An education loan for France splits hard along where you study. A French public university charges low tuition, often only a few hundred to a few thousand euros a year, so the loan mostly funds living costs and the proof-of-funds requirement of about EUR 615 a month. A Grande Ecole or private business school charges real tuition, often EUR 15,000 to EUR 40,000 a year, which pushes the loan above the ₹7.5 lakh unsecured PSU ceiling into collateral territory.

Two students I know went to France in the same year. One did a public-university Master’s in Lyon and borrowed a modest amount, mostly to satisfy the visa’s proof-of-funds rule and cover rent. The other got into a Grande Ecole business programme in Paris and took a loan five times larger, because the tuition alone ran past ₹25 lakh. Same country, completely different loans. That split is the single most important thing to understand before you apply, because the type of institution decides whether you are in the small-loan lane or the collateral lane.

This post is the loan-product picture for France, the funding angle. It is not an admissions guide or a tour of French student life. That broader picture sits in the study in France for Indian students post. Here I stay strictly in the loan lane.

For the wider picture on France beyond the borrowing: the cost of studying in France breakdown.

How an education loan for France is structured

PSU banks treat France as a standard overseas destination under the Indian Banks’ Association framework, the same one that covers Germany, the Netherlands and the rest of Europe. The products are the usual: SBI Global Ed-Vantage, Bank of Baroda’s Baroda Scholar, Canara Bank’s overseas scheme and the Union and PNB parallels. There is no France-specific product. The loan rides on the general studies-abroad scheme, and the sanction follows the familiar three layers.

- Up to ₹4 lakh: no margin, no collateral, no third-party guarantee. A public-university case might sit near here if living costs are modest.

- Above ₹4 lakh to ₹7.5 lakh: parent co-applicant and a third-party guarantee, usually no tangible collateral. Many public-university cases fit inside this band.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory at PSU banks. Every Grande Ecole case lands here.

This is why France is unusual. Depending on the institution, you can be a small unsecured borrower or a large collateral borrower. Few other destinations split this cleanly. The general ceiling picture across countries is in the maximum education loan amount in India post.

Public university versus Grande Ecole, the split that decides your loan

French public universities are state-funded, and tuition for them is set nationally at a low level. For non-EU students the published rates are higher than for EU students but still modest by international standards, typically a few thousand euros a year for a Master’s, and some universities apply lower rates. For a public-university Master’s, tuition is rarely the thing that drives the loan. Living costs and the visa proof-of-funds rule are.

Grandes Ecoles and private business and engineering schools are a different world. These are selective institutions outside the public university system, and they charge real, market-level tuition, often EUR 15,000 to EUR 40,000 a year for a business or management Master’s. For these the tuition alone can run ₹20 lakh to ₹35 lakh, which puts you firmly above the ₹7.5 lakh unsecured wall and into collateral territory at a PSU bank.

The application route for both runs largely through Campus France, the official body that processes Indian students applying to French institutions. The process, the recognised institutions and the procedures sit on the Campus France site. The bank does not require Campus France clearance to sanction, but the visa process does, so it runs in parallel with the loan.

Faz's ruleDecide which lane you are in before you walk into the bank. A public-university case is a small unsecured loan; a Grande Ecole case is a large collateral loan. Confusing the two wastes weeks at the branch.

Bring the admission letter that names the institution clearly. The bank sizes the loan to the tuition on it. A public university and a Grande Ecole produce loans that differ by a factor of five, so the institution type is the first thing the loan officer needs to see, not your nationality or your course name.

The EUR 615 a month proof-of-funds requirement

To get the French long-stay student visa, the VLS-TS, you must show you can support yourself, and the benchmark France uses is roughly EUR 615 a month, the level of the French student maintenance grant. Over a year that is about EUR 7,380 of living-cost proof you must demonstrate access to, separate from tuition. The official long-stay visa rules sit on the France-Visas site.

For the loan this matters the same way it does for any destination with a proof-of-funds rule. The bank can count the loan sanction toward your proof of funds, because an education loan from a recognised bank is accepted evidence. But it only counts if the sanction covers the living-cost figure on top of any tuition. For a public-university student, this proof-of-funds figure is often the main thing the loan is sized around, since tuition is so low. The mechanics of using a loan sanction as visa evidence are in the proof of funds for student visa post.

So for a public-university case, the loan is essentially a living-cost and proof-of-funds loan. For a Grande Ecole case, the loan is a tuition loan with the living-cost proof stacked on top. Both need the EUR 615 a month figure built in; they differ only in how much tuition sits above it.

The worked INR examples, public and Grande Ecole

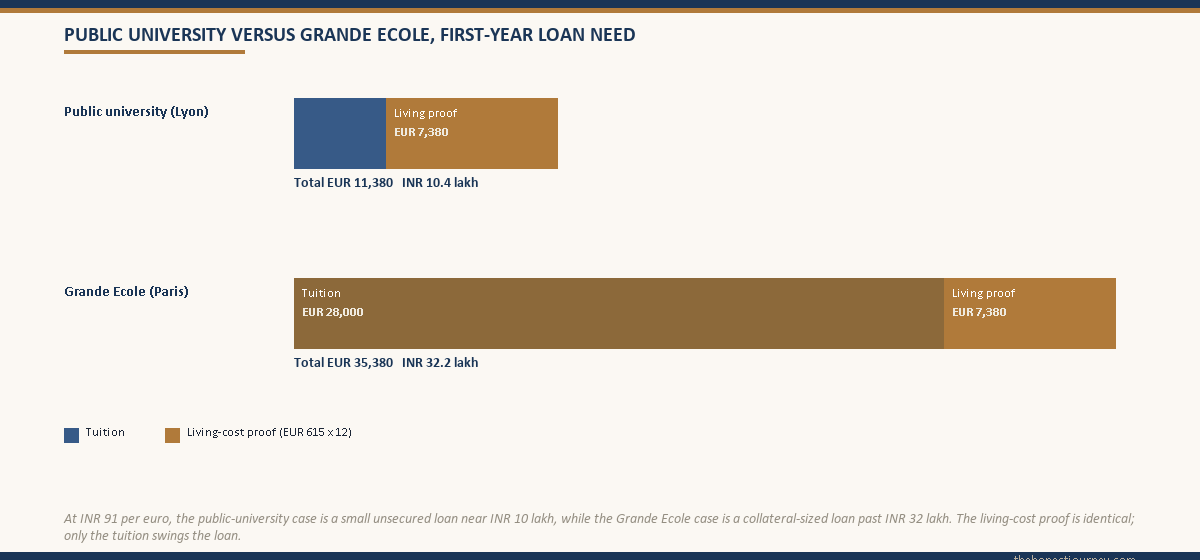

Take two real-shaped cases for the 2026 intake, both one-year Master’s programmes, at ₹91 per euro.

Case one, public university in Lyon. Tuition is EUR 4,000 for the year. The visa requires about EUR 7,380 of living-cost proof. The full first-year need is EUR 11,380, roughly ₹10.4 lakh.

| Item | EUR | INR (at 91) |

|---|---|---|

| Tuition (public university Master’s) | 4,000 | 3,64,000 |

| Living-cost proof (EUR 615 x 12) | 7,380 | 6,71,580 |

| Total first-year need, public | 11,380 | 10,35,580 |

This ₹10.36 lakh sits just above the ₹7.5 lakh unsecured ceiling, so a PSU bank would want some security for the portion above the wall, though a family can often manage with a modest collateral or by going to an NBFC unsecured for an amount this size. It is a small, manageable loan.

Case two, a Grande Ecole business school in Paris. Tuition is EUR 28,000 for the year. The living-cost proof is the same EUR 7,380. The full first-year need is EUR 35,380, roughly ₹32.2 lakh.

| Item | EUR | INR (at 91) |

|---|---|---|

| Tuition (Grande Ecole business Master’s) | 28,000 | 25,48,000 |

| Living-cost proof (EUR 615 x 12) | 7,380 | 6,71,580 |

| Total first-year need, Grande Ecole | 35,380 | 32,19,580 |

This ₹32.2 lakh is firmly in collateral territory at a PSU bank. The family pledges property, the bank applies a valuation haircut, confirms security above the loan, and sanctions. The margin money rule applies: 10 to 15 percent of the amount above ₹4 lakh, paid alongside disbursements. On a ₹32.2 lakh loan at 15 percent margin, the family contributes roughly ₹4.8 lakh across the schedule.

If the Grande Ecole family had no property, the same ₹32 lakh at an NBFC would be unsecured against parent income, needing a clean CIBIL above 750, at 11.5 to 13.5 percent versus a PSU floating rate near 9.65 percent. The honest economics of the unsecured route sit in the education loan for abroad studies without collateral post.

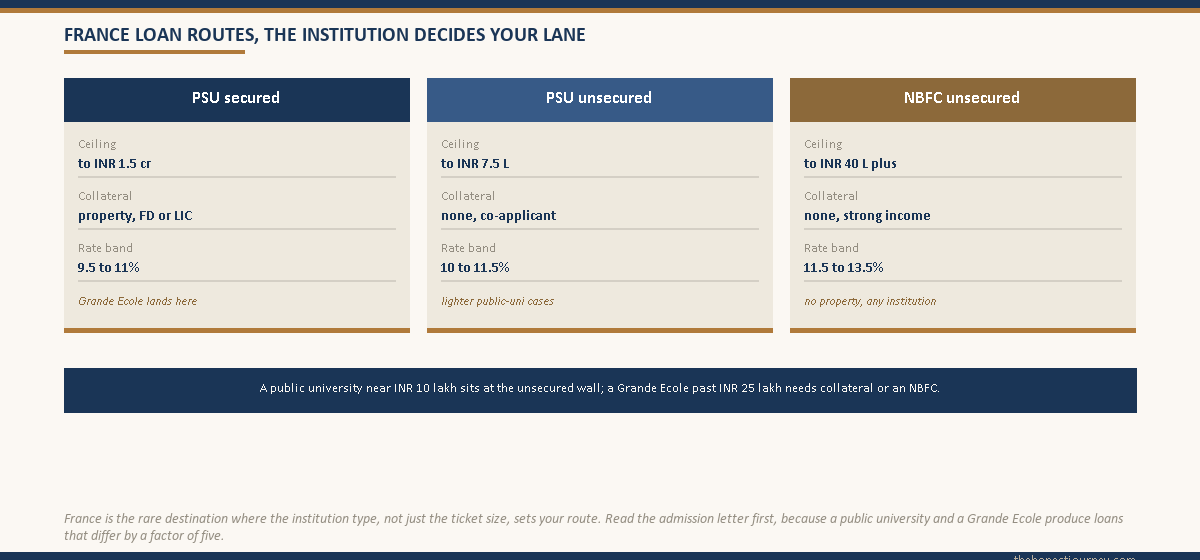

PSU versus NBFC for France, and where the wall is

The wall is the same ₹7.5 lakh unsecured ceiling at PSU banks. The difference with France is which side of the wall you land on depends entirely on your institution. A public-university student near ₹10 lakh is close to the wall and may manage with light security or an NBFC. A Grande Ecole student at ₹32 lakh is well past it and needs collateral or an NBFC unsecured loan at a higher rate.

| Route | Typical ceiling for France | Collateral | Rate band (2026) |

|---|---|---|---|

| PSU secured (SBI, BoB, Canara) | To around ₹1.5 crore | Property, FD or LIC mandatory above ₹7.5 lakh | ~9.5 to 11 percent floating |

| PSU unsecured | To ₹7.5 lakh | None tangible, co-applicant required | ~10 to 11.5 percent |

| NBFC unsecured | To ₹40 lakh or more for premier schools | None tangible, strong co-applicant income | ~11.5 to 13.5 percent |

NBFCs lean on the school’s ranking. A top Grande Ecole business school carries strong earning signals, so an NBFC will sanction unsecured generously against a strong parent co-applicant. A public-university programme draws a smaller unsecured appetite simply because the loan itself is smaller. PSU banks make no ranking distinction; they want collateral above ₹7.5 lakh regardless of where you study.

The post-study work runway, honestly

The reason a French loan repays is the post-study stay-back right. A Master’s graduate from a recognised French institution can apply for a temporary residence permit allowing a job search and, with a qualifying job offer, a transition to work, giving a runway of around one to two years to find and settle into employment. The current rules and permit types are on the Campus France site, since these change.

For a public-university case the small loan repays easily on almost any French graduate salary. For a Grande Ecole case the loan is large, so the math depends on the school being strong enough to place you into a salary that services ₹32 lakh. The honest framing: a Grande Ecole loan is worth it when the school’s placement record is genuinely strong, because the loan only repays on a real post-study salary. A weaker private school at Grande Ecole prices, fully loan-funded, is where the math breaks. The general advice on carrying enough buffer abroad is in the how much money to carry abroad post.

Faz's ruleA Grande Ecole loan is only as good as the school's placement record. The high tuition pushes you into collateral, so the loan only repays if the school reliably places graduates into salaries that service it.

A public-university loan in France is small and forgiving. A Grande Ecole loan is large and demands a school that actually delivers jobs. Before you sign a ₹30 lakh sanction for a private business school, look hard at its real placement numbers, not its brochure.

What banks check on French paperwork at sanction

Beyond the standard income and KYC documents, a French sanction file leans on a few destination-specific items.

- The admission letter from the institution, on letterhead, clearly naming whether it is a public university or a Grande Ecole, with the tuition stated.

- The fee structure, which the bank cross-checks against the tuition on the admission letter.

- Your statement of the living-cost proof figure, roughly EUR 615 a month, so the sanction is sized to cover it.

- For collateralised loans, the property title documents and a valuation from the bank’s empanelled valuer.

- Co-applicant income proof, since even secured loans rely on the parent’s repayment capacity.

The point banks scrutinise most for France is the institution type, because it determines the loan size and the collateral requirement. A clear admission letter that the loan officer can read at a glance prevents the most common delay, which is the bank misreading a Grande Ecole as a public university or the reverse.

The honest take on a French education loan

France works as a loan-funded destination in two very different ways. The public-university route is one of the most affordable in the world: low tuition, a small loan sized mostly around the EUR 615 a month proof of funds, easy to repay on a French graduate salary. The Grande Ecole route is a serious, collateral-sized loan that only makes sense when the school’s placement record genuinely justifies the tuition.

What does not work is paying Grande Ecole prices for a school that does not place, fully on a loan. That is the combination where a large French loan goes wrong. Decide your lane first, size the loan to tuition plus the EUR 615 a month proof, and for the Grande Ecole route, demand real placement numbers before you sign. France rewards the careful and punishes the brochure-led. Redo the math against your actual institution before signing the sanction letter, not after.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for France is in the France student visa guide.

FAQ

Can I get an education loan for France from Indian banks?

Yes. All major PSU banks, including SBI, Bank of Baroda, Canara, Union and PNB, cover France under their general studies-abroad education loan products, and NBFCs fund it unsecured. PSU banks sanction up to around ₹1.5 crore with collateral and up to ₹7.5 lakh without tangible security. France has no separate loan product; it rides on the same Indian Banks’ Association overseas scheme used across Europe, sized to your tuition plus the proof-of-funds requirement.

How much loan do I need for a Master’s in France?

It depends entirely on the institution. A public-university Master’s runs roughly EUR 11,000 to EUR 13,000 for the first year, tuition plus the EUR 615 a month living-cost proof, about ₹10 lakh to ₹12 lakh. A Grande Ecole business Master’s can run EUR 30,000 to EUR 45,000 for the year, around ₹27 lakh to ₹41 lakh. The public route is a small loan; the Grande Ecole route is a collateral-sized one.

What is the EUR 615 a month proof-of-funds requirement?

To get the French long-stay student visa, the VLS-TS, you must show you can support yourself, and France uses a benchmark of about EUR 615 a month, the level of the student maintenance grant. Over a year that is roughly EUR 7,380 of living-cost proof, separate from tuition. An education loan sanction from a recognised bank counts as accepted evidence of these funds, provided the sanction covers the living-cost figure on top of any tuition.

Why is a public university so much cheaper than a Grande Ecole?

French public universities are state-funded, with tuition set nationally at a modest level, typically a few thousand euros a year for non-EU students. Grandes Ecoles and private business and engineering schools sit outside the public system and charge market-level tuition, often EUR 15,000 to EUR 40,000 a year. The loan you need differs by a factor of five depending on which you attend, which is why the institution type is the first thing the bank checks.

Does collateral get needed for a French education loan?

For a public-university case near ₹10 lakh, you are close to the ₹7.5 lakh unsecured ceiling, so you may manage with light security or an NBFC unsecured loan. For a Grande Ecole case at ₹25 lakh to ₹40 lakh, you are well past the ceiling, so tangible collateral is mandatory at a PSU bank, or you take an NBFC unsecured loan at a higher rate against parent income. The institution decides the collateral requirement.

What is Campus France and does the bank need it?

Campus France is the official body that processes Indian students applying to French institutions, handling the application and pre-visa procedures. The recognised institutions and procedures sit on the Campus France site. The bank does not require Campus France clearance to sanction a loan, but the French visa process does, so it runs in parallel with the loan. Bring your admission letter to the bank; Campus France steps belong to the visa file, not the loan file.

What interest rate applies to a French education loan?

PSU banks charge a floating rate near 9.5 to 11 percent for studies abroad, linked to their external benchmark, and France is treated the same as any other destination. NBFCs charge 11.5 to 13.5 percent on unsecured loans. The PSU rate is lower but requires collateral above ₹7.5 lakh, while the NBFC rate is higher but needs no tangible security. For a small public-university loan the rate matters little; for a large Grande Ecole loan the gap compounds to several lakh.

Is a Grande Ecole loan worth it?

It depends on the school’s placement record. A Grande Ecole charges high tuition that pushes the loan into collateral territory at ₹25 lakh to ₹40 lakh, so the loan only repays if the school reliably places graduates into salaries that service it. A top Grande Ecole with strong placement justifies the loan; a weaker private school at similar prices, fully loan-funded, is where the math breaks. Demand real placement numbers before signing a large sanction.

Faz · The Honest Journey · 2026