An education loan for MBBS in Russia, Georgia or Kazakhstan from an Indian PSU bank is sanctioned only when the specific university sits on the current NMC approved list and the course satisfies the NMC FMG Regulations 2021 (54-month minimum duration plus 12-month internship in the same country). SBI Global Ed-Vantage, Bank of Baroda Vidya and Canara Bank are the three lenders that regularly fund CIS MBBS, with total all-in cost landing between ₹25 lakh and ₹40 lakh for the full six-year program. Approved-list status changes every year, so the bank checks the university’s status on the date of sanction, not the date the brochure was printed.

Every March, somebody from a tier-3 town writes to me with a brochure from an agent saying their child has secured an MBBS seat in Volgograd or Tbilisi or Karaganda for an all-in package of ₹22 lakh, and the agent has promised the bank loan will be sanctioned “easily” because the university is “fully NMC approved”. The brochure is always glossy. The promise is rarely accurate.

The CIS country MBBS route is real, it is legitimate, and for a chunk of Indian students it is the only realistic path into a medical degree when the NEET rank does not buy a domestic government seat and the private Indian college fee runs into a crore. But the loan side of it sits on rules most agents either do not know or do not bother to mention, and those rules can stop a sanction in its tracks.

More on funding an MBBS abroad: the education loan for MBBS government college post.

The rule that decides everything: NMC FMG Regulations 2021

Before any bank, before any cost calculation, before any agent conversation, the regulation that decides whether your foreign MBBS will let you practice in India is the National Medical Commission’s FMG Regulations 2021. The PSU banks read this regulation directly, because if a graduate cannot register with the NMC, the loan turns into an unsecured liability with no earning trajectory behind it.

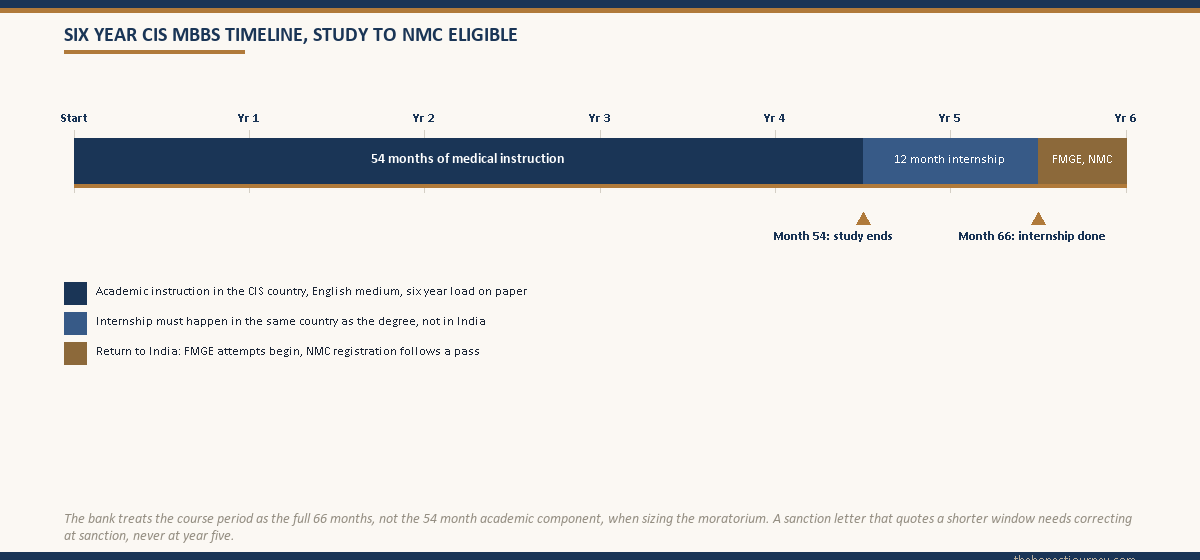

Three hard conditions sit inside that regulation. The course duration must be at least 54 months of medical instruction. The 12-month internship must happen in the same country where the degree was obtained, not split between countries, not done back in India. And the foreign medical institution must be on the NMC approved list at the time of admission and at the time of graduation.

The bit that catches families out is the third one. The NMC approved list is reviewed and republished by the regulator. Some Russian, Georgian and Kazakhstani universities that were considered routine destinations five years ago were removed from the list during the 2023 to 2024 review cycle. I am deliberately not naming a list of “approved universities” in this post, because anything I write today can be stale within six months. The only place to verify is nmc.org.in itself, and the bank will check the same source.

Faz's ruleTreat the agent's claim of NMC approval as a starting point, never as evidence. Confirm directly on nmc.org.in on the day you sign the agent contract and again on the day the bank requests it for sanction.

I have seen two cases in the last two years where the family signed the agent fee, the student travelled, and only then did the bank flag that the specific university was no longer on the current list. One family lost a year. The other lost the deposit. The five minutes it takes to verify on the regulator’s own site is the cheapest insurance in this whole process.

What 54 months plus 12 months actually means for the loan

The 54-month duration is what makes the CIS MBBS a six-year academic load on paper, not the four-and-a-half-year program that some agents pitch. Add the 12-month internship that must be completed in the country of study, and the total time from arrival to NMC-eligible graduation is six years.

This matters for the loan moratorium and the disbursement timeline. Indian banks set the moratorium as “course period plus 6 to 12 months grace”. For a CIS MBBS, the course period in the bank’s eyes is the full six years (54 months of study plus 12 months of internship), not five. If the bank’s sanction letter quotes a shorter moratorium because the underwriting officer misunderstood the course structure, you fix that at sanction, not at the end of year five when you suddenly have an EMI you cannot pay because you are still doing your internship.

The internship year is also when the loan disbursement structure tends to confuse families. Some universities pay a small stipend during the internship year. Some do not. Either way, the bank’s tranche for year six still has to cover living costs, because the internship year is part of the program and the moratorium has not ended. I have laid out the general flow in the education loan disbursement process post, and the CIS MBBS case follows the same logic with one extra annual tranche.

The real cost of a CIS MBBS, end to end

The number agents quote is the tuition figure converted to INR at last year’s exchange rate, rounded down, with hostel and food bundled into a “package”. The number the bank underwrites is everything: tuition, hostel, food, agent fee (where declared), insurance, visa, flights, books, NEET coaching for FMGE prep on return, and a buffer for currency movement.

| Cost head | Russia (6 yrs) | Georgia (6 yrs) | Kazakhstan (6 yrs) |

|---|---|---|---|

| Tuition total | ₹18 to 28 lakh | ₹22 to 32 lakh | ₹16 to 24 lakh |

| Hostel + food (6 yrs) | ₹6 to 9 lakh | ₹6 to 10 lakh | ₹5 to 8 lakh |

| Visa, residence permit, insurance | ₹80k to 1.2 lakh | ₹60k to 1 lakh | ₹60k to 1 lakh |

| Flights (6 trips) | ₹2 to 3 lakh | ₹1.5 to 2.5 lakh | ₹1.5 to 2.5 lakh |

| Books, equipment, miscellaneous | ₹1.5 to 2 lakh | ₹1.5 to 2 lakh | ₹1.5 to 2 lakh |

| Total all-in | ₹28 to 40 lakh | ₹30 to 47 lakh | ₹25 to 36 lakh |

These bands are wide on purpose. Tuition at a state medical university in Russia is materially lower than at one of the federal medical universities. Georgia has a wider spread because the English-medium private medical universities there charge closer to Eastern European rates. Kazakhstan tends to be the lowest of the three on tuition, but flight connectivity from south India bumps the travel head.

The reason the band matters for the loan is that PSU banks size the sanction off your declared total cost, not off a country average. If you under-declare and run short in year three, the bank can refuse a top-up. If you over-declare and the unutilised sanction is large, the unused portion is harmless because interest accrues only on the disbursed amount, but the co-applicant has been judged for a larger commitment than was needed.

Which Indian banks actually fund CIS MBBS, and on what terms

Three PSU banks do the bulk of CIS MBBS loans: State Bank of India under the Global Ed-Vantage scheme, Bank of Baroda under Baroda Vidya for studies abroad, and Canara Bank under its overseas education loan product. A handful of other PSU banks (Union Bank, PNB) also fund CIS MBBS but with smaller portfolios and more conservative underwriting.

The base terms across the three look broadly similar but with meaningful differences once you read the small print.

SBI Global Ed-Vantage will sanction up to ₹1.5 crore for overseas studies, which is far above what any CIS MBBS will require. For a CIS MBBS loan of ₹30 to 40 lakh, SBI typically asks for tangible collateral above ₹7.5 lakh (immovable property, fixed deposit, LIC policy at surrender value). The interest rate sits around 1-year MCLR plus a spread, with concessions for female students and for collateral above 100 percent of the loan.

Bank of Baroda’s Baroda Vidya for studies abroad has a similar ceiling and a similar collateral threshold. The difference shows up at disbursement. BOB tends to be slightly faster on the SWIFT side for Russian and Kazakh remittances because the bank has dealt with those university accounts more times. Georgia, being newer on its books, sometimes takes longer for first-time tranches.

Canara Bank’s product is structurally similar but the underwriting team has historically been more conservative on Russia after some of the 2024 list changes. Sanctions still happen, but the credit officer is more likely to ask for a written confirmation from the university that the program duration matches the FMG Regulations 2021.

NBFCs (Avanse, Auxilo, Credila, InCred) do fund CIS MBBS unsecured up to ₹50 lakh in many cases, which is the route families take when there is no collateral to offer. The interest rate is 2 to 4 percentage points higher than PSU banks, and the NBFC is not bound by the IBA Model Education Loan Scheme, which means the borrower protections are weaker. The flip side is faster sanction and a smaller paperwork load. For families without property to pledge, this is sometimes the only realistic route; for families who can pledge, the PSU bank is almost always cheaper across the loan life. The full unsecured comparison sits in the education loan for abroad studies without collateral post.

Faz's ruleIf you can pledge collateral, go PSU. If you cannot, go NBFC with eyes open. Do not let an agent push you toward an NBFC just because the paperwork is lighter for them.

Agents prefer NBFC routings because the commission cycle is faster and the documentation is simpler. The cost of that convenience is yours to pay every month for ten years. If you have a residential property anywhere in India that can clear the bank’s valuation, the SBI or BOB route is usually two to three percentage points cheaper across the life of the loan, which on ₹35 lakh adds up to several lakhs.

What the bank actually checks before sanctioning CIS MBBS

The standard education loan paperwork (co-applicant income, KYC, admission letter, cost breakdown) applies. The CIS MBBS file adds three extra checks that families need to be ready for.

First, the bank verifies the university’s NMC approved-list status as of the sanction date. Most PSU branches do this by pulling the current list from nmc.org.in and matching the university name exactly. If the agent has used a slightly different transliteration of a Russian or Georgian university name on the admission letter than appears on the NMC list, the file pauses while the bank requests a clarification letter from the university.

Second, the bank confirms the program duration on the admission letter matches the 54-month rule. Some CIS universities issue admission letters that mention only the academic component (4.5 to 5 years) without mentioning the internship year separately. The bank wants both in writing, ideally on the same letter.

Third, the bank checks the fee structure against the university’s published international student fee on its official website. Agents sometimes inflate the figure on the admission letter to cover their own commission, which then forms part of the loan. PSU banks have been catching this more often since 2023, and the safer path is to ask the agent to issue a separate, transparent fee receipt rather than bundling commission into tuition.

Beyond these three, the bank will also look at the co-applicant’s repayment capacity over a six-year moratorium plus a 10 to 15 year repayment window. A weak co-applicant profile is the single biggest reason CIS MBBS loans get rejected at the underwriting stage; the foreign destination only matters once the income side is cleared. The full list of reasons sits in the education loan rejection reasons India post.

The FMGE reality, said honestly

The Foreign Medical Graduate Examination, conducted by the National Board of Examinations in Medical Sciences, is the screening test every foreign medical graduate must clear to register and practice in India. The pass rate has historically sat below 25 percent, with some sittings closer to 15 percent.

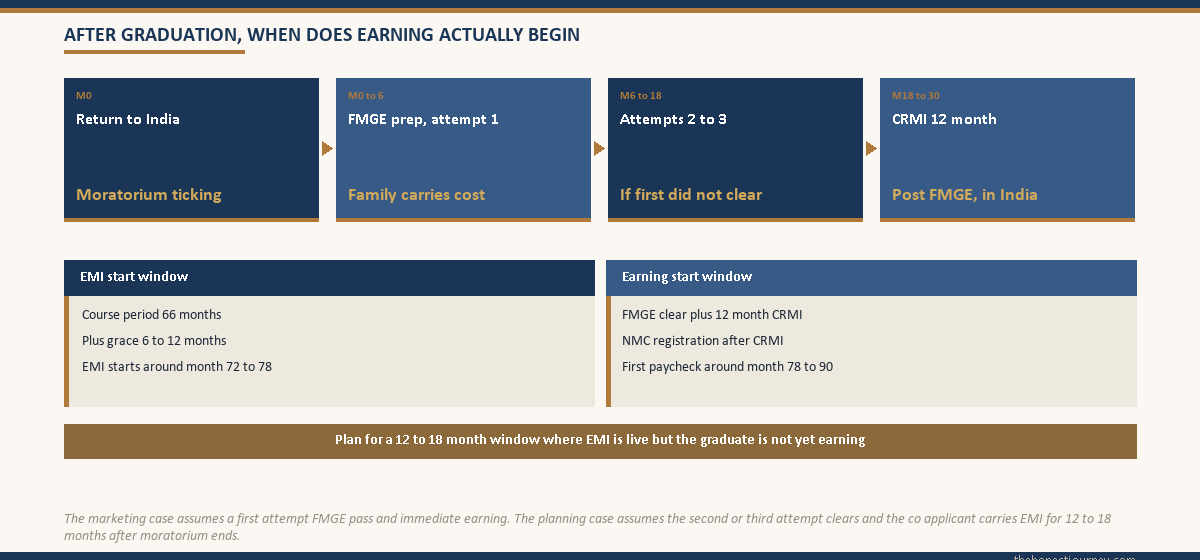

This number gets quoted to scare families away from foreign MBBS entirely, and it gets quoted in agent rebuttals as “the rate is improving”. Both can be true. The pass rate has been climbing since 2022 as more graduates take dedicated coaching after returning and as the FMG Regulations 2021 have raised the floor on what a foreign medical curriculum must cover. But “improving” is not the same as “high”. A realistic planning assumption for a CIS MBBS graduate is that the first attempt may not clear, that the second or third attempt is more likely to succeed if approached with dedicated preparation, and that the loan moratorium accommodates roughly 6 to 12 months of grace before EMI starts.

For the family, what this means in cash terms is that the EMI start date may fall in a window where the graduate is still preparing for FMGE attempts or doing the post-FMGE internship that NMC requires before final registration. The co-applicant carries the EMI during that window. If the co-applicant cannot, the loan goes into stress, and education loan stress on a 30 to 40 lakh balance is not a small thing to recover from.

None of this is a reason to write off the route. It is a reason to size the loan against the realistic worst-case timeline (graduate clears FMGE on second or third attempt, EMI carried by family for 18 to 24 months post-moratorium), not the marketing-case timeline (graduate clears first attempt, registers immediately, starts earning before EMI begins).

Country-by-country notes from what families have actually navigated

Russia is the largest of the three by Indian student enrolment. The state medical universities in cities like Volgograd, Kazan, the Crimean Federal region, Perm and Tver have been routine destinations for two decades. The cost is the lowest of the three for tuition, and the program is taught in English at most universities for international students. The list changes I mentioned earlier hit some Russian universities harder than others; the names on today’s list are not the same as the names on the 2020 list. Verify current status on nmc.org.in.

Georgia has risen sharply over the last five years, especially Tbilisi State Medical University and a few of the private English-medium medical universities. The pitch is European feel, English instruction throughout, smaller class sizes. The cost is the highest of the three on tuition. The banks are comfortable with Georgia in principle but the file moves more slowly because the SWIFT corridor is newer and the bank’s compliance team has fewer past remittances to reference.

Kazakhstan, with universities in Karaganda, South Kazakhstan and Astana, sits between the two on cost and visibility. The Indian student population is smaller than in Russia but growing. The loan side is straightforward when the university is on the NMC list; the practical challenge tends to be the flight connectivity from smaller Indian cities, which adds to the annual travel cost more than families budget for.

Across all three, the recurring theme is the same. The university name on the agent’s brochure is not what matters. What matters is the exact, current NMC-listed name, the program duration on the admission letter, and the bank’s willingness to verify both before disbursing the first tranche.

The honest closing take

CIS MBBS is a legitimate route into medicine for Indian students who cannot get a domestic government seat and cannot afford a domestic private one. The loan side of it is workable. The path that goes wrong is the one where the family treats the agent’s brochure as gospel, skips the NMC verification, takes the cheapest NBFC route without comparing PSU options, and assumes the FMGE will be cleared on first attempt.

The path that goes right is the one where the family verifies the university on nmc.org.in before signing the agent, takes the loan from the PSU bank that gives the lowest rate (which almost always means pledging collateral), sizes the loan to a six-year cost band with currency buffer, and plans the post-graduation cashflow assuming a 12 to 18 month gap between graduation and the first paycheck.

This is not a route that rewards optimism. It rewards documentation. The students who navigate it cleanly are the ones who treat every promise as something to verify on a government website, and who keep the bank, the agent and the family on the same page in writing.

FAQ

Is MBBS in Russia NMC approved?

Specific Russian medical universities are on the NMC approved list, and others are not. The list is reviewed and republished by the National Medical Commission, and some universities that were considered routine five years ago were removed during the 2023 to 2024 review cycle. The only authoritative source is the current list on nmc.org.in. Banks check the same source before sanctioning a loan. Treat any agent claim of “fully NMC approved” as a starting point that needs verification on the regulator’s website on the day of admission and again on the day the loan is requested.

Which Indian banks fund MBBS abroad in CIS countries?

The three PSU banks that handle the bulk of CIS MBBS loans are State Bank of India under Global Ed-Vantage, Bank of Baroda under Baroda Vidya for studies abroad, and Canara Bank under its overseas education loan product. Union Bank and PNB also fund these destinations with more conservative underwriting. NBFCs (Avanse, Auxilo, Credila, InCred) fund the unsecured cases up to around ₹50 lakh, at interest rates 2 to 4 percentage points higher than PSU banks. The PSU route is cheaper across the loan life if collateral can be pledged.

How much does MBBS in Russia, Georgia or Kazakhstan cost in total?

The all-in cost for six years (54 months of study plus 12 months of mandatory in-country internship) lands roughly between ₹25 lakh and ₹40 lakh, with Kazakhstan typically at the lower end and Georgia at the higher end. This includes tuition, hostel and food, visa and residence permit, insurance, six round-trip flights, books and equipment, and a buffer for currency movement. The agent’s quoted “package price” usually covers tuition and hostel only and misses the recurring annual costs that the bank’s underwriting will include in the sanction.

What is the FMGE pass rate for CIS MBBS graduates?

The Foreign Medical Graduate Examination has historically had a pass rate below 25 percent across all foreign destinations, with some sittings closer to 15 percent. The rate has been climbing since 2022 as graduates take dedicated coaching and as the FMG Regulations 2021 have raised the minimum curriculum standard. A realistic planning assumption is that the first attempt may not clear and that the second or third attempt is more likely to succeed with focused preparation. The loan moratorium typically accommodates this window before EMI begins.

Is Georgia MBBS approved by NMC for Indian students?

Specific Georgian medical universities are on the current NMC approved list and graduates from those universities are eligible to sit the FMGE and register with the NMC after clearing it. The university name must appear on the list at the time of admission and at the time of graduation. Verification is done on nmc.org.in, not on the agent’s brochure or the university’s own website. Indian banks check the same source before sanctioning a loan for any Georgian medical university and the file pauses if the name does not match exactly.

Can I get an unsecured education loan for MBBS abroad?

Yes, NBFCs like Avanse, Auxilo, Credila and InCred fund unsecured education loans for MBBS abroad, typically up to ₹50 lakh, depending on the co-applicant’s profile and the university’s standing. PSU banks generally ask for tangible collateral on loan amounts above ₹7.5 lakh, which covers most CIS MBBS cases. The trade-off is interest rate: NBFC rates are 2 to 4 percentage points higher than PSU rates, and NBFCs are not bound by the IBA Model Education Loan Scheme, which means borrower protections are weaker.

Why does the internship have to be in the same country as the degree?

The NMC FMG Regulations 2021 require the foreign medical graduate to complete a 12-month internship in the same country where the medical degree was obtained. The reason is curriculum integrity: the regulation aims to ensure clinical training matches the standards of the institution that taught the academic component, rather than being completed in a different jurisdiction with different protocols. Internships split between countries or done back in India after the degree do not satisfy the regulation and the graduate will not be eligible to sit the FMGE.

What happens if the bank refuses my CIS MBBS loan after I have paid the agent?

This situation is unfortunately common when families pay the agent before securing the loan in writing. Recovery of the agent fee depends on the contract; many agent contracts are written to protect the agent’s commission on enrolment, not on visa or loan outcome. The cleaner sequence is to verify NMC status, get a loan in-principle approval from at least one PSU bank, confirm the university name matches exactly on both documents, and only then sign the agent’s enrolment paperwork. The five-day delay this adds at the start saves much larger losses later.

Faz · The Honest Journey · 2026