An education loan for pilot training in India typically covers ₹35 lakh to ₹50 lakh for the CPL, but the real all-in cost runs ₹55 lakh to ₹75 lakh once you add the type rating. Banks like SBI, BoB, and Axis fund CPL programmes at 10.5 to 13 percent, with a 1 to 2 year moratorium. Most students need a top-up or family contribution for the type rating, since lenders rarely fold it in upfront.

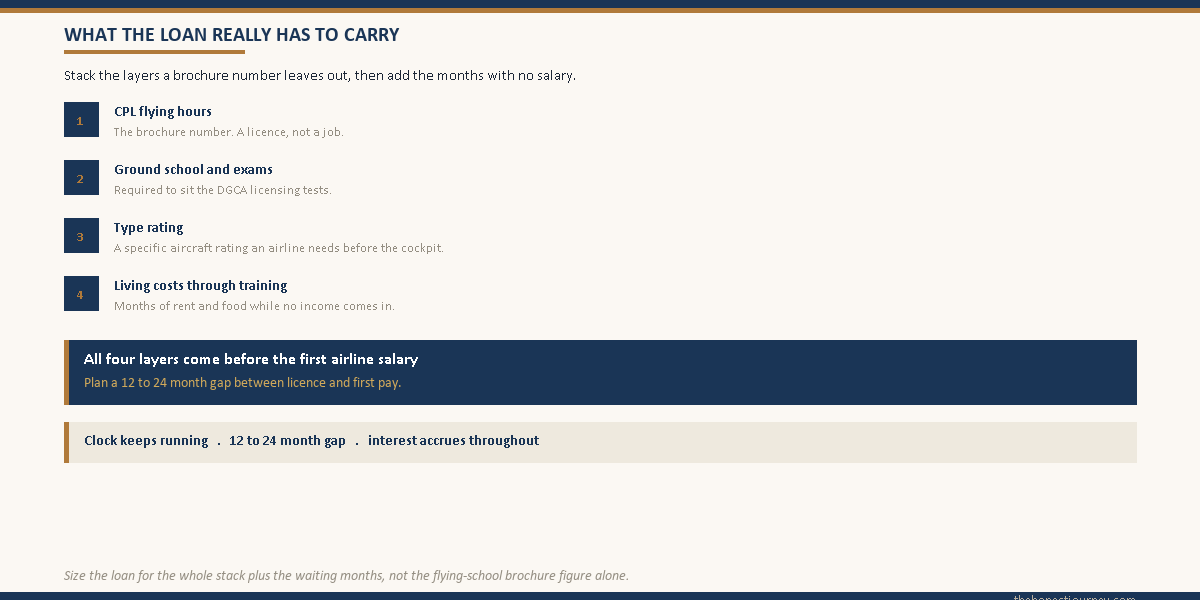

You worked out the cost of a Commercial Pilot Licence the way most aspiring pilots do: you added up the flying-school brochure figure, told yourself the loan would cover it, and assumed an airline job at the end. The brochure said ₹35 lakh. What it did not say is that ₹35 lakh gets you a licence, and a licence is not a job. The job needs a type rating, and the type rating costs another ₹15 lakh to 25 lakh that nobody folds into the brochure number.

This post is for the student or parent staring at a pilot-training quote and trying to figure out what the loan really has to carry. I will give you the honest cost, the honest loan reality, and the part most lender blogs skip entirely.

Yes, you can get an education loan for pilot training, but only at a DGCA-approved institute, and almost always with collateral once the amount crosses ₹7.5 lakh. The bigger issue is not getting the loan. It is that the loan covers the licence while the airline job depends on a hiring cycle, a type rating, and timing you do not control. Size the loan for the gap, not just the course.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

Other eligibility situations worth reading: the education loan rejection reasons india post, the education loan without ITR post, and the education loan for working professionals post.

What a CPL actually costs in 2026

Pilot training is one of the most expensive professional courses an Indian student can take, and the headline number you see advertised is rarely the number you end up paying. A flying school quotes you the cost of the flying hours required for a Commercial Pilot Licence. It does not always quote the ground school, the licensing exams, the medical, the extra hours you will almost certainly need beyond the minimum, or the type rating that comes after.

Here is the honest range, separated so you can see where the money actually goes.

| Cost component | India (DGCA CPL) | Abroad (USA, South Africa, etc.) |

|---|---|---|

| Flying hours (200 hours minimum) | ₹25 lakh to 55 lakh | ₹25 lakh to 60 lakh |

| Ground school and licensing exams | ₹1.5 lakh to 4 lakh | ₹2 lakh to 6 lakh |

| DGCA conversion (for foreign licence) | Not applicable | ₹3 lakh to 8 lakh |

| Living and accommodation during training | ₹3 lakh to 8 lakh | ₹8 lakh to 20 lakh |

| Total to reach CPL | ₹25 lakh to 80 lakh | ₹30 lakh to 1.5 crore |

| Type rating (after CPL, separate) | ₹15 lakh to 25 lakh | ₹15 lakh to 30 lakh |

Read the last two rows together. The spread inside India alone runs from ₹25 lakh to ₹80 lakh, and the reason is not just the school. Weather delays, aircraft availability, and the simple fact that most cadets need 220 to 260 hours rather than the textbook 200 all push the bill up. A quote built on the minimum hours is a quote built on a best case that rarely holds.

And then the type rating. A CPL lets you fly. A type rating on a specific aircraft, an Airbus A320 or a Boeing 737, is what an airline actually needs before it puts you in a cockpit. Most Indian airlines expect the cadet to fund or co-fund this. So when you plan the loan, the real target is not the CPL number. It is the CPL number plus the type rating, because a licence without a type rating is a licence that does not pay.

Faz's ruleThe brochure number is the licence. The loan number is the licence plus the type rating plus the months with no salary.

Flying schools quote the cost of the licence because that is the product they sell. The type rating is sold separately, often by a different provider, so it stays off the brochure. If you size the loan to the brochure, you fund the licence and stall before the job.

Can you actually get an education loan for pilot training?

Yes, and pilot training is explicitly recognised as a fundable course under the Indian Banks’ Association Model Education Loan Scheme, the framework published on the IBA site. But there are conditions that matter more here than for a regular degree loan.

The institute must be DGCA-approved. Banks fund flying training only at a Flying Training Organisation approved by the Directorate General of Civil Aviation, or at a recognised foreign institute that leads to a DGCA-convertible licence. You can check an institute’s approval status on the official DGCA website before you pay a single rupee. If a school cannot show current DGCA approval, no mainstream bank will fund it, and you should treat that as a warning rather than an inconvenience.

Collateral is usually required above ₹7.5 lakh. Under the standard scheme, loans up to ₹4 lakh need no security, loans from ₹4 lakh to ₹7.5 lakh need a third-party guarantee, and loans above ₹7.5 lakh need tangible collateral. Pilot training almost always crosses ₹7.5 lakh, so in practice you should expect to pledge property, a fixed deposit, or another acceptable asset. A small number of NBFCs offer larger unsecured amounts on a strong co-applicant profile, but at a higher rate. The collateral-free route and its limits are covered in the education loan without collateral post.

A co-applicant with stable income is mandatory. The bank assesses repayment capacity on the co-applicant, normally a parent, because the cadet has no income yet. The co-applicant’s income, existing obligations, and credit history carry the file. Why the co-applicant matters so much, and how lenders assess them, is covered in the co-applicant for an education loan post.

Interest rates for pilot-training loans start from around 9.75% on a collateral-secured loan from a public sector bank and run up to 13% or higher on an unsecured NBFC loan. The rate is repo-linked, so it moves with the policy rate the RBI sets over the life of the loan, and the collateral norms also follow the central bank’s lending framework.

Which lenders fund pilot training, and on what terms

Most large public sector banks fund pilot training under their standard education loan products. State Bank of India, for example, lists aviation and pilot training as eligible job-oriented courses under its education loan scheme. Private banks and aviation-focused NBFCs also lend in this space, often with faster processing but a higher rate.

Here is the broad picture. Treat the figures as a planning range, not a quote, because every file is priced on its own collateral and co-applicant strength.

| Lender type | Typical loan ceiling | Indicative rate | Collateral expectation |

|---|---|---|---|

| Public sector bank (secured) | Up to ₹1.5 crore | 9.75% to 11.5% | Property or FD pledged |

| Private bank | Up to ₹60 lakh to 80 lakh | 10.5% to 13% | Often required above ₹20 lakh |

| NBFC (unsecured, strong profile) | Up to ₹40 lakh to 50 lakh | 12% to 14.5% | None, priced into the rate |

The pattern is the same as any large education loan. The cheapest money is the slowest and the most paperwork-heavy, because a property valuation and a legal report take weeks. The fastest money is the most expensive. For a course this large, a 2% rate gap is not small. On ₹50 lakh over 12 years, the difference between 9.75% and 12% is well over ₹12 lakh in total interest. If you have collateral to pledge, the secured route is almost always worth the extra wait.

One practical note on disbursement. The bank releases the loan in tranches against the flying school’s fee schedule, not as a lump sum into your account. So the school’s billing pattern, upfront versus phased, affects how the loan is drawn and when interest starts running on each tranche. Ask for the fee schedule in writing before you finalise the loan amount, and keep the documentation tight. The full list of what banks ask for is in the documents required for an education loan post.

Faz's ruleA DGCA-approved institute is not optional. It is the line between a fundable loan and no loan at all.

Check the approval status yourself on the DGCA site, do not rely on the school’s word. An institute that loses or lacks approval can leave a cadet mid-training with a loan running and no path to a licence. This is the single check that protects you most.

The part lender blogs skip: the gap between licence and job

This is the section that matters most, and it is the one almost no lender or flying-school page will write honestly, because it does not help them sell.

An education loan has a moratorium. You do not pay EMIs while you train, plus a grace period of 6 to 12 months after the course ends. The assumption baked into that grace period is that you walk into a paid job within a year of finishing. For a pilot, that assumption is fragile.

Airline hiring is cyclical. It tracks fleet expansion, fuel prices, the broader economy, and route demand. In a strong cycle, a fresh CPL holder with a type rating can get a cadet or first officer slot within months. In a weak cycle, the same candidate can wait a year or longer, and the licence has a currency requirement, which means you may need to keep flying to stay valid. Flying to stay current costs money. Your loan is accruing interest the whole time.

There is also the sequencing problem. You finish your CPL. The grace period clock starts. But the airline job needs a type rating you have not done yet, and the type rating itself takes a few months plus another large sum. So the realistic timeline from “licence in hand” to “first salary credited” is often 12 to 24 months, while the loan’s grace period assumed 6 to 12. Interest accrues through every month of that gap, and on an education loan it is typically capitalised, added to your principal at the end of the moratorium. How that capitalisation works, and what it does to your EMI, is laid out in the education loan moratorium and interest post.

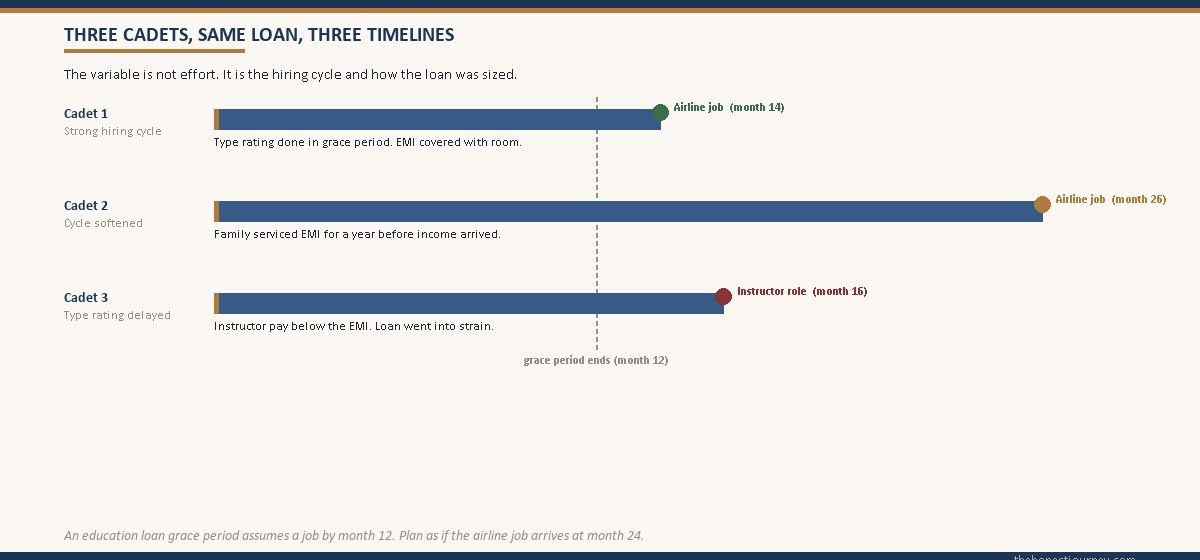

Three honest scenarios

The same loan, the same course, three different outcomes. The variable is not the cadet’s effort. It is timing and how the loan was sized.

The one who landed the airline job. A 21-year-old completed a DGCA CPL at an approved institute in India, financed with a ₹55 lakh secured loan at 10% co-signed by a parent. He finished training in a strong hiring cycle, did his A320 type rating during the grace period, and joined a domestic carrier as a first officer about 14 months after his licence. His first-year pay covered the EMI of roughly ₹65,000 with room to spare. The loan worked because the cycle cooperated and the loan amount included the type rating from the start.

The one who took two years. A 23-year-old trained abroad, returned with a foreign licence, and spent eight months on the DGCA conversion process and exams. Then the hiring cycle softened. Her type rating slot and a first officer offer finally came together about 26 months after she got her licence. The loan’s grace period had long ended, so EMIs began before she had income. Her family serviced the EMI for almost a year out of pocket. She is flying now and the loan is on track, but the family absorbed a cost the brochure never mentioned, and the capitalised interest from those extra months made the loan larger than planned.

The one who could not service the EMI. A 24-year-old finished a CPL, could not afford the type rating immediately, and took a flight-instructor role to build hours and earn something. Instructor pay in India is modest, often well below ₹40,000 a month early on. The EMI on his ₹60 lakh loan was above his entire instructor salary. The loan went into strain, the family stepped in, and the type rating got pushed out by years. He may still reach an airline job, but the loan was sized for a best-case timeline that did not arrive.

The honest pattern across all three: the loan amount and the moratorium were built on an assumption of fast hiring. When hiring cooperated, it worked. When it did not, the family carried the gap. Plan for the slow case, not the fast one.

Faz's ruleBorrow as if the airline job arrives 24 months after your licence, not 6.

Hiring cycles are real and you do not control them. If your loan and your family budget can survive a 24-month gap between licence and first salary, you have planned honestly. If they only survive the brochure timeline, you have planned on hope.

What the EMI actually looks like

Pilot-training loans are large, so the EMI is large. A useful planning benchmark: at roughly 10.5% over a 12-year repayment tenure, the EMI works out to close to ₹1,250 per lakh borrowed per month, before any moratorium interest is capitalised.

That means a ₹40 lakh loan carries an EMI near ₹50,000 a month, and a ₹70 lakh loan carries an EMI near ₹87,000 a month. Add the capitalised moratorium interest and the real EMI sits higher than these figures, because the principal you repay on is larger than the amount you borrowed.

Now hold that against entry-level pilot income. A first officer at an Indian carrier can earn a healthy salary once flying regularly, often enough to service even a large EMI. But a flight instructor, or a licence holder still waiting for a type rating and a job, earns far less. The EMI does not adjust to your employment status. This is why the gap planning matters more than the rate negotiation. A 0.5% better rate saves you a few lakh over the tenure. A two-year delay before income, with EMIs running, can be the difference between a manageable loan and a defaulted one.

The honest closing take

An education loan for pilot training is real, accessible, and reasonable to take, if you go in with clear eyes. The course is fundable, the rates are not predatory at a public sector bank, and a pilot’s career income, once established, can comfortably carry the loan.

The risk is not in the loan product. It is in the gap. The single mistake that turns a workable pilot-training loan into a family crisis is sizing it to the flying-school brochure and the bank’s optimistic 6-to-12 month grace period. The brochure leaves out the type rating. The grace period assumes a hiring cycle that may not arrive on schedule.

So plan the loan around the full path: CPL plus type rating plus 18 to 24 months of possible waiting with interest running. Pledge collateral if you have it, because the rate saving on a sum this large is substantial. If your family can service simple interest during the moratorium, do it, because it stops the capitalisation that quietly inflates the principal. And be honest with yourself about the hiring cycle, because no amount of training effort speeds up an airline that is not recruiting.

Pilot training can be a sound investment with a strong long-term return. Whether to take a loan of this size, knowing the gap is real, is a decision only you and your family can make.

FAQ

Can I get an education loan for pilot training?

Yes. Pilot training is a recognised job-oriented course under the IBA Model Education Loan Scheme, and most public sector banks, several private banks, and aviation-focused NBFCs fund it. The key condition is that the flying institute must be approved by the DGCA, or be a recognised foreign institute leading to a DGCA-convertible licence. You will also need a co-applicant with stable income, since the cadet has no earnings yet, and collateral once the amount crosses ₹7.5 lakh.

How much loan can I get for a CPL?

It depends on the lender and your collateral. A secured loan from a public sector bank can go up to around ₹1.5 crore, which comfortably covers a CPL plus type rating. Unsecured NBFC loans are usually capped near ₹40 lakh to 50 lakh on a strong co-applicant profile. Since a CPL in India costs ₹25 lakh to 80 lakh and abroad ₹30 lakh to 1.5 crore, plan the loan to include the type rating, not just the licence.

Is collateral needed for a pilot training loan?

Usually, yes. Under the standard scheme, loans up to ₹4 lakh are collateral-free, ₹4 lakh to 7.5 lakh need a third-party guarantee, and loans above ₹7.5 lakh need tangible collateral such as property or a fixed deposit. Pilot training almost always exceeds ₹7.5 lakh, so most cadets pledge an asset. Some NBFCs offer larger unsecured amounts on a strong co-applicant, but at a noticeably higher interest rate.

Which bank gives pilot training loans?

Most large public sector banks fund pilot training under their standard education loan products, with State Bank of India listing aviation and pilot training as eligible courses. Private banks and aviation-focused NBFCs also lend in this space, typically with faster processing but higher rates. Secured public sector bank loans carry the lowest rates, from around 9.75%. Compare the rate, the collateral requirement, and the disbursement schedule before choosing, since all three affect the real cost.

Does an education loan cover type rating?

It can, but only if you include the type rating in the sanctioned amount from the start. Many cadets size the loan to the CPL course alone, then find the loan is fully drawn before the type rating, which costs another ₹15 lakh to 30 lakh. Either request a single loan that covers both, or plan a top-up later. A type rating without a CPL is not fundable, and a CPL without a type rating rarely leads to an airline job.

What is the EMI on a pilot training loan?

At roughly 10.5% over a 12-year tenure, the EMI is close to ₹1,250 per lakh borrowed per month. That puts a ₹40 lakh loan near ₹50,000 a month and a ₹70 lakh loan near ₹87,000 a month. The real EMI is higher, because interest that accrued during the moratorium gets capitalised into the principal. A first officer’s salary can carry this, but a flight instructor’s early income often cannot.

What happens to the loan if I do not get an airline job quickly?

The loan does not wait. The moratorium grace period is usually only 6 to 12 months after the course ends, but the realistic gap between getting a licence and a first salary can be 12 to 24 months, given type rating timing and airline hiring cycles. Interest accrues through that gap and is typically capitalised, raising your principal. If EMIs start before you have income, your family has to service them. Plan for the slow case.

Can I claim a tax deduction on a pilot training loan?

Yes. Interest paid on an education loan for a recognised course, including pilot training, qualifies for a deduction under Section 80E of the Income Tax Act. There is no cap on the deduction amount, and it applies for up to 8 years from the year repayment begins. The deduction is available to whoever repays the loan, often the co-applicant parent. It only helps under the old tax regime, so check which regime your co-applicant files under.

Faz · The Honest Journey · 2026