An education loan for MBBS in the Philippines, Bangladesh or Nepal from an Indian PSU bank is sanctioned only when the specific college sits on the current NMC route and the course satisfies the NMC FMG Regulations 2021 (at least 54 months of medical instruction plus a 12-month internship in the same country). SBI Global Ed-Vantage, Bank of Baroda and Canara Bank are the lenders that regularly fund this route, with all-in cost landing between ₹25 lakh and ₹45 lakh for the full degree. The bank checks the college’s NMC status on the date of sanction, not the date the agent printed the brochure.

Last admission season a father from a small town in Bihar sent me a Philippines MBBS package that read like a holiday deal: tropical campus, English everywhere, a friendly EMI plan, and an agent’s line that the loan would clear “no problem” because the college was “100 percent NMC approved”. I asked him one question. Did the agent show him where, on a government website, that approval was written down? He could not answer it. Neither, when I checked, could the agent.

The South and Southeast Asia MBBS route is real and it is legitimate. For families who cannot buy a domestic government seat with their NEET rank and cannot stomach a crore-plus private Indian fee, the Philippines, Bangladesh and Nepal are genuine options. But the loan rests on the same regulation as every other foreign MBBS, and these three countries each carry a structural quirk that trips families up. This post is the companion to my CIS-country MBBS loan post, and the same NMC logic governs both.

More on funding an MBBS abroad: the education loan for MBBS abroad post, the education loan for MBBS government college post, and the education loan for MBBS private college post.

The rule that decides everything: NMC FMG Regulations 2021

Before any cost table, any bank conversation, any agent pitch, the regulation that decides whether your foreign MBBS lets you practise in India is the National Medical Commission’s FMG Regulations 2021. PSU banks read this regulation directly. If a graduate cannot register with the NMC, the loan becomes an unsecured liability with no earning path behind it, which is exactly what an underwriting officer is paid to avoid.

Three hard conditions sit inside that regulation. The course must run at least 54 months of medical instruction. The 12-month internship must be completed in the same country where the degree was earned, not split across countries, not brought back to India. And the medical college must be on the NMC route at both the time of admission and the time of graduation.

I am deliberately not pasting a list of “approved colleges” here, because the NMC route is reviewed and republished, and anything I list today can be stale within months. The only authoritative place is nmc.org.in, and the bank will check the same source. Per the current NMC route is the phrase to keep in your head: it is not the agent’s claim, it is what the regulator shows on the day the file is underwritten.

Faz's ruleVerify the exact college on nmc.org.in on the day you sign the agent contract, and again on the day the bank requests it. The agent's word is a starting point, never proof.

I have watched families pay the agent fee, put the student on a flight, and only then learn the specific college did not satisfy the FMG rule. The damage is rarely recoverable. The five minutes it takes to verify on the regulator’s own site is the cheapest insurance in this entire process, and almost nobody spends it before the money has moved.

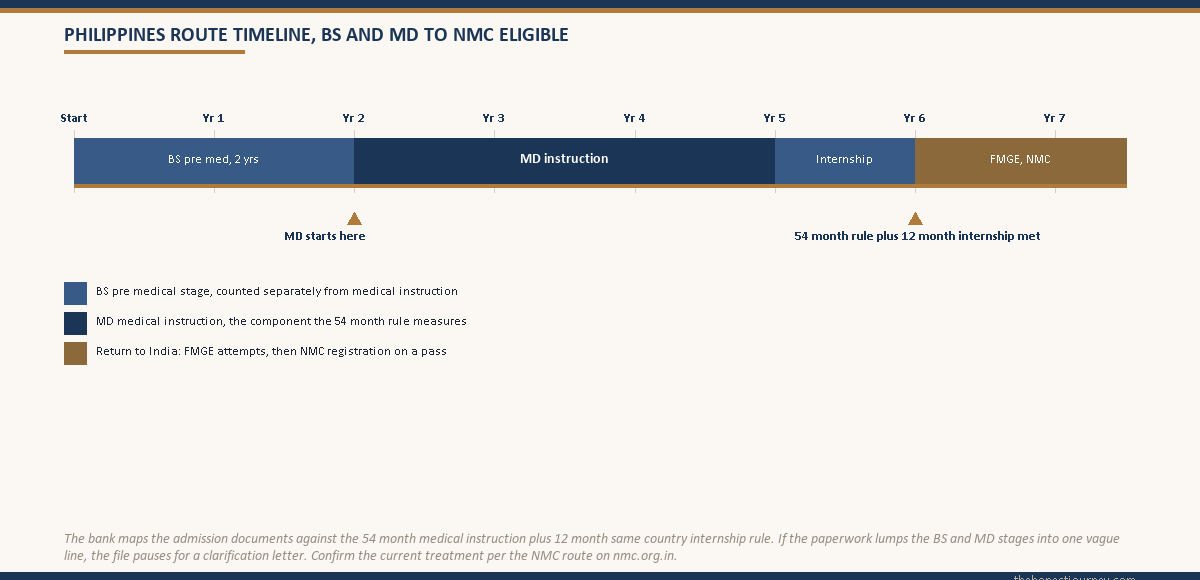

The Philippines: BS pre-med plus MD, and the duration nuance that caught older batches

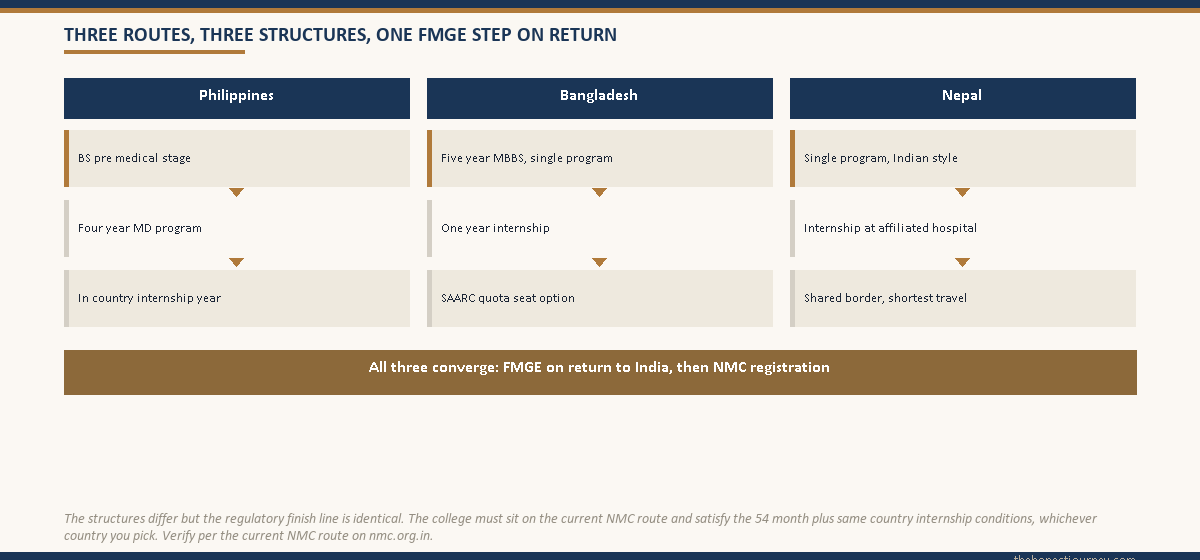

The Philippines does not run a single continuous MBBS the way India does. The structure is two stages. First a Bachelor of Science course, often BS Biology or a designated pre-medical degree, that runs roughly two years in the form Indian students usually take. Then the Doctor of Medicine, the MD, which runs four years and ends with an internship year.

This split is where older batches got hurt. When the FMG Regulations 2021 set the 54-month minimum for medical instruction, families and some colleges read it loosely, assuming the BS years counted as part of the medical duration. The cleaner reading, and the one the NMC and the banks now apply, is that the medical instruction itself plus the in-country internship must satisfy the duration and internship conditions. A student who structured the timeline carelessly, or whose college issued documents that blurred the BS and MD components, found the file questioned.

What this means in practice for the loan is that the bank wants the program structure spelled out in writing. The admission documents should show the BS pre-med stage and the MD stage clearly, with the MD duration and the 12-month internship year stated separately, so the underwriting officer can map it against the 54-month plus 12-month rule. If the paperwork lumps everything into one vague “5.5 year medical program” line, expect the file to pause for a clarification letter. Confirm the current treatment per the current NMC route on nmc.org.in rather than relying on what worked for a batch three years ago.

Bangladesh: SAARC seats, a familiar curriculum, and proximity

Bangladesh is the route a lot of families underrate. The MBBS there runs as a single five-year program plus a one-year internship, which maps neatly onto the 54-month plus 12-month rule without the staging gymnastics the Philippines requires. The curriculum is close to the Indian one, English is the medium of instruction at the colleges that take international students, and the cultural and dietary distance is small.

The piece worth understanding is the SAARC seat arrangement. A share of seats for international students in Bangladeshi medical colleges is allotted under a SAARC quota, and Indian students apply into that channel. The fee under the SAARC route can sit below the open international fee at the same college, which changes the loan math. The catch is that the SAARC allotment runs through a formal process with its own documentation, and the bank will want the admission and the fee both reflected on official college paperwork, not on an agent’s summary sheet.

The college still has to be on the NMC route. Proximity and a familiar curriculum do not exempt Bangladesh from the FMG Regulations 2021. A Bangladeshi medical college that is not on the current route produces a graduate who cannot register in India, exactly as a non-listed college anywhere else would. Verify per the current NMC route on nmc.org.in.

Faz's ruleA lower SAARC-quota fee only helps if the college is on the NMC route. Cheap and unrecognised is the most expensive outcome of all.

Families get excited about the SAARC fee being lakhs lower than the open international rate, and they let that number do the deciding. I have seen it more than once. The fee is the second question. The first question, always, is whether the college sits on the current NMC route, because a degree that cannot be registered in India is not a discount, it is a write-off with a passport stamp.

Nepal: the closest route, a similar fee, and a shared border

Nepal is the nearest foreign MBBS destination an Indian student can pick. The colleges affiliated to the established Nepali universities run a program structure close to the Indian one, with an internship year that satisfies the in-country requirement when completed at the affiliated teaching hospital. The fee at the recognised Nepali colleges often runs in a band similar to Indian private colleges at the lower end, which surprises families who assume foreign automatically means cheaper.

The advantages are practical. Travel is short and cheap, so the flight head in the cost budget is the smallest of the three countries. Language is rarely a barrier. A student can come home for an emergency in a day rather than a week. For families who are anxious about distance, Nepal removes a real source of stress.

The discipline is identical to everywhere else. The college must be on the NMC route, the program must satisfy the 54-month and same-country internship conditions, and the bank verifies status before disbursing. Nepal’s proximity makes the logistics easier, not the regulation softer. Check the specific college per the current NMC route on nmc.org.in.

The real cost, end to end, across the three countries

The figure an agent quotes is the tuition number, converted to rupees at last year’s rate, with hostel folded into a “package”. The figure the bank underwrites is everything: tuition, hostel and food, college and university charges, insurance, visa, flights, books, FMGE coaching for the return, and a buffer for currency movement.

| Cost head | Philippines (full) | Bangladesh (6 yrs) | Nepal (5.5 yrs) |

|---|---|---|---|

| Tuition total | ₹22 to 35 lakh | ₹25 to 38 lakh | ₹28 to 42 lakh |

| Hostel + food (full course) | ₹6 to 10 lakh | ₹5 to 8 lakh | ₹4 to 7 lakh |

| Visa, residence, insurance | ₹80k to 1.3 lakh | ₹50k to 90k | ₹30k to 60k |

| Flights (full course) | ₹2.5 to 4 lakh | ₹1 to 1.8 lakh | ₹50k to 1 lakh |

| Books, equipment, miscellaneous | ₹1.5 to 2.5 lakh | ₹1.5 to 2 lakh | ₹1.5 to 2 lakh |

| Total all-in | ₹33 to 45 lakh | ₹33 to 45 lakh | ₹35 to 45 lakh |

The bands are wide on purpose. The Philippines spread is driven by the BS pre-med stage, which adds tuition and living time that a single-program country does not. Bangladesh swings on whether the seat is under the SAARC quota or the open international fee. Nepal’s tuition can run higher than people expect because the recognised colleges price close to Indian private rates, but its travel head is the lowest of the three because of the shared border.

The band matters for the loan because PSU banks size the sanction off your declared total cost, not a country average. Under-declare and run short in year three, and a top-up is not guaranteed. Over-declare and the unused sanction is harmless, since interest accrues only on the disbursed amount, but the co-applicant has been assessed for a larger commitment than the course needed.

Which Indian banks fund this route, and on what terms

The same three PSU lenders that handle CIS MBBS handle this route: State Bank of India under Global Ed-Vantage, Bank of Baroda under its studies-abroad education loan, and Canara Bank under its overseas product. Union Bank and PNB also fund these countries with smaller portfolios and more cautious underwriting.

SBI Global Ed-Vantage sanctions up to ₹1.5 crore for overseas study, far above what any of these MBBS programs will need. For a ₹35 to 45 lakh MBBS loan, SBI typically asks for tangible collateral on the amount above ₹7.5 lakh: immovable property, a fixed deposit, or an LIC policy at surrender value. The interest rate sits around the 1-year MCLR plus a spread, with concessions for female students and for collateral above the loan value.

Bank of Baroda’s studies-abroad product carries a similar ceiling and collateral threshold. The difference tends to show at disbursement. The SWIFT corridor to Nepal and Bangladesh is well-worn for Indian banks, so first tranches there often clear faster than to the Philippines, where the college account may be newer on the bank’s books.

Canara Bank is structurally similar and historically a touch more conservative, more likely to ask for a written confirmation from the college that the program duration matches the FMG Regulations 2021, especially for the Philippines structure.

NBFCs (Avanse, Auxilo, Credila, InCred) fund this route unsecured up to around ₹50 lakh in many cases, which is where families without collateral end up. The rate runs 2 to 4 percentage points above PSU banks, and the NBFC is not bound by the IBA Model Education Loan Scheme, so borrower protections are weaker. The trade is faster sanction and lighter paperwork. For families with no property to pledge, it is sometimes the only route. For families who can pledge, the PSU bank is almost always cheaper across the loan life. The full unsecured picture sits in my education loan for abroad studies without collateral post, and the overall ceilings are covered in the maximum education loan amount post.

What the bank actually checks before sanctioning

The standard education loan file applies: co-applicant income, KYC, admission letter, cost breakdown. This route adds three checks families should be ready for.

First, the bank verifies the college’s NMC route status as of the sanction date, by matching the college name exactly against the current list on nmc.org.in. If the agent has used a slightly different spelling of a Philippine or Bangladeshi college than the regulator shows, the file pauses for a clarification letter.

Second, the bank confirms the program duration on the admission documents satisfies the 54-month rule. For the Philippines this is the sharpest check, because the BS-plus-MD split has to be laid out clearly so the medical instruction and the internship year are each visible. For Bangladesh and Nepal the single-program structure usually maps cleanly, but the bank still wants the internship year stated.

Third, the bank checks the fee on the admission letter against the college’s published international or SAARC fee. Agents sometimes inflate the figure to bury their commission inside the loan. The safer path is to ask for a separate, transparent fee receipt rather than a bundled tuition line.

Beyond these three, the bank weighs the co-applicant’s repayment capacity over the full moratorium plus a 10 to 15 year repayment window. A weak co-applicant profile is the single biggest reason these loans are rejected at underwriting; the destination only matters once the income side clears. The full list sits in my education loan rejection reasons post.

The FMGE reality, said honestly

The Foreign Medical Graduate Examination, conducted by the National Board of Examinations in Medical Sciences, is the screening test every foreign medical graduate must clear to register and practise in India. The pass rate has historically sat below 25 percent, with some sittings closer to 15 percent.

That number gets used to scare families off foreign MBBS entirely, and it gets used by agents who say the rate is improving. Both can be true. The pass rate has been climbing since 2022, as more graduates take dedicated coaching on return and as the FMG Regulations 2021 raised the floor on what a foreign curriculum must cover. But improving is not the same as high. A realistic planning assumption for a graduate of any of these three countries is that the first attempt may not clear, that the second or third attempt is more likely with focused preparation, and that the loan moratorium accommodates roughly 6 to 12 months of grace before EMI begins.

In cash terms, the EMI start date can land in a window where the graduate is still preparing for FMGE attempts or doing the post-FMGE internship the NMC requires before final registration. The co-applicant carries the EMI through that window. If the co-applicant cannot, the loan goes into stress, and stress on a ₹35 to 45 lakh balance is not a small thing to climb out of.

This is not a reason to write off the route. It is a reason to size the loan against the realistic timeline, graduate clears FMGE on the second or third attempt with the family carrying EMI for 18 to 24 months post-moratorium, rather than the marketing timeline where everything clears on the first try.

The honest closing take

The Philippines, Bangladesh and Nepal are legitimate routes into medicine for Indian students who cannot get a domestic government seat and cannot afford a domestic private one. The loan side is workable. The path that goes wrong is the one where the family treats the agent’s brochure as gospel, skips the NMC check, takes the cheapest NBFC without comparing PSU options, and assumes the FMGE clears on the first attempt.

The path that goes right verifies the college per the current NMC route on nmc.org.in before signing the agent, takes the loan from the PSU bank with the lowest rate, which almost always means pledging collateral, sizes the loan to the full cost band with a currency buffer, and plans the post-graduation cashflow assuming a 12 to 18 month gap between graduation and the first paycheck. For the Philippines specifically, it also means getting the BS-plus-MD structure documented cleanly so the duration rule is never in question.

This is not a route that rewards optimism. It rewards documentation. The families who navigate it cleanly treat every promise as something to verify on a government website, and keep the bank, the agent and the family on the same page in writing. The interest-rate side of any of these loans should also be read against the RBI framework that governs education lending.

FAQ

Is MBBS in the Philippines NMC approved?

Specific Philippine medical colleges sit on the current NMC route and others do not, and the route is reviewed and republished by the National Medical Commission. The only authoritative source is nmc.org.in, which the bank checks before sanctioning. The Philippines also carries a structural nuance: the BS pre-medical stage and the four-year MD must be documented so the medical instruction satisfies the 54-month rule. Treat any agent claim of approval as a starting point to verify per the current NMC route, on the day of admission and again when the loan is requested.

Which Indian banks fund MBBS in the Philippines?

The three PSU banks that handle the bulk of this route are State Bank of India under Global Ed-Vantage, Bank of Baroda under its studies-abroad education loan, and Canara Bank under its overseas product. Union Bank and PNB also fund these countries with more conservative underwriting. NBFCs such as Avanse, Auxilo, Credila and InCred fund unsecured cases up to around ₹50 lakh, at rates 2 to 4 percentage points higher than PSU banks. The PSU route is cheaper across the loan life if collateral can be pledged.

How much is MBBS in Bangladesh in total cost?

The all-in cost for the full degree, a five-year MBBS plus a one-year in-country internship, lands roughly between ₹33 lakh and ₹45 lakh. This includes tuition, hostel and food, college and university charges, insurance, visa, flights, books, and a buffer for currency movement. A SAARC-quota seat can lower the tuition head materially below the open international fee at the same college, which changes the loan math. The agent’s quoted package usually covers tuition and hostel only and misses the recurring costs the bank’s underwriting includes.

Is Nepal MBBS valid in India?

A Nepali MBBS is valid for Indian practice when the specific college sits on the current NMC route and the program satisfies the FMG Regulations 2021, meaning at least 54 months of medical instruction plus a 12-month internship completed at the affiliated teaching hospital in Nepal. The graduate must then clear the FMGE to register with the NMC. Proximity and a shared border do not exempt Nepal from the regulation. Verify the exact college per the current NMC route on nmc.org.in, since the bank checks the same source before disbursing.

What is the FMGE pass rate for Philippines graduates?

The Foreign Medical Graduate Examination has historically had a pass rate below 25 percent across all foreign destinations, with some sittings closer to 15 percent, and the Philippines is not separately exempt from that pattern. The rate has been climbing since 2022 as graduates take dedicated coaching and as the FMG Regulations 2021 raised the minimum curriculum standard. A realistic planning assumption is that the first attempt may not clear and that the second or third is more likely with focused preparation. The loan moratorium typically accommodates this window before EMI begins.

Can I get an unsecured loan for MBBS in Nepal?

Yes, NBFCs such as Avanse, Auxilo, Credila and InCred fund unsecured education loans for MBBS in Nepal, typically up to around ₹50 lakh, depending on the co-applicant’s profile and the college’s standing on the NMC route. PSU banks generally ask for tangible collateral above ₹7.5 lakh, which covers most Nepal MBBS cases. The trade-off is rate: NBFC rates run 2 to 4 percentage points higher than PSU rates, and NBFCs are not bound by the IBA Model Education Loan Scheme, so borrower protections are weaker.

Why does the internship have to be in the same country as the degree?

The NMC FMG Regulations 2021 require the foreign medical graduate to complete a 12-month internship in the same country where the degree was obtained. The aim is curriculum integrity, ensuring clinical training matches the standards of the institution that taught the academic component rather than being completed in a different jurisdiction with different protocols. An internship split between countries, or done back in India after the degree, does not satisfy the regulation, and the graduate will not be eligible to sit the FMGE. This applies equally to the Philippines, Bangladesh and Nepal.

What is the difference between the Philippines and Bangladesh MBBS structure?

The Philippines runs a two-stage path, a BS pre-medical degree followed by a four-year MD that ends with an internship year, so the documentation must clearly separate the BS and MD components for the duration rule. Bangladesh runs a single five-year MBBS plus a one-year internship that maps cleanly onto the 54-month plus 12-month rule, often with a lower SAARC-quota fee. Both require the college to be on the current NMC route and both require the FMGE on return. Verify either per the current NMC route on nmc.org.in.

Faz · The Honest Journey · 2026