An education loan for Canada from an Indian PSU bank sanctions up to around ₹1.5 crore with collateral, but the unsecured ceiling stays near ₹7.5 lakh at PSU banks and ₹60 lakh or more at NBFCs for strong programs. The distinctive part is the GIC, the Guaranteed Investment Certificate of CAD 20,635, that the study permit requires, and a good lender funds it inside the same sanction. A two-year college diploma or Master’s running CAD 35,000 to 55,000 is roughly ₹22 lakh to ₹34 lakh at ₹62 per Canadian dollar, so most families clear the PSU unsecured line and land in collateral or NBFC territory.

A neighbour’s son got into a two-year PG diploma in Toronto last year. He fixed the loan in his head as just tuition plus living, and then the visa checklist asked for proof of a GIC of over CAD 20,000 sitting in a Canadian account before he had even paid the first tuition installment. He had not budgeted that as a loan line. The bank could fund it, but only once he went back to the branch and got the sanction restructured to release a GIC tranche first. He lost three weeks he did not have.

This post is the loan-product picture for Canada, the funding angle. It is not a living-cost breakdown of life in Canada, and it is not a study guide. If you want the cost side or the admissions side, I link those below. Here I stay in the loan lane: how the sanction is built, how the GIC fits, and what a real INR example looks like.

For the wider picture on Canada beyond the borrowing: the USA vs Canada comparison and the UK vs Canada comparison.

How an education loan for Canada is actually structured

PSU banks treat Canada as a top-tier destination, the same bucket as the US, UK and Australia. The flagship products are SBI Global Ed-Vantage, Bank of Baroda’s Baroda Scholar for studies abroad, and Canara Bank’s overseas scheme, all of them built on the Indian Banks’ Association model. Union Bank and PNB run parallel products under the same framework.

For a Canadian program the sanction splits into three layers, and which layer you land in decides your interest rate, your collateral and your repayment runway.

- Up to ₹4 lakh: no margin, no collateral, no third-party guarantee. Almost no Canadian program fits here.

- Above ₹4 lakh to ₹7.5 lakh: parent co-applicant and usually a third-party guarantee, no tangible collateral. A one-year diploma might just touch this, but most do not.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory at PSU banks. This is where almost every two-year Canadian program lands.

A CAD 50,000 ticket is roughly ₹31 lakh, far above the unsecured line, so you are in collateral territory at a PSU bank unless you go to an NBFC. The broader ceiling picture across destinations sits in the maximum education loan amount in India post.

The GIC, and why Canada is different from every other loan

This is the single thing that makes a Canada loan different. The study permit requires you to prove you can support yourself, and the standard way Indian students do that is a Guaranteed Investment Certificate, a GIC. It is a fixed sum you deposit with a Canadian bank before you travel, and the bank releases it back to you in installments over your first year to cover living costs.

For 2024 to 2025, the required GIC amount rose to CAD 20,635, up sharply from the old CAD 10,000. That is roughly ₹12.8 lakh at ₹62 per Canadian dollar, sitting outside India before your course even starts. The official requirement is published by Immigration, Refugees and Citizenship Canada, and the broader study-permit guidance lives on canada.ca.

The honest implication is that the GIC is a chunk of money you need upfront, before any tuition tranche, and a good lender treats it as a fundable line inside the sanction rather than something you scramble to arrange separately. The detail of how the loan funds the certificate is in the dedicated GIC and Canada education loan post, so I keep it brief here and focus on how it shapes the sanction.

SDS versus non-SDS, and what it means for the loan

The Student Direct Stream, SDS, was the faster study-permit route that asked for a GIC, upfront tuition and an English test, in exchange for quicker processing. Canada closed SDS in late 2024, so every applicant now goes through the regular study-permit stream. The practical effect for your loan has not changed much: the GIC and the first-year tuition deposit are still the two upfront cash needs the lender has to fund early, whether or not SDS exists.

What matters for the sanction is the sequence. The lender sees the offer of admission, the tuition deposit the college asks for to confirm the seat, and the GIC requirement. A lender experienced with Canada structures the disbursement so the GIC and the confirmation deposit go out first, then the balance of tuition follows per the fee schedule. A lender that treats Canada like the US, where there is no GIC, can get the order wrong and leave you short at the visa stage.

Faz's ruleTell the bank the GIC requirement on day one, before the sanction is drawn up. The CAD 20,635 has to leave India before tuition does, so the disbursement order has to put it first or your visa proof is not ready in time.

Walk into the branch with the GIC figure written down and ask explicitly whether the sanction funds it and in what order. Many branch officers know the US I-20 flow well but have funded fewer Canada files. If they structure tuition first and GIC later, your study-permit proof of funds will not be ready when you need it, and you will be back restructuring the loan.

The worked INR sanction example for a CAD 50,000 program

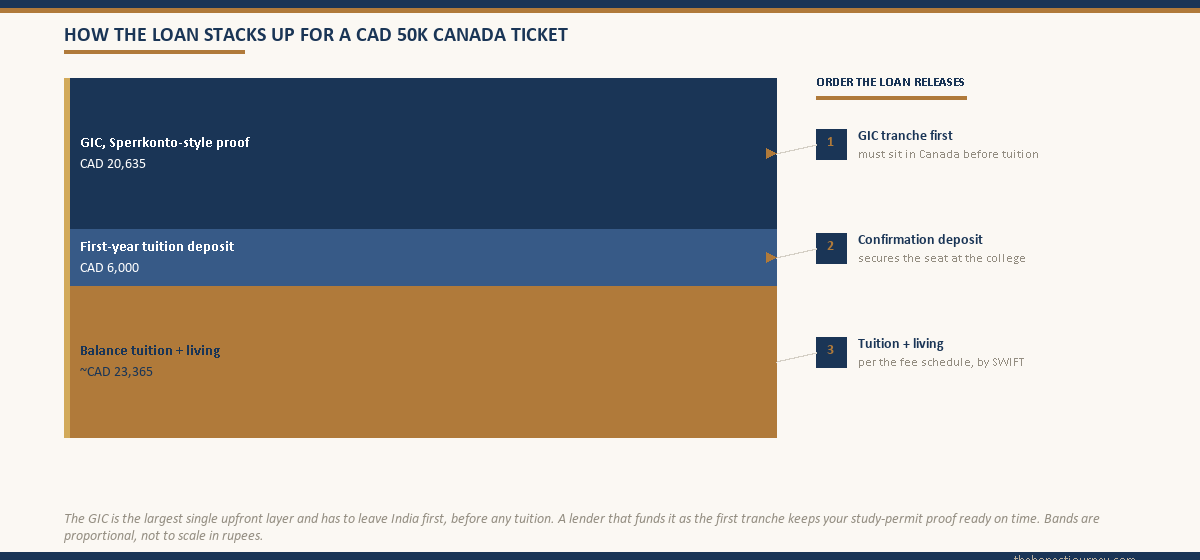

Take a realistic case. A student admitted to a two-year PG diploma at a public college in Ontario for the September intake. Total tuition over two years is CAD 30,000, and the student needs the GIC of CAD 20,635 plus an initial tuition deposit of CAD 6,000 to confirm the seat. Add living beyond the GIC and the headline funding need lands near CAD 50,000. At ₹62 per Canadian dollar, the tuition alone is ₹18.6 lakh, and the GIC is ₹12.8 lakh.

| Item | CAD | INR (at 62) |

|---|---|---|

| Tuition and fees (two years) | 30,000 | 18,60,000 |

| GIC (study-permit requirement) | 20,635 | 12,79,370 |

| First-year living beyond GIC, books, misc | ~9,365 | ~5,80,630 |

| Total funding need | ~60,000 | ~37,20,000 |

This student goes to SBI for a Global Ed-Vantage loan. The amount needed is roughly ₹37 lakh, well above the ₹7.5 lakh unsecured line, so tangible collateral is mandatory. The family pledges a residential property. SBI applies a valuation haircut, confirms a security value comfortably above the loan, and sanctions the full amount including the GIC tranche.

Now the margin money. For studies abroad, PSU banks ask for 10 to 15 percent margin on amounts above ₹4 lakh, contributed by the family alongside each disbursement rather than upfront in one go. On a ₹37 lakh loan at 15 percent margin, the family puts in roughly ₹5.6 lakh of its own across the schedule, and the bank funds the balance. Some banks fold a scholarship into the margin calculation, so confirm at the branch how yours is computed.

| Funding layer | INR | Notes |

|---|---|---|

| Total funding need | 37,20,000 | The sanction basis |

| Family margin (15 percent) | ~5,58,000 | Paid alongside disbursements |

| Bank-funded loan | ~31,62,000 | GIC tranche first, then tuition |

| Collateral pledged | Property, after valuation haircut | Mandatory above ₹7.5 lakh |

If the family had no property to pledge, the same case at an NBFC such as Avanse, HDFC Credila, Auxilo or InCred would mean an unsecured sanction of around ₹37 lakh against the parent’s income, typically needing a clean CIBIL above 750 and demonstrable repayment capacity, at an interest rate of 11.5 to 13.5 percent against SBI’s floating rate near 9.65 percent. Over a long repayment that spread is several lakh of extra interest. The honest economics of the unsecured route sit in the education loan for abroad studies without collateral post.

The sanction routes for Canada, side by side

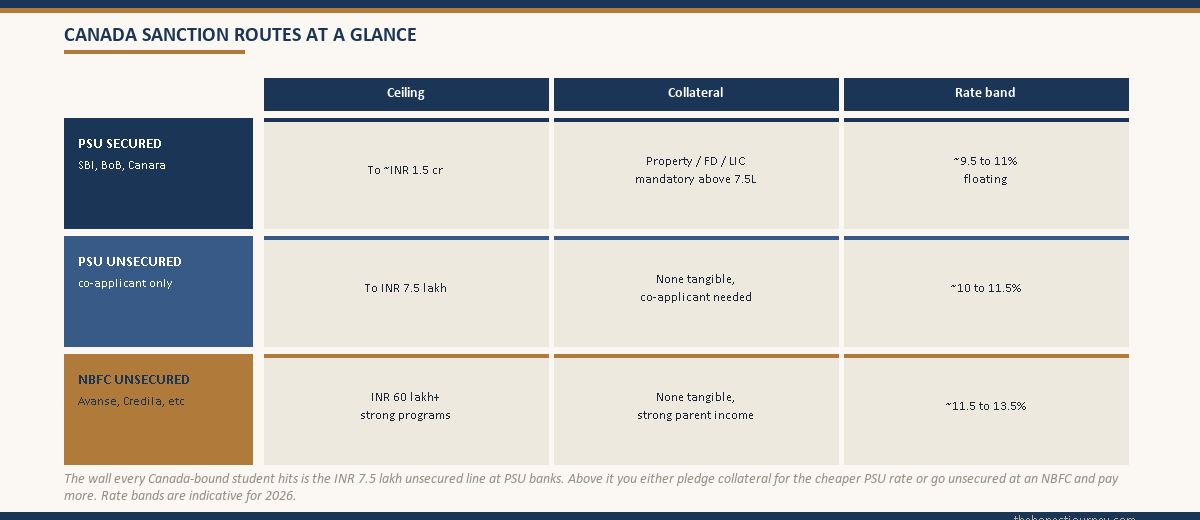

The wall every Canada-bound student hits is the same ₹7.5 lakh unsecured ceiling at PSU banks. A CAD 50,000 program is well past it, so the choice is the familiar one: pledge collateral and take the cheaper PSU rate, or go unsecured at an NBFC and pay more for the convenience.

| Route | Typical ceiling for Canada | Collateral | Rate band (2026) |

|---|---|---|---|

| PSU secured (SBI, BoB, Canara) | To around ₹1.5 crore | Property, FD or LIC mandatory above ₹7.5 lakh | ~9.5 to 11 percent floating |

| PSU unsecured | To ₹7.5 lakh | None tangible, co-applicant required | ~10 to 11.5 percent |

| NBFC unsecured | ₹60 lakh or more for strong programs | None tangible, strong co-applicant income | ~11.5 to 13.5 percent |

NBFCs lean on the college, the program and the earning potential. For a strong program at a well-regarded Canadian institution, an NBFC will sanction unsecured against a strong parent co-applicant, because their model bets on the graduate’s Canadian earning power and the post-study work permit. For a weaker college the unsecured appetite shrinks. PSU banks do not make that distinction; they want collateral above ₹7.5 lakh regardless of how the college ranks. The RBI sets the regulatory framework these lenders operate under, published on its site, and the model scheme PSU banks follow comes from the Indian Banks’ Association. The SBI product detail sits on the SBI education loans page.

The post-study work runway, honestly

The reason a family stomachs a ₹37 lakh loan for Canada is the Post-Graduation Work Permit, the PGWP. A graduate of an eligible program can work in Canada for a period tied to the program length, up to three years for longer programs, and that window is the repayment engine. A graduate earning a Canadian salary across that runway can service, and often prepay, a loan of this size in a way a short work window elsewhere cannot.

But the runway has real conditions attached, and they have tightened. PGWP eligibility now depends on the type of institution, the program and, for some streams, language requirements. A diploma at a college that does not meet the criteria may not yield a PGWP at all. So the honest framing is this: confirm the specific program is PGWP-eligible before you sign a ₹37 lakh sanction, because the whole repayment case rests on that work permit. If the program does not lead to a PGWP, the loan math is far weaker.

Faz's ruleConfirm the program is PGWP-eligible before you sign the sanction, not after you land. The post-study work permit is the entire repayment case for a Canadian loan, and the rules now turn on the institution and program type.

A two-year loan for Canada only repays comfortably if the graduate gets the work permit and a real Canadian salary. The eligibility rules have tightened, so a diploma that looked safe two years ago may not qualify today. Check the current criteria for your exact program, in writing, before the loan is drawn. If it does not yield a PGWP, shrink the ticket or pick a different program.

What banks check on Canada-specific paperwork at sanction

Beyond the standard income and KYC documents, a Canada sanction file leans on a few destination-specific items.

- The offer of admission or letter of acceptance from the designated learning institution, confirming the program and intake.

- The tuition fee structure for the full program, which the bank uses to size the tuition tranches.

- The GIC requirement, so the lender can fund the CAD 20,635 as the first disbursement.

- For collateralised loans, the property title documents and a valuation from the bank’s empanelled valuer.

- Co-applicant income proof, since even secured Canadian loans rely on the parent’s repayment capacity.

The point banks should scrutinise most, and the one inexperienced branches miss, is the disbursement order. A clean Canada file has the GIC tranche and the confirmation deposit going out first, before the bulk of tuition, so the proof of funds is ready for the study permit. A file structured tuition-first leaves you short at the visa stage.

The honest take on a Canada education loan

Canada works as a loan-funded destination when two things hold. One, the program leads to a Post-Graduation Work Permit, because the loan only repays comfortably on a real Canadian earning runway. Two, the lender funds the GIC and the confirmation deposit in the right order, so your study-permit proof of funds is ready on time. Get both right and a CAD 50,000 ticket is a serviceable loan.

What does not work is treating Canada as a soft, cheap default. The GIC rose to CAD 20,635, the unsecured PSU line is still only ₹7.5 lakh, and PGWP eligibility has tightened. A diploma at a college that does not yield a work permit, fully loan-funded at NBFC rates without collateral, is the combination that goes wrong. The loan is real money, the rate is high, and the earning runway may not exist.

Canada is a genuinely strong destination for Indian students, and the loan products fund it well. Just go in with the GIC budgeted, the PGWP confirmed, and the math redone against the real total funding need, not against tuition alone. If you want the living-cost side, the cost of studying in Canada post covers it, and the admissions side is in the study in Canada guide.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for Canada is in the Canada student visa guide.

FAQ

Can I get an education loan for Canada from Indian banks?

Yes. All major PSU banks, including SBI, Bank of Baroda, Canara, Union and PNB, cover Canada under their top-tier overseas education loan products, and NBFCs like Avanse, HDFC Credila, Auxilo and InCred fund it unsecured. PSU banks sanction up to around ₹1.5 crore with collateral and up to ₹7.5 lakh without tangible security. A good lender also funds the GIC requirement inside the same sanction, releasing it as the first tranche before tuition.

Does the education loan cover the GIC for Canada?

It can, and it should. The study permit requires a Guaranteed Investment Certificate of CAD 20,635 for 2024 to 2025, deposited with a Canadian bank before you travel, which is roughly ₹12.8 lakh. A lender experienced with Canada includes the GIC as a fundable line inside the sanction and releases it first, before tuition, so your proof of funds is ready for the visa. Tell the branch about the GIC on day one so the disbursement order is set correctly.

What is the maximum education loan for Canada?

PSU banks like SBI Global Ed-Vantage sanction up to around ₹1.5 crore for Canada, provided collateral and co-applicant income support the amount. The unsecured ceiling at PSU banks stays at ₹7.5 lakh, so anything above needs tangible security such as property, fixed deposit or LIC. NBFCs sanction unsecured loans up to ₹60 lakh or more for strong programs against a strong parent co-applicant, at higher interest rates and without the central interest subsidy.

Is collateral needed for a Canada education loan?

At PSU banks, yes, for almost every two-year Canadian program. The unsecured ceiling is ₹7.5 lakh, and a typical CAD 50,000 ticket runs to around ₹31 lakh, far above it, so any amount above ₹7.5 lakh needs tangible collateral such as property, fixed deposit or LIC. NBFCs sanction unsecured up to ₹60 lakh or more for strong programs against parent income and a clean CIBIL, but at higher interest rates than the PSU floating rate.

How much margin money is needed for a Canada loan?

For studies abroad, PSU banks ask for 10 to 15 percent margin money on the loan amount above ₹4 lakh. Margin is the family’s own contribution, paid alongside each disbursement rather than upfront, so on a ₹37 lakh loan at 15 percent you contribute roughly ₹5.6 lakh across the tranches. Some banks fold a scholarship or part-funding into the margin calculation, so confirm at the branch exactly how your margin is computed before you sign.

What is SDS and does it still apply?

The Student Direct Stream was a faster study-permit route that asked for a GIC, upfront tuition and an English test. Canada closed SDS in late 2024, so all applicants now use the regular study-permit stream. For your loan it changes little: the GIC and the first-year tuition deposit are still the two upfront cash needs the lender must fund early. The sequence of the disbursement, GIC and confirmation deposit first, matters more than the name of the stream.

Does the loan repay on the Post-Graduation Work Permit?

The Post-Graduation Work Permit is the repayment engine for a Canadian loan. A graduate of an eligible program can work in Canada for up to three years, and a Canadian salary across that window can service or prepay a loan of this size. Eligibility now turns on the institution, the program and sometimes language, so confirm your exact program is PGWP-eligible in writing before you sign the sanction. If it does not yield a work permit, the repayment math is far weaker.

Is a Canada loan worth it compared to a cheaper destination?

It depends on the program and the work runway. A two-year Canadian program funds at around ₹37 lakh once you include the GIC, so it makes sense mainly when the program is PGWP-eligible and the graduate can count on a real Canadian salary to repay. A diploma at a college that does not yield a work permit, fully funded at NBFC rates without collateral, is where the math breaks. Compare the total funding need, not just tuition, against the realistic earning window before committing.

Faz · The Honest Journey · 2026