An education loan for the Netherlands from an Indian bank usually funds both tuition and living, because Dutch tuition for non-EU students runs in two bands: a low statutory rate near EUR 2,500 a year for a few cases, and an institutional rate of roughly EUR 8,000 to EUR 20,000 a year for most Master’s. A typical one-year Master’s lands around EUR 18,000 to EUR 25,000 all in, which is roughly ₹16 lakh to ₹23 lakh at ₹91 per euro, well inside what a PSU bank with collateral, or an NBFC unsecured, will sanction.

A friend’s younger sister went to a research university in the Netherlands for a one-year Master’s last year. She nearly applied for the wrong loan amount because the university website quoted the statutory tuition fee on one page and the much higher institutional fee on another, and nobody had told her that as a non-EU student she pays the institutional one. The two numbers were almost EUR 6,000 apart. She fixed it before signing, but only because someone caught it.

This post is the loan-product picture for the Netherlands, the funding angle. It is not a cost-of-living breakdown of Dutch cities. If you want the broader picture of life and study there, the study in Netherlands for Indian students post covers it. Here I stay in the lane of how the loan is built.

For the wider picture on the Netherlands beyond the borrowing: the cost of studying in the Netherlands breakdown.

A loan sanction will not help you bring your family here. Dutch family reunification measures payroll income, not funds. See why the income floor blocks most students.

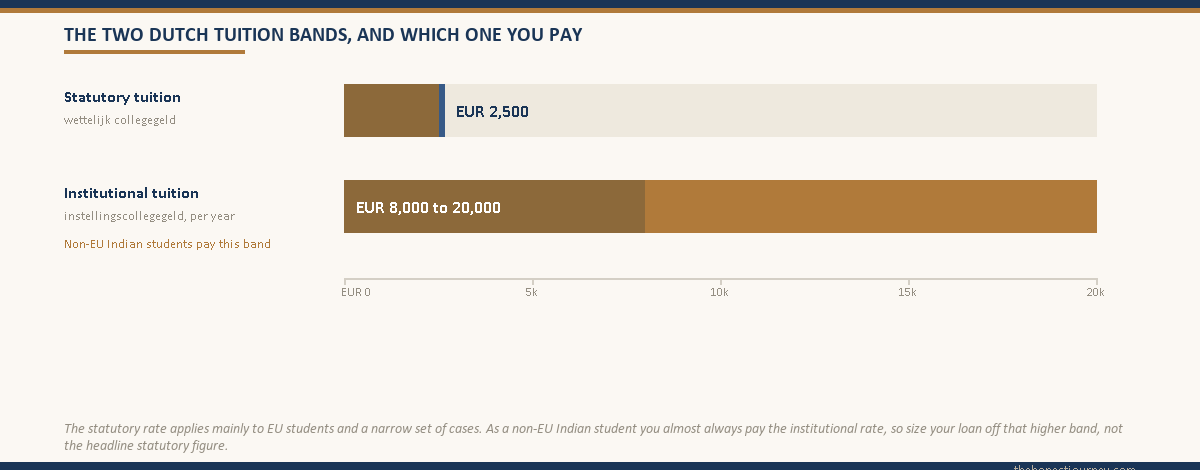

Why Dutch tuition comes in two bands, and why it matters for the loan

The single thing that trips up most families is the two-tier tuition system. Dutch public universities publish two fee figures, and which one applies to you decides the size of your loan.

- Statutory tuition (wettelijk collegegeld): a government-set rate, around EUR 2,500 a year for 2025-26. It applies mainly to EU and EEA students, and to a narrow set of non-EU cases.

- Institutional tuition (instellingscollegegeld): set by each university, typically EUR 8,000 to EUR 20,000 a year for non-EU Master’s, higher for some specialised or business programs. This is what most Indian students pay.

So when you read a Dutch university fee page, find the institutional rate for non-EU students. That figure, plus living costs, is what the bank sanctions against. The official explanation of the two fee types sits on the Dutch government portal at government.nl, and the immigration side, including the entry-visa funds requirement, is on the immigration service site ind.nl.

For the loan, the practical consequence is this. Unlike Germany, where public tuition is near zero and the loan mostly funds a blocked account, in the Netherlands the institutional tuition is a real, sizable number. The loan funds tuition and living together, so the ticket is larger than Germany but smaller than a two-year US Master’s.

Faz's ruleRead the institutional fee, not the statutory fee, when you size your loan for the Netherlands. As a non-EU Indian student you almost always pay the higher institutional rate, and sizing the loan off the statutory number leaves you short.

Open the university’s fee page and look specifically for the non-EU or institutional rate. The two numbers can differ by several thousand euros. If your loan is sanctioned against the wrong figure, you are scrambling for a top-up in the weeks before the program starts.

How the loan is structured for a Dutch Master’s

PSU banks place the Netherlands in their standard overseas tier. The product framework is the same Indian Banks’ Association model that governs every abroad loan, so the structure splits by amount, and which band you fall into decides your collateral and rate.

- Up to ₹4 lakh: no margin, no collateral. No Dutch Master’s fits here.

- Above ₹4 lakh to ₹7.5 lakh: parent co-applicant and a guarantee, usually no tangible collateral. Below most Dutch tickets.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory at PSU banks. This is where almost every Dutch Master’s lands.

A one-year Dutch Master’s at roughly EUR 18,000 to EUR 25,000 all in is ₹16 lakh to ₹23 lakh, comfortably above the ₹7.5 lakh unsecured ceiling. So the same fork as everywhere else applies: pledge collateral and take the cheaper PSU rate, or go unsecured at an NBFC and pay more. The general ceiling picture across destinations is laid out in the maximum education loan amount in India post, and the honest economics of skipping collateral are in the education loan for abroad studies without collateral post.

One detail in the Netherlands favours the borrower: it is mostly a one-year Master’s destination. A one-year ticket is structurally smaller than a two-year US program, so the loan is more often within reach of a modest collateral pledge, and the repayment runway starts a year sooner.

The worked INR sanction example for a Dutch Master’s

Take a real-shaped case. Student admitted to a one-year MSc at a Dutch research university for September 2025. The institutional tuition for non-EU students is EUR 16,000. The university and the immigration service estimate living costs at roughly EUR 12,000 for the year. At ₹91 per euro, the total is ₹25.48 lakh.

| Item | EUR | INR (at 91) |

|---|---|---|

| Institutional tuition (one year) | 16,000 | 14,56,000 |

| Living costs (one year) | 12,000 | 10,92,000 |

| Total program cost | 28,000 | 25,48,000 |

This student goes to a PSU bank for an overseas education loan. The bank can sanction the full ₹25.48 lakh, but because the amount is above ₹7.5 lakh, tangible collateral is mandatory. The family pledges a fixed deposit and a small residential property; after the bank’s valuation haircut the security value sits comfortably above the loan, and the bank sanctions.

Now the margin money. For studies abroad, PSU banks ask 10 to 15 percent margin on amounts above ₹4 lakh, contributed by the family alongside each disbursement rather than upfront. On a ₹25.48 lakh loan at 15 percent, the family puts in roughly ₹3.8 lakh across the disbursement schedule, and the bank funds the balance.

| Funding layer | INR | Notes |

|---|---|---|

| Total program cost | 25,48,000 | The sanction ceiling |

| Family margin (15 percent) | ~3,82,000 | Paid alongside disbursements |

| Bank-funded loan | ~21,66,000 | Disbursed per the fee schedule |

| Collateral pledged | FD plus property | After valuation haircut |

If the family had no collateral, the same case at an NBFC would mean an unsecured sanction of around ₹25 lakh against the parent’s income, typically needing a clean CIBIL above 750, at an interest rate of 11.5 to 13.5 percent versus a PSU floating rate near 9.5 to 11 percent. Over a repayment of several years, that spread is a few lakh of extra interest. For a one-year ticket of this size, the gap between secured and unsecured is smaller in absolute rupees than it is for a US program, which is worth weighing honestly.

The entry visa and proof of funds for the Netherlands

Most Indian students need an entry visa called the MVV (machtiging tot voorlopig verblijf, the provisional residence authorisation) together with a residence permit. The university usually applies for both on your behalf through the immigration service. The piece that touches the loan is the proof of funds.

The immigration service requires evidence that you can cover your living costs and tuition for the first year. The amount is set roughly in line with the official student living-cost norm, around EUR 1,100 to EUR 1,200 a month for 2025-26, which the university converts into a year’s figure you must show. Your sanctioned loan plus the family contribution can serve as this proof, and a bank sanction letter is the document that demonstrates it. How a sanction letter functions as proof of funds for any student visa is covered in the proof of funds for student visa post.

A practical point: many Dutch universities ask you to transfer the first-year tuition, or a substantial deposit, plus sometimes the living-cost amount, into a university or escrow account before they file the MVV application. So the disbursement of your loan has to be timed to that deadline, not to the program start date. Plan the sanction early enough that the first tranche can move when the university asks for it.

Faz's ruleTime your first loan disbursement to the university's MVV funding deadline, not to the September start date. Dutch universities often want the tuition and living-cost proof transferred months before the program begins, and a late tranche can stall your visa.

Ask the admissions office the exact date and amount they need before they file your MVV. Then work backwards: the sanction, the collateral valuation and the first disbursement all have to land ahead of that date. Build in a few weeks of slack.

How disbursement works for a Dutch loan

For a one-year Master’s the disbursement is simpler than a multi-year program. Tuition is usually billed once for the year, or in two instalments, and living costs are released to the student in tranches. The bank wires tuition directly to the university by SWIFT, and releases the living-cost portion to the student or a designated account on a schedule.

Because the Netherlands often needs the funds transferred early for the MVV, the first and largest tranche, the tuition, tends to move well before you fly. The mechanics of how the bank actually moves money to a foreign university are in the education loan disbursement process post. The key thing for the Netherlands is that the early MVV funding requirement front-loads the disbursement, so your loan needs to be sanction-ready earlier than the calendar might suggest.

The student also pays some costs out of pocket before any tranche helps: the visa and residence-permit fees, the flight, and the first month’s accommodation deposit, which in Dutch cities can be steep because rooms are scarce. Treat these as a family buffer, the same way you would for any destination.

Post-study work: the orientation year and the repayment runway

The reason a Dutch loan repays sensibly is the post-study work right. After finishing your degree, you can apply for the zoekjaar, the orientation year (officially the residence permit for the orientation year for highly educated persons). It gives you up to one year to look for work or start a business in the Netherlands, and during it you can work without a separate work permit. If you find a qualifying job, you can move onto a work-based residence permit.

So the runway is the one-year orientation period plus whatever employment follows. For a one-year Master’s costing ₹25 lakh, that is a workable repayment engine: a graduate in a Dutch tech, engineering or business role can service the loan, and the ticket is smaller than the two-year US equivalent, so the loan-to-earning ratio is healthier. The honest caveat is that the orientation year is a window to find work, not a guarantee of it, and Dutch jobs in some fields expect at least conversational Dutch. Model your repayment on landing a job within the orientation year, and treat anything beyond as a buffer, not the base case.

Faz's ruleSize a Dutch loan so it repays on an orientation-year job, not on a five-year Dutch career you have not started. The zoekjaar gives you a year to find work, which is real, but it is a window, not a promise.

A one-year Dutch Master’s at ₹20 to 25 lakh is serviceable on a single qualifying job found during the orientation year, especially if you prepay in the early years. If your repayment plan only works assuming long-term Dutch employment you have not secured, shrink the loan or reconsider the program.

PSU versus NBFC for the Netherlands

The fork is the familiar one. The ₹7.5 lakh unsecured ceiling at PSU banks sits well below a Dutch Master’s ticket, so you either pledge collateral for the cheaper PSU rate or borrow unsecured at an NBFC for more.

For the Netherlands specifically, two things tilt the decision. First, the ticket is smaller than a US program because it is usually one year, so the absolute rupee cost of the higher NBFC rate is smaller, which makes the unsecured route less punishing if you lack collateral. Second, the early MVV funding deadline rewards whichever lender can sanction and disburse faster for your situation; sometimes that is an NBFC, sometimes a PSU branch you already bank with. Weigh speed against rate, not rate alone.

The framework these lenders follow comes from the RBI and the IBA model scheme. Neither sets the Dutch sanction amount; the ceiling comes from each bank’s product policy and your collateral. The institutional tuition you read off the university page, plus the living-cost norm, is the number everything else is built on.

The honest take on a Netherlands education loan

The Netherlands works as a loan-funded destination when the program is a one-year Master’s with real labour-market value, and when you have read the institutional tuition correctly so the loan is sized right. The ticket is moderate, the orientation year gives a fair repayment runway, and the one-year length means you start earning, and repaying, sooner than a two-year program elsewhere.

What goes wrong is sizing the loan off the statutory tuition by mistake, or treating the orientation year as a guaranteed job. Get the institutional fee right, time the disbursement to the MVV deadline, and model repayment on a job found within the orientation year. Do that, and a Dutch Master’s is one of the more sensibly sized loans in this whole batch. Redo the math against the institutional fee and the living-cost norm before you sign the sanction letter, not after.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for the Netherlands is in the Netherlands student visa guide.

FAQ

Can I get an education loan for the Netherlands from Indian banks?

Yes. All major PSU banks (SBI, Bank of Baroda, Canara, Union, PNB) cover the Netherlands under their overseas education loan products, and NBFCs fund it unsecured. PSU banks sanction up to around ₹1.5 crore with collateral, and up to ₹7.5 lakh without tangible security. The loan funds both institutional tuition and living costs, since Dutch tuition for non-EU students is a real, sizable figure rather than near zero. Size the loan off the institutional fee, not the statutory one.

How much does a Master’s in the Netherlands cost an Indian student?

A one-year Dutch Master’s typically costs roughly EUR 18,000 to EUR 25,000 all in, combining institutional tuition of EUR 8,000 to EUR 20,000 with living costs around EUR 12,000 a year. At ₹91 per euro that is roughly ₹16 lakh to ₹23 lakh. Business and some specialised programs cost more. Always confirm the institutional, non-EU tuition rate on the university’s own fee page, because the lower statutory rate does not apply to most Indian students.

What is the difference between statutory and institutional tuition?

Statutory tuition (wettelijk collegegeld) is a government-set rate, around EUR 2,500 a year, applying mainly to EU and EEA students and a narrow set of non-EU cases. Institutional tuition (instellingscollegegeld) is set by each university, typically EUR 8,000 to EUR 20,000 a year, and is what most non-EU Indian students pay. Sizing your loan off the wrong band can leave you several thousand euros short, so confirm which rate applies to you before applying.

Is collateral needed for a Netherlands education loan?

At PSU banks, usually yes. The unsecured ceiling is ₹7.5 lakh, and a Dutch Master’s at ₹16 lakh to ₹23 lakh runs above it, so any amount above ₹7.5 lakh needs tangible collateral such as property, fixed deposit or LIC. NBFCs sanction unsecured against parent income and a clean CIBIL, at higher rates. Because a Dutch ticket is usually one year, the absolute rupee gap between secured and unsecured is smaller than for a two-year US program.

How do I show proof of funds for the Dutch student visa?

The immigration service requires evidence you can cover tuition and living costs for the first year, roughly in line with the living-cost norm of about EUR 1,100 to EUR 1,200 a month. Your sanctioned loan plus family contribution can serve as this proof, and a bank sanction letter is the document that demonstrates it. The university usually applies for the MVV entry visa and residence permit on your behalf, and often asks for the tuition and funds to be transferred before filing.

When does the loan get disbursed for a Dutch program?

Often earlier than the program start date. Dutch universities frequently require the first-year tuition, plus sometimes the living-cost proof, to be transferred before they file the MVV application, which can be months before September. So the first tranche, usually the tuition wired by SWIFT to the university, tends to move early. Time your sanction and first disbursement to the university’s funding deadline, not to the calendar start of the course.

Can I work after my Master’s in the Netherlands to repay the loan?

Yes. After finishing, you can apply for the zoekjaar, the orientation year, which gives up to one year to find work or start a business, and during it you can work without a separate permit. If you land a qualifying job, you move onto a work-based residence permit. A one-year Master’s costing around ₹25 lakh is serviceable on a job found during the orientation year, though some Dutch roles expect conversational Dutch, so factor that into your plan.

Is a Dutch Master’s loan smaller than a US one?

Usually, yes. Most Dutch Master’s programs are one year, so the loan covers one year of tuition and living, whereas a US Master’s is often two years and shows the full two-year cost on the I-20. A Dutch ticket of ₹16 lakh to ₹23 lakh is materially smaller than a US ticket near ₹50 lakh, and the one-year length means you start earning and repaying a year sooner. That smaller, shorter loan is part of why the Netherlands can be a sensible choice.

Faz · The Honest Journey · 2026