An education loan for MBBS in a government college rarely needs collateral, because total tuition for the full 5.5 year course (internship included) sits between ₹6 lakh and ₹10 lakh. SBI Scholar and Bank of Baroda Vidya cover the full amount at 8.05 to 9.15 percent with zero margin money. Skip the private bank pitch.

The first thing to know about an education loan for MBBS in government college is that most families end up borrowing far less than they expect. The full five and a half year course, internship included, costs roughly ₹6 lakh to 10 lakh in total tuition. Bankers and well meaning relatives often quote loan amounts that would suit a private medical seat, and a family walks into the branch ready to mortgage property when the actual need is a small, collateral free loan that two public sector banks will sanction in a fortnight.

I have spent the last two years sitting with parents of NEET qualifiers, looking at fee structures, and running the math on what they actually need to borrow. This post is the honest version of that conversation.

Answer capsule: An education loan for MBBS in a government college in India typically falls between ₹4 lakh and ₹10 lakh because total tuition for the five and a half year course is only ₹6 lakh to 10 lakh. Loans under ₹7.5 lakh are collateral free at most public sector banks. Families earning under ₹4.5 lakh annually qualify for full moratorium interest subsidy under CSIS.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on funding an MBBS abroad: the education loan for MBBS abroad post.

What a government MBBS seat actually costs

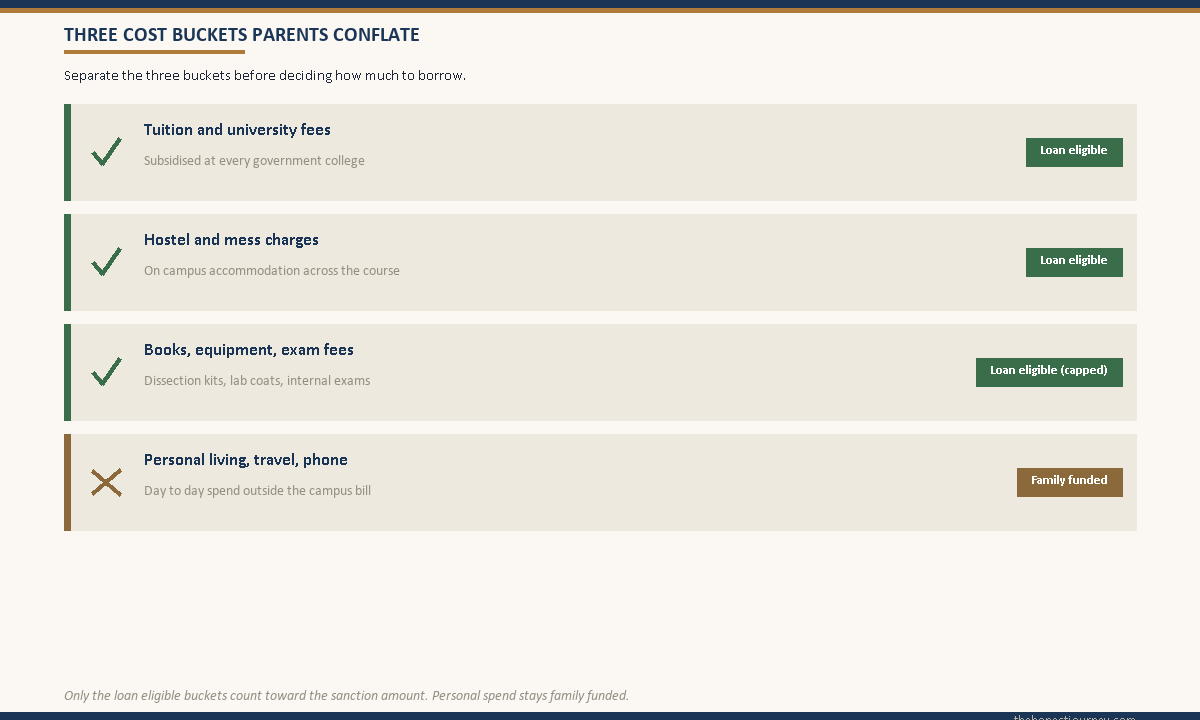

Before deciding how much to borrow, separate the three numbers families routinely lump into one. Tuition fees, hostel and mess charges, and personal living costs are very different buckets, and only the first two are loan eligible at most banks. The third is family funded.

Tuition at a government medical college runs from a token ₹1,000 to 1,500 per year at AIIMS Delhi to roughly ₹25,000 to 1.5 lakh per year at larger state government colleges. The four and a half pre internship years of academic fees and exam costs together rarely cross ₹8 lakh even at the higher rates.

Hostel and mess is where the number doubles. A government college hostel costs roughly ₹30,000 to 60,000 per year all in. Five and a half years of hostel and mess is ₹1.65 lakh to 3.3 lakh. Books, dissection kits, lab coats, and exam fees add another ₹1 lakh to 1.5 lakh.

| Cost bucket | 5.5 year total (state govt college) | 5.5 year total (central govt / AIIMS) | Loan eligible |

|---|---|---|---|

| Tuition and university fees | ₹1.5 lakh to 8 lakh | ₹10,000 to 50,000 | Yes (100 percent) |

| Hostel and mess | ₹1.65 lakh to 3.3 lakh | ₹1.5 lakh to 2.5 lakh | Yes (most banks) |

| Books, equipment, exam fees | ₹1 lakh to 1.5 lakh | ₹1 lakh to 1.5 lakh | Yes (capped) |

| Personal living, travel, phone | ₹1.5 lakh to 3 lakh | ₹1.5 lakh to 3 lakh | No (family funded) |

| Total loan eligible | ₹4.15 lakh to 12.8 lakh | ₹2.6 lakh to 4.5 lakh |

This is why I push back when a family arrives convinced they need to borrow ₹25 lakh. In nine cases out of ten, the honest number sits between ₹4 lakh and 10 lakh, and the loan structure that fits is very different from what a private MBBS seat needs.

Faz's ruleA government MBBS seat is one of the cheapest professional degrees in India. Borrow only what you actually need.

I have seen families take a loan against property for a seat where the total tuition was ₹4 lakh. The seat is so heavily subsidised that the right loan amount is often a fraction of what the bank will gladly sanction. Cap it at what the fee receipts justify.

Why most government MBBS loans are collateral free

Under the Indian Banks’ Association model education loan scheme that public sector banks follow, loans up to ₹7.5 lakh for studies within India do not require any collateral. The co-applicant (a parent or guardian) signs with you, and that is the only security the bank takes. No property mortgage, no fixed deposit lien, no third party guarantor.

Because the total funding need for a government MBBS seat usually sits below this threshold, the typical sanction is a small, unsecured loan with a moratorium that runs through your course duration plus one year. SBI’s Student Loan Scheme, Bank of Baroda’s Vidya, Canara Bank’s Vidya Sagar, and PNB Saraswati all follow this pattern. Rates for these in-India unsecured loans currently sit between 8.5 percent and 10.5 percent, materially lower than the 11 to 14 percent that NBFCs charge for abroad MBBS loans in destinations like the Philippines, Bangladesh, and Nepal, or for the higher-ticket MBBS loans in Russia, Georgia, and Kazakhstan where the all-in cost runs far above a government seat.

Between ₹7.5 lakh and ₹10 lakh, most banks will still sanction without collateral if the co-applicant’s income and credit profile are strong. Above ₹10 lakh, collateral enters the conversation, though for a government MBBS seat you should rarely need to cross that line. The official IBA model loan scheme on the Indian Banks’ Association site spells out these thresholds clearly.

| Loan amount | Collateral needed | Typical interest band | Margin (own contribution) |

|---|---|---|---|

| Up to ₹4 lakh | None | 8.5 to 10 percent | Zero |

| ₹4 lakh to 7.5 lakh | None (co-applicant signs) | 8.5 to 10 percent | 5 percent |

| ₹7.5 lakh to 10 lakh | None at most PSBs (strong co-app) | 9 to 10.5 percent | 5 percent |

| Above ₹10 lakh (rare for govt MBBS) | Property or FD usually required | 9 to 11 percent | 5 to 15 percent |

The rate band on SBI’s in-country Student Loan, on the SBI education loans page, applies a small concession for female students and another for premier institutes. Both apply to most government medical colleges, so the effective rate after concessions can be closer to 8.5 percent than 10.5 percent in practice.

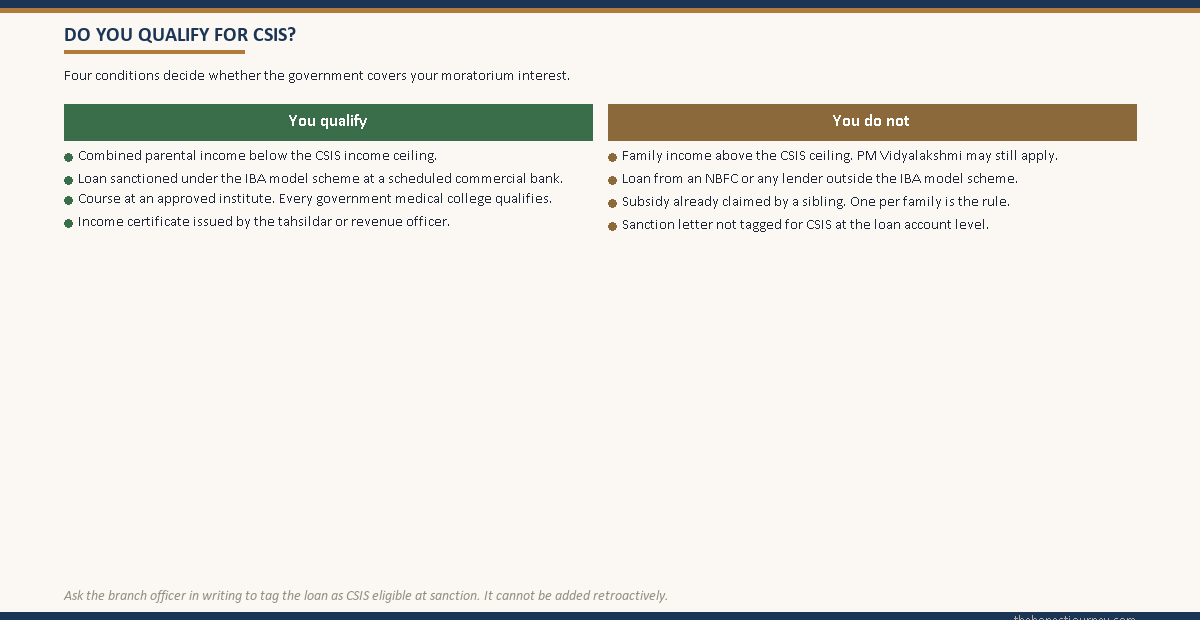

CSIS, the interest subsidy most families ignore

The Central Sector Interest Subsidy scheme is the single most useful feature of the in-India education loan system, and most families who qualify never claim it because nobody at the bank tells them about it clearly. Here is the honest version.

If your parents’ combined gross annual income is under ₹4.5 lakh, you qualify. The government pays the full interest that accrues on your loan during the moratorium period (course duration plus one year). You start repayment on the original sanctioned amount only, with zero interest capitalised onto your principal. On a ₹8 lakh loan over a six and a half year moratorium at 9.5 percent, that is roughly ₹4.5 lakh to 5 lakh that the government picks up instead of you.

The eligibility checklist is short. The course must be at an approved institute (every government medical college qualifies). The loan must be sanctioned under the IBA model scheme at a scheduled commercial bank. The income certificate must come from a competent authority (a tahsildar or revenue officer). The subsidy is claimed once per family, so if a sibling has already used it, you cannot claim it again.

For families just above the ₹4.5 lakh threshold, the newer PM Vidyalakshmi scheme extends subsidy benefits to families with income up to ₹8 lakh at lower subsidy percentages. The full mechanics, including how to apply via the central portal, are in the PM Vidyalakshmi portal post.

Faz's ruleIf your family income is under ₹4.5 lakh, CSIS makes a government MBBS effectively interest free for the study years.

This is the closest thing to free higher education that exists in the Indian banking system. The income certificate from the tahsildar plus the loan sanction letter is all you need. Most branch officers will not volunteer this. Ask for it by name.

The rare cases where a larger loan does make sense

Everything above assumes the modal government MBBS student: a state quota seat in the home state, hostel on campus, family covering personal expenses. There are three honest exceptions where a larger loan, sometimes up to ₹15 lakh to 20 lakh, becomes a reasonable conversation.

Out of state student under the all India quota. If you matched outside your home state through the Medical Counselling Committee’s 15 percent all India quota, your living costs change. You may need a private PG in your first year if the campus hostel is full. Travel home and the higher cost of an unfamiliar city add up. A loan in the ₹10 lakh to 15 lakh range can be appropriate, and banks will sanction it under the IBA model scheme. MCC rules are on the Medical Counselling Committee site.

Tier 1 city government college with high incidentals. A government seat in Mumbai or Delhi has a tuition comparable to a smaller state college, but rent (if hostel space is short), transport, and basic living costs run higher. Families who cannot fund ₹3 lakh to 4 lakh in incidentals comfortably do borrow that bit extra.

NEET coaching or prep year costs. Some families borrowed informally for a year of NEET coaching at ₹1.5 lakh to 3 lakh. A few banks allow that prior preparation cost to be folded into the education loan once admission is confirmed, at branch manager discretion. Worth asking at the home branch.

Outside these three, the answer to “should I borrow more” is almost always no. The loan is sized to the fee receipts, and inflating it because the bank is willing only inflates the EMI later.

How to actually apply, step by step

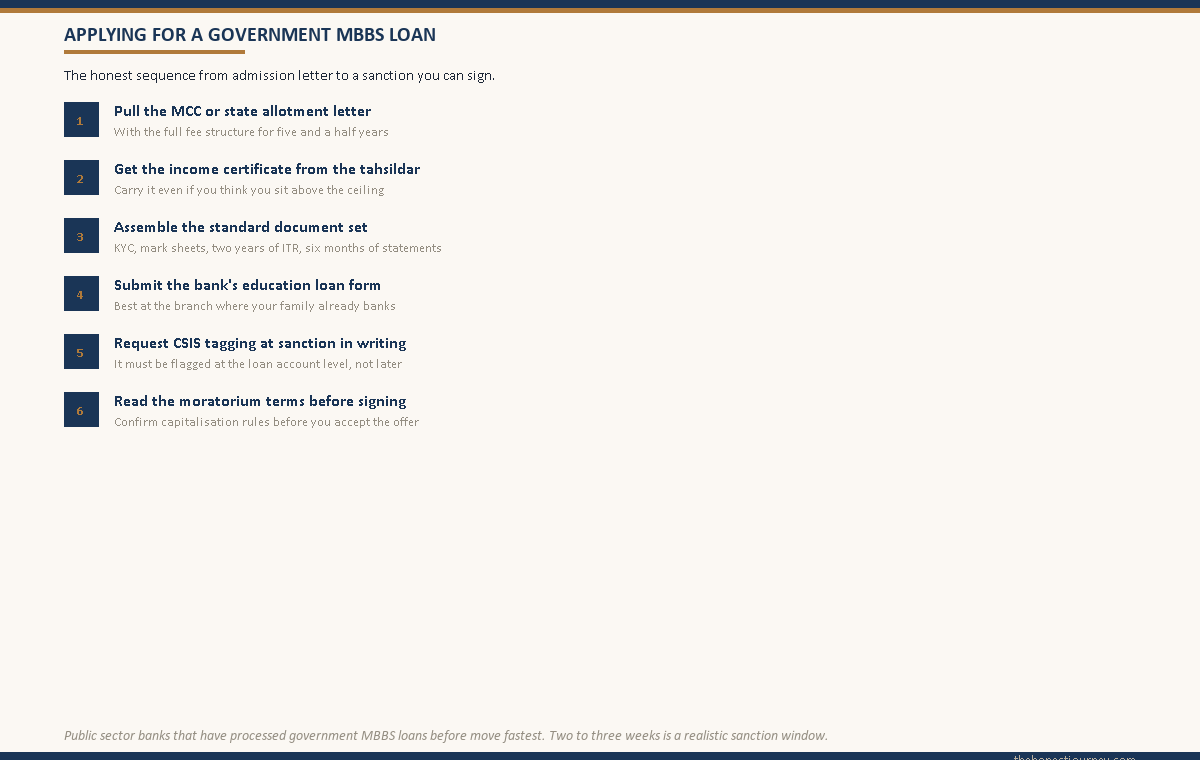

Start at the bank where your family has the longest standing relationship. A salary account or long running savings account with the branch manager who knows your parents will move faster than a fresh application at a new bank, even if the rate is identical.

One, get the admission allotment letter from MCC or your state counselling authority, with the full fee structure for all five and a half years. Two, get the income certificate for the co-applicant from the tahsildar, even if you think you may be above the CSIS threshold. Bank officers may ask anyway. Three, collect the standard document set: KYC of student and co-applicant, mark sheets, ID and address proof, two years of ITR or income proof, six months of bank statements.

Four, submit the bank’s education loan form with all attachments. For government MBBS the sanction is usually two to three weeks at a PSB branch that has done these before. Five, ask the branch officer in writing to flag the loan as eligible for CSIS at sanction if your income is under ₹4.5 lakh. The subsidy claim has to be tagged at the loan account level, not added retroactively.

Six, accept the sanction letter only after you have read the moratorium and interest terms. The deeper math on what a moratorium actually costs when interest is capitalised is in the education loan moratorium interest post.

Tax treatment and Section 80E

Once repayment starts, the interest paid each year qualifies for a deduction under Section 80E of the Income Tax Act in the hands of the person who pays it. There is no upper cap, and it is available for eight assessment years from the year repayment begins, provided the payer files under the old tax regime.

For a ₹8 lakh loan with interest of roughly ₹60,000 in the first repayment year, a parent in the 20 percent slab saves ₹12,000 a year in tax. Over the tenure that compounds into real money. The new tax regime under Section 115BAC does not allow this deduction. The official rule, summarised on the Income Tax India site, and the worked example for a typical MBBS loan is in the Section 80E education loan tax benefit post.

One related point: the National Medical Commission maintains the public list of recognised medical colleges. Any government college you matched into through NEET counselling is recognised by default. You can verify on the NMC site if a bank officer asks for proof.

Faz's ruleThe loan amount should be set by the fee receipts, not by what the bank is willing to sanction.

I have watched families accept a ₹12 lakh sanction when the actual five year fee was ₹5 lakh. Banks will lend you more than you need. Your job is to take what the receipts justify and not a rupee more.

Private MBBS is a completely different conversation

If you matched into a private or deemed medical college, the loan structure is genuinely different. Private MBBS fees run from ₹50 lakh to 1.2 crore for the course, collateral becomes mandatory at almost every lender, and the EMI math is in a different universe. Do not apply this framework to that situation. The walkthrough is in the education loan for MBBS in private college post.

The honest closing take

A government MBBS seat is one of the genuinely affordable professional degrees left in India. Fees are heavily subsidised, the loan amount needed is small, collateral is usually nil, and an interest subsidy scheme exists for families who need it most. The only people who end up with a loan they cannot manage are families who borrow more than the fee structure justifies, because they wanted a buffer that turned into a habit or because nobody at the bank pushed back when the parent asked to round up.

Look at the fee notification, total the tuition and hostel for five and a half years, add a fifteen percent buffer for books and exam fees, and stop there. If your income is under ₹4.5 lakh, ask for CSIS at sanction. If it is above, decide whether to service the interest during the course so capitalisation does not bloat the principal.

FAQ

Can I get an education loan for government MBBS in India?

Yes, every public sector bank and most private banks offer education loans for a government MBBS seat under the IBA model scheme. The course is recognised as a professional degree and government colleges are approved institutes by default. Typical loan amounts sit between ₹4 lakh and 10 lakh, reflecting the actual five and a half year fee structure, not the much higher figures that apply to private medical colleges.

How much loan can I get for a government MBBS seat?

Most families need between ₹4 lakh and 10 lakh, covering tuition, hostel, mess, books, and exam fees across the five and a half year course. For state government colleges the upper end of that range is more common. For central government institutes like AIIMS and JIPMER where tuition is nominal, the loan rarely crosses ₹4 lakh. Banks will sanction higher amounts up to ₹15 lakh in genuine out of state cases, but the loan should match the documented fee structure rather than a notional ceiling.

Is collateral required for a government MBBS education loan?

For loans up to ₹7.5 lakh, no collateral is required under the IBA model loan scheme. The co-applicant, usually a parent, signs the loan and that is the only security taken. Between ₹7.5 lakh and 10 lakh, most public sector banks will still sanction without collateral if the co-applicant’s income and credit profile are strong. Above ₹10 lakh for in-country studies, a property mortgage or fixed deposit lien is typically required, though this rarely applies to a government MBBS situation.

Am I eligible for CSIS interest subsidy on a government MBBS loan?

If your parents’ combined gross annual income is below ₹4.5 lakh, you qualify for the Central Sector Interest Subsidy. The government pays the full interest that accrues during the moratorium period (course duration plus one year). You need an income certificate from the tahsildar or revenue officer, the loan must be sanctioned under the IBA model scheme at a scheduled commercial bank, and the institute must be approved. Every government medical college qualifies as an approved institute.

What is the typical interest rate on a government MBBS loan?

Public sector banks currently price in-country education loans between 8.5 and 10.5 percent per annum. Concessions of 0.5 percent for female students and a further 0.5 percent at premier institutes are common, so the effective rate can be around 8.5 percent. Private banks sit half a percent to one percent higher. NBFC rates of 11 to 14 percent that apply to abroad studies do not apply to a small in-country MBBS loan.

Can I use the PM Vidyalakshmi portal for a government MBBS loan?

Yes. The PM Vidyalakshmi portal lets you submit a single application that is visible to multiple banks at once, which is useful if you do not have a strong existing banking relationship. The portal also routes interest subsidy claims under CSIS and the extended Vidyalakshmi subsidy framework that covers families with income up to ₹8 lakh. For a government MBBS seat, applying through the portal versus walking into a branch are both valid paths and the loan terms are identical.

What documents are needed for a government MBBS education loan?

The standard set includes the MCC or state counselling allotment letter, the college fee structure for five and a half years, KYC for student and co-applicant, mark sheets from class 10 onwards, NEET scorecard, two years of ITR or salary slips, six months of bank statements, and an income certificate from the tahsildar if claiming CSIS. Banks may ask for additional state specific documents.

Should I take a larger loan as a buffer or stick to actual fees?

Stick to actual fees plus a fifteen percent buffer for books and incidentals. A government MBBS seat is genuinely affordable and the lifetime EMI cost of borrowing money you do not need is meaningful. Interest on an unused ₹3 lakh buffer over ten years runs to more than a lakh at typical rates. Families who later regret their loan size almost always cite this exact reason.

Faz · The Honest Journey · 2026