An education loan for MBBS abroad is available from most Indian banks and NBFCs, typically requiring collateral for any amount above ₹7.5 lakh and an NMC listed university. The realistic loan size is ₹25 lakh to ₹40 lakh once you include hostel, food, and FMGE coaching, not the ₹15 lakh tuition figure on the brochure. The honest catch: the FMGE pass rate sits at roughly 20 to 25 percent.

The seminar slide said it cleanly. Become a doctor for ₹25 lakh, fully loan-funded, no NEET cutoff stress, MBBS from a government university in Russia or Georgia. The consultant who ran it was warm, organised, and genuinely helpful with the paperwork. He showed me a financing chart, a hostel photo, a list of Indian students already there. The one number he never put on a slide was the FMGE pass rate, and that single number is the difference between a doctor and a defaulter.

This post is about the education loan for MBBS abroad as a financial decision, not a dream. If you are weighing a ₹15 lakh to ₹40 lakh loan against a foreign medical seat, read this before you sign anything.

An education loan for MBBS abroad is available from most Indian banks and NBFCs, usually requiring collateral above ₹7.5 lakh and an NMC-listed university. The honest catch: the FMGE licensing exam that lets you practise in India has a pass rate of roughly 20 to 25 percent, so a large loan plus a failed exam is a genuine default trap.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on funding an MBBS abroad: the education loan MBBS philippines bangladesh nepal post.

What the MBBS abroad actually costs

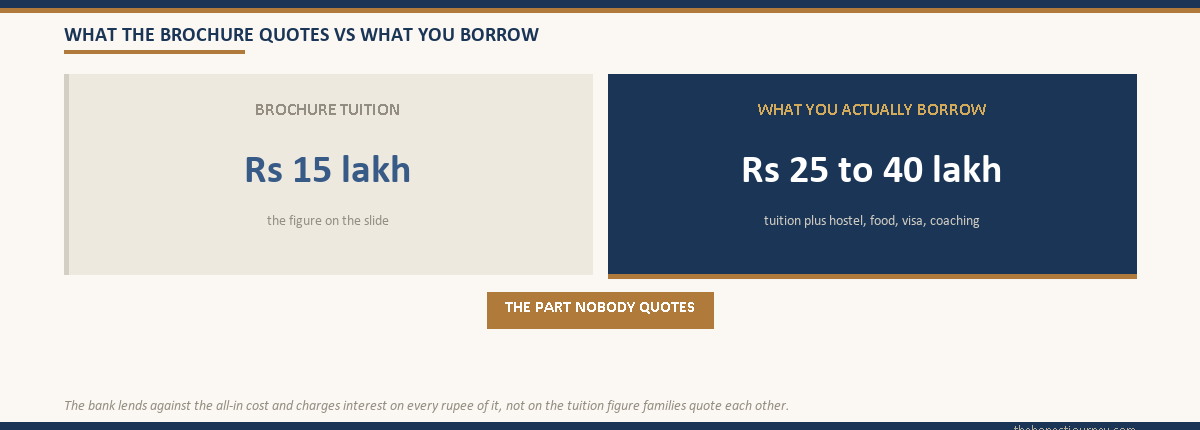

The headline appeal is real. A full MBBS in Russia, Georgia, or Kazakhstan costs a fraction of an Indian private medical seat, where total fees routinely cross ₹60 lakh to over ₹1 crore. But the foreign number families quote each other is almost always the tuition only, and tuition is roughly two-thirds of what you will actually borrow.

Here is the realistic all-in range for the popular destinations, covering tuition, hostel, food, visa, insurance, and the coaching most students end up buying later.

| Country | Course length | Tuition (total) | All-in cost (total) |

|---|---|---|---|

| Russia | 6 years | ₹15 lakh to ₹22 lakh | ₹25 lakh to ₹35 lakh |

| Georgia | 6 years | ₹20 lakh to ₹30 lakh | ₹30 lakh to ₹40 lakh |

| Kazakhstan | 5 to 6 years | ₹14 lakh to ₹20 lakh | ₹22 lakh to ₹30 lakh |

So the loan you are realistically looking at is ₹25 lakh to ₹40 lakh, not the ₹15 lakh tuition figure on the brochure. If you have already narrowed your choice to one of these three destinations, the country-by-country funding detail is in the education loan for MBBS in Russia, Georgia and Kazakhstan post. That gap matters enormously when you run the repayment math later, because the bank lends against the all-in cost and charges interest on every rupee of it.

One more cost most families forget: living expenses are remitted in foreign currency, so the rupee cost drifts upward across six years as the exchange rate moves. A six-year program is six years of currency risk on top of the loan interest.

How the loan is structured

An education loan for MBBS abroad follows the standard abroad-study loan template, with two thresholds that decide your entire experience.

Below ₹7.5 lakh, public sector banks can lend without collateral against a co-applicant. But almost no genuine MBBS abroad fits under ₹7.5 lakh, so this band is mostly theoretical for medical students. Above ₹7.5 lakh, which is essentially every real case, you will need collateral: typically immovable property worth at least the loan amount, or in some cases a high-value fixed deposit or LIC policy. The co-applicant, usually a parent, must also clear the bank’s income and FOIR checks.

The interest rate depends heavily on who lends. A collateral-secured loan from a public sector bank such as SBI under its education loan schemes, governed by the IBA model framework, typically runs 8.5 to 10.5 percent. An NBFC or private lender willing to move faster runs 11.5 to 14 percent. On a ₹30 lakh loan over a six-year course plus moratorium, that rate gap is not a footnote. It is several lakh rupees.

| Lender type | Typical rate | Collateral above ₹7.5L | Speed |

|---|---|---|---|

| Public sector bank (IBA scheme) | 8.5% to 10.5% | Required | Slower, more documentation |

| Private bank | 10.5% to 12.5% | Usually required | Moderate |

| NBFC | 11.5% to 14% | Sometimes flexible | Fast |

The single most important eligibility rule is the university. Indian banks will only fund an MBBS abroad if the university is recognised by the relevant authorities and the degree is acceptable for the Indian licensing route. The National Medical Commission sets the framework that decides whether your foreign degree can ever convert into an Indian practice licence. If the university is not on the right list, the bank may decline, or worse, you fund the whole thing and find the degree leads nowhere in India. Confirm this in writing before the first disbursement. The wider rule on which institutions qualify for funding is covered in the approved foreign universities for education loan post.

Faz's ruleThe university must clear both the bank and the NMC. One without the other is a trap.

A bank loan and an NMC-recognised pathway are two separate approvals. Get both confirmed in writing before you remit a single rupee of tuition. A funded degree that cannot lead to an Indian licence is the most expensive mistake in this entire decision.

The number every consultancy leaves off the slide: FMGE

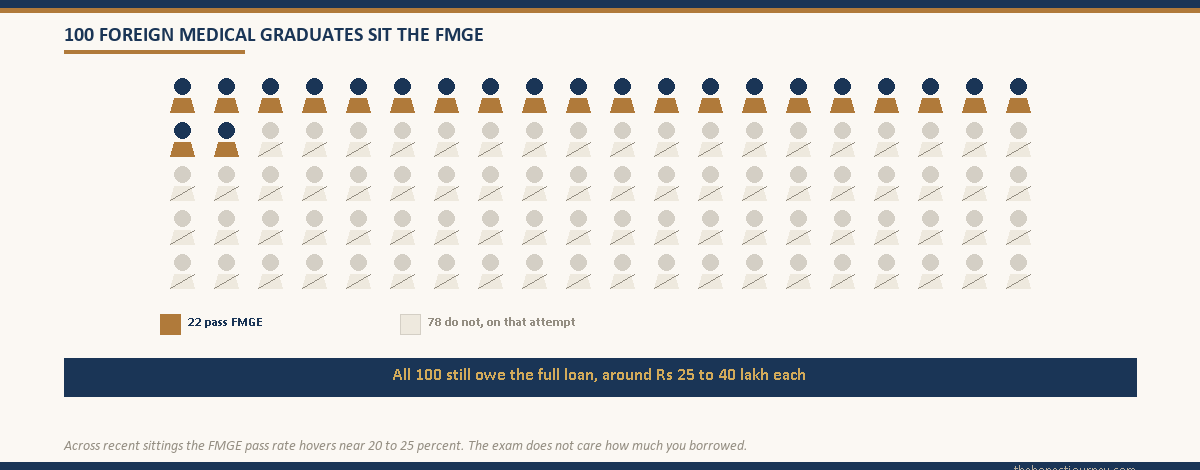

Here is the part that decides whether this loan is an investment or a trap. To practise medicine in India with a foreign MBBS, you must clear the Foreign Medical Graduate Examination, the FMGE, conducted by the National Board of Examinations. There is no shortcut around it. No matter how good your foreign degree looks, you cannot legally treat a patient in India until you pass the FMGE and complete registration with the NMC.

The pass rate is the number the brochures never show. Across recent sittings, the FMGE pass rate has hovered around 20 to 25 percent. Read that again. Roughly three out of four foreign medical graduates who sit the exam do not clear it on a given attempt. The official scope and structure of the exam is published by the NBEMS FMGE information desk, and the qualifying bar is a flat 50 percent, with no relative grading to soften it.

You can re-attempt the FMGE, and many students eventually clear it on a second or third try, often after a year of dedicated coaching back in India. But every re-attempt is another year of not earning, while the loan moratorium has ended and EMIs have started. The exam does not care how much you borrowed.

The default trap, in hard numbers

Let me run the scenario the seminar never runs. You borrow ₹30 lakh at 11.5 percent from an NBFC for a six-year MBBS in Georgia. The moratorium covers the six-year course plus a 12-month grace period, so 84 months. Interest accrues the entire time and capitalizes at the end.

Monthly interest on ₹30 lakh at 11.5 percent is about ₹28,750. Over 84 months of moratorium, that is roughly ₹24 lakh of accrued interest added to your principal. Your balance when EMIs begin is not ₹30 lakh. It is closer to ₹54 lakh. The mechanics of why this happens are explained fully in the moratorium period interest post.

| Outcome | Balance at EMI start | Approx EMI (10 yr) | Reality |

|---|---|---|---|

| Pass FMGE, practise in India | ₹54 lakh | ₹76,000 | Hard but survivable as a doctor |

| Fail FMGE, no Indian licence | ₹54 lakh | ₹76,000 | EMI with non-doctor income, default risk |

That second row is the trap in one line. A ₹76,000 monthly EMI is heavy even on a doctor’s income. On the income of someone who finished an MBBS but cannot legally practise it in India, it is a default waiting to happen. And because the loan was secured against your family’s property, a default does not just hurt your credit. It can put the home that was pledged as collateral at risk. This is the conversation that should happen at the kitchen table before the seminar, not after the third failed attempt.

Faz's ruleA ₹30 lakh loan with a failed FMGE is not a setback. It is a default trap that can reach the collateral.

The exam is the gate, not the degree. Plan the loan around a realistic probability of clearing FMGE, not the brochure’s promise. If the family cannot service the EMI on a non-doctor income for a year or two while you re-attempt, the loan is too large for the risk.

Who this genuinely suits, and who should not

I am not against MBBS abroad. For the right person it is a legitimate, life-changing path. The problem is that consultancies sell it to everyone, and it only works for some.

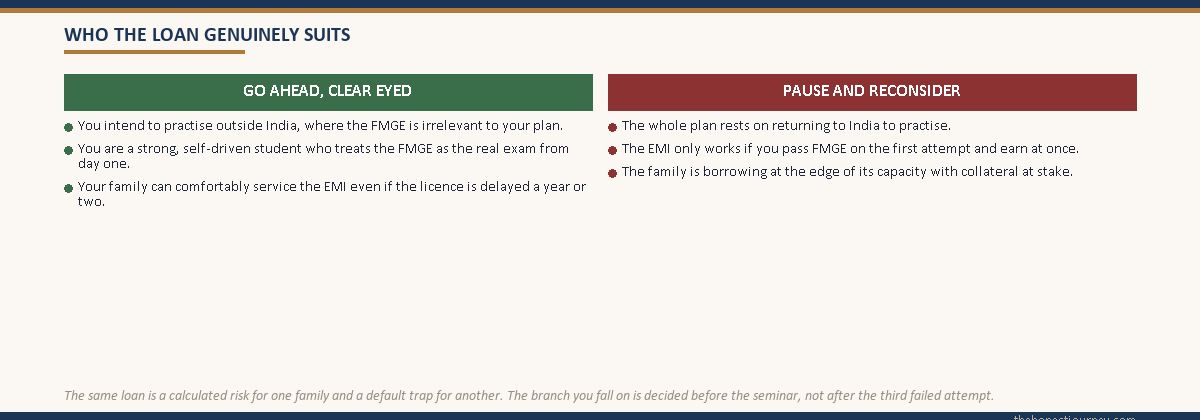

It genuinely suits you if you intend to practise medicine outside India, in a country whose own licensing route you have researched, where the FMGE is irrelevant to your plan. It also suits you if you are an exceptionally strong, self-driven student who will treat the foreign MBBS as the easy part and the FMGE as the real exam from day one, building it into a six-year study plan rather than a panic in the final year. And it suits families who can comfortably service the EMI even in the worst case, where the licence is delayed by a year or two of re-attempts.

It does not suit you if the entire plan rests on returning to India to practise and the family is borrowing at the edge of its capacity. If the EMI only works on the assumption that you pass FMGE on the first attempt and start earning immediately as a doctor, you are betting a ₹30 lakh loan on a 20 to 25 percent first-attempt event. That is not a plan. That is a wager with your family’s collateral as the stake.

This is also where the alternatives deserve an honest look. An Indian private MBBS is far more expensive but keeps you inside the Indian licensing system from day one, with no FMGE gate. The trade-offs there are covered in the education loan for MBBS in a private college post and, for the lower-cost route, the government college MBBS loan post. If a NEET-eligible government seat is realistically within reach, it is almost always the better financial bet than a foreign MBBS plus an FMGE lottery.

If collateral is the obstacle and you are exploring unsecured routes to fund a smaller foreign program, understand those limits clearly first in the education loan without collateral post, because unsecured lending at ₹30 lakh for an FMGE-gated degree is the riskiest combination of all.

The honest closing take

The MBBS abroad loan is one of the few study-abroad decisions where the financing is the easy part and the outcome is the hard part. Banks will lend you the money. Consultancies will arrange the seat. Neither of them sits the FMGE for you, and neither of them pays the EMI if you do not clear it.

So the number to fix on is not the tuition, and it is not even the interest rate. It is this: can your family service the full EMI on the worst-case timeline, where you graduate, fail the FMGE once or twice, spend a year coaching, and only then start earning as a doctor? If the answer is yes, the loan is a calculated risk and you should go in clear-eyed and study like the FMGE is the only exam that matters. If the answer is no, the loan is too big for the bet, and a cheaper or domestic path will serve you far better than a foreign degree you cannot license.

Borrow against a realistic probability, not a brochure. That is the whole post.

Faz's ruleSize the loan to the worst case, not the brochure case.

The honest test is simple. Can the family pay the EMI for two years on a non-doctor income while you re-attempt FMGE? If yes, proceed carefully. If no, the loan is the wrong size for the risk, and no seminar slide changes that math.

FAQ

Can I get an education loan for MBBS abroad?

Yes. Most Indian public sector banks, private banks, and NBFCs offer education loans for MBBS abroad. The standard requirement is collateral for any loan above ₹7.5 lakh, which covers almost every real MBBS case, plus a co-applicant who clears the bank’s income checks. The critical condition is that the university must be recognised under the framework set by the National Medical Commission so the degree can lead to an Indian practice licence. Confirm both the bank’s approval and the NMC pathway in writing before the first disbursement.

How much does MBBS in Russia cost?

Tuition for a six-year MBBS in Russia typically runs ₹15 lakh to ₹22 lakh in total. But the all-in cost, including hostel, food, visa, insurance, travel, and the FMGE coaching most students eventually buy, lands closer to ₹25 lakh to ₹35 lakh. Families often quote only the tuition figure, which understates the real loan by roughly a third. Living costs are remitted in foreign currency across six years, so currency movement adds further variability to the rupee total.

Is collateral needed for an MBBS abroad education loan?

For practical purposes, yes. Banks can lend up to ₹7.5 lakh without collateral against a co-applicant, but a genuine MBBS abroad almost always costs far more than that, so collateral is required in nearly every case. This usually means immovable property worth at least the loan amount, or sometimes a high-value fixed deposit or LIC policy. Collateral-secured loans also carry lower interest rates, typically 8.5 to 10.5 percent at public sector banks versus 11.5 to 14 percent at NBFCs.

What is the FMGE pass rate?

The Foreign Medical Graduate Examination pass rate has hovered around 20 to 25 percent across recent sittings, conducted by the National Board of Examinations. Roughly three out of four candidates do not clear it on a given attempt. The qualifying bar is a flat 50 percent with no relative grading. You can re-attempt the exam, and many graduates eventually pass on a second or third try, but each re-attempt is another year without doctor-level income while loan EMIs may already have started.

What happens to my loan if I fail FMGE?

The loan does not pause or shrink because you failed the licensing exam. Once your moratorium ends, EMIs begin regardless of whether you can practise. If you graduated but cannot clear the FMGE, you face a large EMI on a non-doctor income, which is the core default risk in this decision. Because most MBBS abroad loans are secured against family property, a sustained default can put that collateral at risk, which is why the loan should be sized for the worst-case timeline.

Which countries are NMC-approved for MBBS abroad?

The National Medical Commission sets the recognition framework that decides whether a foreign medical degree is acceptable for Indian licensing, including criteria on course duration, medium of instruction, and the university’s standing. Russia, Georgia, and Kazakhstan host many universities that fit the framework, but recognition is university-specific, not country-wide. Always verify the exact institution against current NMC guidance before enrolling or borrowing, because a degree from a non-qualifying university cannot convert into an Indian practice licence no matter how much you spend.

Is MBBS abroad cheaper than an Indian private college?

On tuition alone, yes, often dramatically. An Indian private medical seat can cost ₹60 lakh to over ₹1 crore, while a foreign MBBS all-in runs ₹22 lakh to ₹40 lakh. But the comparison is not just about cost. An Indian degree keeps you inside the domestic licensing system with no FMGE gate, while the foreign route adds the FMGE hurdle with its low pass rate. The cheaper sticker price is only a real saving if you clear FMGE and can practise in India.

Should I take an MBBS abroad loan if I plan to practise in India?

Only if your family can comfortably service the EMI even in the worst case, where you graduate, fail the FMGE once or twice, spend a year on coaching, and start earning as a doctor only after that. If the plan depends on passing FMGE on the first attempt to make the EMI affordable, you are betting a large loan on a 20 to 25 percent first-attempt event. If a NEET-eligible Indian government seat is realistically within reach, it is almost always the safer financial choice.

Faz · The Honest Journey · 2026