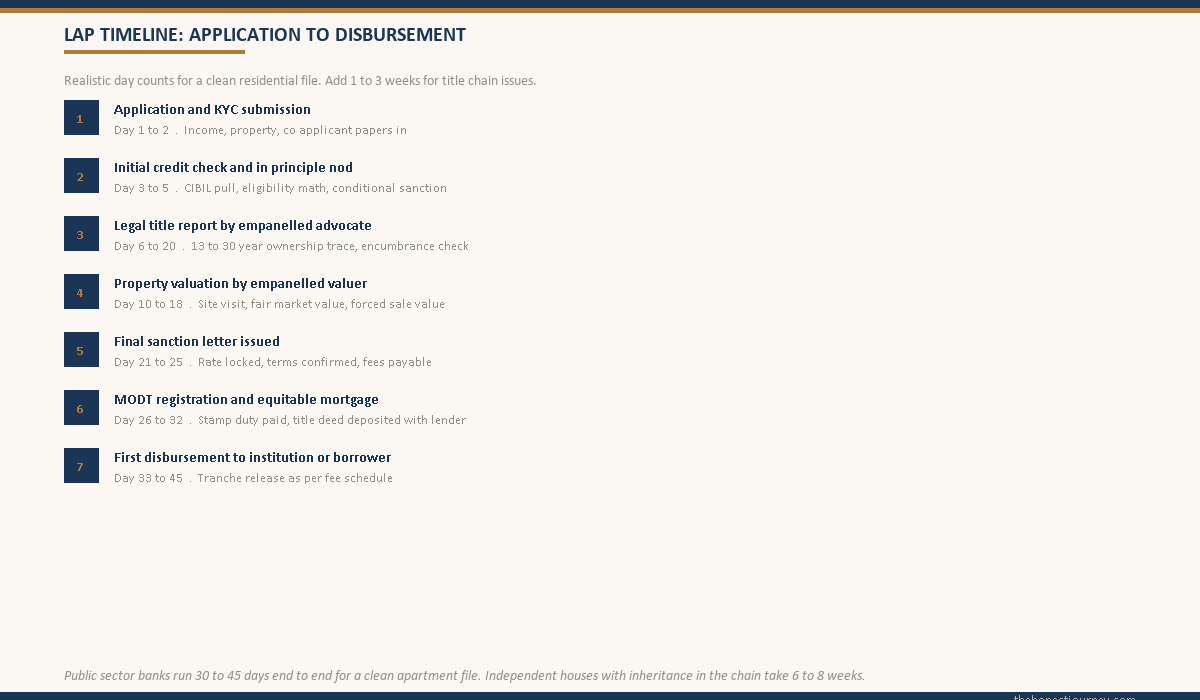

A secured education loan or LAP routed to education is not a 14-day process. It is a 30 to 45 day process, sometimes longer if the title chain has gaps.

The legal title report is done by a bank-empanelled advocate. It traces ownership for the last 13 to 30 years, checks for encumbrances, confirms the property is free from litigation, and verifies that each seller had the right to sell. An apartment in a planned society takes 10 to 14 days. An independent house with a partition or inheritance in the chain takes 3 to 4 weeks. Cost: ₹3,000 to ₹8,000.

The valuation report is separate. A bank-empanelled valuer visits the property, measures it, photographs it, and writes a report with fair market value and forced sale value. Cost: ₹5,000 to ₹15,000. Time: 7 to 10 days.

Then the registration charges. The MODT gets stamped at 0.1 to 0.5 percent of the loan amount (Maharashtra 0.3 percent capped at ₹20,000, Karnataka 0.5 percent, Delhi 0.15 percent). On ₹40 lakh in Maharashtra, MODT stamp duty alone is ₹12,000 to ₹20,000. Add processing fees of 0.5 to 1 percent (₹20,000 to ₹40,000) and you are looking at ₹50,000 to ₹80,000 in pre-disbursement costs. SARFAESI procedures and lender obligations are governed by RBI master directions on recovery and asset classification.

| Cost head | Typical range |

|---|---|

| Legal title search | ₹3,000 to ₹8,000 |

| Valuation report | ₹5,000 to ₹15,000 |

| Processing fee (0.5 to 1 percent) | ₹20,000 to ₹40,000 on ₹40L |

| MODT or equitable mortgage stamp duty | ₹4,000 to ₹20,000 (state dependent) |

| Documentation and notary | ₹2,000 to ₹5,000 |

| Total upfront cost (₹40L loan) | ₹34,000 to ₹88,000 |

Compare this to an unsecured SBI Global Ed-Vantage where the processing fee is ₹10,000 plus GST and disbursement happens in 10 to 14 days. The LAP saves ₹8 lakh over 10 years but costs an extra ₹50,000 upfront and 3 to 4 weeks of waiting. If your semester starts in 6 weeks, the math is no longer about interest, it is about whether the visa will be stamped in time.

The real risk: the family home on the line

This is the part the rate calculator does not show. When the borrower defaults on an unsecured education loan, the bank’s recovery options are limited: file a money suit, send recovery agents, damage CIBIL, drag civil courts for years. They cannot directly take any asset because none was pledged. The pressure is real but the family asset stays intact.

When you default on a secured education loan or LAP, the options change completely. After 90 days of non-payment (NPA classification), the lender can invoke SARFAESI, 2002: a 60-day notice under Section 13(2), followed by possession under Section 13(4) if dues are not cleared. The bank can then auction the property to recover the loan. The borrower’s right to redeem survives until the auction notice is published, after which it ends.

Stare at the math directly. ₹8 lakh in interest savings over 10 years is roughly ₹80,000 per year on the EMI line. Against that, you are putting a ₹1.4 crore family home into the recovery chain if the loan goes bad. If the earning trajectory is stable, this is an acceptable trade. If the course outcome is uncertain (low-ranked program, saturated job market, restrictive post-study visas), this trade needs serious thought.

Faz's ruleThe rate saving is on the EMI. The risk is on the address.

₹8 lakh saved over 10 years sounds large until you put it next to the value of the home you grew up in. If the loan goes bad on an unsecured product, your CIBIL takes the hit. If it goes bad on a LAP, the bank can take the flat. That asymmetry is the whole conversation.

Tenure, prepayment, and the 80E question

LAP tenure flexibility is underrated. Unsecured education loans cap at 10 to 15 years. LAP can stretch to 20 years. A ₹40 lakh LAP at 9 percent over 20 years has an EMI of ₹35,989 versus ₹50,668 over 10 years, but total interest jumps from ₹20.8 lakh to ₹46.4 lakh. Useful if cash flow is the bottleneck, expensive if you forget to prepay once income stabilises. See the education loan interest rate comparison post for prepayment mechanics. RBI scrapped prepayment penalties on floating-rate retail loans, so default to floating.

Section 80E (deduction on education loan interest, unlimited amount, 8-year window) applies only to loans booked as education loans. A secured education loan with property collateral qualifies. A pure LAP routed to education does not, because the Income Tax Act ties the deduction to a loan booked as an education loan “for the purpose of higher education.” Ask the branch in writing which product code appears on the sanction letter.

Use LAP when, do not use LAP when

The frame I use. Not a flowchart, just conditions to check honestly.

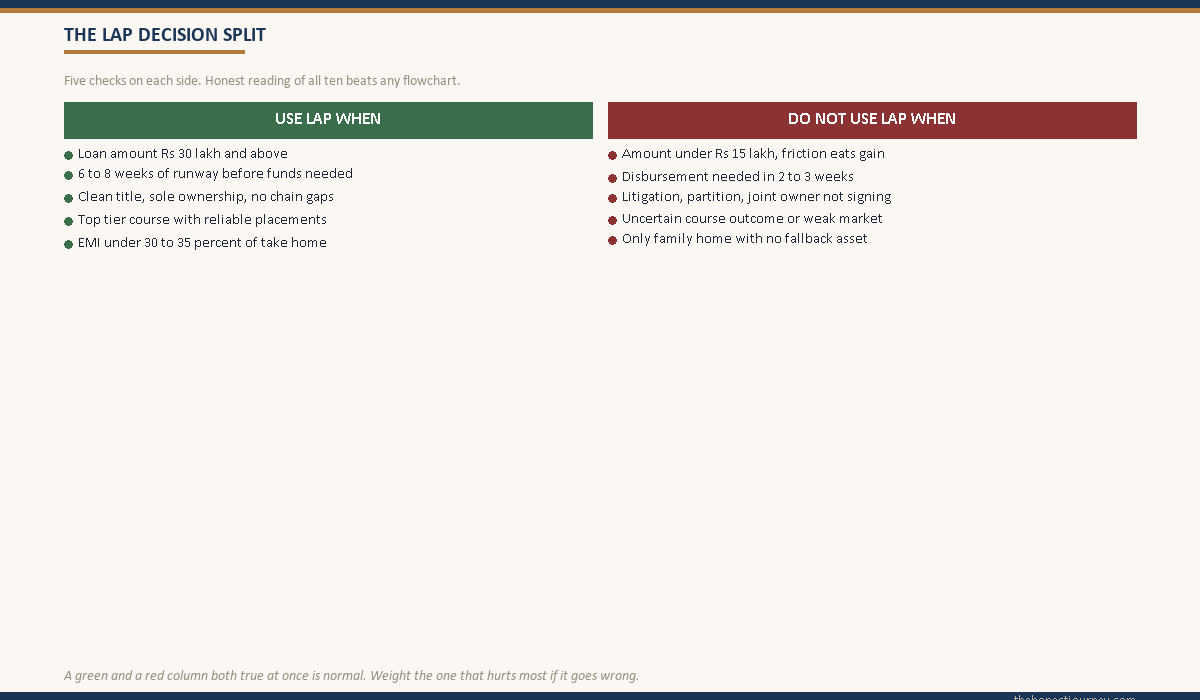

Use LAP when:

- The loan amount is ₹30 lakh and above, where the 3 percent rate gap creates ₹6 lakh-plus in lifetime savings.

- You have 6 to 8 weeks of runway before funds are needed.

- The property is clean, in your own name, with a trail that will pass title search.

- The course is at a top-tier institution with reliable placement outcomes.

- Co-applicant income is stable and EMI sits comfortably below 30 to 35 percent of take-home.

Do not use LAP when:

- The amount is under ₹15 lakh, where savings do not justify the friction and upfront costs eat the gain.

- You need disbursement in 2 to 3 weeks. The title and valuation cycle will not collapse.

- The property has red flags: litigation, partition issues, missing share certificate, joint ownership with a relative who has not signed.

- The course outcome is uncertain. A low-ranked program in a saturated market is not a place to put the family home as collateral.

- The property is the only family residence with no fallback. EMI affordability needs a wider buffer when the downside is homelessness, not just CIBIL damage.

The middle ground: if the amount is ₹20 lakh to ₹30 lakh and you are on the fence, the partial-collateral route from SBI or BoB lets you pledge property up to the loan value at a rate between full unsecured and full secured (usually 10 to 11 percent). More on this in the secured versus unsecured education loan post, and on collateral-free options in the education loan for abroad studies without collateral post.

Faz's ruleIf the answer to do you need it in 2 weeks is yes, LAP is not your product.

The interest savings are real but they live in the tenure, not the disbursement window. Forcing a title search and valuation into a tight visa timeline is how families end up missing semester start. Choose the route that matches your clock, not just your rate sheet.

The honest closing take

The trade-off is not subtle. A 3 percent rate reduction on ₹40 lakh is ₹8 lakh over a decade. Significant. Also the price you pay for not putting the home into the recovery chain if life goes sideways.

An unsecured loan at 12 percent is more expensive but fundamentally less dangerous for the family balance sheet. If the borrower cannot pay, the worst case is CIBIL damage, recovery agent pressure, a possible settlement at 60 to 70 cents on the rupee, and eventual closure. The address on the property card does not change.

The decision is not “which is cheaper.” It is “what risk does my family run if this goes wrong, and is the saving worth that risk.” For families with multiple properties, stable co-applicant income, and a high-confidence course outcome, LAP is rational. For families where the pledged property is the only home or the course outcome is uncertain, the extra interest on the unsecured loan is the premium you pay for keeping the asset out of recovery. That premium is insurance, not a mistake. Margin money mechanics on the secured route are in the margin money education loan post.

Run the math on your specific rates. Walk into the branch with two sanction letters if you can. Ask what happens to your CIBIL versus your property in each default scenario. The answers will tell you which product fits your family, not just the rate sheet.

FAQ

Can I take a loan against property to fund education in India?

Yes. Most banks and NBFCs offer LAP products where funds can be used for any legitimate purpose including education. You can also take a secured education loan where the bank specifically books the product as an education loan with property collateral. The second route preserves Section 80E benefits and the moratorium, while a pure LAP does not. The IBA model scheme covers the education loan variant.

What is the interest rate on an education loan against property?

Secured education loans against property from public sector banks like SBI, BoB, PNB, and BoI typically range from 8.5 to 10 percent per annum, depending on co-applicant CIBIL and property quality. Pure LAP products from the same banks run 9 to 11 percent. Compare this with unsecured education loans at 12 to 14 percent. The 3 to 4 percent differential is the central reason families consider pledging property.

How much loan can I get against my property?

Banks lend 60 to 70 percent of fair market value on residential property, 50 to 60 percent on commercial, and 40 to 50 percent on industrial or vacant land. Fair market value is set by a bank-empanelled valuer’s report, not the owner’s estimate. On a property valued at ₹1.4 crore, the maximum drawable is roughly ₹84 lakh to ₹98 lakh, well above most education funding needs.

How long does an education loan against property take to disburse?

Plan for 30 to 45 days from application to first disbursement. The legal title report takes 2 to 3 weeks (longer if the chain has gaps), valuation takes 7 to 10 days, and MODT registration adds 5 to 7 days. If your visa or semester deadline is under 4 weeks away, the LAP timeline will not collapse to fit. An unsecured loan from SBI Global Ed-Vantage typically disburses in 10 to 14 days.

What are the upfront costs of taking a loan against property?

Budget ₹35,000 to ₹90,000 on a ₹40 lakh loan: legal title search ₹3,000 to ₹8,000, valuation ₹5,000 to ₹15,000, processing fee at 0.5 to 1 percent, MODT stamp duty at 0.1 to 0.5 percent depending on state, and documentation charges. These are paid before disbursement. Some lenders allow the processing fee to be deducted from the first disbursement.

What happens if I cannot repay an education loan against property?

After 90 days of non-payment, the loan is classified as a non-performing asset (NPA) and the bank can invoke SARFAESI. You receive a 60-day notice under Section 13(2), and if dues are not cleared, the bank can take possession under Section 13(4) and auction the property. This is the central risk difference versus an unsecured loan, where recovery stops at civil suits and CIBIL damage. On a LAP default, the family home is in the recovery process.

Is Section 80E tax benefit available on a loan against property used for education?

Only if the bank books the product as an education loan. Section 80E ties the deduction to a loan from a recognised financial institution “for the purpose of higher education” booked as an education loan. A secured education loan with property collateral qualifies. A pure LAP routed to education does not, because the product code is LAP, not education loan. Ask the branch in writing which product code appears on the sanction letter before you sign.

What if my property has title issues or pending litigation?

The legal title report surfaces these, and the bank will either reject the loan or require resolution before sanction. Common deal-breakers: missing share certificate, partition disputes, unresolved succession, joint ownership where a co-owner has not signed, encroachment, and pending litigation. Some issues can be cured (probate certificate, registered family settlement) but the timeline stretches to 2 to 6 months. If you need funds quickly, an unsecured route is more viable.

Faz · The Honest Journey · 2026