Education loan insurance is a single premium credit life policy that repays your loan if you die or become permanently disabled, and it usually costs 1 to 3 percent of the sanctioned amount added to your EMI. For a ₹40 lakh loan that is roughly ₹40,000 to ₹1.2 lakh in extra interest over the tenure. It is optional under RBI rules, even when the bank presents it as mandatory.

You sat through the sanction call thinking the hard part was over. The loan was approved, the rate was locked, and then the relationship manager added one more line near the end: a “policy” that protects the loan, costs almost nothing per month, and is “standard for all our students.” It did not sound like a choice. It sounded like a formality. So you said yes, and a number you never quite registered got folded into your loan.

That number was education loan insurance. This post explains exactly what it is, what it costs you over the full tenure, when it genuinely earns its place, and when it is just a quiet markup on a loan you were going to repay anyway.

Education loan insurance is not mandatory under RBI rules. It is a credit life cover that pays off your outstanding loan balance if the borrower or co-applicant dies or becomes permanently disabled. It typically costs 1% to 2% of the sanctioned amount, and on collateral-free loans from private NBFCs it is often made a de facto condition of approval. Worth it for large unsecured loans funded by a single-earner co-applicant. Weak value for small secured loans.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The loan basics nearby: the what education loan covers post, the education loan EMI calculator math post, and the RBI guidelines education loan post.

What education loan insurance actually is

Strip away the brochure language and education loan insurance is a credit life insurance policy. It is a term-style cover whose sum assured is tied to your loan. If the insured person dies during the policy term, the insurer pays the outstanding loan balance directly to the lender. The family does not inherit the debt. The loan closes.

The “insured person” is usually the borrower (the student) or the co-applicant (most often a parent), and sometimes both under a joint structure. This matters more than it looks. On a study-abroad loan, the student rarely has the income that carries the file. The co-applicant does. So the person whose death would actually leave the loan unpayable is the parent, and that is the life the cover should be sitting on.

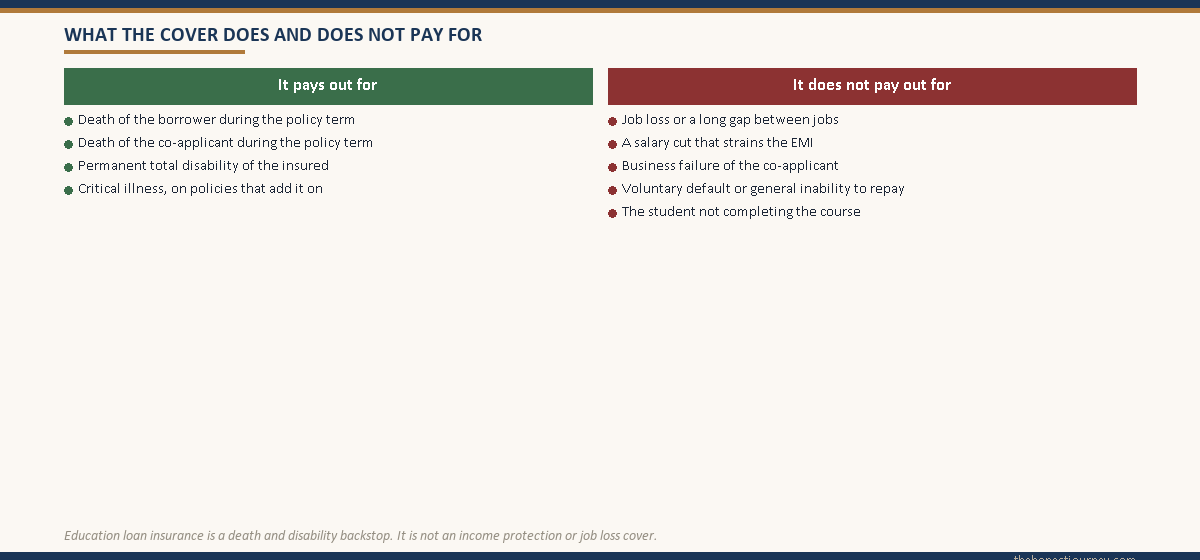

What it commonly covers:

- Death of the insured during the policy term. The outstanding balance is cleared.

- Permanent total disability, where an accident or illness permanently ends the insured person’s ability to earn. Most policies treat this on par with death and clear the balance.

- Critical illness, on some policies only. A defined list of conditions (certain cancers, major organ failure, stroke) triggers a payout. This is an add-on, not a default, and the definitions are narrow.

What it does not do: it is not a job-loss cover, it is not an EMI-holiday cover, and it does not protect you if you simply struggle to repay. It is a death-and-disability backstop. Nothing more. If a salesperson implies it covers “any situation where you cannot pay,” that is not what the policy document says, and the policy document is what pays claims.

Is education loan insurance mandatory? The honest answer

No regulation in India makes education loan insurance compulsory. The RBI’s framework for education loans, built on the Indian Banks’ Association Model Education Loan Scheme, does not require a borrower to buy a life cover as a condition of the loan. You can read the broad lending norms on the RBI site and the model scheme on the IBA site. Neither mandates insurance.

So why does it feel mandatory? Because the practice and the rule have drifted apart. Public sector banks, when they take collateral, generally do not push insurance hard. They already hold security against the loan, and a scheme like the one on the State Bank of India education loans page treats insurance as optional rather than built in. Private NBFCs that fund collateral-free abroad loans carry the full credit risk themselves, so many of them bundle a credit life policy into the sanction and present it as part of the package. Technically you can decline. Practically, on an unsecured loan where the lender has discretion over your file, declining can slow or sour an approval that is otherwise ready to go.

This is the honest grey zone. It is not illegal for a lender to offer insurance, and it is not illegal for them to prefer insured borrowers. What is not allowed is telling you it is an RBI requirement when it is not, or refusing to put the loan and the insurance on separate, clearly priced lines. The insurance regulator, the IRDAI, requires that insurance be sold transparently and not misrepresented. If a lender will not show you the premium as its own number, that is your signal to push back.

Faz's ruleInsurance is never an RBI requirement. If anyone tells you it is, they are either misinformed or selling.

A lender can prefer to insure your loan. That is their commercial choice. What they cannot do is dress a sales decision up as a regulation. Ask the simple question: is this required by RBI, or is it your bank’s policy? Watch how they answer.

What it actually costs (and the part nobody explains)

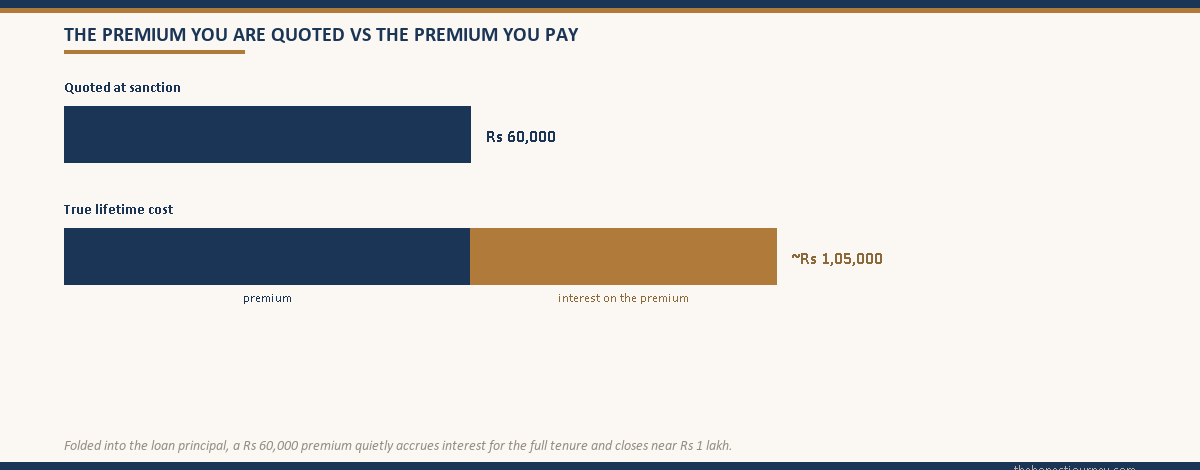

The headline cost of education loan insurance is a single premium of roughly 1% to 2% of the sanctioned loan amount. On the surface that sounds small. The detail that changes everything is how you pay it.

You almost never pay the premium out of pocket. It is funded by the loan itself. The lender adds the premium to your sanctioned principal and disburses it to the insurer on your behalf. So a premium is not a one-time fee you settle and forget. It becomes part of the borrowed amount, and you pay interest on it for the entire tenure of the loan, exactly as you do on your tuition.

Here is what that does on a real abroad-loan scenario. Take a ₹40 lakh collateral-free loan at 11.5% with a 1.5% insurance premium.

| Line item | Amount |

|---|---|

| Sanctioned loan | ₹40,00,000 |

| Insurance premium at 1.5% | ₹60,000 |

| Premium folded into principal | New principal ₹40,60,000 |

| Interest paid on the ₹60,000 premium over a 10-year tenure (approx) | ₹42,000 to 50,000 |

| True lifetime cost of the cover (premium plus interest on premium) | Roughly ₹1,02,000 to 1,10,000 |

Read that last row slowly. The brochure number is ₹60,000. The real number, by the time the loan closes, is closer to ₹1 lakh, because the premium sat inside your principal accruing interest the whole way. That is not a scam. It is just compounding doing its job on a line item the salesperson described as “almost nothing per month.”

The premium itself varies with the sum assured, the tenure, the age and health of the insured person, and whether critical illness is bundled in. A 52-year-old co-applicant attracts a higher premium than a 44-year-old. A 10-year tenure costs more to cover than a 7-year one. None of this is hidden, but you have to ask for the breakup to see it.

When the cover is genuinely worth it

Insurance earns its place when the loss it protects against would actually be catastrophic. For an education loan, that test is simple: if the income-earning co-applicant died tomorrow, could the family still service this loan?

Run through it honestly with your own family. The cover is worth buying when most of these are true:

- The loan is large. A ₹35 lakh to 75 lakh abroad loan is a debt that can crush a household. A ₹6 lakh domestic loan usually is not.

- The loan is unsecured. With no collateral, the lender will pursue the co-applicant’s other assets and income. The family is fully exposed.

- The co-applicant is the sole or primary earner. If that one income disappears, repayment disappears with it.

- The co-applicant has no separate term life cover. This is the one most people miss. If your parent already holds a ₹1 crore term plan, that plan can absorb the loan. A second loan-linked cover is then duplicate spending.

- The student’s post-study earning is uncertain. If the student cannot realistically take over the EMI for some years, the co-applicant’s life is the only thing holding the loan up.

The clearest “buy it” case is the typical study-abroad file: a ₹45 lakh collateral-free loan, a single-earner father in his early fifties as co-applicant, no existing term plan, and a student heading into a job market that may take a year to convert. If that father dies during the moratorium, the family inherits a ₹50 lakh-plus debt with no income to service it and no collateral the bank can quietly seize instead of chasing them. ₹1 lakh of lifetime cost to remove that risk is, in that situation, money well spent.

Faz's ruleThe cover protects the co-applicant's life, so it is the co-applicant's existing insurance you must check first.

A 26-year-old I spoke with had bought loan insurance on a ₹38 lakh abroad loan. Good call, except her father, the co-applicant, already held a ₹1.5 crore term plan. The loan-linked cover was pure duplication. Always audit what the family already holds before adding more.

When it is weak value and you can reasonably skip it

The same logic in reverse tells you when to decline. Education loan insurance is poor value when the downside it covers is not actually catastrophic, or is already covered elsewhere.

- The loan is small and secured. On a ₹7 lakh loan backed by an FD or property, the bank already holds security worth the debt. A death does not leave the family exposed in the same way, and the collateral itself is a backstop.

- The co-applicant already holds adequate term life cover. A standalone term plan is almost always cheaper per rupee of cover than a loan-linked single-premium policy, and it does not shrink as you repay. If the existing cover comfortably exceeds the loan, buying more is waste.

- There are multiple earners in the household. If two parents earn, or the student has a working sibling who could co-carry the loan, one death does not end repayment capacity.

- The student has strong, near-certain post-study income. A funded PhD with a stipend, or an offer already in hand, changes the risk picture.

There is also a structural weakness in many loan-linked covers worth knowing. The sum assured is often “reducing”, meaning it falls as your outstanding balance falls. By year eight of a ten-year loan you have a small cover for which you paid a premium calculated partly on the full original amount. A separate level-term plan, by contrast, keeps its full sum assured the whole term and can be used for anything, not just this one loan. For many families, a clean term plan on the co-applicant is the better instrument, and the loan-linked policy is just the convenient one.

Convenience has a price. You are allowed to decide it is not worth paying.

How to handle the conversation at sanction time

You do not need to be combative about this. You need to be specific. Four questions, asked plainly, change the entire dynamic.

Ask whether it is mandatory. “Is this insurance an RBI requirement, or is it your bank’s policy?” The honest answer is always the second one. Note how readily they give it.

Ask for the premium as a separate line. Get the loan amount and the insurance premium written as two distinct numbers in the sanction letter, never merged into one “total.” If a lender resists separating them, that resistance is itself information.

Ask whose life is insured and what the term is. Confirm the cover sits on the co-applicant if the co-applicant is the earner. Confirm the policy term matches the loan tenure. A cover that lapses three years before the loan closes is a gap nobody mentions.

Ask whether you can decline or substitute. You can usually decline. You can also often satisfy the lender with an existing or freshly bought independent term plan assigned to the loan, which may be cheaper. If you decline on an unsecured NBFC loan, be ready for some friction, and decide in advance whether the rate and approval on offer are good enough to hold your ground for.

Before you even reach this conversation, two earlier decisions shape how exposed you are. Whether your loan is collateral-free at all is covered in the education loan without collateral guide, and who carries the file as co-applicant is covered in the co-applicant for an education loan post. Both feed directly into whether insurance is sensible for you.

Faz's ruleGet the loan and the premium written as two separate numbers. One merged figure is how a markup hides.

A single “total sanctioned” line lets the premium disappear into the noise. Two lines force the lender to own the price of the cover, and force you to actually look at it. Insist on the breakup before you sign anything.

Where insurance fits in the full cost of your loan

Education loan insurance is one line in a stack of costs, and it helps to see the stack. The interest rate is the largest cost by far. The moratorium structure is the second largest, because interest accrues and compounds while you study, a mechanic explained in detail in the education loan moratorium and interest post. Processing fees, documentation charges, and insurance sit below those.

That ordering matters because of where attention goes. A borrower who fights hard over a ₹60,000 insurance premium but does not check the moratorium capitalization, which can add several lakh to the principal, has optimised the small number and missed the big one. Insurance is worth getting right. It is not worth getting right at the expense of the rate and the moratorium math.

The other piece students forget is the document trail. The insurance certificate, the premium receipt, and the policy schedule are loan documents. Keep them with your sanction letter and disbursement records, the full list of which is in the documents required for an education loan post. If a claim ever has to be made, the family will need that policy schedule, and a claim is exactly the moment nobody wants to be hunting for paperwork.

The honest closing take

Education loan insurance is neither a scam nor a must-buy. It is a specific tool for a specific risk: the death or permanent disability of the person whose income holds the loan together. Whether you need it comes down to one honest sentence you have to finish for your own family. “If the co-applicant died during this loan, the family would…”

If the end of that sentence is “be financially ruined, because the loan is large, unsecured, and rests on one income with no other cover”, then buy it, and treat the roughly ₹1 lakh lifetime cost as the price of removing a real catastrophe. If the end of that sentence is “be fine, because the loan is small, or secured, or the co-applicant already has solid term cover”, then you are being sold convenience, and you are allowed to pass.

What you are never obliged to accept is the framing that it is compulsory, or a sanction letter that hides the premium inside a single merged number. Ask the four questions. Get the breakup in writing. Then make the call. It is your loan, your family’s exposure, and your decision to make with the real numbers in front of you.

FAQ

Is education loan insurance mandatory in India?

No. There is no RBI rule or IBA Model Education Loan Scheme provision that makes education loan insurance compulsory. It is an optional credit life cover. However, many private NBFCs that issue collateral-free abroad loans make it a de facto condition of approval, because they carry the full credit risk. You can technically decline, though on an unsecured loan declining may create some friction with the lender, so decide in advance how firm you want to be.

How much does education loan insurance cost?

The premium is typically 1% to 2% of the sanctioned loan amount, paid as a single one-time premium. On a ₹40 lakh loan at 1.5%, that is ₹60,000. The real cost is higher, because the premium is usually added to your principal, so you pay interest on it for the full loan tenure. On a 10-year loan, that interest can add another ₹42,000 to 50,000, taking the true lifetime cost of a ₹60,000 premium to roughly ₹1 lakh.

What does education loan insurance cover?

It clears your outstanding loan balance if the insured person, usually the borrower or the co-applicant, dies during the policy term. Most policies also cover permanent total disability on the same terms. Some policies include critical illness as an add-on, triggered by a defined list of serious conditions. It does not cover job loss, salary cuts, business failure, or general difficulty repaying. It is strictly a death-and-disability backstop, not an income-protection cover.

Can I refuse education loan insurance?

Yes, because it is not legally mandatory. On a collateral-backed loan from a public sector bank, declining is usually straightforward. On a collateral-free NBFC loan, the lender may push back, since the cover protects their risk. You can often satisfy them instead with an existing or new independent term life plan assigned to the loan, which is frequently cheaper. Get any agreement on this in writing in the sanction letter.

Is the insurance premium added to the loan amount?

In most cases, yes. Lenders rarely ask you to pay the premium out of pocket. They fold it into your sanctioned principal and disburse it directly to the insurer. This means the premium accrues interest for the entire loan tenure, exactly like your tuition. It is why the true cost of the cover is meaningfully higher than the headline 1% to 2% premium quoted to you at sanction time.

Is education loan insurance worth it for abroad studies?

Often yes, for the typical abroad-loan profile. These loans are large, frequently collateral-free, and usually rest on a single-earner parent as co-applicant. If that co-applicant has no separate term life cover, their death would leave the family with a ₹40 lakh-plus debt and no way to service it. In that situation the roughly ₹1 lakh lifetime cost is justified. It is weak value if the loan is small, secured, or the co-applicant already holds adequate term insurance.

Whose life should the insurance cover, the student or the parent?

It should cover whoever’s income actually carries the loan, which on a study-abroad loan is almost always the co-applicant parent, not the student. The student usually has little or no income at sanction time. If the loan rests on the parent’s earning capacity, the parent’s death is the real risk, so the cover should sit on the parent. Confirm this explicitly, since some policies default to the borrower only.

Is loan-linked insurance better than a regular term life plan?

Not usually. A standalone term plan on the co-applicant is generally cheaper per rupee of cover, keeps its full sum assured for the whole term, and can be used for any need, not just this one loan. Loan-linked cover often has a reducing sum assured that shrinks as you repay. Its only real advantage is convenience at sanction. If the family can arrange independent term cover, that is usually the stronger instrument.

Faz · The Honest Journey · 2026