An education loan for New Zealand from an Indian PSU bank typically sanctions up to around ₹1.5 crore for a Master’s with collateral, while the unsecured ceiling without tangible security stays at ₹7.5 lakh at PSU banks and runs higher at NBFCs. New Zealand is a smaller ticket than the US, with most programmes landing between NZD 35,000 and NZD 50,000 for tuition plus living, roughly ₹18 lakh to ₹26 lakh at ₹51 per New Zealand dollar.

A friend’s younger brother went to Auckland for a Master’s in Information Technology in 2024. He had assumed New Zealand would be a small, easy loan because the country itself felt low-key compared to the US and the UK that everyone around him was chasing. He was half right. The ticket was genuinely smaller. What caught him off guard was the living-cost proof the visa demanded, a fixed NZD figure per year that the bank had to be told about clearly, because it sits on top of the tuition and the bank does not assume it for you.

This post is the loan-product picture for New Zealand, the funding angle. It is not a cost-of-living tour or a ranking of universities. If you want the broader picture of student life and admissions, that sits in the study in New Zealand for Indian students post. Here I stay in the loan lane.

For the wider picture on New Zealand beyond the borrowing: the cost of studying in New Zealand breakdown.

How an education loan for New Zealand is structured

PSU banks treat New Zealand as a real overseas destination under the same Indian Banks’ Association framework they apply to Australia, Canada and the UK. The products are the familiar ones: SBI Global Ed-Vantage, Bank of Baroda’s Baroda Scholar, Canara Bank’s overseas scheme, plus the Union Bank and PNB parallels. None of them carries a separate New Zealand product. It rides on the general studies-abroad scheme.

The sanction structure splits into the same three layers that decide your rate, your collateral and your repayment runway.

- Up to ₹4 lakh: no margin, no collateral, no third-party guarantee. No New Zealand programme fits inside this.

- Above ₹4 lakh to ₹7.5 lakh: parent co-applicant and a third-party guarantee, usually no tangible collateral. Below most New Zealand tickets.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory at PSU banks. This is where almost every New Zealand Master’s lands.

Because a typical New Zealand Master’s runs ₹18 lakh to ₹26 lakh all in, you are above the ₹7.5 lakh unsecured wall at a PSU bank, so collateral is usually in play. The general ceiling picture across destinations is laid out in the maximum education loan amount in India post.

The offer of place is the sanction input, not the visa

For New Zealand the bank works off the offer of place from the institution, plus the tuition fee on that offer, plus the published living-cost figure the visa requires. There is no single all-in cost document the way the US I-20 bundles everything. The bank assembles the picture from two pieces: the tuition on your offer of place, and the living-cost proof the immigration rules set.

The offer of place is the formal admission document from a New Zealand university or institute. It states the programme, the duration and the annual tuition. The bank reads the tuition straight off it. What the bank does not automatically know, and what you must surface, is the living-cost component, because that is set by immigration, not by the university.

Faz's ruleTell the bank the living-cost proof figure up front, in writing, when you apply. It sits on top of the tuition on your offer of place, and if you leave it out the sanction comes back too small to cover the visa requirement.

The university offer shows tuition only. The NZD living-cost figure is an immigration rule, not a university charge, so the bank will not add it unless you ask. Bring both numbers to the branch on day one so the sanction covers tuition and the proof-of-funds requirement together.

The NZD 20,000 a year living-cost proof

This is the piece that makes a New Zealand loan different from a UK one. To get the student visa, you must show you can meet living costs, and Immigration New Zealand sets a fixed figure for this: NZD 20,000 for a full year of study, or NZD 1,667 a month for shorter courses. This is a proof-of-funds requirement, money you must demonstrate access to, separate from and on top of your first-year tuition. The official rule sits on the Immigration New Zealand site.

For the loan, this matters in two ways. First, the bank can count the loan sanction toward your proof of funds, because an education loan from a recognised bank is accepted evidence of funds for the visa. Second, the bank only counts it if the sanction is large enough to cover both tuition and the living-cost figure, which is why you must build the NZD 20,000 into your loan ask, not just the tuition. The mechanics of how a loan sanction serves as visa evidence are covered in the proof of funds for student visa post.

A common mistake is to apply for a loan that covers only tuition, then discover at visa time that you have nothing to show for living costs. The fix is simple but has to happen early: ask for a sanction that covers tuition plus at least NZD 20,000 of living costs, so the sanction letter itself satisfies the proof-of-funds test.

The worked INR sanction example for a Master’s in New Zealand

Take a real-shaped case. Student admitted to a one-year taught Master’s in Information Technology at a New Zealand university for the 2026 intake. The offer of place shows tuition of NZD 38,000 for the year. The visa requires NZD 20,000 of living-cost proof. So the full first-year funding need is NZD 58,000. At ₹51 per New Zealand dollar, that is about ₹29.6 lakh.

| Item | NZD | INR (at 51) |

|---|---|---|

| Tuition (one-year Master’s) | 38,000 | 19,38,000 |

| Living-cost proof (visa requirement) | 20,000 | 10,20,000 |

| Total first-year funding need | 58,000 | 29,58,000 |

This student goes to a PSU bank. The ₹29.58 lakh sits well above the ₹7.5 lakh unsecured ceiling, so tangible collateral is mandatory. The family pledges a residential property. The bank applies a haircut on the valuation, confirms the security value comfortably exceeds the loan, and sanctions the full amount. Crucially, because the sanction covers both tuition and the NZD 20,000 living-cost figure, the sanction letter doubles as the proof-of-funds evidence for the visa.

Now the margin money. For studies abroad, PSU banks ask for 10 to 15 percent margin on the loan amount above ₹4 lakh, contributed by the family alongside each disbursement, not upfront in one lump. On a ₹29.58 lakh loan at 15 percent margin, the family puts in roughly ₹4.4 lakh of its own across the schedule, and the bank funds the balance.

| Funding layer | INR | Notes |

|---|---|---|

| Total first-year funding need | 29,58,000 | Tuition plus living-cost proof |

| Family margin (15 percent) | ~4,44,000 | Paid alongside disbursements |

| Bank-funded loan | ~25,14,000 | Disbursed per the schedule |

| Collateral pledged | Property after haircut | Above the loan value |

If the family had no property to pledge, the same case at an NBFC would mean an unsecured sanction of around ₹30 lakh against the parent’s income, typically needing a clean CIBIL above 750, at an interest rate of 11.5 to 13.5 percent versus a PSU floating rate near 9.65 percent. Over a long repayment that spread costs several lakh more in interest. The honest economics of the unsecured route sit in the education loan for abroad studies without collateral post.

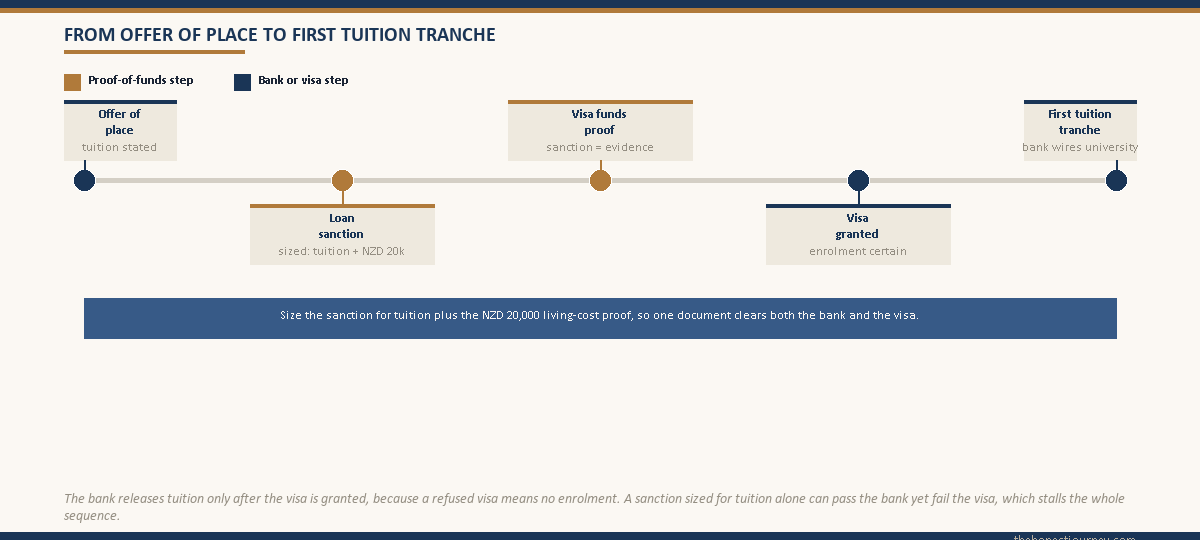

From offer of place to first disbursement

The sequence for New Zealand follows a clean order, and knowing it keeps you from missing the tuition deadline. You receive the offer of place. You apply for the loan, building in the NZD 20,000 living-cost figure. The bank sanctions, and the sanction letter becomes part of your visa file as proof of funds. You apply for the student visa using the offer, the sanction and your other documents. Once the visa is granted, the bank disburses the first tuition tranche to the university.

The reason the bank waits for the visa before releasing tuition is the same everywhere: a refused visa means no enrolment, so the bank does not wire tuition into a course that may not happen. This is why the proof-of-funds piece matters so much. A sanction that covers only tuition can still clear the bank, but it may not clear the visa, and then nothing disburses at all. The disbursement mechanics in detail are in the education loan disbursement process post.

Faz's ruleA sanction that covers only tuition can pass the bank and still fail the visa. Build the living-cost proof into the loan amount so the sanction letter satisfies both the bank and Immigration New Zealand in one document.

The bank cares that the security covers the loan. Immigration cares that you can fund living costs. A single sanction sized for tuition plus NZD 20,000 satisfies both, which is cleaner than scrambling for a separate bank balance to show at visa time. Size the loan once, correctly, at the start.

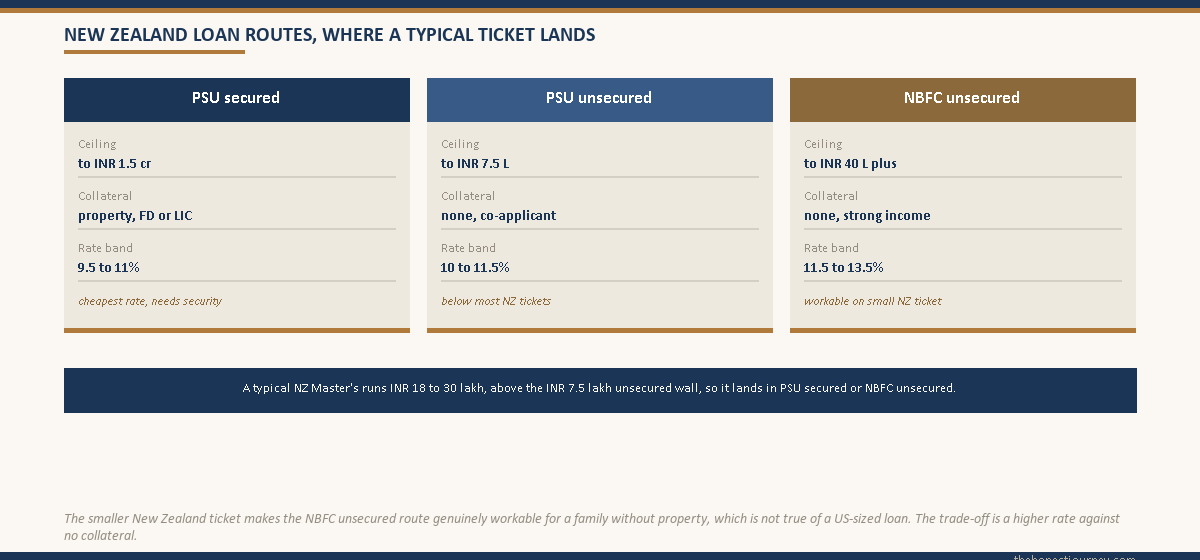

PSU versus NBFC for New Zealand, and where the wall is

The wall every New Zealand-bound student meets is the same ₹7.5 lakh unsecured ceiling at PSU banks. Since a New Zealand Master’s runs ₹18 lakh to ₹30 lakh all in, you are above that wall, so the choice is the familiar one: pledge tangible collateral and take the cheaper PSU rate, or go unsecured at an NBFC and pay more.

| Route | Typical ceiling for NZ | Collateral | Rate band (2026) |

|---|---|---|---|

| PSU secured (SBI, BoB, Canara) | To around ₹1.5 crore | Property, FD or LIC mandatory above ₹7.5 lakh | ~9.5 to 11 percent floating |

| PSU unsecured | To ₹7.5 lakh | None tangible, co-applicant required | ~10 to 11.5 percent |

| NBFC unsecured | To ₹40 lakh or more for strong cases | None tangible, strong co-applicant income | ~11.5 to 13.5 percent |

New Zealand’s smaller ticket actually helps the NBFC case here. A ₹30 lakh unsecured loan is more comfortable for an NBFC to underwrite than a ₹75 lakh US ticket, so a family without collateral has a genuine option, just at a higher rate. PSU banks make no such distinction by ticket size; they want collateral above ₹7.5 lakh regardless. The official guidance on studying in New Zealand, including the institutions recognised for student visas, sits on the government’s Study with New Zealand site.

The post-study work runway, honestly

The reason a New Zealand loan repays is the post-study work right. A graduate of an eligible qualification at degree level or above can apply for a post-study work visa, generally giving up to three years of open work rights depending on the level and where you studied. That window is the repayment runway, and three years is enough to service a ₹25 lakh to ₹30 lakh loan on a New Zealand graduate salary if you live carefully and prepay.

The honest caveat is that the runway is shorter and the salaries lower than the US for tech roles, so the math only works because the loan is smaller. A ₹30 lakh New Zealand loan against three years of work is a reasonable bet. The same logic would not survive a US-sized ticket. Keep the loan proportionate to the realistic earning window, and check the current post-study work rules on the Immigration New Zealand site before you commit, because these rules change.

Faz's ruleNew Zealand works as a loan-funded destination precisely because the ticket is small. Do not let a smaller loan tempt you into a programme that does not give the post-study work right, because that right is the whole repayment plan.

A three-year post-study work visa is what turns a ₹30 lakh loan into a serviceable one. Confirm your qualification is eligible at the level you are studying before you sign the sanction. A loan without the work right behind it is a loan with no repayment engine.

What banks check on New Zealand paperwork at sanction

Beyond the standard income and KYC documents, a New Zealand sanction file leans on a few destination-specific items.

- The offer of place from the institution, on letterhead, confirming the programme, duration and tuition.

- The fee structure, which the bank cross-checks against the tuition on the offer of place.

- Your statement of the living-cost proof figure, NZD 20,000 a year, so the sanction is sized to cover it.

- For collateralised loans, the property title documents and a valuation from the bank’s empanelled valuer.

- Co-applicant income proof, since even secured loans rely on the parent’s repayment capacity.

The point banks scrutinise most is whether the sanction is sized to cover the full first-year need, tuition plus living-cost proof, because a sanction that covers only tuition creates a problem at visa time, not at sanction time. Get the sizing right at the branch and the rest of the file is routine.

The honest take on a New Zealand education loan

New Zealand works as a loan-funded destination when two things hold. One, the programme gives you the post-study work right, because that three-year window is the repayment runway. Two, you size the loan to cover tuition plus the NZD 20,000 living-cost proof from the start, so the sanction letter clears both the bank and the visa.

What does not work is treating New Zealand as the cheap option and under-sizing the loan. A sanction that covers tuition alone leaves you scrambling for living-cost evidence at visa time, and the smaller ticket can lull a family into skipping the careful sizing that the destination actually rewards. New Zealand is forgiving on ticket size and unforgiving on proof of funds. Plan for both before you sign the sanction letter, not after.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for New Zealand is in the New Zealand student visa guide.

FAQ

Can I get an education loan for New Zealand from Indian banks?

Yes. All major PSU banks, including SBI, Bank of Baroda, Canara, Union and PNB, cover New Zealand under their general studies-abroad education loan products, and NBFCs fund it unsecured. PSU banks sanction up to around ₹1.5 crore with collateral and up to ₹7.5 lakh without tangible security. New Zealand has no separate loan product; it rides on the same Indian Banks’ Association overseas scheme used for Australia and Canada, sized to your tuition plus the living-cost proof.

How much loan do I need for a Master’s in New Zealand?

A one-year taught Master’s in New Zealand typically runs NZD 35,000 to NZD 50,000 for tuition plus the NZD 20,000 living-cost proof, so the first-year funding need lands around NZD 55,000 to NZD 70,000. At ₹51 per New Zealand dollar that is roughly ₹28 lakh to ₹36 lakh. Size your loan to cover both tuition and the living-cost figure, not tuition alone, so the sanction letter also satisfies the visa proof-of-funds requirement.

What is the NZD 20,000 living-cost requirement?

Immigration New Zealand requires student visa applicants to show they can meet living costs, set at NZD 20,000 for a full year of study or NZD 1,667 a month for shorter courses. This is a proof-of-funds requirement separate from and on top of tuition. An education loan sanction from a recognised bank counts as accepted evidence of these funds, but only if the sanction is large enough to cover both tuition and the living-cost figure, which is why you must build it into your loan ask.

Does collateral get needed for a New Zealand loan?

At PSU banks, usually yes. The unsecured ceiling is ₹7.5 lakh, and a New Zealand Master’s runs well above that at ₹18 lakh to ₹30 lakh all in, so any amount above ₹7.5 lakh needs tangible collateral such as property, fixed deposit or LIC. NBFCs sanction unsecured against parent income and a clean CIBIL, but at higher interest rates. The smaller New Zealand ticket makes the NBFC route more workable than it is for larger US-sized loans.

Can the loan sanction serve as proof of funds for the visa?

Yes. An education loan sanction from a recognised bank is accepted as evidence of funds for a New Zealand student visa, covering both tuition and living costs. The condition is that the sanction must be large enough to cover the full first-year need, tuition plus the NZD 20,000 living-cost figure. A sanction sized for tuition alone can clear the bank but may fail the visa, so size the loan to satisfy both in one document from the start.

What interest rate applies to a New Zealand education loan?

PSU banks charge a floating rate near 9.5 to 11 percent for studies abroad, linked to their external benchmark, and this applies to New Zealand the same as any other destination. NBFCs charge 11.5 to 13.5 percent on unsecured loans. The PSU rate is lower but requires collateral above ₹7.5 lakh, while the NBFC rate is higher but needs no tangible security. Over a long tenure the rate gap compounds to several lakh of extra interest on the NBFC route.

How does the post-study work visa affect repayment?

A graduate of an eligible qualification at degree level or above can apply for a post-study work visa giving up to three years of open work rights, depending on the level and study location. That window is the repayment runway. Three years of New Zealand graduate income can service a ₹25 lakh to ₹30 lakh loan if you live carefully and prepay. Confirm your qualification is eligible for the work right before committing, since the rules change.

Is New Zealand cheaper than the US or UK for a loan?

Generally yes on ticket size. A New Zealand Master’s at ₹18 lakh to ₹30 lakh all in is smaller than a two-year US Master’s, which often runs ₹50 lakh or more. The smaller loan is easier to service and makes the unsecured NBFC route more workable. The trade-off is a shorter, lower-paying earning window than US tech roles, so the math works precisely because the loan stays proportionate to the realistic post-study salary.

Faz · The Honest Journey · 2026