An education loan for Ireland from an Indian PSU bank typically sanctions up to ₹1.5 crore for a Master’s, but the unsecured ceiling without collateral stays around ₹7.5 lakh at PSU banks and ₹40 to 50 lakh at NBFCs. Ireland’s total cost for a one-year taught Master’s runs EUR 25K to 45K including tuition (EUR 10K to 30K), living (EUR 12K to 15K), visa (EUR 300) and the IRP card (EUR 300). At ₹91 per euro, that’s ₹22.75 lakh to ₹41 lakh, which means most students need either collateral or a parent co-applicant with strong income to bridge the gap above ₹7.5 lakh.

A friend’s younger brother got into UCD for a Master’s in Data Analytics last August. He had a Canada offer too, but the PAL letter delay made him swing toward Dublin instead. By the time he landed, three things had surprised him: the rent reality, how long the IRP card actually takes to arrive, and the gap between his sanctioned loan amount and what the year actually cost.

This post is the loan-side picture I wish someone had handed him in May, before he signed the sanction letter and before he booked the flight.

Why Ireland moved up the list for Indian students after 2024

The UK Graduate Route got narrower in early 2024 (dependents banned for most taught Master’s, eligibility under review). Canada introduced the Provincial Attestation Letter cap and tightened post-graduation work permit rules for college programs. Australia raised proof-of-funds thresholds. Ireland sat quietly through all of it with its existing rules intact, an English-taught Master’s ecosystem, and the Third Level Graduate Programme that gives Master’s graduates 24 months of stay-back to find work.

For loan-funded students, Ireland’s appeal is concrete. The country is in the EU, the currency is the euro, the universities (Trinity College Dublin, UCD, UCC, Galway, Limerick, DCU, Maynooth) appear on every PSU bank’s approved list under their tier-1 Europe bucket, and the program length is usually 12 months for a taught Master’s. A shorter program means a smaller total cost than a two-year US or Canadian Master’s, which keeps the loan tighter.

What an education loan for Ireland actually covers

PSU banks treat Ireland the same way they treat Germany, France or the Netherlands: tier-1 Europe, eligible under their flagship overseas products. The two most relevant for Ireland are SBI Global Ed-Vantage and Bank of Baroda Baroda Vidya, with Canara Bank’s IBA Premier and Union Bank’s Special Education Loan filling in as alternatives.

The covered heads on a tier-1 Europe sanction usually include:

- Full tuition for the entire program duration.

- Living expenses up to a stated annual cap, often 20 to 30 percent of tuition.

- Health insurance premium (mandatory for the Irish visa).

- Visa application fee and the IRP registration fee.

- One return economy airfare per year.

- Laptop and study material against bills, capped.

- The proof-of-funds amount the visa officer requires you to show in your account before grant.

The last item matters more for Ireland than for most destinations. The Irish visa requires you to show EUR 10,000 in an account in your name before the visa is granted, separate from the tuition you have already paid. PSU banks handle this either by including it inside the sanction (released as living expenses tranche to your overseas account once opened) or by sanctioning it as a parked sum the family arranges short-term. The full visa-stage funds picture is in the proof of funds for student visa post.

The real cost math: tuition, living and the EUR 10K visa proof

Here is what a one-year Master’s at a Dublin university looked like in 2025 for a non-EU student, based on the fee pages published by the universities and the official cost-of-living guidance on educationinireland.com.

| Cost head | EUR range | INR at 91 per EUR |

|---|---|---|

| Tuition (Master’s, taught) | 10,000 to 30,000 | 9.10 lakh to 27.30 lakh |

| Accommodation (Dublin, 12 months) | 9,000 to 12,000 | 8.19 lakh to 10.92 lakh |

| Food and groceries | 2,400 to 3,600 | 2.18 lakh to 3.28 lakh |

| Transport (Leap Card student) | 400 to 600 | 36,400 to 54,600 |

| Health insurance (mandatory) | 150 to 300 | 13,650 to 27,300 |

| Visa fee (single entry D study) | 60 to 100 | 5,460 to 9,100 |

| IRP registration card | 300 | 27,300 |

| One-way flight, books, setup | 1,200 to 1,800 | 1.09 lakh to 1.64 lakh |

| Total one-year cost | 23,510 to 47,700 | 21.39 lakh to 43.40 lakh |

Two things to call out. Tuition at Trinity for a Master’s in Business Analytics is on the higher end (around EUR 23K to 25K for 2025 entry), while a Master’s in Computer Science at a regional university like Limerick or Maynooth sits closer to EUR 13K to 16K. The spread is wide. And Dublin rent is the single biggest variable. A student room in purpose-built accommodation runs EUR 900 to 1,100 a month; a shared house room outside the centre can drop to EUR 600 to 750.

Faz's rulePick your Irish university by tuition + city rent together, not tuition alone. Saving EUR 8,000 on fees gets eaten if you land in Dublin and pay EUR 4,000 extra on rent.

Trinity, UCD and DCU sit in Dublin, where one-bed and shared housing is the tightest in the country. UCC (Cork), UL (Limerick), Galway and Maynooth (just outside Dublin) all have meaningfully cheaper rent and shorter waitlists. The total cost gap between Dublin and a Tier-2 city can be EUR 4K to 6K a year, which is ₹3.6 to 5.4 lakh on the loan.

PSU sanction limits and where the math actually breaks

The PSU education loan products that cover Ireland follow the IBA framework on collateral and ceiling:

| Loan tier | Amount | Collateral required |

|---|---|---|

| Up to ₹4 lakh | Margin nil, no collateral, no third-party guarantee | None |

| Above ₹4 lakh to ₹7.5 lakh | Third-party guarantee, parent co-applicant | Often no tangible collateral |

| Above ₹7.5 lakh to ₹1.5 crore (Global Ed-Vantage tier) | Tangible collateral mandatory (property, FD, LIC) | Yes, at 100 percent of loan amount |

The wall most Ireland-bound students hit is right there. A Trinity Master’s costing EUR 40K total is ₹36.4 lakh. That sits firmly above the ₹7.5 lakh unsecured ceiling at PSU banks, which means you either bring tangible collateral (typically a property worth ₹36 to 40 lakh after the bank’s haircut) or you split the funding across a PSU loan up to ₹7.5 lakh and either family contribution or an NBFC top-up.

NBFCs (Avanse, HDFC Credila, Auxilo, InCred) sanction unsecured loans up to ₹40 to 50 lakh for Ireland against parent co-applicant income, but at interest rates 200 to 400 basis points higher than PSU floating rates, and without the CSIS subsidy benefit. The honest picture on NBFC versus PSU economics is in the education loan for abroad studies without collateral post.

Worked example: UCC Master’s, total cost vs PSU sanction

Take a real-shaped case. Student admitted to MSc Data Science at UCC, Cork, for September 2025. Tuition EUR 20,500. Estimated total one-year cost EUR 33,500.

| Item | EUR | INR (at 91) |

|---|---|---|

| Tuition (UCC, MSc Data Science) | 20,500 | 18,65,500 |

| Accommodation Cork (12 months, mid) | 8,400 | 7,64,400 |

| Food + groceries | 3,000 | 2,73,000 |

| Transport, health, books | 1,000 | 91,000 |

| Visa + IRP | 360 | 32,760 |

| Flight + setup | 1,300 | 1,18,300 |

| Total cost | 34,560 | 31,44,960 |

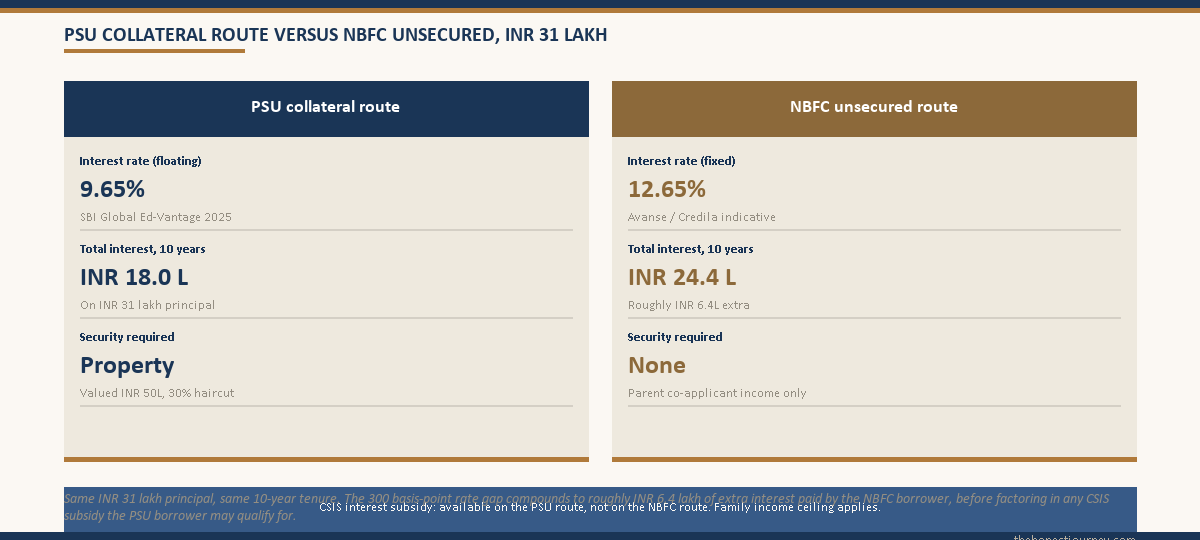

This student goes to SBI for a Global Ed-Vantage loan. SBI sanctions the full ₹31.45 lakh, but because the amount is above ₹7.5 lakh, collateral is mandatory. The family pledges a residential property valued at ₹50 lakh (SBI applies a 30 percent haircut, so the security value the bank counts is ₹35 lakh, comfortably above the loan).

Tuition is wired EUR 20,500 to UCC’s bank account in two tranches (or one full payment) via SWIFT. The EUR 10,000 visa proof requirement is met by the family parking funds short-term in the student’s account, then replaced after visa grant by the living-expenses tranche from SBI once the student lands and opens an Irish bank account.

If the family had no property to pledge, the same case at an NBFC would mean an unsecured sanction of around ₹32 lakh against the parent’s income (typically needing CTC of ₹12 to 15 lakh and a clean CIBIL above 750), at an interest rate of 12 to 13.5 percent versus SBI’s 9.65 percent floating. Over a 10-year repayment, that 300 basis point gap on ₹32 lakh is roughly ₹6 to 7 lakh of extra interest.

The Stamp 2 work-right and what it actually pays

Non-EU students on a long-stay D study visa in Ireland get Stamp 2 conditions on their IRP card. The rules from citizensinformation.ie are clear:

- 20 hours of paid work per week during term time.

- 40 hours per week during the official holiday periods (June to September and 15 December to 15 January).

- Work permitted on a regular employment contract, no need for a separate work permit.

The minimum wage in Ireland in 2025 is EUR 13.50 per hour. That’s the floor, not the ceiling. Student-friendly jobs (retail, hospitality, supermarket, campus roles) typically pay EUR 13.50 to 15.50 an hour. Tech-adjacent part-time work (internships, paid teaching assistant roles) can pay EUR 18 to 25 an hour.

At 20 hours a week of minimum-wage work during the 8 to 9 months of term, plus 40 hours a week through the summer, a focused student can realistically earn EUR 11,000 to 14,000 across the year before tax. After PAYE and PRSI deductions (Ireland’s tax credits absorb most of the lower band), take-home tends to land around EUR 10,000 to 12,500. That comfortably covers accommodation in a non-Dublin city, or about 60 to 70 percent of Dublin rent.

What it does not cover is tuition. Don’t model your loan on work-income offset for tuition. The loan should fund the program fully. Treat work income as buffer for unexpected costs (medical, travel home, the rent-deposit gap when you switch accommodation in month four), not as a tuition substitute.

Faz's ruleDon't bank on Stamp 2 work earnings during your first month in Ireland. The IRP card takes weeks to arrive, and most employers won't put you on payroll until it does.

The visa-vignette in your passport gets you into the country. The IRP card (the physical residence permit) is what employers actually want to see, along with your PPS number. Both take 4 to 8 weeks after arrival. Plan to fund the first two months entirely from your loan’s living-expenses tranche and family buffer.

The IRP card and PPS number: timing the bank cares about

After you land in Ireland on the visa vignette, two registrations matter, and both are slower than students expect.

The IRP (Irish Residence Permit) is the physical card issued by the Department of Justice through the GNIB process. It replaces the older GNIB card system. You book an online appointment via inis.gov.ie, attend in person with your passport, visa, college letter, proof of address and EUR 300 fee, and the card arrives by post in 4 to 8 weeks. Until it arrives you cannot legally start most jobs.

The PPS (Personal Public Service) number is your tax and social insurance ID. You apply at MyWelfare.ie after you have an Irish address. It also takes 2 to 6 weeks. Employers and banks ask for it.

This timing matters for the loan because the second tranche from your Indian bank usually goes to your Irish bank account for living expenses, and the Irish bank account opening needs proof of address plus often the PPS or IRP. So the practical sequence is: land, find accommodation, get an address letter, apply PPS, open Irish bank account (most banks accept the proof-of-address documents from accommodation provider), ask Indian bank to release the living expenses tranche to the Irish account, register for IRP. The whole sequence is 4 to 10 weeks.

What banks check on Ireland-specific paperwork at sanction

For an Irish university Master’s, the documents that go into the sanction file beyond the standard ones include:

- The unconditional Letter of Acceptance from the Irish university, on letterhead, signed by the admissions office.

- The fee structure document showing tuition for the program year and any installment plan offered.

- Proof that the university is recognised by Quality and Qualifications Ireland (QQI) and that the program is on the Interim List of Eligible Programmes if applicable.

- The cost-of-living estimate, either from the university’s own documentation or from educationinireland.com’s published guidance.

- For collateralised loans, the property documents and valuation that the bank’s empanelled valuer signs off on.

The point banks scrutinise most is the gap between the sanctioned amount and the visa proof requirement. The Irish visa officer wants to see EUR 10,000 in an account in the student’s name, ideally for at least 28 days before the visa application, in addition to evidence the tuition is paid or fully funded by the loan. PSU banks know this and will issue a separate sanction letter confirming the full loan amount along with a covering letter stating the loan covers tuition and living expenses, which the visa officer accepts in lieu of cash in account if the family cannot park EUR 10K separately.

The honest take on Ireland as a loan-funded destination

Ireland works well as a one-year, focused, English-taught Master’s destination for an Indian student with PSU loan funding, provided two things hold. One, the family can either pledge collateral for amounts above ₹7.5 lakh or stomach the higher NBFC rate. Two, the student treats the 24-month post-study work window as the actual ROI window, not a fallback.

The Third Level Graduate Programme gives Master’s graduates 24 months on Stamp 1G after course completion to find work in Ireland. With a degree from a recognised Irish university and the local tech and pharma job market (Google, Meta, Pfizer, Stripe, Salesforce all have Dublin offices), graduates in software, data, fintech and pharma have a defensible path. Outside those fields the market is thinner, and graduates often pivot to roles in the UK or back home after the 24 months.

What does not work is treating Ireland as a back-door cheap path to Europe. Tuition at top Irish universities is now within shouting distance of UK fees. The savings come from the shorter program (one year vs two), the right to work 20 hours during term, and the post-study work visa, not from any structural cost advantage. If your loan math only works because you assumed Ireland is the cheap option, redo the math before signing the sanction letter.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for Ireland is in the Ireland student visa guide.

FAQ

What is the maximum education loan for Ireland from Indian banks?

SBI Global Ed-Vantage and BoB’s overseas product both sanction up to ₹1.5 crore for tier-1 Europe destinations including Ireland, provided collateral and co-applicant income support the amount. The unsecured ceiling at PSU banks stays at ₹7.5 lakh; anything above needs tangible security (property, FD or LIC). NBFCs like Avanse and HDFC Credila sanction unsecured loans up to ₹40 to 50 lakh for Ireland against parent co-applicant income, but at higher interest rates than PSU banks.

Do Indian banks sanction loans for Ireland Master’s programs?

Yes. All major PSU banks (SBI, Bank of Baroda, Canara, Union, PNB) cover Ireland under their tier-1 Europe overseas education loan products. Universities like Trinity College Dublin, UCD, UCC, NUI Galway, University of Limerick, DCU and Maynooth sit on every bank’s approved list. The bank checks that the program is at QQI-recognised institution and that the Letter of Acceptance is unconditional. The full maximum education loan amount in India post covers the limits in detail.

Is Ireland approved by SBI Global Ed-Vantage?

Yes. Ireland is on SBI’s tier-1 Europe approved-country list for Global Ed-Vantage, which is the product designed for overseas Master’s and PhD programs at amounts above ₹7.5 lakh. The approved-university list within Ireland covers the seven public universities and the major Institutes of Technology that have been redesignated as Technological Universities (TU Dublin, Munster TU, Atlantic TU). Private colleges sit on a separate review track and need branch-level confirmation before you apply.

How much proof of funds do I need to show for an Ireland student visa?

The Department of Justice requires non-EU students applying for a long-stay D study visa to show EUR 10,000 in an account in the student’s name, in addition to evidence that the first year’s tuition is paid in full or sanctioned by an education loan. The EUR 10K is intended to demonstrate living-expense capacity for the first year. PSU banks usually issue a covering letter confirming the sanctioned amount includes living expenses, which the visa officer accepts in place of the EUR 10K cash balance.

Can I work part time in Ireland on a student visa?

Yes. Non-EU students on a D study visa get Stamp 2 conditions, which permit 20 hours of paid work per week during term time and 40 hours per week during the official holiday periods (June to September and 15 December to 15 January). The minimum wage in 2025 is EUR 13.50 per hour, so a focused student can earn EUR 11,000 to 14,000 across the year. The right to work is confirmed on the IRP card, which arrives 4 to 8 weeks after registration.

How long does the IRP card take to arrive in Ireland?

The IRP (Irish Residence Permit) card is issued by the Department of Justice after the in-person GNIB appointment. You book the appointment via inis.gov.ie, attend with your passport, visa vignette, college letter, proof of address and the EUR 300 fee. The physical card is posted to your address within 4 to 8 weeks of the appointment. Until the card arrives, most employers will not put you on payroll, so plan to fund the first two months entirely from loan tranches.

What’s the total cost for a one-year Master’s in Ireland for an Indian student?

Total one-year cost ranges from EUR 23,500 to EUR 47,700 depending on university and city. Tuition runs EUR 10,000 to 30,000, Dublin accommodation EUR 9,000 to 12,000, food and groceries EUR 2,400 to 3,600, transport EUR 400 to 600, mandatory health insurance EUR 150 to 300, visa and IRP EUR 360, flight and setup EUR 1,200 to 1,800. In INR at 1 EUR equals 91, that’s roughly ₹21.4 lakh to ₹43.4 lakh. Cork, Galway and Limerick run cheaper than Dublin on rent.

Is a collateral-free education loan possible for Ireland?

Up to ₹7.5 lakh from PSU banks without tangible collateral, but you still need a parent co-applicant. Beyond that, NBFCs (Avanse, HDFC Credila, Auxilo, InCred) sanction unsecured loans up to ₹40 to 50 lakh for Ireland against co-applicant income, typically requiring parent CTC of ₹12 to 15 lakh and clean CIBIL above 750. Interest rates run 200 to 400 basis points higher than PSU floating rates, and you lose access to the CSIS interest subsidy. The trade-off is real and worth modelling on a 10-year repayment.

Faz · The Honest Journey · 2026