An education loan without ITR is possible: most public sector banks accept Form 16, salary slips, or a CA-certified income declaration in place of an ITR when the co-applicant is salaried or runs a non-filing small business. SBI, Bank of Baroda, and Canara accept Form 16 alone for loans up to ₹20 lakh. NBFCs like Avanse and InCred go further and underwrite on bank statements plus GST returns.

The first time a relationship manager asked my friend’s father for three years of ITR, the conversation stopped cold. He ran a small auto-parts shop, paid GST, did ₹80 lakh in current-account turnover, and had never filed an income tax return because his CA had said for years he fell below the threshold after deductions. The executive shrugged and said the file could not move forward.

An education loan without ITR is possible. Most banks (and almost every blog on this topic) treat ITR as the only acceptable income proof, when lenders actually accept a documented matrix of substitutes depending on what kind of earner your co-applicant is. This post is the matrix: what works, what does not, and which lender categories will approve the file.

Answer capsule: An education loan without ITR is approvable when the co-applicant provides equivalent income proof. Self-employed: GST returns, 12-month bank statements, business registration, and a CA-certified income statement. Agricultural: 7/12 extract, land records, crop receipts, and market-yard committee slips. Housewife: spouse as primary co-applicant with their salary or rental and FD interest certificates. Pensioner: PPO copy and pension account credits. NBFCs are more flexible than PSU banks.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

Other eligibility situations worth reading: the education loan for working professionals post, the education loan for distance mba post, and the education loan with backlogs india post.

Why banks ask for ITR in the first place

An education loan is not approved on the student’s profile. It is approved on the co-applicant’s capacity to service the EMI if the student cannot. The lender’s risk team needs two answers: is the declared income real, and what is the Fixed Obligation to Income Ratio (FOIR) after factoring in this new EMI. ITR is the cleanest single document that answers both, because it is filed with the government, verifiable on the income tax portal, and shows a multi-year pattern.

When ITR is missing, the lender reconstructs the same picture from other documents. They are not refusing your file. They are asking you to assemble proof that adds up to the same confidence level. The Income Tax Department itself sets filing thresholds, and many small business owners, agricultural families, and pensioners legitimately fall below them. Absence of ITR is not a red flag. The bank’s question is simply, “How do I verify income then.” That is a documentation question, not a character question.

Faz's ruleNo ITR is not a no. It is a request to prove income through a different document stack.

Most rejections at this stage happen because the family walks away after the first conversation. The loan is not refused. The bank has just asked a second question, and the family does not know they are allowed to answer it differently.

The four co-applicant profiles and what each one needs

Almost every “no ITR” case I have seen falls into one of four buckets. The required document stack is different for each. Mixing them up is one of the top reasons files get returned at the verification stage, so the matrix below is worth reading slowly.

| Co-applicant type | Primary proof | Secondary proof | Income verification anchor |

|---|---|---|---|

| Self-employed (no ITR) | GST returns (last 12 months) | Current account statements (12 months), GST registration, Udyam/MSME certificate | CA-certified income statement on letterhead with UDIN |

| Agricultural income | 7/12 extract or Patta and Chitta | Crop sale receipts, APMC market-yard slips, Kisan Credit Card statement | Tehsildar or revenue officer’s land-holding certificate |

| Housewife as co-applicant | Rental agreement and rent credits in account | FD interest certificates, dividend statements, mutual fund SoA | Spouse joined as second co-applicant with their salary slips or ITR |

| Pensioner | PPO (Pension Payment Order) copy | Pension account statement (last 12 months), Form 16 from pension disbursing authority | Bank-stamped pension credit certificate |

The right-hand column is what makes the file bankable. Without an anchor, the rest of the stack reads as “claimed income.” With it, the stack reads as “documented income.” That single shift moves a file from pending to sanctioned.

Self-employed without ITR: the documentation that actually works

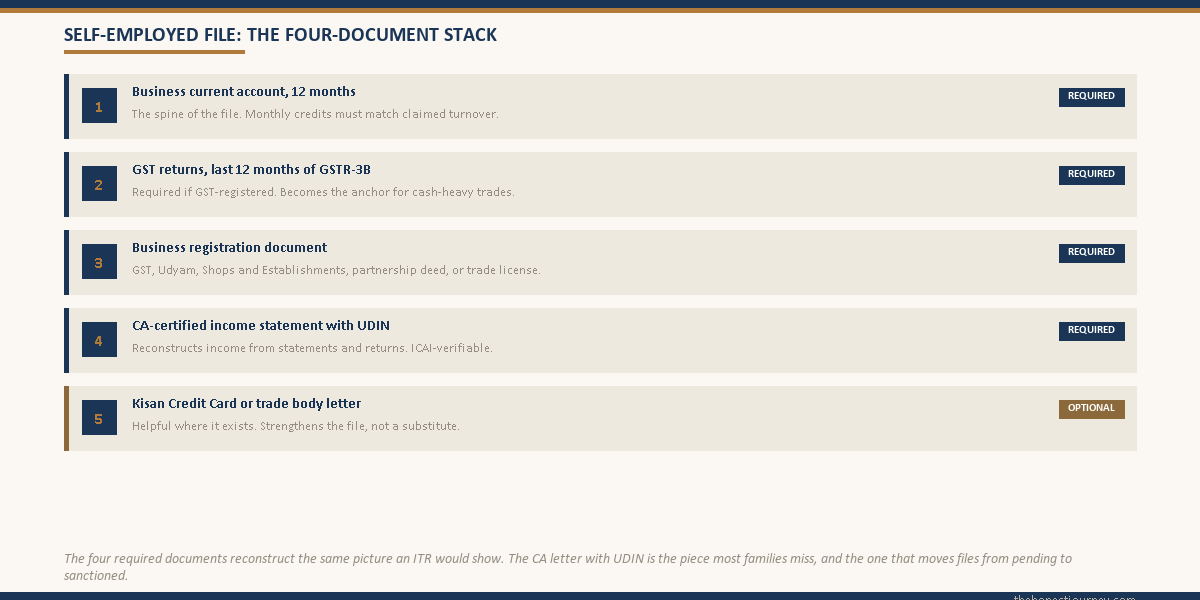

This is the most common case. A shopkeeper, a tailor, a contractor, a freelance professional, a small trader. The business is real, the income is real, but the ITR was either not filed or was filed at a level that does not reflect actual cash flow.

The non-negotiable documents are: twelve months of business current-account statements (the spine of the file, showing consistent monthly credits that match the claimed turnover); twelve months of GST returns if the business is GST-registered (GSTR-3B monthly summaries are usually enough); the business registration document, whichever applies (GST certificate, Udyam, Shops and Establishments license, partnership deed, or state trade license); and, the document most families do not know about, a CA-certified income statement on letterhead, signed with UDIN, reconstructing the income from bank statements and GST returns.

The current account must be in the business name, not a personal savings account. If the business runs through a savings account (common for sole proprietors), the lender will ask you to account for it through the CA letter. Cash-heavy businesses are the hardest case because the bank statement does not reflect the real turnover. There, GST returns become the anchor; without GST returns either, you are looking at NBFCs only.

The Reserve Bank of India’s master directions on retail lending require lenders to consider “alternative income evidence” where available, particularly for MSME borrowers. If a lender refuses your file outright without examining the alternative stack, quote this and ask for a written reason for rejection. Most relationship managers do not want to put a rejection in writing, and the conversation tends to reopen.

Agricultural co-applicant: land records as the income proof

Agricultural income is exempt under Section 10(1), so most farming families have never filed an ITR. Ironically this is one of the cleanest cases to document, because state revenue departments maintain detailed land records the lender can verify.

The core documents are the 7/12 extract (Maharashtra, Gujarat), Patta and Chitta (Tamil Nadu), Khasra Khatauni (north India), or the state’s equivalent land record; crop sale receipts for the last two cycles, ideally APMC market-yard slips (the closest thing to a verifiable cash receipt in agriculture); the Kisan Credit Card statement if one exists, since KCC limits are themselves set on land-holding and crop pattern; and a Tehsildar’s certificate of land holding as the income verification anchor.

Banks attribute income per acre based on crop pattern and the state’s yield tables. Eight acres of irrigated sugarcane will be assessed very differently from eight acres of rain-fed jowar. If the assessed annual income covers the eventual EMI under FOIR (typically 50 to 65 percent), the file moves. If not, the bank may ask you to add a second co-applicant from the extended family.

Faz's ruleFor agricultural co-applicants, the 7/12 extract is the equivalent of three years of ITR.

Lenders are familiar with land-record-based income assessment because they run their priority sector lending on the same formulas. If your file is sitting on the agricultural-officer desk at a PSU bank, it will move faster than you think. The branch is used to this paperwork.

Housewife as co-applicant: when this works and when it does not

Listing a housewife as the sole co-applicant rarely works alone. A co-applicant has to demonstrate independent income capacity to service the EMI if needed, and a housewife with no documented income stream cannot do that, regardless of how stable the household is.

Two configurations do work. One, the housewife has genuine independent income in her own name (rental from a property she owns, FD interest from her own deposits, dividend or mutual fund income). Rental needs the registered rent agreement plus 12 months of rent credits. FD interest needs Form 16A and the FD certificates. This works only if the documented income alone clears FOIR, which usually means rental and FD income above ₹40,000 to 60,000 per month combined. Two, more commonly, the housewife is named as primary co-applicant for procedural reasons and the spouse is added as a secondary co-applicant whose salary slips or ITR carry the FOIR. The case that fails is listing the housewife mother as sole co-applicant because the father’s ITR is missing, with no income document for either parent. That gets rejected at first scrutiny.

Pensioner as co-applicant: the cleanest no-ITR case

If the co-applicant is a retired government employee, retired defence personnel, or a PSU pensioner, the case is almost always approvable, often without an ITR at all. The pension itself is a documented, recurring, government-backed income credit. The lender has very little to verify.

The required documents are the PPO (Pension Payment Order) copy, twelve months of pension account statements showing the monthly credit, Form 16 from the pension disbursing authority, and the bank’s pension credit certificate on its letterhead. Commuted pension or family pension need separate documentation but follow the same logic.

One nuance. Remaining tenure matters. If the co-applicant is 68 and the loan runs 10 years past the moratorium, the bank may insist on a second, younger co-applicant. This is not a no-ITR issue; it is an age-and-tenure issue. The fix is a younger child or sibling added to the application.

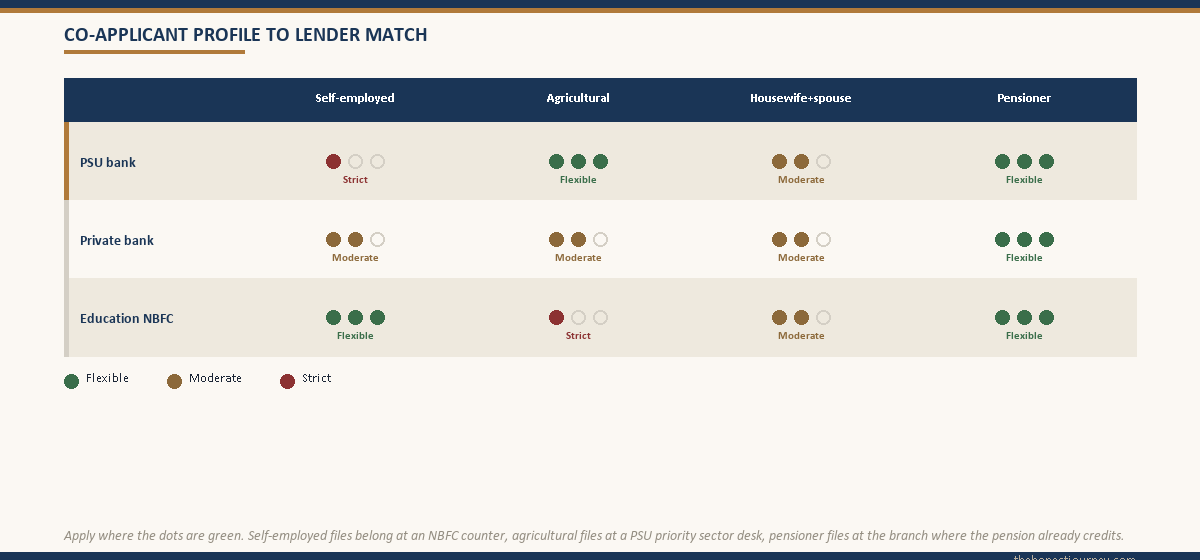

Which lender category accepts which combination

This is the question that determines where you actually apply, and it is the question that almost every other blog skips. Lender flexibility on no-ITR cases is not random. It tracks a fairly predictable hierarchy.

| Lender category | Self-employed (no ITR) | Agricultural | Housewife + spouse | Pensioner |

|---|---|---|---|---|

| PSU banks (SBI, BoB, Canara, PNB) | Strict. Usually need 2 years ITR or strong GST + CA letter | Flexible. Land records well accepted | Workable if spouse has clean ITR | Most flexible. PPO is sufficient |

| Private banks (Axis, HDFC, ICICI, Federal) | Moderate. Accept CA-certified income with bank statements | Moderate. Some branches handle, others refer to agri desk | Workable. FOIR-driven assessment | Flexible |

| Education NBFCs (Avanse, Auxilo, Credila, InCred) | Most flexible. Cash-flow lending models built for this | Less common. Often refer back to PSU banks | Workable with documented secondary income | Flexible |

| International lenders (Prodigy, MPower) | Not relevant. Lend on student profile, not co-applicant ITR | Not relevant | Not relevant | Not relevant |

Two patterns. PSU banks are most flexible on agricultural and pensioner cases (priority sector lending, long history with these profiles) and strictest on self-employed without ITR (credit policies built around filed returns). NBFCs flip this: most flexible on self-employed cash-flow cases (underwriting runs off bank statements and GST data) and least relevant for agricultural cases.

Apply to the lender category that matches your co-applicant profile. A self-employed family without ITR should start with an education NBFC, not a PSU bank. An agricultural family should start with the agricultural desk of a PSU bank in their home district, not an NBFC. A pensioner family has the easiest case; the PSU branch where the pension account already sits is the lowest-friction option. The State Bank of India’s education loan product pages and the Indian Banks’ Association model scheme spell out the documentation lists for each profile.

Faz's ruleMatch the co-applicant profile to the lender category before you fill the first form.

Half the “education loan rejected, no ITR” stories I hear are not rejections. They are mismatches. A self-employed file at a PSU branch and an agricultural file at an NBFC are both going to stall. Move them to the right counter and the same documents become acceptable.

The CA-certified income statement: how it actually works

This document is the single most useful tool a self-employed family has, and almost nobody explains how to get it done correctly. It is a one or two-page document on a Chartered Accountant’s letterhead stating the co-applicant’s gross income, net income, business turnover, and the basis of computation (bank statements, GST returns, books of accounts). The CA signs, stamps, and provides a UDIN generated through the ICAI portal. The UDIN is what makes the certificate verifiable: any lender can check it online.

The certificate should cover the last two financial years and align with the bank statements and GST returns in the same file. If the CA letter shows ₹18 lakh of annual income but the bank credits only ₹9 lakh, the underwriter will flag the file. A CA typically charges ₹3,000 to ₹10,000 for a properly drafted certificate with UDIN. A small price for a document that can unlock a ₹30 lakh sanction.

The honest closing

The absence of ITR is not the real issue in most of these cases. The real issue is that the family does not know the alternative document stack exists, and the relationship manager at the first branch does not walk them through it because the conversation is easier if the file is just refused.

If your co-applicant does not have an ITR, you are not in a worse position than a family with one. You are in a different position. The document collection is heavier, the file takes longer to underwrite, and lender choice matters more (a wrong first application can waste three to four weeks). But the outcome, if you assemble the matrix above and apply to the right counter, is the same sanction letter at the same rate.

A clean documents stack on the student side reduces friction on the co-applicant side, because underwriters look at the file as a whole. For the full list see the education loan documents required post and, if collateral is involved, the education loan without collateral guide. If a file has already been returned, the rejection reasons post covers re-submission. And if you are weighing co-applicant choice itself, the co-applicant guide goes deeper into FOIR.

“No ITR” is a paperwork problem, not a creditworthiness problem. Treat it as paperwork. Solve it document by document.

FAQ

Is ITR mandatory for an education loan in India?

No. ITR is not mandatory if the co-applicant’s income can be documented through alternative means. RBI master directions on retail lending require lenders to consider alternative income evidence, particularly for MSME borrowers, agricultural families, and pensioners. The standard substitutes are GST returns and CA-certified statements for the self-employed, land records and crop receipts for agricultural co-applicants, PPO copies for pensioners, and spouse salary slips when a non-ITR-filing housewife is named.

What proof of income works for a self-employed co-applicant without ITR?

The standard stack is twelve months of business current-account statements, twelve months of GST returns if registered, the business registration document (GST certificate, Udyam, or Shops and Establishments license), and a CA-certified income statement on letterhead with UDIN covering the last two financial years. NBFCs are typically the most flexible category for this profile. PSU banks may still ask for at least one or two years of filed ITR even if the rest of the stack is strong.

Can agricultural income be used as proof for an education loan?

Yes. Agricultural income is tax-exempt under Section 10(1) so most farming families do not file ITR, and lenders are familiar with assessing income through land records. The standard documents are the 7/12 extract or state-equivalent land-holding record, two cycles of crop sale receipts (ideally APMC market-yard slips), the Kisan Credit Card statement if one exists, and a Tehsildar’s land-holding certificate. PSU banks handle these files most comfortably through their priority sector desks.

Can a housewife be the sole co-applicant on an education loan?

Rarely. A co-applicant must demonstrate independent income capacity to clear the FOIR check, which a housewife with no documented income stream usually cannot do alone. Two configurations work. One, the housewife has genuine independent income through rental, FD interest, or dividends that clears FOIR on its own. Two, the housewife is named as primary co-applicant for procedural reasons and the spouse is added as a secondary co-applicant whose salary or ITR carries the file.

Will banks accept a CA-certified income statement instead of ITR?

Most lenders accept a CA-certified income statement as part of a complete stack, not as a standalone replacement for ITR. It should be on the CA’s letterhead, signed and stamped, with a UDIN generated through ICAI, covering the last two financial years. The figures must align with the bank statements and GST returns in the same file. NBFCs accept CA certificates more readily than PSU banks. The certificate typically costs ₹3,000 to ₹10,000.

What documents does a pensioner co-applicant need?

The required documents are the PPO (Pension Payment Order) copy, twelve months of pension account statements showing monthly credits, Form 16 from the pension disbursing authority, and a pension credit certificate from the bank on its letterhead. The main constraint is age and tenure. If the pensioner is older and the loan runs ten or more years, lenders may ask for a younger second co-applicant.

Which lenders are most flexible with no-ITR cases?

Education NBFCs (Avanse, Auxilo, HDFC Credila, InCred) are most flexible for self-employed co-applicants because their underwriting runs off bank statements and GST data directly. PSU banks (SBI, Bank of Baroda, Canara, PNB) are most flexible for agricultural and pensioner cases through their priority sector desks. Private banks sit in the middle. Match the co-applicant profile to the lender category before applying.

What if the co-applicant should have filed ITR but did not?

If income is above the filing threshold and ITR is simply pending, most lenders will ask for the missing returns to be filed before processing, and a CA can usually file the last two years within a few weeks with late fees. If income was historically below the threshold and is only now higher, that is easier to explain. The cleanest path is to discuss the situation with a CA first, regularise the position if needed, and then apply. A patchy filing history that does not match the bank statements is a frequent rejection trigger.

Faz · The Honest Journey · 2026