Working professionals can get an education loan of up to ₹1.5 crore based on their own salary, with rates of 10.5 to 12.5 percent and no co-applicant needed once monthly income crosses roughly ₹1 lakh. The moratorium is usually shorter (course period only, not course plus six months), and most banks ask for an employer NOC. ISB and IIM executive programs qualify with every major lender.

Most education loan content is written for a 22 year old applying for a master’s abroad. If you are 29, three years into a job, and looking at a part time MBA or an executive program at ISB, the standard advice does not quite fit. The income proof is your own. The bank asks for things a fresher would never see, like an employer NOC. And the moratorium math you read about everywhere else may not even apply.

This post covers what is actually different about an education loan for working professionals, from the eligibility checks to the immediate EMI structure to the after tax math at the 30 percent slab. If you are sitting on a sanction call right now, this is the post.

Answer capsule. Yes, a working professional can get an education loan in India for an executive MBA, a part time degree, or a one year residential program. Some banks require an employer NOC, lenders often start EMI from disbursement instead of after a moratorium, and the after tax cost at the 30 percent slab under Section 80E is far lower than the headline rate. Plan around the post tax EMI, not the brochure rate.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

Other eligibility situations worth reading: the education loan rejection reasons india post, the education loan without ITR post, and the education loan with backlogs india post.

What changes when the borrower is the working professional

In a standard education loan, the student is the borrower, a parent is the co applicant, and the moratorium gives the student time to graduate and find a job before EMIs start. The whole product assumes the borrower is currently not earning.

A working professional inverts almost every one of those assumptions. You are the borrower. You already earn. You may not even need a co applicant depending on the loan size. Your employer is in the picture because your job is funding the EMI. The moratorium concept gets diluted or disappears entirely. And the loan documents look more like a personal loan than a classic education loan, even though it qualifies as one for tax purposes.

The four real differences are these. Employer involvement, in the form of an NOC or a leave letter. Repayment structure, where some lenders make you pay EMI from disbursement. Income proof complexity, because the bank underwrites your salary and your liabilities, not your parents’. And the post tax math, where Section 80E lets you deduct the full interest paid from taxable income, which changes the effective cost meaningfully at the 30 percent slab.

Faz's ruleA working professional's education loan is a hybrid product. It looks like an education loan on paper, it underwrites like a personal loan in practice.

The bank is not waiting for you to graduate before charging you. You already earn. So the moratorium logic that protects students gets replaced by an EMI from month one, and the eligibility math runs on your salary slip, not on your father’s ITR.

The employer NOC question

The most common surprise for working professionals is that some banks ask for an employer No Objection Certificate, and some do not.

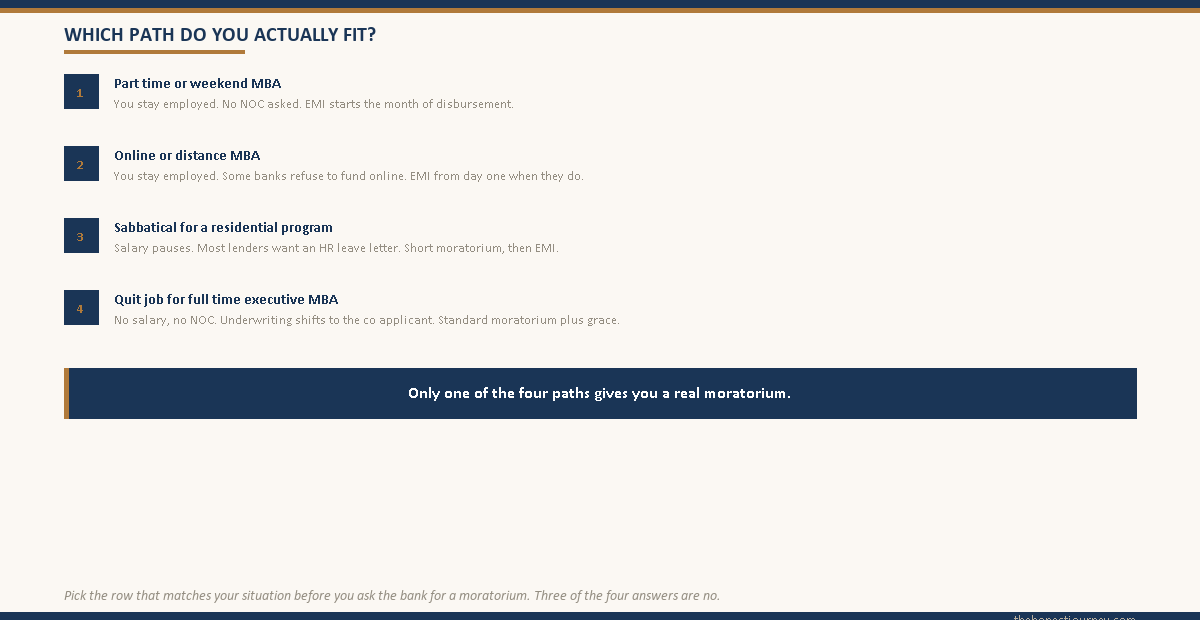

For a part time or weekend MBA where you continue working full time, most banks do not require an NOC. For a residential executive program where you take a sabbatical, several public sector banks and some private banks want a letter from your employer confirming the leave dates and the post sabbatical salary. The substance is the same as an NOC. If you have quit outright, the bank treats you closer to a fresher student and underwriting shifts to your co applicant. The lender specific schemes from ICICI Bank, HDFC Credila, Avanse, and Auxilo are designed for this exact situation and build the post program job assumption into the EMI schedule.

| Program type | Working status during program | NOC or sabbatical letter | Typical EMI structure |

|---|---|---|---|

| Part time or weekend MBA | Continue full time job | Rarely required | EMI from disbursement |

| Online or distance MBA | Continue full time job | Not required at most banks | EMI from disbursement, some banks do not fund this category |

| Sabbatical for 1 year residential | On leave, paid or unpaid | Required by most lenders | Short moratorium (program length) then EMI |

| Quit job for full time executive MBA | Not employed during program | Not applicable, co applicant strength matters more | Standard moratorium plus grace |

If your employer is reluctant, a leave sanction letter from HR usually carries the same weight. A handful of NBFCs do not require an NOC at all and will go on your salary slips and bank statements alone.

The immediate EMI structure most blogs do not mention

In a standard education loan, the moratorium runs through the program plus a 6 to 12 month grace period after graduation. Interest accrues and capitalises, but you pay nothing during that window. For a working professional on a part time or online program, several lenders do not offer that structure. They start the EMI clock from the date of first disbursement, because you already have a salary.

The consequence is twofold. You pay more cash out of pocket during the program. On a ₹15 lakh loan at 11 percent over 7 years, that is roughly ₹25,750 per month from day one. But you avoid the capitalisation trap entirely, and the total interest paid over the life of the loan is significantly lower. This is a better deal for someone who can afford the EMI from current salary. Some banks do offer the choice. If you are on a sabbatical and your income drops to zero, you can request a moratorium tied to the program duration, though the rate may be marginally higher. The education loan moratorium period interest post walks through the full math. RBI master directions require lenders to disclose the moratorium interest treatment clearly at sanction.

Faz's ruleImmediate EMI is not a punishment. It is the cheaper way to pay back the same loan.

The moratorium feels like a benefit because you defer cash outflow, but the interest does not stop accruing. If your salary can absorb the EMI, paying from month one saves you several lakhs in capitalised interest over the loan tenure.

The after tax math at the 30 percent slab

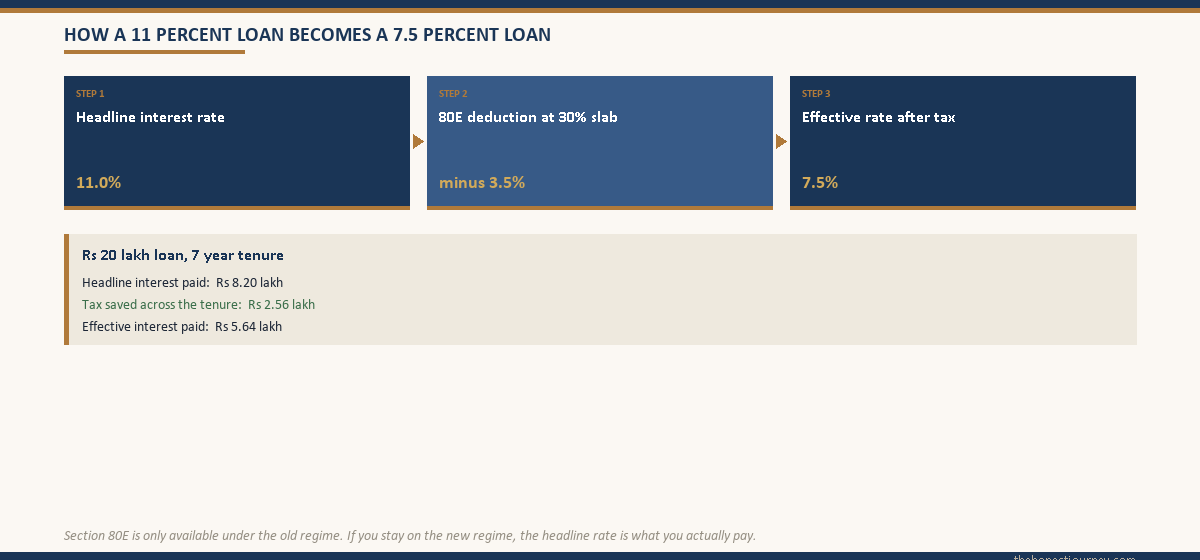

Section 80E lets the borrower deduct the entire interest paid in a financial year from taxable income. There is no upper cap. The deduction is available for 8 years from the year you start repayment, or until the loan is closed, whichever is earlier. This is the single biggest thing that makes a working professional’s education loan cheaper than it looks.

Take a ₹20 lakh loan at 11 percent over 7 years. Total interest is roughly ₹8.2 lakh. At the 30 percent slab plus 4 percent cess, your effective tax rate is 31.2 percent. Across the tenure, the deduction saves you about ₹2.56 lakh in tax. The effective interest paid drops from ₹8.2 lakh to ₹5.64 lakh, and the effective rate on a 11 percent loan, after tax, becomes roughly 7.5 percent.

The catch is that 80E is only available under the old tax regime. On the new regime, you pay the sticker rate. For most working professionals on an education loan, especially those earning above ₹15 lakh, the old regime with 80E works out better for the duration of the loan. The Section 80E education loan tax benefit post covers the full rules. The official source is the Income Tax Department.

The executive MBA edge case

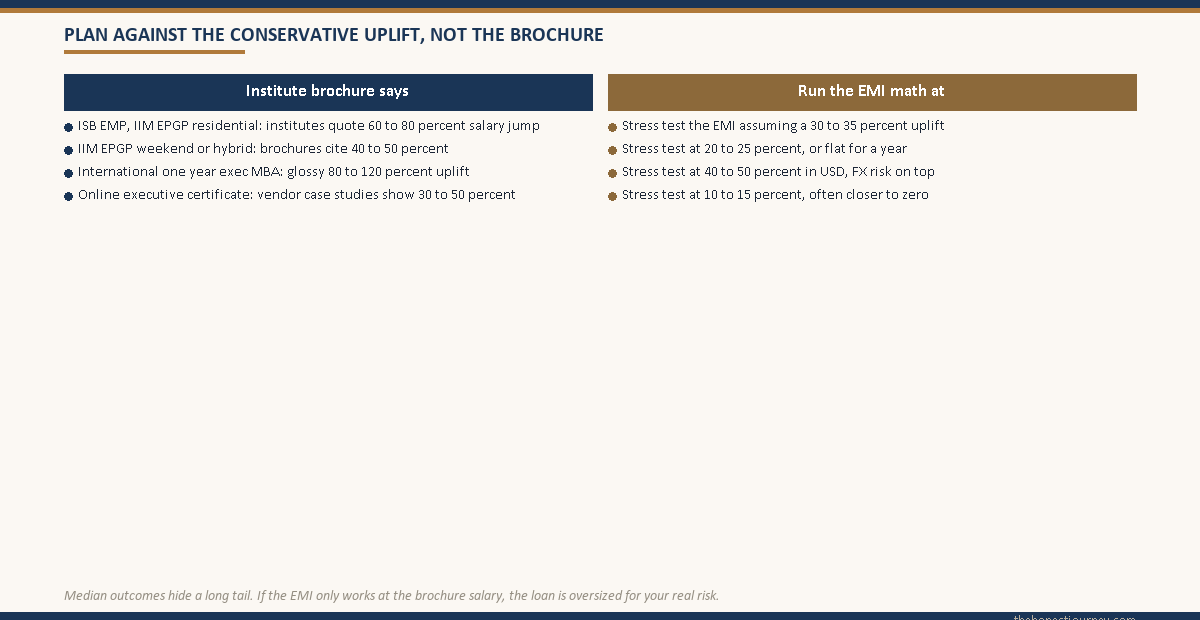

The cleanest example is the executive MBA, where lenders have actually built specific products. ISB EMP, IIM EPGP variants, and international programs like HBS Executive Education or Wharton’s residential exec MBA all sit in a category banks understand. Placement reports are public, salary uplift is concrete, and a bank funding an ISB EMP knows roughly what the median post program compensation looks like.

That is why ICICI Bank and HDFC Credila have named executive MBA schemes with higher loan amounts (up to ₹60 to 80 lakh for premier institutes), lighter documentation, and rates typically 0.5 to 1 percent below the standard education loan rate. For ISB EMP and IIM EPGP, the loan usually funds the full program fee (₹35 to 45 lakh), disbursed in tranches. For international executive MBAs (HBS, INSEAD, IMD, LBS), loan amounts go to ₹80 lakh to ₹1.5 crore, and the lender list narrows to the NBFCs that fund abroad education. Avanse and Auxilo have specific executive program schemes here. ICICI and Credila fund these too but with stricter collateral asks above ₹50 lakh.

| Program category | Typical loan size | Common lender categories | Collateral usually required |

|---|---|---|---|

| ISB EMP, IIM EPGP residential | ₹35 lakh to 45 lakh | Private banks, large NBFCs | Usually unsecured up to ₹40 lakh for premier institutes |

| IIM EPGP weekend or hybrid | ₹20 lakh to 30 lakh | Private banks, public sector banks | Unsecured for most working professionals |

| One year international exec MBA | ₹80 lakh to 1.5 crore | NBFCs (Avanse, Auxilo, Credila), private banks | Required above ₹50 lakh |

| Online executive certificate programs | ₹5 lakh to 15 lakh | NBFCs, fintech lenders | Not required, treated closer to personal loan |

The brochure ROI numbers from institutes are averages. If you are funding an executive MBA on the assumption that your post program salary will jump 60 percent, run the numbers with a 30 percent jump and check whether the EMI still works. The education loan versus self funding post covers this tradeoff.

Eligibility and documents for a working professional

The eligibility check is closer to a personal loan than to a classic education loan. The standard documents: three months of salary slips, six to twelve months of bank statements, two years of Form 16 or ITRs, the offer letter and a current employment letter from HR, PAN, Aadhaar, address proof, the admission letter with fee breakdown, and a statement of any existing loans. For sabbatical based programs, add the HR sabbatical letter. For loans above ₹20 to 25 lakh, the bank may ask for collateral, typically property papers or a fixed deposit lien.

The FOIR check is where most working professional loans get downsized. FOIR is the ratio of your total EMIs (including the new education loan EMI) to your monthly take home. Banks cap this at 50 to 55 percent. If you already have a home loan at ₹35,000 and a car loan at ₹12,000, with monthly take home of ₹1.4 lakh, your existing FOIR is 33 percent. A new EMI of ₹25,000 takes you to 51 percent. The education loan for MBA post covers documentation in detail, and the IBA model scheme outlines the standard baseline.

Faz's ruleThe FOIR check is where most working professional loans get downsized or rejected. Clean up other EMIs before you apply if you can.

Banks add the new education loan EMI to your existing obligations and check the ratio against your take home. If you are already running a home loan and a car loan, the room for a fresh ₹25,000 to 40,000 EMI is narrower than you think. Close a small loan or two before applying.

Top up loans and online program funding

If you already have an education loan from your undergrad and are now funding an executive program, you may be eligible for a top up rather than a fresh loan. The lender adds the new amount to the existing facility, often at a slightly better rate. The education loan top up post covers when this is the right path. It makes sense when you are with the same lender, your repayment record is clean, and the new program is recognised.

Online and distance MBAs are more complicated. Several public sector banks, including SBI (see the SBI education loans page), do not fund online programs unless from a UGC recognised university. Private banks and NBFCs are more flexible, especially for online programs from IIMs, ISB, Wharton Online, or MIT Sloan. Get written confirmation from the lender that the specific program is on their approved list before applying.

The honest take on funding versus self paying

A working professional taking an education loan is not always making the right financial choice, even when the math works on paper. If the qualification you are funding is a professional certification rather than a degree, such as the CA route many finance professionals pursue alongside work, the lender appetite is narrower and the loan sizing is different, which the education loan for CA students post breaks down. The 80E deduction is real money, but it requires you to stay in the workforce and at the 30 percent slab to capture it. If your post program plan involves a sabbatical, a startup, or a lower salary international role, the deduction utility shrinks.

A partial loan often makes more sense than a full loan or full self funding. Pay 40 to 50 percent from savings, borrow the rest, use 80E on the borrowed portion, keep enough liquidity for the program year, and avoid pushing your FOIR to the ceiling. This is rarely what the relationship manager will suggest, because their incentive is to sanction the maximum.

The number that matters is the same as for any education loan. Your post program monthly EMI as a percentage of your conservative post program take home. If that ratio is above 35 to 40 percent, the loan is oversized, regardless of how good the 80E math looks.

FAQ

Can a working professional get an education loan in India?

Yes. Most public sector banks, private banks, and NBFCs fund education loans for working professionals, including executive MBAs, part time programs, online degrees, and one year residential courses. The underwriting runs on your salary slips, bank statements, and ITRs rather than on a co applicant’s income. The loan amount and EMI structure depend on the lender, the program, and whether you continue working or take a sabbatical.

Is an executive MBA loan different from a standard education loan?

Structurally, yes. ICICI Bank, HDFC Credila, Avanse, and Auxilo have specific schemes for executive MBA programs at ISB, IIM, and international institutes. These schemes typically offer higher loan amounts (up to ₹60 to 80 lakh for premier residential exec programs), often without collateral up to a defined limit, with rates 0.5 to 1 percent below standard education loans, and the choice of immediate EMI or a short moratorium. Documentation is also lighter because the program is recognised.

Does my employer need to give an NOC for an education loan?

It depends on the bank and the program. For part time or weekend programs where you continue working full time, most lenders do not ask for an NOC. For residential programs requiring a sabbatical, several banks ask for a leave sanction letter from HR confirming the dates and return role. If you have quit your job, the requirement no longer applies and the bank assesses your file on the co applicant. NBFCs tend to be more flexible on this than public sector banks.

Is there a moratorium period for working professional education loans?

Sometimes, not always. Many lenders start the EMI from the date of first disbursement for working professionals on part time or online programs, because you already have a salary to service the EMI. For residential programs where you are on a sabbatical and your income drops, some banks offer a moratorium aligned with the program duration. The immediate EMI structure is actually cheaper overall because it avoids the interest capitalisation that happens during a moratorium.

Can I claim Section 80E on an executive MBA loan?

Yes. Section 80E applies to any education loan from a recognised institute, including executive MBAs and one year programs. You can deduct the entire interest paid in a financial year from your taxable income, with no upper cap. The deduction is available for 8 years from the year you start repayment, and only under the old tax regime. At the 30 percent slab, the effective interest cost on a 11 percent loan drops to roughly 7.5 percent.

Do banks fund online or distance MBA programs?

Some do, some do not. Several public sector banks, including SBI, restrict funding to UGC recognised programs. Private banks and NBFCs are more flexible, especially for online programs from IIMs, ISB, Wharton, and MIT Sloan. Before assuming a program is fundable, get written confirmation from the lender that the specific program is on their approved list. If the lender will not fund it, a personal loan loses the Section 80E benefit.

How much can a working professional borrow for an education loan?

For domestic executive programs at ISB or IIM, unsecured loans go up to ₹40 to 45 lakh at most private banks and NBFCs, with higher amounts against collateral. For international one year executive MBAs, loan sizes go up to ₹1 to 1.5 crore, with collateral typically required above ₹50 lakh. The actual amount sanctioned depends on your salary, your FOIR after the new EMI, your credit score, and the institute. Banks usually fund the full fee plus a small living expense component for residential programs.

Will the loan affect my credit score during the program?

If you start EMI from disbursement, the loan appears on your CIBIL report from month one and you build a positive repayment track record as long as you pay on time. If you are on a moratorium structure, the loan still appears on the report as a sanctioned facility, but no EMI activity is reported until repayment begins. Missed EMIs at any point hit your CIBIL hard. The bigger ongoing risk is the FOIR limit on any future home loan or car loan during the education loan tenure.

Faz · The Honest Journey · 2026