Most public sector banks decline an education loan for a distance MBA or online MBA, because their IBA model scheme still treats only regular full-time campus programs as eligible. The realistic funding paths are NBFCs like Avanse, Credila and Auxilo for UGC-DEB approved online MBAs (typical sanction ₹2 lakh to ₹20 lakh at 12 to 15 percent), a few private banks for executive online MBAs from IIMs or top-tier institutes, and personal loans only as a last resort. Section 80E still applies if the course qualifies under the Income Tax Act definition of higher education.

I get this question almost every week. Someone has decided to do an online MBA from NMIMS, Symbiosis, Amity, or one of the IIM executive online programs, they have walked into their salary account branch expecting a routine sanction, and they have walked back out with a polite no. Then they ask me whether private banks or NBFCs will fund it, and whether the rate will be brutal.

This post is the honest version of that conversation. What actually gets funded, what does not, where the gatekeeper sits, and whether the loan is worth taking at the rates on offer for a part-time qualification you will study in your free time.

Other eligibility situations worth reading: the education loan rejection reasons india post, the education loan without ITR post, and the education loan with backlogs india post.

Why public sector banks usually decline an education loan for distance MBA

The Indian Banks’ Association model education loan scheme, which most public sector banks (SBI, PNB, Bank of Baroda, Canara, Union Bank) still anchor their education loan policies to, was written around regular full-time programs that require physical attendance. The eligible course list in the scheme covers degree, diploma and PG courses approved by UGC, AICTE, government and recognised regulatory bodies, with a strong bias toward full-time programs offered on campus.

Distance learning and online MBA programs sit awkwardly inside that framework. Even when the program is from a reputed institute and is duly approved by the UGC Distance Education Bureau (UGC-DEB) and AICTE, the branch officer running the file often defaults to a no, because their internal credit policy treats part-time and distance courses as ineligible by default. Some banks will fund SBI’s own list of specific full-time online programs from IIMs, but a general online MBA from a private deemed-to-be-university almost always gets refused at the public sector counter. You can read the IBA model scheme positioning on the Indian Banks’ Association site to see how the eligibility frame is structured.

There is also a quieter reason. The IBA model scheme caps interest rate for loans up to ₹7.5 lakh at fairly thin spreads over the bank’s marginal cost of funds. For a part-time student who is already employed, the bank’s risk-adjusted return on a small distance MBA loan does not look attractive next to a regular full-time loan with a parent co-applicant and a clear repayment runway. The product simply is not built for this customer.

Faz's ruleDo not waste a week chasing PSU branches. If your program is online or distance, start with NBFCs and private banks built for working professionals.

Every public sector branch I have heard from has either flatly refused or asked for so much paperwork (employer NOC, full collateral, parent co-applicant despite the student being 32) that the loan becomes unviable. Calling five PSU branches to get five different versions of no is not research. It is delay.

UGC-DEB approval is the actual gatekeeper

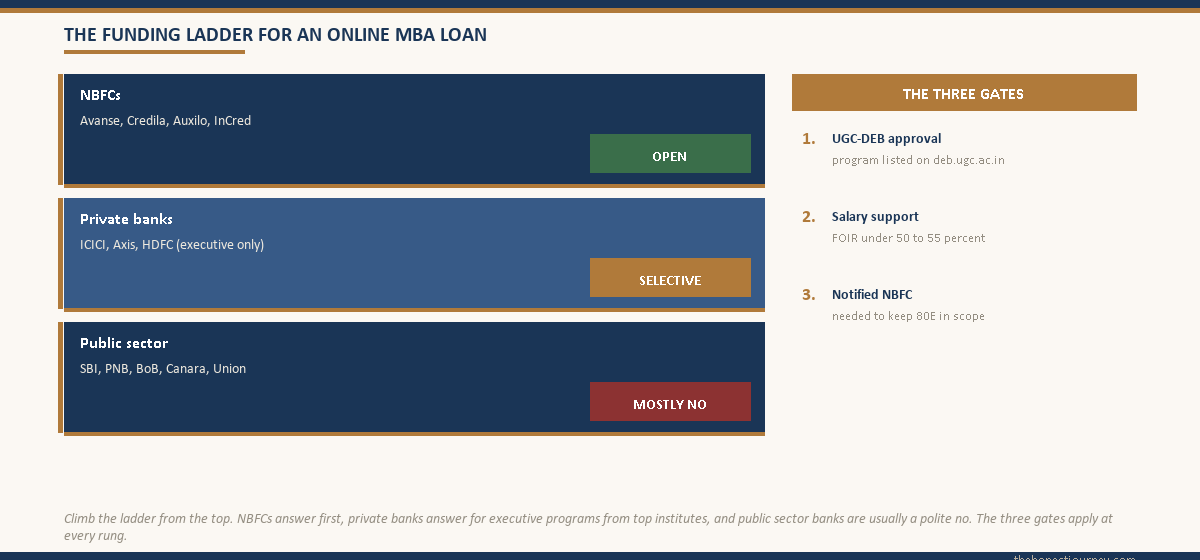

The single most important question for anyone considering an education loan for a distance MBA is whether the program is approved by the UGC Distance Education Bureau. This is the body that recognises Open and Distance Learning (ODL) and Online programs in India. The official list of recognised higher educational institutions and approved programs is published on the UGC Distance Education Bureau portal, with the broader regulatory framework available on the UGC main site.

If your program is not UGC-DEB approved, two things follow. First, almost no formal lender will treat it as an eligible higher education course, regardless of how heavily it is marketed. Second, you may have trouble claiming Section 80E tax deduction on the interest, because the Income Tax department’s definition of higher education leans on courses pursued from a recognised institution.

Before you apply for the loan or pay any fee, do this one check. Go to deb.ugc.ac.in, find the institution’s name in the recognised list for the relevant academic year, and confirm the specific program (Online MBA or ODL MBA, as applicable) is listed against that institution. Save a screenshot. NBFC loan officers will sometimes ask for evidence, and you will need it again at tax time.

Which NBFCs and banks actually fund a distance or online MBA

The funding pool is narrower than for a regular MBA, but it exists. Here is the realistic landscape in 2025-26 for someone applying for an online or distance MBA loan in India.

| Lender type | Likelihood for online or distance MBA | Typical loan size | Typical interest rate |

|---|---|---|---|

| Public sector banks (SBI, PNB, BoB, Canara) | Mostly no, very rare yes for select IIM online programs | ₹2L to ₹7.5L if approved | 9 to 11 percent |

| Private banks (ICICI, Axis, HDFC) | Selective, mostly executive online MBAs from top institutes | ₹2L to ₹20L | 11 to 14 percent |

| NBFCs (Avanse, Credila, Auxilo, InCred) | Yes, for UGC-DEB approved online MBAs | ₹2L to ₹25L | 12 to 15 percent |

| Fintech and small NBFCs | Yes, but often as a working professional loan dressed as education loan | ₹1L to ₹10L | 13 to 18 percent |

Two patterns are worth calling out. NBFCs in this space (Avanse, Credila, Auxilo, InCred and a couple of others) have a dedicated product for working professionals pursuing an online or executive program, and they will assess your case on your salary income rather than treating you as a dependent student with a parent co-applicant. The trade-off is the rate. You will pay 12 to 15 percent, which is materially higher than the 9 to 11 percent a regular MBA loan from a public sector bank attracts.

A few private banks will fund executive online MBA programs from IIMs (the IIMK, IIMI, IIMR online programs, for example), and from top-ranked deemed universities. The pricing is closer to 11 to 13 percent and the experience is closer to a regular salaried personal loan with a tax-efficient wrapper. Worth checking with your existing salary account bank before going to an NBFC.

Faz's ruleIf a lender offers you 17 percent plus and calls it an education loan, it is a personal loan in disguise. Walk.

A real education loan even from an NBFC for an online MBA tops out around 14 to 15 percent. Above that, you are looking at a salaried personal loan with the word ‘education’ on the cover. The rate, the tenure, and often the 80E eligibility are worse than what you can get on a true education product.

Section 80E and the distance MBA loan

This is where the tax angle saves a meaningful amount of money over the loan tenure, if your course qualifies. Section 80E of the Income Tax Act allows you to deduct the entire interest paid on a loan taken for higher education, with no upper limit, for up to 8 assessment years from the year you start repaying.

The key conditions under Section 80E, summarised from the Income Tax Department source rules, are these. The loan must be from a financial institution (scheduled bank or notified NBFC) or an approved charitable institution. The loan must be for higher education, defined as any course of study pursued after passing the senior secondary examination from a recognised institution. The deduction is available to the individual who took the loan, paid the interest, and is being assessed.

A distance or online MBA from a UGC-DEB recognised institution qualifies on the higher education test. The loan being from an NBFC is fine, provided the NBFC is notified for this purpose (Avanse, Credila and Auxilo are well-established players here). The interest you pay annually becomes a straight deduction from your taxable income. At a 30 percent marginal tax slab, ₹1 lakh of annual interest paid saves you roughly ₹31,200 in tax (including cess). Over the typical 5 to 7 year tenure of a working-professional education loan, this can recover ₹3 to ₹6 lakh of effective cost.

Two caveats. If the institution is not UGC-DEB recognised, the deduction is at risk and could be denied on assessment. If you are on the new tax regime under Section 115BAC, the 80E deduction is not available (the new regime gives up most deductions in return for lower slabs). For the comparison between the two regimes and whether 80E justifies staying on the old regime, see the broader breakdown in the Section 80E education loan tax benefit post.

How a distance MBA loan compares to a personal loan or self-funding

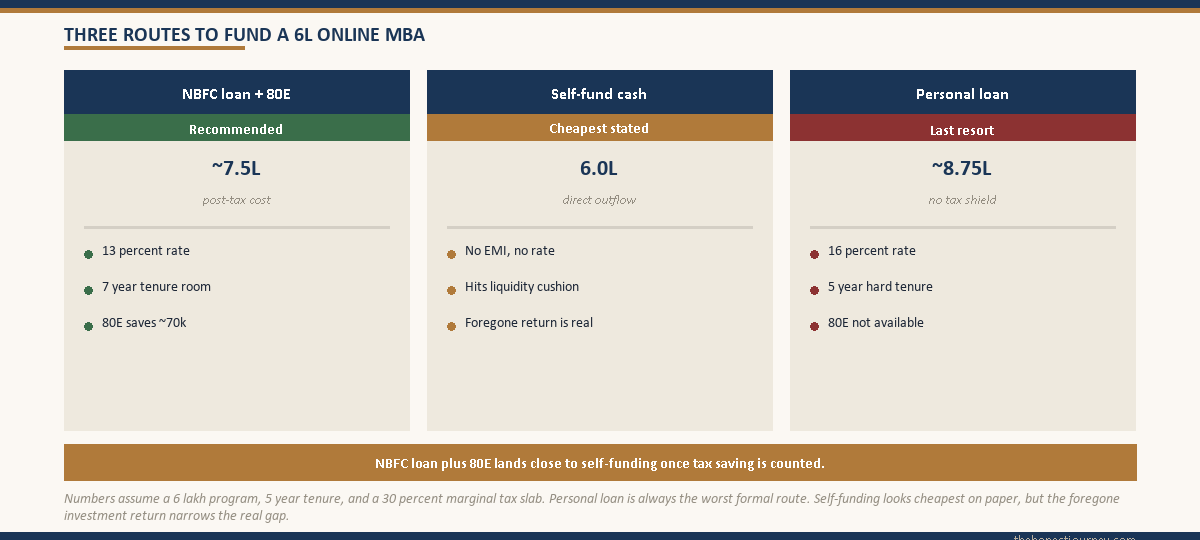

Most working professionals pursuing an online MBA can technically self-fund the program if they stretch. A typical online MBA from a recognised institution costs ₹2.5 lakh to ₹10 lakh in total tuition spread over 2 years, which is much smaller than a regular MBA or an abroad master’s. So the relevant comparison is not “education loan or no loan” but rather “education loan, personal loan, or self-fund out of cash flow and savings.”

Let us run a simple example. ₹6 lakh program cost, 5-year tenure, comparing the three routes.

| Funding route | Effective rate | Approx EMI | 80E available | Total cost over tenure |

|---|---|---|---|---|

| NBFC education loan | 13 percent | ₹13,650 | Yes | ₹8.19L (gross), ~₹7.5L after 80E at 30 percent slab |

| Salaried personal loan | 16 percent | ₹14,590 | No | ₹8.75L |

| Self-fund from salary and savings | 0 percent stated, opportunity cost real | N/A | N/A | ₹6L direct, plus foregone return on the ₹6L you would otherwise have kept invested |

For the majority of working professionals, the choice is between an NBFC education loan with 80E and self-funding. The NBFC loan is almost always cheaper than a personal loan, and once you factor in 80E, the gap to self-funding narrows considerably. A personal loan should be the last option, because you give up 80E, you pay a higher rate, and the tenure is usually shorter (5 years versus 7 on an education loan), which spikes the EMI.

For more on this comparison in the general education loan context, the education loan versus personal loan post runs the full math for larger loan sizes.

What the lender will actually ask you for

The documentation list for a distance or online MBA loan is closer to a salaried personal loan than to a regular education loan. Expect to be asked for the following.

Identity and address: PAN, Aadhaar, passport if you have one. Income: latest 3 to 6 months salary slips, 6 to 12 months bank statements of the salary account, latest Form 16 or ITR for 2 financial years. Employment: offer letter from current employer, employment ID, sometimes an employer NOC (rare for online programs, common for executive MBAs). Course: admission letter from the institution, fee structure document, UGC-DEB approval screenshot if the loan officer is unfamiliar with the program. Co-applicant: not always mandatory if your salary supports the EMI, but often requested as a parent or spouse to strengthen the file.

One specific point worth flagging. NBFCs often disburse the loan in tranches aligned to the institution’s fee schedule (per semester or per term), not as a lump sum. This matches the cash flow of the program and reduces the principal on which interest accrues in the early months. Ask for the disbursement plan in writing at sanction and confirm it matches your institution’s payment calendar.

Faz's ruleThe single document that decides your file is your last 6 months of salary slips. Treat them as the loan application.

Loan officers at NBFCs in this space approve or decline based on your in-hand salary and FOIR (the share of your monthly income already going to existing EMIs). If your in-hand cleanly supports the proposed EMI at a 50 to 55 percent FOIR ceiling, you will get the loan. If it does not, no amount of co-applicants or supporting documents will rescue it.

When the loan is worth it and when it is not

The honest test is whether the online MBA changes your earnings trajectory enough to justify the post-tax cost of the loan. For a ₹6 lakh NBFC loan at 13 percent over 5 years, the post-80E cost is roughly ₹7.5 lakh. If the qualification realistically opens a salary jump of ₹15,000 to ₹25,000 per month inside 2 years (or a role you could not otherwise access), the math is fine. If it is mostly a credential for personal satisfaction with no clear earnings impact, then taking on ₹7.5 lakh of post-tax cost to study in your evenings is a heavier commitment than it looks.

Two situations where I think the loan is genuinely worth it. Mid-career professionals (5 to 12 years experience) where lack of an MBA is a visible ceiling for promotions or role changes, and the online format lets them keep earning. Career changers using a UGC-DEB approved program from a known institute as the credential to pivot from one function to another (engineering to product, for example).

Two situations where it is worth a second think. Early career (under 3 years experience) where a full-time regular MBA at a top school is realistically still on the table, since the career impact and lender support are both materially better. And programs from institutions that are not UGC-DEB approved, where you may end up with a degree the market does not value and a loan you cannot get 80E benefit on.

For the broader question of education loans as a working professional, including executive MBA at IIMs and ISB, the education loan for working professionals post covers the salaried-borrower angle in depth, and the education loan for MBA post covers the full-time MBA route. If you are funding a specialised vocational course rather than a management degree, the education loan for pilot training post shows how lenders treat a high-cost skill program that sits outside the standard campus-degree mould.

The honest closing take

A distance or online MBA can be funded. The market for it is narrower than for a regular MBA, the rates are higher, and the gatekeeper is UGC-DEB approval rather than the bank you have always banked with. If your program is recognised and your salary supports the EMI at a sane FOIR, an NBFC education loan with 80E is almost always the right product, and almost always cheaper than the salaried personal loan that your bank’s mobile app will try to push at you.

The mistake I see most often is people spending 3 to 4 weeks chasing public sector branches that were never going to fund the program, and then giving up and taking a 17 percent personal loan because the term has already started. Skip that detour. Verify UGC-DEB approval, run the EMI through the FOIR check on your salary, get two NBFC quotes, and decide.

FAQ

Can I get an education loan for a distance MBA in India?

Yes, but mostly from NBFCs and a few private banks, not from public sector banks. The IBA model scheme that public sector banks anchor their education loan policies on does not cleanly cover distance or online programs, so most PSU branches will decline. NBFCs like Avanse, Credila and Auxilo have dedicated products for working professionals pursuing UGC-DEB approved online MBAs, with sanctions typically between ₹2 lakh and ₹20 lakh at 12 to 15 percent interest. The starting requirement is that your program is UGC-DEB recognised.

Which banks fund online MBA programs?

Private banks (ICICI, Axis, HDFC) selectively fund executive online MBAs from IIMs and top-tier deemed universities, typically at 11 to 14 percent. NBFCs (Avanse, Credila, Auxilo, InCred) are the most reliable source for general UGC-DEB approved online MBAs. SBI and a few other public sector banks have specific lists for select IIM online programs but decline most others. Your starting point should be your existing salary account bank first, then NBFCs, then specialised fintech players if both decline.

Is UGC-DEB approval mandatory for an education loan on a distance MBA?

For all practical purposes, yes. Without UGC Distance Education Bureau approval, mainstream lenders will not classify the program as eligible higher education, and you will struggle to claim Section 80E tax benefit on the interest. Before you apply for the loan or pay any fees, verify the institution and the specific program on the official UGC-DEB portal at deb.ugc.ac.in. Take a screenshot for your file. Loan officers at NBFCs sometimes ask for evidence, and you will want it again at tax filing time.

Can I claim Section 80E tax benefit on a distance MBA loan?

Yes, if the program qualifies as higher education under the Income Tax Act and the loan is from a scheduled bank or notified NBFC. Section 80E allows deduction of the full interest paid (no upper limit) for up to 8 assessment years from the year repayment starts. A distance or online MBA from a UGC-DEB recognised institution funded by Avanse, Credila, Auxilo or similar notified NBFCs typically qualifies. The deduction is available only under the old tax regime, not the new regime under Section 115BAC, so factor that in when choosing your tax regime.

Are NBFCs better than banks for an online MBA loan?

For most online MBA applicants, NBFCs are the realistic option rather than the better option. Public sector banks usually decline. Private banks fund selectively, mostly for executive online MBAs from top institutes. NBFCs are open to UGC-DEB approved programs across a wider set of institutions, assess your file on salary rather than student-with-parent-co-applicant logic, and tend to be faster. The trade-off is a higher interest rate (12 to 15 percent versus 9 to 11 percent on public sector loans for full-time programs). If a private bank approves you at 11 to 13 percent, take that. Otherwise NBFC is the path.

What is the maximum loan I can get for a distance or online MBA?

Typically up to ₹20 lakh from NBFCs and select private banks, and up to ₹25 lakh in some cases for executive online MBAs from premier institutes. The actual sanction depends on the program fee, your in-hand salary and FOIR, your credit score, and the institution’s standing. For a working professional with a stable salary, expect a sanction in the range of 60 to 80 percent of your annual in-hand income for unsecured loans, scaling up if you offer collateral. Online MBA programs themselves usually cost ₹2.5 lakh to ₹10 lakh total, so most applicants do not need the full ceiling.

Do I need a co-applicant for a distance MBA loan if I am salaried?

Often yes, but the requirement is softer than for regular full-time education loans. NBFCs assess your file primarily on your own salary income, so if your in-hand comfortably supports the proposed EMI at a 50 to 55 percent FOIR, you may get sanctioned without a strict co-applicant. Most lenders still prefer a parent or spouse as co-applicant to strengthen the file, especially for loan sizes above ₹10 lakh. If you are 35 or older with a long salary record, the chances of an individual sanction improve. Ask the lender upfront whether co-applicant is mandatory or recommended.

Is a personal loan a reasonable alternative to an education loan for an online MBA?

Only as a last resort. A salaried personal loan at 14 to 18 percent over 5 years will cost meaningfully more than an NBFC education loan at 12 to 15 percent over 5 to 7 years, especially after factoring in Section 80E tax savings on the education loan interest. The personal loan also gives up 80E entirely and usually has a shorter tenure, which raises the EMI. The one situation where a personal loan makes sense is if your program is not UGC-DEB approved and no lender will treat it as an education loan, in which case you need to seriously reconsider whether the program is worth funding at all.

Faz · The Honest Journey · 2026